|

市場調査レポート

商品コード

1636485

中国のEVバッテリーアノード:市場シェア分析、産業動向・統計、成長予測(2025~2030年)China Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のEVバッテリーアノード:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

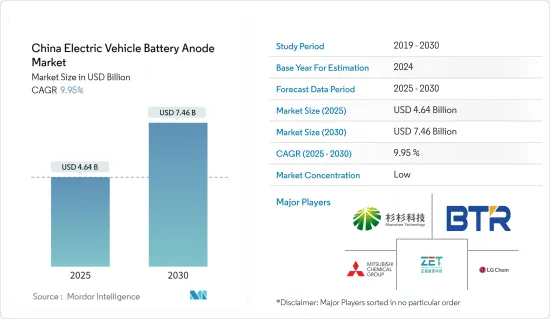

中国のEVバッテリーアノードの市場規模は2025年に46億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは9.95%で、2030年には74億6,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、電池製造に対する政府の支援政策と投資、リチウムイオン電池の価格低下が予測期間の市場を牽引するとみられます。

- 一方、アノード材料の製造コストが高いことが、今後の市場成長を抑制すると予想されます。

- とはいえ、アノード材料と効率的な電解質に関する継続的な調査と進歩は、市場成長の機会を提供する可能性があります。

中国のEVバッテリーアノードの市場動向

リチウムイオン電池タイプが大きなシェアを占める見込み

- 当初、リチウムイオン電池は主に携帯電話やパソコンなどの家電製品に電力を供給していました。しかし、リチウムイオン電池の用途は大幅に拡大し、中国ではハイブリッド車や完全電気自動車(EV)の主要な動力源となっています。この移行は、主にCO2や窒素酸化物などの温室効果ガスを排出しないEVの環境上の利点によって推進されています。

- リチウムイオン電池はエネルギー密度が高く、費用対効果に優れ、効率的であるため、電気自動車(EV)に好まれる選択肢となっています。このような採用の増加は、製造工程におけるアノード材料の需要増加に拍車をかけています。

- さらに、リチウムイオン材料のコストが低下していることも、電気自動車用リチウムイオン電池製造の需要増加の大きな理由となっています。2023年には、リチウムイオン電池パックの価格は前年比14%減の139米ドル/kWhになります。電池価格の下落に伴い、EVはより手頃な価格となり、電気自動車の普及と市場シェアの拡大が進みます。この需要の急増は、負極を含む電池部品の消費量の増加を促し、電池性能を向上させるための技術進歩を促進します。

- 今後、技術革新によって電気自動車のリチウムイオン電池の効率が向上すると同時に、負極材の需要も増加すると予測されます。

- 例えば、2024年4月、中国の電気自動車メーカーであるContemporary Amperex Technology Co.は、電気自動車用のリン酸鉄リチウム(LFP)電池を発売しました。この新しい電池のエネルギー密度は1kgあたり205Whで、このような電池の現在の技術水準より8%近く高いです。このような開発により、予測期間中にEV用リチウムイオン負極材の需要が高まると予想されます。

- さらに、中国工業情報化部の監督下で策定された「自動車産業グリーン・低炭素開発ロードマップ1.0」によると、中国の乗用車用新エネルギー車(NEV)の電気自動車販売台数は、2025年までにシェア50%に達すると予想されています。このようなロードマップは、中国におけるEV負極製造にも未来的なチャンスをもたらすと期待されています。

- このように、電気自動車におけるリチウムイオン電池の使用の増加と価格の低下により、リチウムイオン電池負極セグメントは予測期間中に大きく成長すると予想されます。

電池製造に向けた政府の政策と投資が市場を牽引する見込み

- 政府による支援政策と電池製造への多額の投資の組み合わせが、中国の電気自動車用電池製造を後押ししており、これがEVバッテリーアノードの需要を押し上げると予想されます。政府は直接的な財政支援、税制優遇措置、補助金を提供し、メーカーのコストを削減し、先端設備への投資を奨励しています。中国の電気自動車メーカーは政府補助金の恩恵を受けています。例えば、航続距離が400kmを超えるオール・エレクトリック・プラグイン・カーには、12,600人民元(約2,000米ドル)の補助金が支給されます。一方、航続距離が300~400kmの車には9,100人民元(約1,400米ドル)の補助金が支給されます。

- さらに、同国の電気自動車需要の増加は、電気自動車用バッテリー製造プロジェクトへの投資を促進し、EVバッテリーアノード材の潜在的なニーズを生み出しています。国際エネルギー機関(IEA)によると、2023年の中国の電気自動車用電池需要は417GWhで、昨年の314GWhから増加しています。

- さらに、電気自動車の販売台数の増加は、電池製造会社が電気自動車用電池の生産にさらに投資する動機付けとなっており、それによってEVバッテリーアノード材料の需要が創出されています。国際エネルギー機関(IEA)によると、2023年のEV車販売台数は810万台で、2022年の590万台を上回る。

- 今後、同国では電気自動車の製造が急ピッチで進められており、EVバッテリー製造への投資が拡大するため、EVバッテリー用負極材の需要は増加すると予想されます。例えば、中国は2024年5月、電気自動車を駆動する次世代電池技術を開発するために8億4,500万米ドルを投資すると発表しました。このような投資は、予測期間における電気自動車用バッテリー製造の需要を押し上げると思われます。

- このように、政府の支援政策と電池製造への投資は市場を牽引すると予想されます。

中国のEVバッテリーアノード産業の概要

中国のEVバッテリーアノード市場は半分裂状態です。市場の主要企業(順不同)には、上海杉杉科技、BTR新材料グループ、江西正都新能源科技、三菱化学グループ、LG化学グループなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 電池製造に向けた政府の政策と投資

- 電池原材料コストの低下

- 抑制要因

- 負極材の高い製造コスト

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- バッテリータイプ別

- リチウムイオン

- 鉛蓄電池

- その他のバッテリータイプ

- 材料別

- リチウム

- グラファイト

- シリコン

- その他

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Shanghai Shanshan Technology Co., Ltd.

- BTR New Material Group Co., Ltd.

- Jiangxi Zhengtuo New Energy Technology

- Mitsubishi Chemical Group.

- Shanghai Putailai New Energy Technology

- Targray Industries Inc.

- Ningbo Shanshan Co., Ltd.

- LG Chemical Group

- Tokai Carbon Co., Ltd.

- Resonac Holdings Corporation.

- List of Other Prominent Companies

- 市場ランキング分析

第7章 市場機会と今後の動向

- 他のアノード材料の研究開発の増加

目次

Product Code: 50003754

The China Electric Vehicle Battery Anode Market size is estimated at USD 4.64 billion in 2025, and is expected to reach USD 7.46 billion by 2030, at a CAGR of 9.95% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, supportive government policies and investments in battery manufacturing and the decreasing price of lithium-ion batteries are expected to drive the market in the forecast period.

- On the other hand, high production cost for anode materials is expected to restrain market growth in the future.

- Nevertheless, the ongoing research and advancement in anode material and efficient electrolytes may offer opportunities for market growth.

China Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Type is Expected to Have a Major Share

- Initially, lithium-ion batteries primarily powered consumer electronics, including mobile phones and personal computers. However, their application has broadened significantly, making them the dominant power source for hybrid and fully electric vehicles (EVs) in China. This transition is primarily driven by the environmental advantages of EVs, which emit no CO2, nitrogen oxides, or other greenhouse gases.

- Due to their high energy density, cost-effectiveness, and efficiency, lithium-ion batteries have become the preferred choice for electric vehicles (EVs). This growing adoption has spurred a rising demand for anode materials during the manufacturing process.

- Further, the decreasing cost of lithium-ion materials is also a significant reason for the increasing demand for lithium-ion battery manufacturing for electric vehicles. In 2023, the price of lithium-ion battery packs decreased by 14% compared to the previous year to USD139/kWh. As battery prices drop, EVs become more affordable, increasing adoption and a larger market share for electric vehicles. This surge in demand will drive higher consumption of battery components, including the anode, and encourage technological advancements to improve battery performance.

- In the future, as technological innovations enhance the efficiency of lithium-ion batteries in electric vehicles, the demand for anode materials is projected to rise simultaneously.

- For instance, in April 2024, Contemporary Amperex Technology Co., a Chinese electric vehicle manufacturer, launched a lithium iron phosphate (LFP) battery for electric vehicles. The new battery has an energy density of 205 Wh per kg, almost 8% higher than the current state of the art for such batteries. Such developments are expected to boost the demand for EV lithium-ion anode materials in the forecast period.

- Additionally, as per Automotive Industry Green and Low-Carbon Development Roadmap 1.0 developed under the supervision of China's Ministry of Industry and Information Technology, electric car sales in China for passenger new energy vehicle (NEV) is expected to reach a 50% share by 2025. Such roadmaps are expected to raise a futuristic oppotunity for EV anode manufacturing too in China.

- Thus, owing to the increasing use of lithium-ion batteries in electric vehicles and decreasing prices, the lithium-ion battery anode segment is expected to grow significantly in the forecast period.

Government Policies and Investments Towards Battery Manufacturing is Expected to Drive the Market

- A combination of supportive government policies and significant investment in battery production drives China's EV battery manufacturing, which, in turn, is expected to boost the demand for electric vehicle battery anodes. The government offers direct financial support, tax incentives, and subsidies, reducing manufacturers' costs and encouraging investment in advanced equipment. Manufacturers of electric vehicles in China benefit from government subsidies. For instance, all-electric plug-in cars boasting a range exceeding 400 km qualify for a subsidy of RMB 12,600 (around USD 2,000). Meanwhile, those ranging between 300 to 400 km receive a subsidy of RMB 9,100 (approximately USD 1,400).

- Further, the country's increasing demand for electric vehicles is fueling investment in electric vehicle battery manufacturing projects, thereby creating a potential need for electric vehicle battery anode materials. According to the International Energy Agency, in 2023, the demand for electric vehicle batteries in China accounted for 417 GWh, up from 314 GWh last year.

- Moreover, rising electric vehicle sales are motivating battery manufacturing companies to invest more in EV battery production, thereby creating demand for EV battery anode materials. According to the International Energy Agency, in 2023, the country's total EV car sales accounted for 8.1 million, higher than 5.9 million in 2022.

- In the future, the demand for EV battery anode materials is expected to increase as the country rushes towards manufacturing electric vehicles, and investments are expected to grow in EV battery manufacturing. For instance, in May 2024, China announced to invest 845 USD million to develop next-generation battery technology powering electricl vehicles. Such investments will boost the demand for electric vehicle battery manufacturing in the forecast period.

- Thus, supportive government policies and investments in battery manufacturing are expected to drive the market.

China Electric Vehicle Battery Anode Industry Overview

The China electric vehicle battery anode market is semi-fragmented. Some of the major players in the market (in no particular order) include Shanghai Shanshan Technology Co., Ltd., BTR New Material Group Co., Ltd., Jiangxi Zhengtuo New Energy Technology, Mitsubishi Chemical Group., and LG Chemical Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments towards battery manufacturing

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 High Production Cost for Anode Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Lithium

- 5.2.2 Graphite

- 5.2.3 Silicon

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Shanghai Shanshan Technology Co., Ltd.

- 6.3.2 BTR New Material Group Co., Ltd.

- 6.3.3 Jiangxi Zhengtuo New Energy Technology

- 6.3.4 Mitsubishi Chemical Group.

- 6.3.5 Shanghai Putailai New Energy Technology

- 6.3.6 Targray Industries Inc.

- 6.3.7 Ningbo Shanshan Co., Ltd.

- 6.3.8 LG Chemical Group

- 6.3.9 Tokai Carbon Co., Ltd.

- 6.3.10 Resonac Holdings Corporation.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Research and Development of Other Anode Materials