|

市場調査レポート

商品コード

1636486

米国の電気自動車用電池負極:市場シェア分析、産業動向、成長予測(2025~2030年)United States Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の電気自動車用電池負極:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

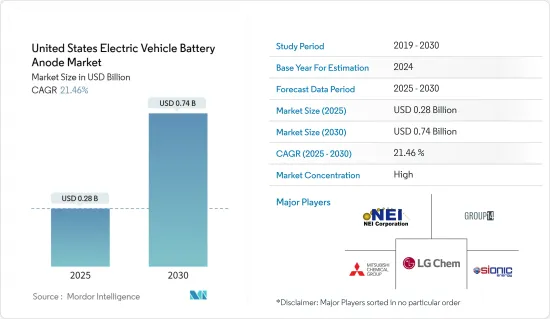

米国の電気自動車用電池負極市場規模は2025年に2億8,000万米ドルと推定・予測され、予測期間(2025~2030年)のCAGRは21.46%で、2030年には7億4,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電池製造に対する政府の支援施策と投資、リチウムイオン電池の価格低下が予測期間の市場を牽引するとみられます。

- 一方、負極材料の国内生産が不十分であることが、今後の市場成長を抑制すると予想されます。

- しかし、現在進行中の負極材料と効率的な電解質の調査と進歩は、市場成長の有望な機会をもたらします。

米国の電気自動車用電池負極市場動向

リチウムイオン電池が大きなシェアを占める見込み

- 米国では、電気自動車とPHEVは主にリチウムイオン電池を使用しており、その化学的性質は民生用電子機器製品とは異なることが多いです。電気自動車にこのような電池が大幅に採用された背景には、他の電気エネルギー貯蔵システムと比較して、単位質量・体積当たりのエネルギーが高いことがあります。また、高出力重量比、高エネルギー効率、高温性能、長寿命、低自己放電という特徴もあります。

- さらに、リチウムイオン電池の材料価格の下落は、EV用電池メーカーにとって有利です。EV用リチウムイオン電池の生産が拡大するにつれて、その製造における負極の需要は増加します。この動向は、同部門の技術革新と効率化を後押しするだけでなく、EV用電池メーカーの国際競合を強化するものでもあります。

- 例えば、2023年のリチウムイオン電池パックの価格は前年から14%下落し、139米ドル/kWhに落ち着く。この電池価格の下落は、EVをより手ごろな価格で購入できることにつながり、普及に拍車をかけ、電気自動車市場のシェアを拡大します。このような需要の高まりは、負極をはじめとする電池部品の消費の増加につながり、電池性能向上のための技術進歩を促進します。

- 現在進行中の研究開発イニシアティブは、電気自動車用リチウムイオン電池のより安定した効率的な負極材料の開発に重点を置いており、負極の需要増加が予想されることをさらに明確にしています。

- 例えば、2023年12月、米国の電池材料会社Sila Nanotechnologies, Inc.はPanasonicと提携し、シリコン負極を採用した電気自動車用電池を開発しました。Silaは、同社のナノ複合シリコン負極材料は、現在のリチウムイオン電池に使われている従来の黒鉛ベースの負極に比べて航続距離を20%向上させることができると主張しています。

- 今後、米国ではEV用リチウムイオン電池の製造に新たな投資が行われるため、負極材に対する需要は急増すると考えられます。例えば、ExxonMobilは2025年6月、EV用電池開発企業のSK Onと、アーカンソー州での初プロジェクトから10万トンのMobil Lithiumを供給するという拘束力のない覚書を交わしました。ExxonMobilは野心的な計画を持っており、2030年までに年間約100万台のEV用電池にリチウムを供給し、米国のEVサプライチェーンを強化することを目標としています。

- 電気自動車へのリチウムイオン電池の採用が増加し、価格が下落していることから、リチウムイオン電池用負極のセグメントは今後数年で大きく成長する見込みです。

電池製造に向けた政府の施策と投資が市場を牽引する展望

- 近年、米国の電気自動車(EV)用電池製造は、政府の支援施策により急増しています。税制優遇措置、補助金、助成金、融資を含むこれらの施策は、極めて重要な役割を果たしています。特に、先進技術自動車製造(ATVM)融資プログラムのような連邦政府のイニシアチブは、最先端の電池技術とその製造施設の開発に資金を流しています。

- 電気自動車の販売台数が増加傾向にあることから、政府は電池製造をさらに刺激する施策をさらに導入する可能性が高いです。その結果、EVバッテリー用負極の国内需要が高まると考えられます。国際エネルギー機関のデータはこの動向を浮き彫りにしています。2023年、米国のEV自動車販売台数は139万台に達し、2022年の99万台から顕著に増加しました。

- さらに政府は、国内での電池製造を拡大するための新たな法整備を積極的に推進しています。これには電池そのものだけでなく、陽極、陰極、セパレーターといった重要な部品も含まれます。こうした動きは、アメリカのEV用電池のサプライチェーンを強化し、クリーンエネルギーへの移行を促進することを目的としています。

- 例えば、2024年4月、オーストラリア出身のSicona Battery Technologiesは、米国南東部にシリコンカーボン負極材生産施設を設立する計画を明らかにしました。Siconaは、2030年代初頭までに年間2万6,500トンの生産量を目標としており、これは毎年325万台以上の電気自動車に電力を供給するのに十分な量です。

- さらに、政府は電気自動車需要に強気の展望を示す複数のイニシアティブや施策を展開しています。その一例として、米国は2024年3月、EV販売の拡大と温室効果ガス排出の抑制を目的として、自動車のテールパイプ排出に関する新たな規制を導入しました。米国環境保護庁(EPA)は、この規制によって2030~2032年の間に新車の30~56%が電気自動車になると予測しています。これは、2030年までに新車販売台数の60%をEVが占め、2032年までに67%まで上昇すると予測していたEPAの以前の予測からの転換です。このような施策により、電気自動車用電池製造の需要は今後数年間でさらに高まることが予想されます。

- 結論として、政府の施策と投資の後押しにより、電池製造の軌道は有望です。

米国の電気自動車用電池負極産業概要

米国の電気自動車用電池負極市場は半固体化しています。市場の主要企業(順不同)には、NEI Corporation, Ltd.、Group14 Technologies、Sionic Energy、Mitsubishi Chemical Group Corporation、LG Chemical Groupなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電池製造に向けた政府の施策と投資

- 電池原料コストの低下

- 抑制要因

- 負極材料の国内生産不足

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- リチウムイオン

- 鉛-酸

- その他の電池タイプ

- 材料

- リチウム

- 黒鉛

- シリコン

- その他

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- NEI Corporation, Ltd.

- Group14 Technologies

- Sionic Energy

- Mitsubishi Chemical Group.

- Sicona Battery Technologies

- Targray Industries Inc.

- Sila Nanotechnologies

- LG Chemical Group

- Nexeon ltd

- Amprius Technologies

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- その他の負極材料の研究開発の増加

目次

Product Code: 50003755

The United States Electric Vehicle Battery Anode Market size is estimated at USD 0.28 billion in 2025, and is expected to reach USD 0.74 billion by 2030, at a CAGR of 21.46% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, supportive government policies and investments in battery manufacturing, and the decreasing price of lithium-ion batteries are expected to drive the market in the forecast period.

- On the other hand, insufficient domestic manufacturing of anode materials is expected to restrain market growth in the future.

- However, ongoing research and advancements in anode materials and efficient electrolytes present promising opportunities for market growth.

United States Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery is Expected to Have a Major Share

- In the United States, all-electric vehicles and PHEVs predominantly utilize lithium-ion batteries, with chemistries that often differ from those in consumer electronics. The reason behind the drastic adoption of such batteries in electric vehicles is their high energy per unit mass and volume relative to other electrical energy storage systems. They also have a high power-to-weight ratio, high energy efficiency, high-temperature performance, long life, and low self-discharge.

- Additionally, falling material prices for lithium-ion batteries are proving advantageous for EV battery manufacturers. As production of EV lithium-ion batteries scales up, the demand for anodes in their manufacturing is set to increase. This trend not only signals a boost in innovation and efficiency within the sector but also strengthens the global competitiveness of EV battery manufacturers.

- For example, in 2023, lithium-ion battery pack prices dropped by 14% from the previous year, settling at USD139/kWh. This decline in battery prices translates to more affordable EVs, spurring adoption and expanding the electric vehicle market share. Such heightened demand will lead to increased consumption of battery components, notably the anode, and propel technological advancements for enhanced battery performance.

- Ongoing R&D initiatives are focused on developing more stable and efficient anode materials for lithium-ion batteries in electric vehicles, further underscoring the anticipated rise in demand for these anodes.

- For instance, in December 2023, Sila Nanotechnologies, Inc., a US-based battery materials firm, partnered with Panasonic to craft electric vehicle batteries featuring silicon anodes. Sila claims their nano-composite silicon anode material could offer a 20% range boost over the conventional graphite-based anodes in today's lithium-ion batteries.

- Looking ahead, with fresh investments pouring into EV lithium-ion battery manufacturing in the United States, the appetite for anode materials is set to surge. For instance, in June 2025, ExxonMobil entered a non-binding memorandum of understanding with SK On, an EV battery developer, to deliver 100,000 metric tons of Mobil Lithium from its inaugural project in Arkansas. ExxonMobil has ambitious plans, targeting lithium supply for approximately 1 million EV batteries annually by 2030, bolstering the U.S. EV supply chain.

- Given the rising adoption of lithium-ion batteries in electric vehicles and the declining prices, the segment for lithium-ion battery anodes is poised for significant growth in the coming years.

Government Policies and Investments Towards Battery Manufacturing is Expected to Drive the Market

- In recent years, the United States electric vehicle (EV) battery manufacturing has surged, due to supportive government policies. These policies, encompassing tax incentives, subsidies, grants, and loans, have played a pivotal role. Notably, federal initiatives like the Advanced Technology Vehicles Manufacturing (ATVM) loan program are channeling funds into the development of cutting-edge battery technologies and their manufacturing facilities.

- With electric vehicle sales on the rise, the government is likely to introduce more policies to further stimulate battery manufacturing. This, in turn, will heighten the demand for EV battery anodes domestically. Data from the International Energy Agency highlights this trend: in 2023, the United States EV car sales reached 1.39 million units, a notable increase from 0.99 million in 2022.

- Moreover, the government is actively pushing for new legislation to expand domestic battery manufacturing. This includes not just the batteries themselves but also crucial components like anodes, cathodes, and separators. Such moves aim to strengthen America's supply chains for EV batteries and facilitate the transition to clean energy.

- For example, in April 2024, Sicona Battery Technologies, hailing from Australia, revealed plans for its inaugural silicon-carbon anode materials production facility in the Southeastern U.S. Looking ahead, Sicona targets an annual output of 26,500 tons by the early 2030s, enough to power over 3.25 million electric vehicles each year.

- Additionally, the government has rolled out multiple initiatives and policies, signaling a bullish outlook on electric vehicle demand. A case in point: in March 2024, the U.S. introduced new regulations on car tailpipe emissions, a move aimed at amplifying EV sales and curbing greenhouse gas emissions. The U.S. Environmental Protection Agency (EPA) projects these regulations could lead to 30 to 56 percent of new cars being electric between 2030 and 2032. This is a shift from the EPA's previous forecast, which anticipated EVs would make up 60 percent of new car sales by 2030, climbing to 67 percent by 2032. Such policies are poised to bolster the demand for electric vehicle battery manufacturing in the coming years.

- In conclusion, with the backing of government policies and investments, the trajectory for battery manufacturing looks promising.

United States Electric Vehicle Battery Anode Industry Overview

The United States electric vehicle battery anode market is semi-consolidated. Some of the major players in the market (in no particular order) include NEI Corporation, Ltd., Group14 Technologies, Sionic Energy, Mitsubishi Chemical Group., and LG Chemical Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments towards battery manufacturing

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 Insufficient Domestic Manufacturing of Anode Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Lithium

- 5.2.2 Graphite

- 5.2.3 Silicon

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 NEI Corporation, Ltd.

- 6.3.2 Group14 Technologies

- 6.3.3 Sionic Energy

- 6.3.4 Mitsubishi Chemical Group.

- 6.3.5 Sicona Battery Technologies

- 6.3.6 Targray Industries Inc.

- 6.3.7 Sila Nanotechnologies

- 6.3.8 LG Chemical Group

- 6.3.9 Nexeon ltd

- 6.3.10 Amprius Technologies

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Research and Development of Other Anode Materials