|

市場調査レポート

商品コード

1636502

ASEANのEVバッテリーアノード:市場シェア分析、産業動向、成長予測(2025年~2030年)ASEAN Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ASEANのEVバッテリーアノード:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

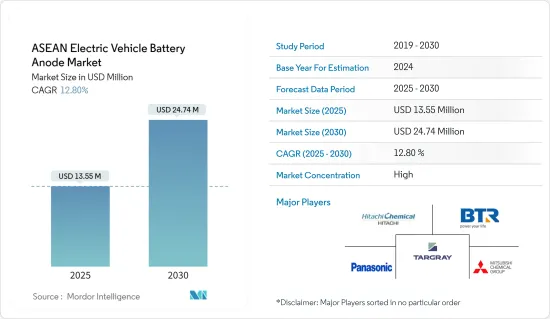

ASEANのEVバッテリーアノードの市場規模は、2025年に1,355万米ドルと推定され、予測期間(2025-2030年)のCAGRは12.8%で、2030年には2,474万米ドルに達すると予測されます。

主なハイライト

- 今後数年間、ASEANのEVバッテリーアノード市場は、電気自動車の普及拡大、リチウムイオン電池原料のコスト低下、政府の支援政策などの要因によって成長する見込みです。

- しかし、原材料の埋蔵量に限りがあることやサプライチェーンの格差といった課題は、市場の拡大を妨げる可能性があります。

- しかし、電池材料の技術進歩が進み、電気自動車の長期目標が意欲的であることから、ASEANのEVバッテリーアノード市場には大きなビジネスチャンスが待ち受けています。

- ASEAN諸国の中では、インドネシアがEVバッテリーアノード市場の主要企業として台頭してくるものと思われます。

ASEANのEVバッテリーアノード市場の動向

リチウムイオン電池セグメントが市場を独占

- 当初、東南アジアのリチウムイオン電池産業は主に家電セクターを対象としていました。これは、この地域が業界プレイヤーの大半とリチウムイオン電池に不可欠な鉱物の両方の本拠地であることが主な理由でした。しかし、時間の経過とともに大きな変化が起こった。電気自動車(EV)メーカーが家電部門を凌駕し始め、リチウムイオン電池の主要消費者として台頭し、鉛蓄電池やその他の電池タイプを凌駕しました。この変化は、ASEAN諸国におけるEV販売の急増と、リチウムイオン電池とそれに関連するEVバッテリーアノード市場への投資の急増が主な要因となっています。

- インドネシア、タイ、シンガポール、ベトナムなどの国々では、過去数十年間、特に自動車分野でリチウムイオン電池技術が急成長してきました。ASEAN諸国では、主にその優れた容量対重量比により、リチウムイオン二次電池への支持が高まっています。さらに、EVに搭載されるリチウム電池は、NOX、CO2、その他の温室効果ガスを排出しないため、従来の内燃機関(ICE)車に比べて環境負荷が大幅に低いです。この利点を踏まえ、ASEAN諸国はEVの普及と電池負極の現地製造市場の開拓を積極的に推進しています。

- フィリピンとベトナムの乗用車販売台数は、2023年には2022年比でそれぞれ16.4%と2.8%増加しました。これは、リチウムイオン電気自動車セクターのプレーヤー、ひいてはASEAN各国のEVバッテリーアノード市場のプレーヤーにとって良い兆しです。

- 2023年12月、タイの著名な石油・ガス複合企業であるPTTは、リチウムイオン電池の生産に乗り出しました。このイニシアチブは、電気自動車ブランド「ネタ」のサプライチェーンを構築し、タイの拡大するグリーン・カー市場を活用するというPTTの広範な戦略に沿ったものです。PTT関係者は、合弁パートナーであるNVゴティオン社が、バンコクの南東に位置するラヨーン県にリチウムイオン電池の生産ラインを設立したと発表しました。この施設は現在、年間2ギガワット時の生産能力を誇っており、近い将来には8ギガワット時まで規模を拡大する野心的な計画を立てています。

- 2024年7月、インドネシアは初のリチウムイオンEVバッテリー工場の落成を祝った。東南アジア最大の経済大国であり、世界で最も豊富なリチウムイオン電池鉱物を産出するインドネシアは、世界の電気自動車サプライチェーンにおいて戦略的な位置づけにあります。韓国の大手企業LGエナジー・ソリューション(LGES)と現代自動車グループの合弁事業であるこの工場は、年間10ギガワット時(GWh)という驚異的なリチウムイオン電池セルを生産する予定です。このような重要な開発は、ASEANのEVバッテリーアノード市場の利害関係者にとって好都合です。

- タイ自動車研究所(TAI)のデータによると、タイでは電気自動車の登録台数が著しく急増しています。2023年の登録台数は17万台に達し、2022年の8万4,570台から大幅に急増しました。これらの自動車の95%以上がリチウムイオン技術を動力源としていることを考えると、この成長はタイのEVバッテリーアノード市場におけるリチウムイオン分野の優位性を強調しています。

- 結論として、リチウムイオン電池セグメントが市場セグメンテーションのEVバッテリーアノード市場を独占することを強く示しています。

市場を独占するインドネシア

- インドネシアは、2030年までにCO2排出量を29%削減することを目指しており、これは約3億300万トンに相当します。二酸化炭素排出と化石燃料への依存に対する懸念が高まる中、インドネシアは電気自動車(EV)のイントロダクションを実行可能な解決策と見なしています。このシフトは、同国のEVバッテリーアノード市場に大きなチャンスをもたらすことになります。

- さらに、インドネシア政府は、世界の大手EVメーカーに国内投資を積極的に働きかけています。例えば、2024年5月にバリ島で開催された世界水フォーラムで、インドネシアの海事・投資担当調整相は、テスラのCEOがインドネシア政府にEVバッテリー工場の設置を提案していることを明らかにしました。この動きは、ジャカルタのEV負極材生産における支配的なプレーヤーとしての台頭という野望を大きく後押しすると思われます。

- 2023年11月、米国とインドネシアは、電気自動車(EV)バッテリーに不可欠な金属の取引に重点を置いた、重要鉱物に焦点を当てたパートナーシップの構築を中心に協議しました。

- 2024年9月、インドネシア外務省は、電気自動車(EV)バッテリーの生産に必要な重要鉱物の協力関係を拡大する意向を表明し、今度はアフリカ諸国と協力することになった。インドネシア・アフリカ・フォーラム(IAF)で同省の事務局長は、EVバッテリーだけでなく、正極や負極などの関連部品にも重要鉱物の膨大な需要があることを強調しました。同省はまた、特にインドネシア鉱業(MIND ID)とタンザニアとのリチウムにおける活発な協力関係を指摘しました。これらの試みは、インドネシアのEVバッテリーアノード市場の力強い成長の可能性を示唆しています。

- 国連COMTRADEのデータによると、電池鉱物が豊富な国でありながら、インドネシアのリチウムイオン電池の輸入は急増し、高止まりしています。2023年、リチウムイオン電池の輸入額は2,759万米ドルに達し、2022年の2,757万米ドルからわずかに上昇しました。この動向は、インドネシアのEVセクターにおけるリチウムイオン電池の旺盛な需要を浮き彫りにし、インドネシアのEVバッテリーアノード製造能力が急成長していることを浮き彫りにしています。

- 2024年5月、オーストラリアのシラー・リソース・グループは、モザンビークのバラマ黒鉛鉱業から1万トンの天然黒鉛微粉末を出荷しました。この出荷は、インドネシアにあるBTRニュー・エナジー・マテリアルズの新工場向けです。インドネシアでは、EVバッテリーの生産とそれに関連する負極材のインフラ整備が進められており、今回の出荷は、3月に試験的に送られたコンテナに続くものです。この動きは、シラーの多角化戦略において極めて重要な瞬間であるだけでなく、天然黒鉛と活性負極材(AAM)の供給における世界的リーダーとしての地位を確固たるものにするものです。

- これらの開発から、インドネシアがASEANのEVバッテリーアノード市場において足場を固めつつあることは明らかです。

ASEANのEVバッテリーアノード産業の概要

ASEANのEVバッテリーアノード市場は半固体化しています。市場の主要企業(順不同)には、BTR New Material Group、Targray Technology International Inc.、三菱化学グループ、日立化成工業、パナソニックなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- 有利な政府政策

- リチウムイオン電池の価格低下

- 抑制要因

- サプライチェーンのギャップ

- 促進要因

- サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- バッテリータイプ別

- リチウムイオン

- 鉛蓄電池

- その他の技術

- 材料タイプ別

- シリコン

- グラファイト

- リチウム

- その他の材料

- 地域別

- マレーシア

- インドネシア

- タイ

- ベトナム

- その他のASEAN諸国

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BTR New Material Group Co., Ltd

- Shenzhen Dynanonic Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Hitachi Chemical Company Ltd

- Northern Graphite Corporation

- Panasonic Corporation

- Targray Technology International Inc.

- Epsilon Advanced Materials Pvt. Ltd.

- Volt14 Solutions Pte Ltd

- List of Other Prominent Companies

- Market Ranking/Share(%)Analysis

第7章 市場機会と今後の動向

- 負極材における進行中の調査と進歩

The ASEAN Electric Vehicle Battery Anode Market size is estimated at USD 13.55 million in 2025, and is expected to reach USD 24.74 million by 2030, at a CAGR of 12.8% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the ASEAN Electric Vehicle Battery Anode Market is poised for growth, driven by factors such as the rising adoption of electric vehicles, decreasing costs of Li-ion battery raw materials, and supportive government policies.

- However, challenges like limited raw material reserves and supply chain gaps may hinder the market's expansion.

- Yet, with ongoing technological advancements in battery materials and ambitious long-term targets for electric vehicles, significant opportunities await players in the ASEAN Electric Vehicle Battery Anode Market.

- Among the ASEAN nations, Indonesia is set to emerge as a leading player in the electric vehicle battery anode landscape.

ASEAN Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Segment to Dominate the Market

- Initially, the lithium-ion battery industry in Southeast Asia primarily served the consumer electronics sector. This was largely due to the region being home to both a majority of industry players and the minerals essential for Li-ion batteries. However, a significant transformation occurred over time. Electric vehicle (EV) manufacturers began to eclipse the consumer electronics sector, emerging as the primary consumers of lithium-ion batteries, outpacing lead-acid and other battery types. This shift was predominantly fueled by surging EV sales in ASEAN countries and escalating investments in Li-ion batteries and the associated Electric Vehicle Battery Anode Market.

- In nations such as Indonesia, Thailand, Singapore, and Vietnam, the past few decades have seen a meteoric rise of lithium-ion battery technology, especially in the automotive sector. ASEAN nations are increasingly favoring lithium-ion rechargeable batteries, primarily due to their superior capacity-to-weight ratio. Furthermore, lithium batteries in EVs do not emit NOX, CO2, or any other greenhouse gases, resulting in a significantly lower environmental impact compared to conventional internal combustion engine (ICE) vehicles. Given this advantage, ASEAN nations are actively promoting EV adoption and the development of local battery anode manufacturing markets.

- Data from the Organisation Internationale des Constructeurs d'Automobiles highlights a positive trend: both the Philippines and Vietnam saw passenger vehicle sales grow by 16.4% and 2.8% respectively in 2023 compared to 2022. This bodes well for players in the Li-ion Electric Vehicle sector and, by extension, those in the Electric Vehicle Battery Anode Market across ASEAN countries.

- In December 2023, PTT, a prominent oil and gas conglomerate from Thailand, ventured into lithium-ion battery production. This initiative aligns with PTT's broader strategy to create a supply chain for its electric vehicle brand, Neta, and capitalize on Thailand's expanding green car market. PTT officials announced that their joint venture partner, NV Gotion, has established a lithium-ion battery production line in Rayong province, southeast of Bangkok. The facility currently boasts a production capacity of 2 gigawatt-hours per year, with ambitious plans to scale up to 8 gigawatt-hours in the near future, directly catering to the surging demand and subsequently fueling the nation's EV Battery Anode Market.

- In July 2024, Indonesia celebrated the inauguration of its first Li-ion EV battery plant. As the largest economy in Southeast Asia and home to the world's richest Li-ion battery minerals, Indonesia is strategically positioning itself in the global electric vehicle supply chain. This plant, a joint venture between South Korean titans LG Energy Solution (LGES) and Hyundai Motor Group, is set to produce a staggering 10 Gigawatt hours (GWh) of Li-ion battery cells annually. Such a significant development augurs well for stakeholders in the ASEAN Electric Vehicle Battery Anode Market.

- Data from the Thailand Automotive Institute (TAI) reveals a remarkable surge in electric vehicle registrations in Thailand. In 2023, registrations reached 170,000, a significant jump from 84,570 in 2022. Given that over 95% of these vehicles are powered by Li-ion technology, this growth underscores the dominance of the Li-ion segment in Thailand's Electric Vehicle Battery Anode Market.

- In conclusion, the evidence strongly indicates that the lithium-ion battery segment is poised to dominate the ASEAN Electric Vehicle Battery Anode Market.

Indonesia to Dominate the Market

- Indonesia aims to cut CO2 emissions by 29%, equating to approximately 303 million tons, by the year 2030. With rising concerns over carbon emissions and reliance on fossil fuels, Indonesia views the introduction of electric vehicles (EVs) as a viable solution. This shift is poised to unlock substantial opportunities for the Electric Vehicle Battery Anode Market in the nation.

- Moreover, the Indonesian government is actively courting major global EV players to invest domestically. For instance, in May 2024, at the World Water Forum in Bali, Indonesia's coordinating minister for maritime affairs and investment revealed that Tesla's CEO is contemplating a proposal from the Indonesian government to set up an EV battery plant in the nation. This move would significantly bolster Jakarta's ambition to emerge as a dominant player in EV anode production.

- In November 2023, discussions between the U.S. and Indonesia centered on forging a partnership focused on critical minerals, with an emphasis on trading metals essential for electric vehicle (EV) batteries.

- In September 2024, the Indonesian Foreign Affairs Ministry expressed its intent to expand collaborations on critical minerals for EV battery production, this time engaging with African nations. At the Indonesia-Africa Forum (IAF), the ministry's Director General underscored Indonesia's vast demand for critical minerals, not only for EV batteries but also for related components like cathodes and anodes. The ministry also pointed out an active collaboration in lithium, especially between Mining Industry Indonesia (MIND ID) and Tanzania. These endeavors hint at a robust growth potential for Indonesia's Electric Vehicle Battery Anode Market.

- Data from the United Nations COMTRADE reveals that even as a nation rich in battery minerals, Indonesia's imports of Li-ion batteries have surged and remained elevated. In 2023, the value of imported Li-ion batteries reached USD 27.59 million, a slight uptick from USD 27.57 million in 2022. This trend underscores a strong demand for Li-ion batteries in Indonesia's EV sector and highlights the nation's burgeoning capacity for Electric Vehicle Battery Anode manufacturing.

- In May 2024, Australia's Syrah Resources Group dispatched 10,000 metric tons of natural graphite fines from its Balama graphite operation in Mozambique. The shipment was destined for BTR New Energy Materials' new plant in Indonesia. As Indonesia ramps up its infrastructure for EV battery production and associated anode materials, this shipment follows a trial container sent in March. This move not only marks a pivotal moment in Syrah's diversification strategy but also cements its position as a global leader in supplying natural graphite and active anode materials (AAM).

- Given these developments, it's evident that Indonesia is solidifying its foothold in the ASEAN Electric Vehicle Battery Anode Market.

ASEAN Electric Vehicle Battery Anode Industry Overview

The ASEAN Electric Vehicle Battery Anode Market is semi-consolidated. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Targray Technology International Inc., Mitsubishi Chemical Group Corporation, Hitachi Chemical Company Ltd, and Panasonic Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Growing Adoption of Electric Vehicles

- 4.5.1.2 Favorable Government Policies

- 4.5.1.3 Decreasing Price of Lithium-ion Batteries

- 4.5.2 Restraints

- 4.5.2.1 The Supply Chain Gap

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Battery type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-acid

- 5.1.3 Other technology

- 5.2 By Material Type

- 5.2.1 Silicon

- 5.2.2 Graphite

- 5.2.3 Lithium

- 5.2.4 Other Materials

- 5.3 Geography

- 5.3.1 Malaysia

- 5.3.2 Indonesia

- 5.3.3 Thailand

- 5.3.4 Vietnam

- 5.3.5 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BTR New Material Group Co., Ltd

- 6.3.2 Shenzhen Dynanonic Co., Ltd.

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 Hitachi Chemical Company Ltd

- 6.3.5 Northern Graphite Corporation

- 6.3.6 Panasonic Corporation

- 6.3.7 Targray Technology International Inc.

- 6.3.8 Epsilon Advanced Materials Pvt. Ltd.

- 6.3.9 Volt14 Solutions Pte Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ongoing Research and Advancement in Anode Material