|

市場調査レポート

商品コード

1636506

欧州の電気自動車用バッテリー負極:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の電気自動車用バッテリー負極:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

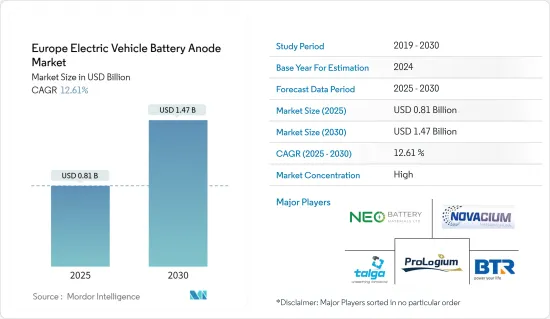

欧州の電気自動車用バッテリー負極市場規模は、2025年に8億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは12.61%で、2030年には14億7,000万米ドルに達すると予測されます。

主要ハイライト

- 今後数年間、欧州の電気自動車用電池負極市場は、電気自動車の普及拡大、電池原料のコスト低下(リチウムイオン電池の低価格化につながる)、政府の支援施策に牽引され、成長が見込まれます。

- 逆に、原料の埋蔵量に限りがあることやサプライチェーンにギャップがあることなどの課題は、欧州の電気自動車用電池負極市場の成長を妨げる可能性があります。

- しかし、バッテリー負極技術の進歩や電気自動車の野心的な長期目標は、欧州電気自動車バッテリー負極市場の参入企業に大きな機会を与えています。

- 欧州の主要参入企業の中では、フランスが欧州電気自動車バッテリー負極市場で顕著な成長を遂げると考えられます。

欧州電気自動車用バッテリー負極市場の動向

リチウムイオン電池セグメントが市場を独占

- リチウムイオン電池産業の初期には、民生用電子機器が主要市場でした。しかし、時が経つにつれて、電気自動車(EV)メーカーがリチウムイオン電池の主要消費者として台頭しました。このEVセグメントでのリチウムイオン電池の需要拡大は、電池負極材料の市場を強化しました。

- 過去10年間、欧州では、特に自動車セグメントでリチウムイオン電池の採用が急増しています。フランス、英国、ドイツ、イタリア、スペインなどの国々では、容量対重量比が優れていることから、リチウムイオン二次電池の支持が高まっています。さらに、EVに搭載されるリチウム電池は、NOX、CO2、その他の温室効果ガスを排出しないため、従来の内燃機関(ICE)車に比べて環境負荷が大幅に低いです。この利点を認識し、欧州の数カ国はリチウムイオン技術主導のEVを積極的に推進し、補助金や政府のイニシアチブを通じて電気自動車用バッテリー負極市場の開拓を促進しています。

- Bloombergは、2023年に電気自動車(EV)に使用されるリチウムイオン電池パックの世界平均価格が前年比13%減の139米ドル/kWhに下落したと報じました。この下落は、それ以前の価格上昇傾向に続くものです。継続的な技術の進歩と製造効率の向上により、価格は今後も下落基調を続けると予測されます。予測によれば、2025年には113米ドル/kWhまで下がり、2030年には80米ドル/kWhまでさらに急落します。こうした動向は、予測期間中、欧州の電気自動車用電池負極市場におけるリチウムイオン電池セグメントの優位性を強化します。

- 国際エネルギー機関(IEA)によると、リチウムイオン電池技術を主に利用する(シェア95%以上)英国の電気自動車販売台数は、2022年の37万台から2023年には45万台に達します。このような電気自動車セグメントの堅調な成長を考えると、リチウムイオン電池は、その明確な利点により、欧州の電気自動車用電池負極市場で大きなシェアを獲得する準備が整っています。

- 2024年6月、Stora EnsoとAltrisは、欧州におけるサステイナブル電池バリューチェーンと材料チェーンの確立を目指した提携を発表しました。両社の提携は、Stora Ensoの硬質炭素ソリューションであるリグノードをAltrisのナトリウムイオン電池セルの負極材として統合することに焦点を当てています。これらの電池は、走行用と据置型の両方の電力貯蔵用に設計されています。Stora Ensoが説明するLignodeは、パルプ製造の製品別であるリグニン由来のサステイナブル硬質炭素です。この新しい負極材は、リチウムイオンバッテリーとナトリウムイオンバッテリーの両方との互換性を誇り、従来の負極ソリューションに比べてよりサステイナブル選択肢となります。

- このような新興国市場の開発を考えると、今後数年間はリチウムイオン電池セグメントが欧州の電気自動車用電池負極市場を独占することは明らかです。

欧州の電気自動車用電池負極市場を独占するフランス

- 先進国の代表格であるフランスは、近年の温室効果ガス排出量の大幅削減という途方もない課題に取り組んでいます。再生可能エネルギー源をエネルギーミックスに組み込むことに加え、フランスは気候変動との戦いにおける重要な戦略として、自動車排出への取り組みを優先しています。この焦点は、EV用バッテリー負極市場の参入企業に有利な機会をもたらしました。数多くの外国企業がフランスに進出し、一貫して製造能力を拡大しています。

- 2024年10月14日、Paris Motor Showで、リチウムセラミック電池の技術革新のトップランナーであるProLogium技術が、100%シリコン複合負極を採用した世界初のEV用電池を発表しました。この画期的なバッテリーは、わずか8.5分で充電できます。このような進歩は、EV用電池の負極材料の技術革新に積極的に取り組んでいる欧州の負極市場が急成長していることを裏付けています。

- 2024年5月、クリーンエネルギー技術企業のAnteoTechは、著名な電気自動車メーカーが同社のバッテリー負極技術を試作バッテリーに採用することを明らかにしました。ストラスブールで開催された第14回国際先進自動車電池会議(AABC)で、AnteoTechはEV1のプロジェクト管理チームとの会合を含め、電池メーカーと会談を行った。世界の電気自動車メーカーであるEV1は、車両へのAnteoTech XTM技術の統合を評価しています。AnteoTechは、EV1がAnteo XTMが投入コストを削減するだけでなく、独自の負極の性能を高めることを確認したと強調しています。

- 2024年8月、シリカとシリコンをベースとする負極材料のグリーンエンジニアリングに注力するフランスの子会社、Novacium SASは、バッテリー革新において極めて重要なマイルストーンに到達しました。黒鉛と精製された第三世代(GEN3)シリコン系負極を組み合わせた同社の最新バッテリーは、4,030 mAhを超える容量を達成しました。これは、18650電池の世界記録4,095mAhに迫るものです。この偉業により、Novacium SASは、4,000 mAhを超える1万8,650のバッテリーの容量を報告した世界で3社のみのうちの1社となりました。このようなマイルストーンは、フランスのEVバッテリー負極材市場展望を強化するものです。

- 国際エネルギー機関(IEA)のデータによると、2023年のフランスの電気自動車販売台数は47万台に達し、2022年の34万台から増加し、95%以上がリチウムイオン電池技術に依存しています。このような電気自動車セグメントの急成長を考えると、リチウムイオン電池はその明確な優位性から、フランスの電気自動車用電池負極市場でかなりのシェアを占めることになります。

- その結果、こうした新興国市場の開拓により、フランスは今後数年間、欧州の電気自動車用負極市場で極めて重要な位置を占めることになります。

欧州の電気自動車用電池負極産業概要

欧州の電気自動車用電池負極市場は適度に統合されています。市場の主要企業(順不同)には、BTR New Material Group、Novacium SAS、ProLogium Technology、Talga Group、NEO Battery Materials Ltdなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- 有利な政府施策

- リチウムイオン電池の価格低下

- 抑制要因

- サプライチェーンのギャップ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 電池タイプ別

- リチウムイオン

- 鉛蓄電池

- その他

- 材料タイプ別

- シリコン

- 黒鉛

- リチウム

- その他

- 地域別

- フランス

- 英国

- ドイツ

- スペイン

- イタリア

- 北欧諸国

- その他の欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BTR New Material Group Co., Ltd

- Novacium SAS

- ProLogium Technology Co., Ltd

- Talga Group

- NEO Battery Materials Ltd

- IPCEI European Battery Innovation

- Vianode

- Epsilon Advanced Materials Pvt. Ltd.

- Altech Batteries Ltd

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 負極材における進行中の調査と進歩

目次

Product Code: 50003835

The Europe Electric Vehicle Battery Anode Market size is estimated at USD 0.81 billion in 2025, and is expected to reach USD 1.47 billion by 2030, at a CAGR of 12.61% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the Europe electric vehicle battery anode market is poised for growth, driven by the rising adoption of electric vehicles, decreasing costs of battery raw materials (leading to lower prices for Li-ion batteries), and supportive government policies.

- Conversely, challenges such as limited raw material reserves and gaps in the supply chain may hinder the growth of the Europe electric vehicle battery anode market.

- However, advancements in battery anode technologies and ambitious long-term targets for electric vehicles present significant opportunities for players in the European electric Vehicle Battery Anode Market.

- Among the key players in Europe, France is set to experience notable growth in the Europe electric vehicle battery anode market.

Europe Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Segment to Dominate the Market

- In the early days of the lithium-ion battery industry, consumer electronics were the primary market. However, over time, electric vehicle (EV) manufacturers emerged as the leading consumers of these batteries, driven by a surge in EV sales, particularly in plug-in hybrid electric vehicles (PHEVs). This growing demand for lithium-ion batteries in the EV sector bolstered the market for battery anode materials.

- Over the past decade, Europe has seen a meteoric rise in the adoption of lithium-ion batteries, especially in the automotive sector. Countries like France, the UK, Germany, Italy, and Spain are increasingly favoring lithium-ion rechargeable batteries, due to their superior capacity-to-weight ratio. Moreover, lithium batteries in EVs produce no emissions of NOX, CO2, or other greenhouse gases, resulting in a significantly lower environmental impact compared to traditional internal combustion engine (ICE) vehicles. Recognizing this advantage, several European nations are actively promoting lithium-ion technology-driven EVs and fostering the development of the Electric Vehicle Battery Anode Market through subsidies and government initiatives.

- Bloomberg reported that in 2023, global average prices for lithium-ion battery packs used in electric vehicles (EVs) fell to USD 139/kWh, a 13% drop from the previous year. This decline followed a trend of rising prices in earlier years. With ongoing technological advancements and improved manufacturing efficiencies, prices are projected to continue their downward trajectory. Forecasts indicate a price drop to USD 113/kWh by 2025, and an even steeper decline to USD 80/kWh by 2030. Such trends bolster the dominance of the lithium-ion battery segment in Europe's Electric Vehicle Battery Anode Market during the forecast period.

- According to the International Energy Agency (IEA), in 2023, electric vehicle sales in the United Kingdom, predominantly utilizing lithium-ion battery technology (over 95% share), reached 450,000, up from 370,000 in 2022. Given this robust growth in the battery electric vehicle sector, lithium-ion batteries, with their distinct advantages, are poised to capture a significant share of Europe's Electric Vehicle Battery Anode Market.

- In June 2024, Stora Enso and Altris unveiled their partnership aimed at establishing a sustainable battery value and materials chain in Europe. Their collaboration focuses on integrating Stora Enso's Lignode, a hard carbon solution, as an anode material in Altris' sodium-ion battery cells. These cells are designed for both motive and stationary power storage. Lignode, as described by Stora Enso, is a sustainable hard carbon derived from lignin, a pulp manufacturing byproduct. This novel anode material boasts compatibility with both lithium-ion and sodium-ion batteries, marking it as a more sustainable choice compared to conventional anode solutions.

- Given these developments, it's evident that the lithium-ion battery segment is set to dominate Europe's Electric Vehicle Battery Anode Market in the coming years.

France to Dominate the Electric Vehicle Battery Anode Market in Europe

- France, a leading developed nation, has taken on the monumental challenge of significantly reducing its greenhouse gas emissions in recent years. In addition to integrating renewable energy sources into its energy mix, France has prioritized tackling vehicular emissions as a key strategy in its fight against climate change. This focus has opened up lucrative opportunities for players in the EV battery anode market. Numerous foreign companies have set up operations in France, consistently expanding their manufacturing capabilities.

- On October 14th, 2024, at the Paris Motor Show, ProLogium Technology, a frontrunner in lithium ceramic battery innovation, unveiled the world's first EV battery featuring a 100% silicon composite anode. This revolutionary battery can be charged in a mere 8.5 minutes. Such advancements underscore the burgeoning anode market in Europe, with companies actively innovating in EV battery anode materials.

- In May 2024, AnteoTech, a clean energy tech firm, revealed that a prominent electric vehicle maker will adopt its battery anode technology in their prototype batteries. At the 14th International Advanced Automotive Battery Conference (AABC) in Strasbourg, AnteoTech held talks with battery manufacturers, including a meeting with EV1's project management team. EV1, a global electric vehicle manufacturer, is evaluating the integration of Anteo XTM technology into its vehicles. AnteoTech highlights that EV1 has confirmed that Anteo XTM not only reduces their input costs but also boosts the performance of their proprietary anode.

- In August 2024, Novacium SAS, a French subsidiary focused on green engineering of silica and silicon-based anode materials, reached a pivotal milestone in battery innovation. Their latest batteries, combining graphite with a refined third-generation (GEN3) silicon-based anode, achieved a capacity of over 4,030 mAh. This is nearing the world record of 4,095 mAh for 18650 batteries. With this feat, Novacium SAS becomes one of only three companies worldwide to report 18650 battery capacities surpassing 4,000 mAh. Such milestones bolster the prospects of the EV battery anode material market in France.

- Data from the International Energy Agency (IEA) reveals that in 2023, France saw electric vehicle sales hit 470,000, up from 340,000 in 2022, with over 95% relying on Li-ion battery technology. Given this surge in the battery electric vehicle sector, lithium-ion batteries, with their distinct advantages, are poised to command a substantial share of the Electric Vehicle Battery Anode Market in France.

- Consequently, these developments position France as a pivotal player in the European Electric Vehicle Battery Anode Market in the coming years.

Europe Electric Vehicle Battery Anode Industry Overview

The Europe Electric Vehicle Battery Anode Market is moderately consolidated. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Novacium SAS, ProLogium Technology Co., Ltd, Talga Group, and NEO Battery Materials Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Growing Adoption of Electric Vehicles

- 4.5.1.2 Favorable Government Policies

- 4.5.1.3 Decreasing Price of Lithium-ion Batteries

- 4.5.2 Restraints

- 4.5.2.1 The Supply Chain Gap

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Battery type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-acid

- 5.1.3 Other technology

- 5.2 By Material Type

- 5.2.1 Silicon

- 5.2.2 Graphite

- 5.2.3 Lithium

- 5.2.4 Other Materials

- 5.3 Geography

- 5.3.1 France

- 5.3.2 United Kingdom

- 5.3.3 Germany

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 Nordic countries

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BTR New Material Group Co., Ltd

- 6.3.2 Novacium SAS

- 6.3.3 ProLogium Technology Co., Ltd

- 6.3.4 Talga Group

- 6.3.5 NEO Battery Materials Ltd

- 6.3.6 IPCEI European Battery Innovation

- 6.3.7 Vianode

- 6.3.8 Epsilon Advanced Materials Pvt. Ltd.

- 6.3.9 Altech Batteries Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ongoing Research and Advancement in Anode Material