|

市場調査レポート

商品コード

1636503

英国の電気自動車用バッテリー負極:市場シェア分析、産業動向、成長予測(2025~2030年)United Kingdom Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の電気自動車用バッテリー負極:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

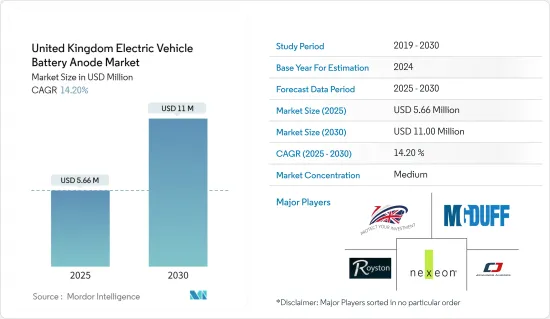

英国の電気自動車用バッテリー負極市場規模は2025年に566万米ドルと推定され、予測期間(2025~2030年)のCAGRは14.2%で、2030年には1,100万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、政府の野心的な目標とそれに対応する投資によって電気自動車の普及が進み、市場はその恩恵を受けることになります。

- しかし、土地コスト、原料の物流、バッテリー製造に対する補助金の不在といった課題が、市場拡大の妨げになる可能性があります。

- 負極材料の研究開発が進行中であるため、市場には有望な成長の可能性があります。

英国の電気自動車用バッテリー負極市場動向

リチウムイオンバッテリーが市場を独占

- リチウムイオンバッテリーは電気自動車(EV)革命の最前線にあります。その優れたエネルギー密度と長寿命サイクルにより、自動車産業がサステイナブルエネルギーソリューションに軸足を移す中で極めて重要な存在となっています。英国では、リチウムイオンバッテリーセグメントの研究開発が勢いを増しています。

- 2023年9月、英国の電気化学エネルギー貯蔵研究の最高機関であるファラデーラボは、リチウムイオン構想に重点を置いた4つの主要バッテリー研究プロジェクトに2,100万米ドルを投資すると発表しました。これらの投資は、負極製造の将来的な需要を強化する態勢を整えています。

- さらに、英国はリチウム鉱床を利用する大手企業を引き寄せており、この動きは国内のリチウムイオンバッテリー生産を強化すると予想されています。例えば、2023年6月、工業鉱物のリーダーであるフランスの多国籍企業Imerys S.A.は、British Lithiumの株式の80%を取得しました。この民間企業は、雲母御影石からバッテリー用リチウムを持続的に抽出する最前線にいます。両社の提携は、英国初のバッテリーグレード炭酸リチウムの総合的な生産会社を設立することを目的としています。

- 歴史的に、リチウムイオンバッテリーの価格が急落するにつれ、関連部品、特に負極の需要が急増しています。Bloomberg NEFによると、2023年のリチウムイオンバッテリーの平均価格は139米ドル/KWhで、2014年以来5倍という驚異的な価格下落を記録しました。価格下落に牽引されたこの迅速な採用は、負極市場の成長にとって良い兆しです。

- リチウムイオンバッテリーと負極の生産におけるこのような動向を考えると、インドの電気自動車用バッテリー負極市場は今後数年で成長する態勢が整っています。

電気自動車の普及に向けた政府の支援

- 英国政府は、2050年までに炭素排出量を正味ゼロにするという野心的な目標を掲げており、特に運輸部門からの排出削減に重点を置いています。エネルギー安全保障・ネットゼロ省によると、国内の運輸部門は温室効果ガス排出量の約29.1%を占め、様々な部門の中で最大の排出源となっています。こうした背景から、英国が電気自動車を推進することで、今後数年間はバッテリー部品、特にアノードの需要が高まると予想されます。

- 例えば、2024年1月、政府は自動車メーカーを対象としたゼロエミッション車(ZEV)義務化を導入しました。このイニシアチブは、消費者に電気自動車の選択肢を広げると同時に、メーカーに確実性を提供することを目的としています。

- さらに、この義務化では、メーカーのゼロ・エミッション車(ZEV)販売比率を段階的に引き上げることを規定しています。2024年に22%という目標から始まり、2030年までに80%、2035年までに100%となります。こうした段階的目標を達成することで、予測期間中に電気自動車用バッテリーとその部品(陽極など)の需要が大幅に増加することになります。

- さらに、英国では電気自動車普及の動向が顕著です。国際エネルギー機関のデータによると、2023年の同国の電気自動車販売台数は45万台に達し、前年比21.62%の大幅増を記録します。このような軌跡を踏まえると、同国における電気自動車の需要はさらなる成長を遂げ、陽極市場も上昇する可能性が高いです。

- 結論として、現在の動向と予測を踏まえると、英国の電気自動車用バッテリー負極市場は、当分の間、上昇に転じると考えられます。

英国の電気自動車用バッテリー負極産業概要

英国の電気自動車用バッテリー負極市場は半固体化状態です。主要企業(順不同)には、UK Anodes LTD、Jennings Anodes、MG Duff International Ltd、Royston Lead、Nexeonなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の導入を支援する政府の施策

- リチウムイオンバッテリーの価格低下

- 抑制要因

- 欧州大陸におけるバッテリー製造用の原料と関連資源の不足

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- バッテリータイプ

- 鉛蓄バッテリー

- リチウムイオンバッテリー

- その他のバッテリータイプ

- 材料

- 黒鉛

- シリコン

- その他

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- UK Anodes LTD

- Jennings Anodes

- MG Duff International Ltd

- Royston Lead

- Nexeon Ltd

- Tata Group

- DKL Metals Ltd

- Impalloy Ltd.

- Nextrode

- Phillips 66

第7章 市場機会と今後の動向

- 負極材の研究開発

目次

Product Code: 50003832

The United Kingdom Electric Vehicle Battery Anode Market size is estimated at USD 5.66 million in 2025, and is expected to reach USD 11.00 million by 2030, at a CAGR of 14.2% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing adoption of electric vehicles due to the government's In the medium term, the market is poised to benefit from the rising adoption of electric vehicles, spurred by the government's ambitious targets and corresponding investments.

- However, challenges such as land costs, logistics for raw materials, and the absence of subsidies for battery manufacturing may hinder the market's expansion.

- Ongoing research and development in anode materials present promising growth avenues for the market.

United Kingdom Electric Vehicle Battery Anode Market Trends

Lithium Ion Batteries to Dominate the Market

- Lithium-ion batteries are at the forefront of the electric vehicle (EV) revolution. Their superior energy density and extended life cycle make them pivotal as the automotive industry pivots towards sustainable energy solutions. In the United Kingdom, research and development in the lithium-ion battery sector is gaining momentum.

- In September 2023, the Faraday Institution, the United Kingdom's premier institute for electrochemical energy storage research, announced a USD 21 million investment spread across four key battery research projects, with a focus on lithium-ion initiatives. These investments are poised to bolster future demand for anode manufacturing.

- Furthermore, the United Kingdom is drawing in major players to tap into its lithium deposits, a move anticipated to bolster domestic lithium-ion battery production. For example, in June 2023, French multinational Imerys S.A., a leader in industrial minerals, secured an 80% stake in British Lithium. This private firm is at the forefront of sustainably extracting battery-grade lithium from mica granite. Their collaboration aims to set up the UK's first integrated producer of battery-grade lithium carbonate.

- Historically, as the prices of lithium-ion batteries have plummeted, the demand for related components, notably anodes, has surged. Bloomberg NEF reported that in 2023, the average price of lithium-ion batteries was USD 139 USD/KWh, marking a staggering fivefold price drop since 2014. This swift adoption, driven by falling prices, bodes well for the anode market's growth.

- Given these trends in lithium-ion batteries and anode production, India's electric vehicle battery anode market is poised for growth in the coming years.

Government Support to Raise Adoption of Electric Vehicles

- The United Kingdom government has set an ambitious goal to achieve net-zero carbon emissions by 2050, with a particular focus on reducing emissions from the transportation sector. According to the Department for Energy Security & Net-Zero, domestic transport accounted for approximately 29.1% of greenhouse gas emissions, making it the largest contributor among various sectors. In light of this, the UK's push for electric vehicles is anticipated to drive up the demand for battery components, especially anodes, in the coming years.

- For instance, in January 2024, the government introduced a zero-emission vehicle (ZEV) mandate aimed at car manufacturers. This initiative seeks to provide manufacturers with greater certainty while broadening the selection of electric vehicles for consumers.

- Furthermore, the mandate stipulates a gradual increase in the sales proportion of zero-emission vehicles (ZEVs) for manufacturers. Beginning with a target of 22% in 2024, the goal rises to 80% by 2030 and reaches a complete 100% by 2035. Meeting these phased targets is set to significantly boost the demand for electric vehicle batteries and their components, like anodes, during the forecast period.

- Additionally, the trend of rising electric vehicle adoption in the United Kingdom is evident. Data from the International Energy Agency reveals that in 2023, the country's electric car sales hit 450,000 units, marking a substantial 21.62% increase from the prior year. Given this trajectory, the demand for electric vehicles in the country is poised for further growth, which in turn is likely to elevate the anode market.

- In conclusion, given the current trends and projections, the UK Electric Vehicle Battery Anode Market is set for an upswing in the foreseeable future.

United Kingdom Electric Vehicle Battery Anode Industry Overview

The United Kingdom electric vehicle battery anode market is semi-consolidated. Some of the major players (not in particular order) include UK Anodes LTD, Jennings Anodes, MG Duff International Ltd, Royston Lead, and Nexeon.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government policies supporting adoption of electric vehicles

- 4.5.1.2 Declining Lithium-ion Battery Prices

- 4.5.2 Restraints

- 4.5.2.1 Lack of raw materials and associated resources on the European continent for manufacturing batteries

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lead Acid Batteries

- 5.1.2 Lithium-ion Batteries

- 5.1.3 Other Battery Types

- 5.2 Material

- 5.2.1 Graphite

- 5.2.2 Silicon

- 5.2.3 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 UK Anodes LTD

- 6.3.2 Jennings Anodes

- 6.3.3 MG Duff International Ltd

- 6.3.4 Royston Lead

- 6.3.5 Nexeon Ltd

- 6.3.6 Tata Group

- 6.3.7 DKL Metals Ltd

- 6.3.8 Impalloy Ltd.

- 6.3.9 Nextrode

- 6.3.10 Phillips 66

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Research & Development in anode material