|

市場調査レポート

商品コード

1636464

ASEAN諸国の電気自動車用バッテリーセパレータ:市場シェア分析、産業動向、成長予測(2025年~2030年)ASEAN Countries Electric Vehicle Battery Separator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ASEAN諸国の電気自動車用バッテリーセパレータ:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

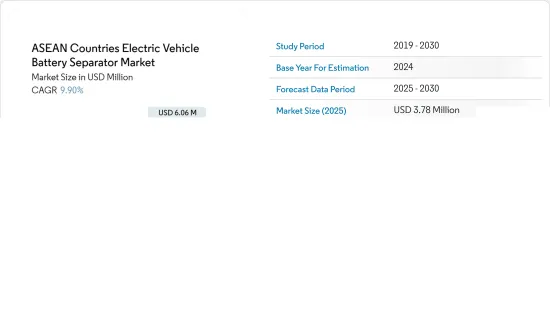

ASEAN諸国の電気自動車用バッテリーセパレータ市場規模は、2025年に378万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.9%で、2030年には606万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車の普及とリチウムイオンバッテリーの価格低下が予測期間の市場を牽引するとみられます。

- 一方、一部の国の独占によって生じるバッテリー材料のサプライチェーン格差(成分不足や流通のボトルネックなど)は、今後の市場成長を抑制すると予想されます。

- 固体バッテリー、先進リチウムイオン化学、ナトリウムイオンバッテリーなど、他のバッテリー化学の研究開発が進んでいることは、将来的に市場に機会をもたらすと予想されます。

- ASEAN諸国の電気自動車用バッテリー分離市場では、地域全体でEVの普及が進んでいることから、タイが大きな成長を遂げると予測されています。

ASEAN諸国の電気自動車用バッテリーセパレータ市場動向

リチウムイオンバッテリータイプが市場を独占

- エネルギー密度が高く、サイクル寿命が長く、自己放電率が低いことで知られるリチウムイオンバッテリーは、電気自動車(EV)に好まれています。この圧倒的な嗜好は、EV用バッテリーセパレータ市場の成長を促進するだけでなく、EV産業の幅広い軌道を形成しています。

- 主要市場参入企業は研究開発投資と生産能力を強化し、競争を激化させて価格を引き下げています。Bloomberg NEFは、EVとバッテリーエネルギー貯蔵システム(BESS)のバッテリーパックの平均価格は概して上昇しているが、2023年には13%も大幅に下落し、139米ドル/kWhになると指摘しています。予測によると、この下落は今後も続き、2025年には113米ドル/kWhに達し、2030年にはさらに80米ドル/kWhまで下落すると予想されています。

- タイ、フィリピン、マレーシア、インドネシア、ベトナムを含むASEAN諸国は、世界のリチウムイオンバッテリーサプライチェーンの主要企業として台頭しつつあります。戦略的立地、政府の優遇措置、豊富な天然資源が、バッテリー製造への投資を誘致することに成功しています。

- 2024年7月、インドネシアは初のEV用バッテリー工場を立ち上げました。東南アジア最大の経済大国であり、世界有数のニッケル埋蔵量を誇るインドネシアは、世界の電気自動車サプライチェーンにおいて重要な役割を担っています。韓国の大手企業LG Energy Solution(LGES)と現代自動車グループの合弁事業であるこの工場は、バッテリーセル生産で10ギガワット時(GWh)の年間生産能力を誇る。このような取り組みは、今後数年間、この地域でのリチウムイオンバッテリー生産を強化する構えです。

- さらに、エネルギー密度の向上、安全機能の改善、充電の高速化といったリチウムイオンバッテリー技術の進歩が、革新的なセパレータ材料の開発に拍車をかけています。リチウムイオンバッテリーのエネルギーと熱の需要を満たすために重要なこれらのセパレータは、安全性と信頼性を確保する上で重要な役割を果たし、それによってセパレータ市場の革新と需要を促進しています。

- 2023年6月、ProLogiumは画期的なバッテリーアーキテクチャを発表し、30年にわたるリチウムイオン技術に大きな進化をもたらしました。従来のポリマーセパレータフィルムをセラミックで代替することで、ProLogiumは電気自動車用リチウムイオンバッテリーセグメントに新たな基準を打ち立てた。このような技術革新は、同地域における先進的なリチウムバッテリー用セパレータの需要を拡大する態勢を整えています。

- こうした開発により、リチウムイオンバッテリーの生産が急増し、予測期間中に電気自動車用バッテリーセパレータの容量が大幅に増加することになります。

著しい成長を遂げるタイ

- 堅調な自動車産業、戦略的位置づけ、政府の支援により、タイはASEAN地域でEV用バッテリーセパレータのトップ生産国に浮上しました。同国がクリーンエネルギーにシフトし、電気自動車を受け入れるにつれて、企業はこの重要なセグメントへの注力を強めています。消費者の関心が高まっている背景には、環境意識の高まり、電気自動車所有の経済的メリット、産業の急速な技術進歩があります。

- 最近、ASEAN地域では電気自動車(EV)の販売が急増しています。例えば、タイ自動車ラボによると、2023年のバッテリー式電気自動車(BEV)の登録台数は7万6,360台に達し、2022年比で6.89倍、2019年比で47.6倍という驚異的な伸びを示しました。BEVを含むEV販売台数の増加が予測される中、同地域のバッテリーとバッテリーセパレータの需要は拡大するとみられます。

- さらに、同地域のバッテリーセパレータは、リチウムイオンバッテリー価格の下落、需要の急増、EV用途における安全性と効率性の重要なニーズなどの課題を克服しています。最近、主要世界企業は、この地域のEV用リチウムイオンバッテリー生産を強化するプロジェクトに投資しています。

- 例えば、BMWは2024年2月、タイのラヨーンに電気自動車用バッテリー工場を新設すると発表しました。この構想により、同国のバッテリーサプライチェーンが強化されると期待されています。BMWはタイをEV用バッテリーの重要な輸出拠点と位置づけ、より大きなアジア太平洋市場を狙っています。このような動きは、タイでのバッテリー生産を後押しし、今後数年間でリチウムイオン・バッテリー用セパレータの需要を高める可能性が高いです。

- さらに、タイの自動車産業は革新的な電気自動車(EV)モデルの生産を強化しています。世界の主要企業がEV製造に軸足を移す中、高級バッテリー部品、特にセパレータの需要が顕著に急増しています。この動向は、産業の革新と持続可能性への取り組みを浮き彫りにしています。

- 例えば、2024年8月、Omodaと中国の自動車メーカーChery Automobileの支社であるJaecoo Thailandは、2つの電気自動車(EV)モデルを発表し、タイでの存在感を強めました。コンパクトSUVのOmoda C5 EVと、オフロードSUVのJaecoo 6 EVです。このような取り組みにより、同地域では電気自動車のラインナップが拡大し、EV用バッテリーセパレータ市場の成長を後押ししています。

- その結果、こうしたプロジェクトや取り組みがEV需要を押し上げ、今後数年間でEV用バッテリーセパレータのニーズを大幅に高めることになると考えられます。

ASEAN諸国の電気自動車用バッテリーセパレータ産業概要

ASEAN諸国の電気自動車用バッテリーセパレータ市場はセミフラグメントです。主要参入企業(順不同)は、Mitsubishi Chemical Group Corporation、Hitachi Chemical Company Ltd、Toray Industries Inc.、Sumitomo Chemical、Teijin Ltdなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- バッテリー原料コストの低下

- 抑制要因

- サプライチェーンのギャップ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- バッテリー

- リチウムイオン

- 鉛-酸

- その他

- 材料タイプ

- ポリプロピレン

- ポリエチレン

- その他の材料タイプ

- 地域

- インドネシア

- ベトナム

- タイ

- ミャンマー

- フィリピン

- その他のASEAN諸国

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Mitsubishi Chemical Group Corporation

- Hitachi Chemical Company Ltd

- Toray Industries Inc.

- Sumitomo Chemical Co. Ltd

- Teijin Ltd

- SK Nexilis

- Asahi Kasei

- W-Scope Corporation

- Southeast Asia Manufacturing Co., Ltd

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- その他のバッテリー化学の研究開発の増加

The ASEAN Countries Electric Vehicle Battery Separator Market size is estimated at USD 3.78 million in 2025, and is expected to reach USD 6.06 million by 2030, at a CAGR of 9.9% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, the growing adoption of electric vehicles and the decreasing price of lithium-ion batteries is expected to drive the market in the forecast period.

- On the other hand, the supply chain gap in battery materials created by the monopolies of some countries, such as ingredient shortages or distribution bottlenecks, is expected to restrain market growth in the future.

- Nevertheless, the increasing research and development of other battery chemistries like solid-state batteries, advanced lithium-ion chemistry, Sodium-ion batteries, etc, are expected to create an opportunity for the market in the future.

- Thailand is anticipated to witness significant growth in the ASEAN countries' electric vehicle battery separation market due to the rising adoption of EVs across the region.

ASEAN Countries Electric Vehicle Battery Separator Market Trends

Lithium-Ion Battery Type to Dominate the Market

- Li-ion batteries, known for their high energy density, long cycle life, and low self-discharge rate, are the preferred choice for electric vehicles (EVs). This dominant preference not only propels the growth of the EV battery separator market but also shapes the broader trajectory of the EV industry.

- Key market players are boosting their R&D investments and production capabilities, intensifying competition and driving prices down. Bloomberg NEF highlights that while average battery pack prices for EVs and battery energy storage systems (BESS) have generally risen, 2023 marked a significant 13% drop, bringing prices down to USD 139/kWh. Projections suggest this decline will persist, with prices anticipated to reach USD 113/kWh by 2025 and plummet further to USD 80/kWh by 2030, driven by relentless technological and manufacturing advancements.

- ASEAN nations, including Thailand, the Philippines, Malaysia, Indonesia, and Vietnam, are emerging as key players in the global lithium-ion battery supply chain. Their strategic locations, government incentives, and abundant natural resources have successfully attracted investments into battery manufacturing.

- In July 2024, Indonesia launched its first-ever EV battery plant. As Southeast Asia's largest economy and the custodian of the world's most extensive nickel reserves, Indonesia is carving out a significant role in the global electric vehicle supply chain. This plant, a joint venture between South Korean titans LG Energy Solution (LGES) and Hyundai Motor Group, boasts a robust annual capacity of 10 Gigawatt hours (GWh) for battery cell production. Such initiatives are poised to bolster lithium-ion battery production in the region in the coming years.

- Moreover, advancements in lithium-ion battery technology, such as heightened energy density, improved safety features, and accelerated charging, are spurring the development of innovative separator materials. These separators, crucial for meeting the energy and thermal demands of Li-ion batteries, play a vital role in ensuring safety and reliability, thereby driving innovation and demand in the separator market.

- In June 2023, ProLogium unveiled a groundbreaking battery architecture, marking a significant evolution in three decades of lithium-ion technology. By substituting the traditional polymer separator film with a ceramic alternative, ProLogium has set a new standard in the lithium-ion battery sector for electric vehicles. Such innovations are poised to amplify the demand for advanced lithium battery separators in the region.

- Given these developments, the production of lithium-ion batteries is set to surge, leading to a substantial increase in the capacity of EV battery separators during the forecast period.

Thailand to Witness Significant Growth

- Thailand, with its robust automotive industry, strategic positioning, and government support, has emerged as the top producer of EV battery separators in the ASEAN region. As the country shifts towards clean energy and embraces electric vehicles, companies are sharpening their focus on this crucial segment. Rising consumer interest is driven by increased environmental awareness, the economic advantages of EV ownership, and swift technological progress in the industry.

- Recently, electric vehicle (EV) sales have surged in the ASEAN region. For instance, the Thailand Automotive Institute reported that in 2023, registered battery electric vehicles (BEVs) reached 76.36 thousand units, marking a 6.89-fold increase from 2022 and a staggering 47.6-fold jump since 2019. With EV sales, including BEVs, projected to rise, the demand for batteries and battery separators in the region is set to amplify.

- Additionally, battery separators in the region are navigating challenges like falling lithium-ion battery prices, escalating demand, and the crucial need for safety and efficiency in EV applications. Recently, leading global companies have invested in projects to enhance lithium-ion battery production for EVs in the region.

- For example, in February 2024, BMW announced a new battery factory for electric vehicles in Rayong, Thailand. This initiative is expected to strengthen the country's battery supply chains. BMW sees Thailand as a key export center for its EV batteries, aiming at the larger Asia Pacific market. Such moves are likely to boost battery production in Thailand and heighten the demand for lithium-ion battery separators in the coming years.

- Furthermore, Thailand's automotive industry is ramping up the production of innovative electric vehicle (EV) models. As global leaders pivot to include EV manufacturing, there's a notable surge in demand for premium battery components, especially separators. This trend highlights the industry's commitment to innovation and sustainability.

- For instance, in August 2024, Omoda and Jaecoo Thailand, a branch of the Chinese automaker Chery Automobile, strengthened their presence in Thailand by launching two electric vehicle (EV) models. The debut included two versions for each model: the compact SUV Omoda C5 EV and the rugged off-road SUV Jaecoo 6 EV, making its global debut in a right-hand drive variant. Such initiatives are expanding their electric vehicle offerings in the region, fueling the growth of the EV battery separator market.

- Consequently, these projects and initiatives are poised to boost EV demand and substantially elevate the need for EV battery separators in the coming years.

ASEAN Countries Electric Vehicle Battery Separator Industry Overview

ASEAN Countries' electric vehicle battery separator market is semi-fragmented. Some key players (not in particular order) are Mitsubishi Chemical Group Corporation, Hitachi Chemical Company Ltd, Toray Industries Inc., Sumitomo Chemical Co. Ltd, Teijin Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Electric Vehicles

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 The Supply Chain Gap

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Others

- 5.2 Material Type

- 5.2.1 Polypropylene

- 5.2.2 Polyethylene

- 5.2.3 Other Material Types

- 5.3 Geography

- 5.3.1 Indonesia

- 5.3.2 Vietnam

- 5.3.3 Thailand

- 5.3.4 Myanmar

- 5.3.5 Philippines

- 5.3.6 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Mitsubishi Chemical Group Corporation

- 6.3.2 Hitachi Chemical Company Ltd

- 6.3.3 Toray Industries Inc.

- 6.3.4 Sumitomo Chemical Co. Ltd

- 6.3.5 Teijin Ltd

- 6.3.6 SK Nexilis

- 6.3.7 Asahi Kasei

- 6.3.8 W-Scope Corporation

- 6.3.9 Southeast Asia Manufacturing Co., Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Research and Development of Other Battery Chemistries