|

市場調査レポート

商品コード

1636444

中国のEV用バッテリーセパレータ:市場シェア分析、産業動向・統計、成長予測(2025~2030年)China Electric Vehicle Battery Separator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のEV用バッテリーセパレータ:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

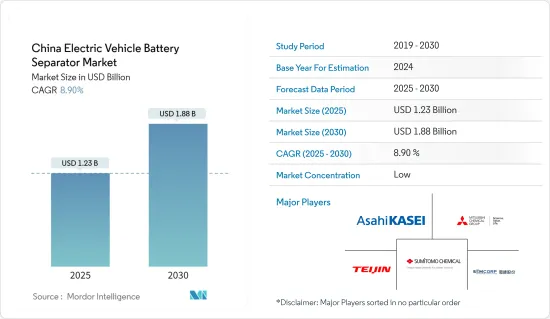

中国のEV用バッテリーセパレータ市場規模は2025年に12億3,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは8.9%で、2030年には18億8,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、電気自動車需要の増加や政府の支援策などの要因が、予測期間中の市場を牽引すると見込まれます。

- その一方で、サプライチェーンの課題が予測期間中の市場成長を阻害する可能性が高いです。

- とはいえ、技術革新と持続可能な材料の開発は、今後数年間、市場に大きな機会をもたらすと予想されます。

中国のEV用バッテリーセパレータ市場動向

電気自動車需要の増加

- 中国は世界最大の電気自動車(EV)市場であり、EVバッテリーの需要急増がバッテリーセパレータ市場の成長を後押ししています。国際エネルギー機関(IEA)の報告によると、中国は2023年に810万台の電気自動車を販売し、これにはバッテリー電気自動車(BEV)とプラグインハイブリッド電気自動車(PHEV)の両方が含まれます。

- EVの需要増加に伴い、バッテリー性能を高める高機能セパレータのニーズが高まっています。これらのセパレータは、特に自動車メーカーが航続距離、効率、安全性の向上に注力する中で、短絡を防ぎバッテリーの安定性を確保する上で重要な役割を果たしています。

- 中国は世界の電気自動車の半分以上を占め、新エネルギー車(NEV)の2025年販売目標を上回っています。この躍進は、政府のインセンティブと支援政策によって後押しされています。

- 例えば、2023年6月、国内のEV販売をさらに刺激することを目的として、財政部(財務省)、国家税務総局(STA)、工業情報化部(MIIT)の連合は、"新エネルギー車に対する自動車購入税減免政策"の延長を発表しました。この免税措置は2024年1月1日から適用され、2027年12月31日まで継続されます。

- さらに、政府の強力なバックアップに支えられた中国の野心的なEV導入目標は、バッテリー製造セクターの成長に拍車をかけています。この急成長は、生産能力の拡大、先駆的な研究開発、バッテリー技術の限界への課題に向けられた多額の投資からも明らかです。

- 注目すべき動きとして、2024年8月、中国の有名なハイテク企業であるシャオミが、北京で2つ目のEV工場を着工しました。北京市当局の文書によると、すでにスマートフォンの分野で圧倒的な強さを誇るシャオミは、7月25日に土地を確保し、その翌日にはすぐに建設に着手しました。戦略上、この新しい施設はシャオミの最初のEV工場のすぐ隣に建っています。高まるEV需要に対応するため、メーカー各社が増産に乗り出すなか、バッテリーセパレータの重要性はますます明らかになっています。

- このように、EV産業が技術革新と性能に重点を置いて進化するにつれて、バッテリーセパレータは極めて重要なプレーヤーとして台頭し、中国市場の成長に拍車をかけています。EV市場が上昇基調にある中、こうした重要なバッテリー部品の需要は急増する見通しです。

市場を独占するリチウムイオンバッテリーセグメント

- 中国では、急成長する電気自動車(EV)のエコシステムにおいて、リチウムイオンバッテリーセグメントが重要な役割を果たしています。2023年には、電気自動車の新規登録台数の60%を中国が占める。世界有数の電気自動車の生産国・消費国である中国の影響力は、電気自動車のエネルギー源として不可欠なリチウムイオンバッテリーの進化と受容において最も重要です。

- エネルギー密度と効率で知られるリチウムイオンバッテリーは、安全性と信頼性において高性能セパレータに依存しています。これらのセパレータは、負極と正極間の短絡を防ぐだけでなく、充放電中の効率的なイオン移動を促進します。

- 中国では、ポリエチレン(PE)やポリプロピレン(PP)などのセパレータ素材の進歩により、リチウムイオンバッテリーの性能、耐久性、熱安定性が向上しています。

- 例えば2024年1月、中国科学院(CAS)の現代物理学研究所(IMP)と先進エネルギー科学技術広東研究所のチームが、新しいポリエチレンテレフタレート(PET)セパレータを発表しました。リチウムイオン・バッテリー用に設計されたこのセパレータは、高温に耐えることができ、電気自動車の性能と消費者の魅力を直接的に高める。

- 注目すべきは、リチウムイオンバッテリーの平均価格が一貫して下落していることで、2023年には1kWhあたり約139米ドルに達します。これは2013年以来82%以上の下落を意味します。この動向は今後も続き、2025年には113米ドル/kWhを下回り、2030年には80米ドル/kWhに達する可能性があると予測されています。リチウムイオンバッテリーの価格が下がり、電気自動車がより身近なものになるにつれ、バッテリーセパレータの需要も急増します。コストの最適化と性能の向上に熱心なメーカーがこの需要を牽引しています。

- さらに、自動車販売台数の40%を電気自動車にするという中国の野望は、EV用バッテリーとその部品(セパレータを含む)の需要増加をさらに際立たせています。

- このように、技術的な進歩、急成長するEV市場、バッテリー価格の急落により、中国のバッテリーセパレータ市場は大きく拡大しようとしています。

中国のEV用バッテリーセパレータ産業の概要

中国のEV用バッテリーセパレータ市場は細分化されています。主なプレーヤー(順不同)には、上海能源新材料技術有限公司(SEMCORP)、帝人株式会社、住友化学株式会社、三菱化学株式会社、旭化成株式会社などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 電気自動車需要の増加

- 政府の支援策

- 抑制要因

- サプライチェーンの課題

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ別

- リチウムイオンバッテリー

- 鉛蓄電池

- その他

- 材料タイプ別

- ポリプロピレン

- ポリエチレン

- その他の材料タイプ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Shanghai Energy New Materials Technology Co., Ltd.(SEMCORP)

- Teijin Limited

- Sumitomo Chemical Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Asahi Kasei Corporation

- Entek International

- Shanghai PTL New Energy Technology Co., Ltd.

- Toray Industries Inc.

- UBE Corp

- SK Innovation Co. Ltd

- 市場ランキング/シェア分析

- その他の有名企業一覧

第7章 市場機会と今後の動向

- 新興電池材料の拡大

目次

Product Code: 50003711

The China Electric Vehicle Battery Separator Market size is estimated at USD 1.23 billion in 2025, and is expected to reach USD 1.88 billion by 2030, at a CAGR of 8.9% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing demand for electric vehicles and suppotive government initiatives are expected to drive the market during the forecast period.

- On the other hand, supply chain challanges are likely to hinder the market growth during the forecast period.

- Nevertheless, technological innovations and development of sustainable materials are expected to provide significant opportunities for the market in the coming years.

China Electric Vehicle Battery Separator Market Trends

Increasing Demand for Electric Vehicles

- China stands as the world's largest electric vehicle (EV) market, with the surging demand for EV batteries propelling the growth of the battery separator market. The International Energy Agency reported that in 2023, China sold 8.1 million electric vehicles, encompassing both Battery Electric Vehicles (BEV) and Plug-in Hybrid Electric Vehicles (PHEV).

- With the rising demand for EVs comes an increased need for sophisticated separators that enhance battery performance. These separators play a crucial role in preventing short circuits and ensuring battery stability, especially as automakers focus on improving vehicle range, efficiency, and safety.

- China dominates the global EV landscape, boasting over half of the world's electric automobiles and surpassing its 2025 sales target for new energy vehicles (NEVs). This surge is bolstered by government incentives and supportive policies.

- For example, in June 2023, aiming to further stimulate domestic EV sales, a coalition of the Ministry of Finance (MOF), State Taxation Administration (STA), and Ministry of Industry and Information Technology (MIIT) announced an extension of the "Vehicle Purchase Tax Reduction and Exemption Policy for New Energy Vehicles." This tax exemption, effective from January 1, 2024, is set to continue until December 31, 2027.

- Furthermore, China's ambitious EV adoption targets, underpinned by robust government backing, have catalyzed the growth of its battery manufacturing sector. This surge is evident in substantial investments directed towards expanding production capacities, pioneering research & development, and pushing the boundaries of battery technologies.

- In a notable move, in August 2024, Xiaomi, the renowned Chinese tech titan, broke ground on its second EV plant in Beijing. Documents from the Beijing city authorities reveal that Xiaomi, already a dominant player in the smartphone arena, secured the land on July 25 and promptly initiated construction the very next day. Strategically, this new facility is rising right next to Xiaomi's inaugural EV plant. As manufacturers ramp up to cater to the escalating EV demand, the significance of battery separators becomes increasingly evident.

- Thus, as the EV industry evolves with a keen focus on innovation and performance, battery separators emerge as pivotal players, fueling market growth in China. With the EV market on an upward trajectory, the demand for these critical battery components is set to soar.

Lithium-Ion Batteries Segment to Dominate the Market

- In China, the lithium-ion battery segment plays a crucial role in the burgeoning electric vehicle (EV) ecosystem. In 2023, China accounted for 60% of all new electric car registrations. As a leading global producer and consumer of electric vehicles, China's influence is paramount in the evolution and acceptance of lithium-ion batteries, which are indispensable for energizing these vehicles.

- Lithium-ion batteries, known for their energy density and efficiency, depend on high-performance separators for safety and reliability. These separators not only prevent short circuits between the anode and cathode but also facilitate efficient ion transfer during charging and discharging.

- In China, advancements in separator materials like polyethylene (PE) and polypropylene (PP) have enhanced the performance, durability, and thermal stability of lithium-ion batteries.

- For example, in January 2024, a team from the Institute of Modern Physics (IMP) at the Chinese Academy of Sciences (CAS) and the Advanced Energy Science and Technology Guangdong Laboratory unveiled new polyethylene terephthalate (PET) separators. These separators, designed for lithium-ion batteries, can endure high temperatures, directly boosting electric vehicle performance and consumer appeal.

- Notably, the average price of lithium-ion batteries has consistently fallen, hitting approximately USD 139 per kWh in 2023. This marks an over 82% drop since 2013. Projections suggest this trend will persist, with prices potentially dipping below USD 113/kWh by 2025 and reaching USD 80/kWh by 2030. As lithium-ion battery prices decline, making electric vehicles more accessible, there's a corresponding surge in demand for battery separators. Manufacturers, keen on optimizing costs and boosting performance, are driving this demand.

- Moreover, China's ambition to have 40% of all vehicle sales be electric further underscores the rising demand for EV batteries and their components, including separators.

- Thus, with technological strides, a burgeoning EV market, and plummeting battery prices, China's battery separator landscape is set for significant expansion.

China Electric Vehicle Battery Separator Industry Overview

The Chinese electric vehicle battery separator market is semi-fragmented. Some of the major players (not in particular order) include Shanghai Energy New Materials Technology Co., Ltd. (SEMCORP), Teijin Limited, Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group Corporation, and Asahi Kasei Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand of Electric Vehicles

- 4.5.1.2 Supportive Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Challanges

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Others

- 5.2 Material Type

- 5.2.1 Polypropylene

- 5.2.2 Polyethylene

- 5.2.3 Other Material Types

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Shanghai Energy New Materials Technology Co., Ltd. (SEMCORP)

- 6.3.2 Teijin Limited

- 6.3.3 Sumitomo Chemical Co., Ltd.

- 6.3.4 Mitsubishi Chemical Group Corporation

- 6.3.5 Asahi Kasei Corporation

- 6.3.6 Entek International

- 6.3.7 Shanghai PTL New Energy Technology Co., Ltd.

- 6.3.8 Toray Industries Inc.

- 6.3.9 UBE Corp

- 6.3.10 SK Innovation Co. Ltd

- 6.4 Market Ranking/Share Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion in Emerging Battery Materials