|

市場調査レポート

商品コード

1636443

インドの電気自動車用バッテリーセパレータ:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Electric Vehicle Battery Separator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの電気自動車用バッテリーセパレータ:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

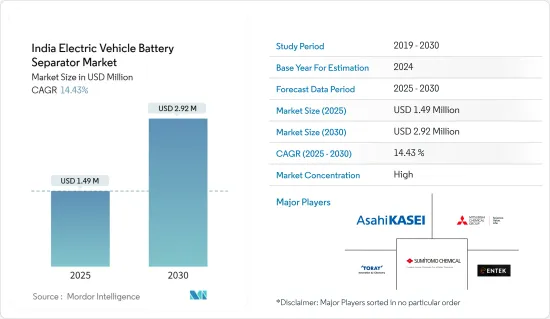

インドの電気自動車用バッテリーセパレータ市場規模は2025年に149万米ドルと推定され、予測期間(2025~2030年)のCAGRは14.43%で、2030年には292万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車需要の増加や政府の支援策などの要因が、予測期間中の市場を牽引すると予想されます。

- 一方、国内企業の参入が限定的であることが、予測期間中の市場成長の妨げになるとみられます。

- 技術革新とサステイナブル材料の開発は、今後数年間で市場に大きな機会をもたらすと予想されます。

インドの電気自動車用バッテリーセパレーター市場動向

電気自動車需要の増加

- インドは世界のCO2排出量上位5に入る。喫緊の課題である大気汚染に対応するため、インド政府は電気自動車(EV)の普及を促進する施策を積極的に推進しています。電気自動車製造者協会(SMEV)は、インドが2023年に167万台のEV販売を達成すると報告しています。

- 充電ステーションの設置を検討している企業は、政府から明確な説明を受けています。さらに政府は、2030年までにすべての新車販売を完全な電気自動車にするという野心的な目標を掲げています。

- インド政府は2030年までに、自家用車の販売台数の30%、商用車の販売台数の70%、二輪車と三輪車の販売台数の80%を電気自動車にすることを目指しています。このような野心的な目標により、インドではバッテリーの需要が高まり、バッテリーの効率と寿命を確保するために重要な高品質のバッテリーセパレータの必要性が高まっている

- 2019年4月、インドは「インドにおける電気自動車の迅速な導入と製造」(FAMEインド)計画の第2段階を開始しました。この構想は、ハイブリッド車や電気自動車の購入価格を引き下げることを目的としており、特に公共輸送(バス、リキシャ、タクシーなど)や自家用二輪車に焦点を当てています。

- 2024年2月、政府はFAME IIスキームへの投資額を1,000億インドルピー(12億650万米ドル)から1,150億インドルピー(13億8,740万米ドル)に引き上げると発表しました。この計画は、電気自動車の普及を促進するだけでなく、必要不可欠な充電インフラの整備にも重点を置いています。さらに、政府は補助金のインセンティブを1kWhあたり1万インドルピーから1万5,000ルピーに引き上げました。こうした措置により、インドでは電気自動車の導入が大幅に促進され、それに伴いリチウムイオンバッテリーの需要も増加すると予想されます。

- こうした需要急増を受け、バッテリーメーカー各社はバッテリー部品生産設備の設置を積極的に進めています。例えば、インドのHimadri Speciality Chemicalsは2024年2月、年産2,000トンのリチウムイオンバッテリー部品製造施設の計画を発表しました。このプロジェクトは480億インドルピー(5億7,910万米ドル)と見積もられ、約6年かけて展開される予定です。

- 技術革新と性能に強く焦点を当てたEV産業のダイナミックな進化を考えると、バッテリーセパレーターは、インドの市場成長を推進する極めて重要な参入企業として浮上しています。EV市場が上昇基調を続ける中、こうした重要なバッテリー部品の需要は急増するとみられます。

市場を独占するリチウムイオンバッテリーセグメント

- 従来、リチウムイオンバッテリーは携帯電話やパソコンなどの民生用電子機器製品に電力を供給していました。しかし、その役割は進化し、ハイブリッド車や完全電気自動車(EV)の電源として好まれるようになりました。この変化は、CO2や窒素酸化物などの温室効果ガスを排出しないEVの環境上の利点によるところが大きいです。

- リチウムイオンバッテリーは、その有利な容量対重量比のおかげで、他のタイプのバッテリーを凌いで普及しています。リチウムイオンバッテリーの採用は、優れた性能、長寿命、価格下落によってさらに加速しています。エネルギー密度が高く、サイクル寿命が長いリチウムイオンバッテリーは、EVメーカーにとって最適な選択肢となっています。世界のEV市場をリードするインドでは、リチウムイオンバッテリー、ひいてはバッテリー用セパレータの需要が増加しています。

- この動向を後押ししている大きな要因は、リチウムイオンバッテリーの価格が一貫して下落していることです。過去10年間で、技術の進歩、規模の経済、製造プロセスの洗練がコストを引き下げました。

- 世界規模で見ても、リチウムイオンバッテリーの価格は過去10年間で劇的に下落しています。2023年には、平均的なリチウムイオンバッテリーの価格は1kWhあたり約139米ドルとなり、2013年の水準から82%も下落しました。

- BloombergNEFは、2025年以降、バッテリーコストが再び低下すると予測しています。これは、新たな採掘・精製能力が活性化し、リチウム価格が軟化するためです。同社の2023年バッテリー価格調査では、2025年までに平均パック価格が113米ドル/kWhを下回り、2030年までにさらに80米ドル/kWhまで下がると予測しています。

- この価格低下により、電気自動車は予算内で購入しやすくなり、インドでの普及に拍車がかかっています。電気自動車を導入する消費者や企業が増加する中、リチウムイオンバッテリーの生産と需要が急増し、バッテリーセパレーター市場はさらに活性化しています。

- その結果、リチウムイオンバッテリーはインドの電気自動車用バッテリーの中心的存在であり続け、最先端のセパレータの需要を促進し、市場での優位性を確固たるものにしています。

インドの電気自動車用バッテリーセパレーター産業概要

インドの電気自動車用バッテリーセパレーター市場は半固体化しています。主要参入企業(順不同)としては、Sumitomo Chemical、Mitsubishi Chemical Group Corporation、Asahi Kasei Corp.、Toray Industries, Inc.、Entek International LLCなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車需要の増加

- 政府の支援策

- 抑制要因

- 限られた企業の参入

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- バッテリータイプ

- リチウムイオンバッテリー

- 鉛蓄バッテリー

- その他

- 材料タイプ

- ポリプロピレン

- ポリエチレン

- その他の材料タイプ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Sumitomo Chemical Co., Ltd.

- Asahi Kasei Corporation

- Mitsubishi Chemical Group Corporation

- Entek International

- Toray Industries Inc.

- 24M Technologies

- Celgard LLC

- SK Innovation Co. Ltd

- UBE Corp

- LG Chem Ltd.

- その他の著名な企業一覧

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 新興バッテリー材料の拡大

The India Electric Vehicle Battery Separator Market size is estimated at USD 1.49 million in 2025, and is expected to reach USD 2.92 million by 2030, at a CAGR of 14.43% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing demand for electric vehicles and supportive government initiatives are expected to drive the market during the forecast period.

- On the other hand, limited domestic company participation is likely to hinder market growth during the forecast period.

- Nevertheless, technological innovations and the development of sustainable materials are expected to provide significant opportunities for the market in the coming years.

India Electric Vehicle Battery Separator Market Trends

Increasing Demand for Electric Vehicles

- India ranks among the world's top five CO2 emitters. In response to the pressing issue of air pollution, the Indian government is actively promoting policies to boost the number of electric vehicles (EVs) on the roads. The Society of Manufacturers of Electric Vehicles (SMEV) reported that India achieved sales of 1.67 million EVs in 2023.

- Entities looking to establish charging stations have received clarity from the government: licensing from the ministry may not be necessary. Furthermore, the government has set an ambitious goal: by 2030, all new vehicle sales will be fully electric.

- By 2030, the Indian government aims for electric vehicles to make up 30% of private car sales, 70% of commercial vehicle sales, and a remarkable 80% of sales for two-and three-wheelers. These ambitious targets are poised to boost the demand for batteries in India and heightened the need for high-quality battery separators, which are crucial for ensuring battery efficiency and longevity.

- In April 2019, India rolled out the second phase of its "Faster Adoption and Manufacturing of Electric Vehicles in India" (FAME India) scheme. This initiative aims to lower the purchase price of hybrid and electric vehicles, particularly focusing on public transportation (like buses, rickshaws, and taxis) and private two-wheelers.

- In February 2024, the government announced a boost in investment for the FAME II scheme, raising it from INR 10,000 crore (USD 1206.5 million) to INR 11,500 crore (USD 1387.4 million). This scheme not only focuses on enhancing the adoption of electric vehicles but also emphasizes the establishment of essential charging infrastructure. Additionally, the government has upped the subsidy incentives from Rs 10,000 per kWh to Rs 15,000 per kWh. Such measures are anticipated to significantly bolster the adoption of electric vehicles in India, subsequently driving up the demand for lithium-ion batteries.

- In light of this surging demand, battery manufacturers are proactively setting up facilities for battery component production. For example, in February 2024, Himadri Speciality Chemicals, an Indian firm, unveiled plans for a lithium-ion battery component manufacturing facility, boasting a capacity of 2 lakh tonnes per annum. The project, estimated at INR 4,800 crore (USD 579.1 million), is set to unfold over approximately six years.

- Given the dynamic evolution of the EV industry, with its strong focus on innovation and performance, battery separators are emerging as pivotal players, propelling market growth in India. As the EV market continues its upward trajectory, the demand for these vital battery components is set to surge.

Lithium-Ion Batteries Segment to Dominate the Market

- Traditionally, lithium-ion batteries powered consumer electronics like mobile phones and PCs. However, their role has evolved, becoming the preferred power source for hybrid and fully electric vehicles (EVs). This shift is largely attributed to the environmental benefits of EVs, which produce no CO2, nitrogen oxides, or other greenhouse gases.

- Lithium-ion batteries are outpacing other battery types in popularity, thanks to their favorable capacity-to-weight ratio. Their adoption is further fueled by superior performance, extended shelf life, and plummeting prices. With high energy density and long cycle life, lithium-ion batteries have become the go-to choice for EV manufacturers. As India spearheads the global EV market, the demand for lithium-ion batteries-and by extension, battery separators-is on the rise.

- A major factor bolstering this trend is the consistent drop in lithium-ion battery prices. Over the last decade, technological advancements, economies of scale, and refined manufacturing processes have driven down costs.

- On a global scale, lithium-ion battery prices have seen a dramatic decline over the past decade. In 2023, an average lithium-ion battery was priced at approximately USD 139 per kWh, marking an impressive 82% drop from 2013 levels.

- Looking ahead, BloombergNEF projects a renewed decline in battery costs starting 2025. This is attributed to the activation of new extraction and refinery capacities, leading to a softening of lithium prices. Their 2023 Battery Price Survey forecasts the average pack price to dip below USD 113/kWh by 2025 and further down to USD 80/kWh by 2030.

- This price reduction has made electric vehicles more budget-friendly, spurring their widespread adoption in India. With a growing number of consumers and businesses embracing EVs, the surge in lithium-ion battery production and demand has further bolstered the market for battery separators.

- Consequently, lithium-ion batteries remain central to India's EV battery landscape, propelling the demand for cutting-edge separators and solidifying their dominant market position.

India Electric Vehicle Battery Separator Industry Overview

The Indian electric vehicle battery separator market is semi-consolidated. Some of the major players (not in particular order) include Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group Corporation, Asahi Kasei Corporation, Toray Industries, Inc., and Entek International LLC among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand of Electric Vehicles

- 4.5.1.2 Supportive Government Initiatives

- 4.5.2 Restraints

- 4.5.2.1 Limited Company Participation

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-Ion Batteries

- 5.1.2 Lead-Acid Batteries

- 5.1.3 Others

- 5.2 Material Type

- 5.2.1 Polypropylene

- 5.2.2 Polyethylene

- 5.2.3 Other Material Types

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Sumitomo Chemical Co., Ltd.

- 6.3.2 Asahi Kasei Corporation

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 Entek International

- 6.3.5 Toray Industries Inc.

- 6.3.6 24M Technologies

- 6.3.7 Celgard LLC

- 6.3.8 SK Innovation Co. Ltd

- 6.3.9 UBE Corp

- 6.3.10 LG Chem Ltd.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion in Emerging Battery Materials