|

市場調査レポート

商品コード

1636181

SLI用鉛蓄電池セパレータの世界市場:市場シェア分析、産業動向、成長予測(2025年~2030年)Global Lead-Acid Battery Separator For SLI Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| SLI用鉛蓄電池セパレータの世界市場:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

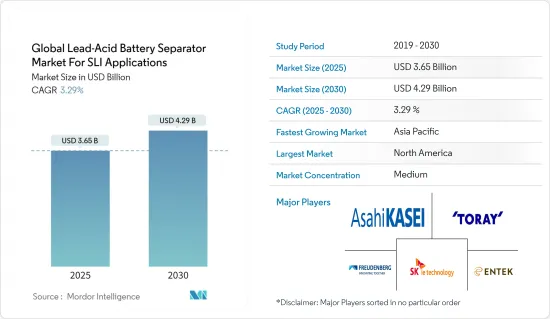

SLI用途向け鉛蓄電池セパレータの世界市場は、予測期間(2025~2030年)のCAGR 3.29%で、2025年の36億5,000万米ドルから2030年には42億9,000万米ドルに成長すると予測されます。

主要ハイライト

- 中期的には、オートメーションセグメントの成長率上昇や鉛蓄電池の費用対効果といった要因が、予測期間中のSLI用途向け鉛蓄電池セパレータ世界市場の最も大きな促進要因の1つになると予想されます。

- 一方、電池セパレータ製造のための複雑なサプライチェーン制約が、予測期間中の市場調査を脅かします。

- 強化された電池セパレータ材料の開発には継続的な努力が払われています。この要因によって、世界の鉛蓄電池用セパレータ市場には、将来的にSLIアプリケーションのためのいくつかの機会が生まれると予想されます。

- アジア太平洋は大きな成長が見込まれ、予測期間中に最も高いCAGRで推移する可能性が高いです。これは、同地域の電池と関連機器・材料の製造産業が大きいためです。

世界の鉛蓄電池セパレータ市場動向

ポリプロピレンセグメントが著しい成長を遂げる

- ポリプロピレンは近年、世界の鉛蓄電池セパレータ市場、特に始動・点灯・点火(SLI)用途で欠かせない存在となっています。この汎用性の高い熱可塑性ポリマーは、優れた耐薬品性、高い機械的強度、優れた電気絶縁性など、最適な特性を備えています。

- ポリプロピレンの汎用性は、様々な添加剤や表面処理を取り入れることで、その性能特性を高め、電池の寿命を延ばすことを可能にします。この適応性により、製品の効率と耐久性の向上を目指す電池メーカーにとって、ポリプロピレンは魅力的な選択肢となっています。自動車産業が、より効率的で環境に優しい自動車を生産するというプレッシャーの高まりに直面する中、高性能SLI電池の需要が伸びており、セパレータ市場におけるポリプロピレンの地位はさらに強固なものとなっています。

- 世界の自動車生産台数の増加に伴い、SLI用途の電池需要が急増し、電池セパレータ材料におけるポリプロピレンのニーズが高まっています。これは、効率的で耐久性の高い電池部品を必要とする電気自動車やハイブリッド車の生産台数が増加していることが背景にあります。さらに、電池技術の進歩が高品質ポリプロピレン製セパレータの需要をさらに押し上げています。

- 国際自動車工業協会によると、世界の自動車生産台数はパンデミック前の水準を超えました。今後も同様の成長傾向が続くと予想されます。例えば、2019~2023年にかけて、年間生産能力は2%以上増加したのに対し、2022~2023年にかけての成長率は10%を超えており、自動車の生産が拡大していることを示しています。

- 現在進行中の研究開発は、ポリプロピレンセパレータ技術の改良に重点を置いています。ナノ複合材料の開発や先進的表面改質など、ポリプロピレンセパレータのすでに素晴らしい能力を強化するための研究が行われています。これらの技術革新は、電池の性能、寿命、安全性を向上させ、鉛蓄電池技術に依存する自動車産業やその他のセグメントの進化するニーズに応えることを目的としています。

- 例えば2024年2月、仁川大学の科学者たちは、電池セパレータの安定性と特性を向上させる方法を開拓しました。その方法は、二酸化ケイ素と他の特殊な分子の層を塗布することです。エネルギー貯蔵材料』誌に掲載されたこの研究結果は、ポリプロピレン(PP)セパレータに効果的なグラフト重合を行い、二酸化ケイ素(SiO2)の一貫した層を導入したことを示しています。

- したがって、以上の点から、ポリプロピレンセパレータ材料セグメントは予測期間中に成長すると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は、世界の鉛蓄電池用セパレータ市場、特にSLI用途のポリプロピレンセグメントで圧倒的な強さを見せています。この成長の主要要因は、同地域の自動車産業の活況、急速な工業化、エネルギー貯蔵ニーズの増加です。

- 国際自動車工業会(International Organization of Motor Vehicle Manufacturers)によると、アジア太平洋の自動車生産台数は2022~2023年にかけて大幅に増加しました。2023年、同地域は5,511万5,837台の自動車を製造し、10%の成長率を再開しました。2019~2023年にかけてのCAGRは12%を超えており、同地域における歯車需要の高まりを意味しています。

- 中国、日本、韓国、インドがこの市場拡大の最前線にいます。これらの国の堅調な製造部門と国内自動車需要の拡大は、ポリプロピレン電池セパレータの取り込みに大きく寄与しています。

- 特に中国は、この地域の市場力学を形成する上で重要な役割を果たしています。世界最大の自動車市場であり、鉛蓄電池の重要な生産国である中国では、近年、高品質のポリプロピレン製セパレータに対する需要が急増しています。電気自動車とハイブリッド技術を推進する中国は、逆説的にSLI電池市場を強化しています。

- 技術力の高さで知られる日本と韓国は、ポリプロピレンセパレータ製造の技術革新を牽引してきました。これらの国々の企業は、耐パンク性の向上や電気抵抗の低減など、性能特性を強化したセパレータ材料の開発に注力してきました。こうした進歩は、国内市場に貢献するとともに、域内外の国々へ高品質なセパレータを輸出する重要な役割を担っています。

- 例えば、2024年1月、韓国の仁川大学の科学者は、セパレータの安定性と特性を向上させる技術を開発しました。二酸化ケイ素やその他の特殊な分子の層を組み込むことで、このセパレータを使用した電池は性能が向上し、侵入性の根のような構造の成長が抑制されました。この画期的な成果は、電気自動車や最先端のエネルギー貯蔵ソリューションの普及に不可欠な、安全性の高い電池の開発につながるものです。

- したがって、前述のように、予測期間中はアジア太平洋が市場を独占すると予想されます。

世界の鉛蓄電池セパレータ産業概要

SLI用途の世界の鉛蓄電池セパレータ市場は、半分断型です。この市場の主要企業(順不同)には、Asahi Kasei Corporation、Toray Battery Separator Film、Freudenberg Performance Materials、SK ie Technology Corporation Ltd、Entek Internationalなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 自動車産業の成長

- 費用対効果

- 抑制要因

- サプライチェーンの制約

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 材料

- ポリエチレン

- ポリプロピレン

- その他

- 2029年までの市場規模・需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ノルディック

- ロシア

- トルコ

- その他の欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- カタール

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略とSWOT分析

- 企業プロファイル

- Asahi Kasei Corporation

- Toray Battery Separator Film Co. Ltd

- Freudenberg Performance Materials

- SK ie Technology Corporation Ltd

- Entek International

- Sumitomo Chemical Co. Ltd

- Ube Maxell Co. Ltd

- W-Scope Corporation

- Daramic

- Amer SIL

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 強化型セパレータ材料の開発

The Global Lead-Acid Battery Separator Market For SLI Applications Industry is expected to grow from USD 3.65 billion in 2025 to USD 4.29 billion by 2030, at a CAGR of 3.29% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising growth in the automation sector and the cost-effectiveness of lead-acid batteries are expected to be among the most significant drivers for the global lead-acid battery separator market for SLI applications during the forecast period.

- On the other hand, complex supply chain constraints for manufacturing battery separators threaten the market studied during the forecast period.

- Nevertheless, continued efforts are being made to develop enhanced battery separator materials. This factor is expected to create several opportunities for SLI applications in the global lead-acid battery separator market in the future.

- Asia-Pacific is expected to witness significant growth and will likely register the highest CAGR during the forecast period. This is due to the region's considerable battery and associated equipment and materials manufacturing industry.

Global Lead-Acid Battery Separator Market Trends

Polypropylene Segment to Witness Significant Growth

- Polypropylene has become essential in the global lead-acid battery separator market, especially for Starting, Lighting, and Ignition (SLI) applications in recent years. This versatile thermoplastic polymer offers optimal properties, including excellent chemical resistance, high mechanical strength, and good electrical insulation.

- Polypropylene's versatility allows for incorporating various additives and surface treatments, enhancing its performance characteristics and extending battery life. This adaptability has made it an attractive option for battery manufacturers looking to improve their products' efficiency and durability. As the automotive industry faces increasing pressure to produce more efficient and environmentally friendly vehicles, the demand for high-performance SLI batteries has grown, further solidifying polypropylene's position in the separator market.

- As global automobile manufacturing escalates, the demand for batteries in SLI applications is set to surge, consequently boosting the need for polypropylene in battery separator materials. This increase is driven by the growing production of electric and hybrid vehicles requiring efficient and durable battery components. Additionally, advancements in battery technology are further propelling the demand for high-quality polypropylene separators.

- According to the International Organization of Motor Vehicle Manufacturers, global automobile manufacturing has surpassed the pre-pandemic level. It is expected to continue on a similar growth trend in the coming years. For instance, between 2019 and 2023, the annual production capacity increased by more than 2%, whereas the growth rate between 2022 and 2023 was over 10%, signifying the growing production of automobiles.

- Ongoing research and development efforts are focused on improving polypropylene separator technology. Areas of exploration include developing nanocomposite materials and advanced surface modifications to enhance polypropylene separators' already impressive capabilities. These innovations aim to improve battery performance, longevity, and safety, meeting the evolving needs of the automotive industry and other sectors reliant on lead-acid battery technology.

- For instance, in February 2024, Scientists at Incheon National University pioneered a method to enhance battery separators' stability and properties. Their approach involves applying a layer of silicon dioxide and other specialized molecules. The findings, detailed in a publication in Energy Storage Materials, showcase the effective graft polymerization on a polypropylene (PP) separator, introducing a consistent layer of silicon dioxide (SiO2).

- Therefore, as per the above points, the polypropylene separator material segment is expected to grow during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific region has emerged as a dominant force in the global lead-acid battery separator market, particularly in the polypropylene segment for SLI applications. This growth is primarily driven by the region's booming automotive industry, rapid industrialization, and increasing energy storage needs.

- According to the International Organization of Motor Vehicle Manufacturers, automobile manufacturing in Asia-Pacific significantly rose between 2022 and 2023. In 2023, the region manufactured 55,115,837 automobiles, resuming a 10% growth rate. The annual average growth rate between 2019 and 2023 was over 12%, signifying the rising demand for gears in the region.

- China, Japan, South Korea, and India are at the forefront of this market expansion. Their robust manufacturing sectors and growing domestic vehicle demand contribute significantly to the uptake of polypropylene battery separators.

- China, in particular, plays a crucial role in shaping the regional market dynamics. As the world's largest automobile market and a significant producer of lead-acid batteries, China's demand for high-quality polypropylene separators has surged in recent years. The country's push toward electric vehicles and hybrid technologies has paradoxically bolstered the SLI battery market, as these vehicles still require traditional lead-acid batteries for their 12V systems.

- Japan and South Korea, known for their technological prowess, have driven innovations in polypropylene separator manufacturing. Companies in these countries have focused on developing separator materials with enhanced performance characteristics, such as improved puncture resistance and reduced electrical resistance. These advancements have served their domestic markets and positioned them as key exporters of high-quality separators to other countries in the region and beyond.

- For instance, in January 2024, Incheon National University scientists in South Korea pioneered a technique to enhance separator stability and characteristics. By incorporating a layer of silicon dioxide and other specialized molecules, batteries utilizing these separators showcased enhanced performance and curbed the growth of intrusive root-like structures. This breakthrough sets the stage for developing high-safety batteries, which are crucial for the widespread acceptance of electric vehicles and cutting-edge energy storage solutions.

- Therefore, as mentioned above, the Asia-Pacific region is expected to dominate the market during the forecast period.

Global Lead-Acid Battery Separator Industry Overview

The global lead-acid battery separator market for SLI applications is semi-fragmented. Some key players in this market (in no particular order) are Asahi Kasei Corporation, Toray Battery Separator Film Co. Ltd, Freudenberg Performance Materials, SK ie Technology Corporation Ltd, and Entek International.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growth in Automotive Industry

- 4.5.1.2 Cost Effectiveness

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Constraints

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Material

- 5.1.1 Polyethylene

- 5.1.2 Polypropylene

- 5.1.3 Others

- 5.2 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 NORDIC

- 5.2.2.7 Russia

- 5.2.2.8 Turkey

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Australia

- 5.2.3.4 Japan

- 5.2.3.5 South Korea

- 5.2.3.6 Malaysia

- 5.2.3.7 Thailand

- 5.2.3.8 Indonesia

- 5.2.3.9 Vietnam

- 5.2.3.10 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 Saudi Arabia

- 5.2.4.2 United Arab Emirates

- 5.2.4.3 Nigeria

- 5.2.4.4 Egypt

- 5.2.4.5 Qatar

- 5.2.4.6 South Africa

- 5.2.4.7 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Colombia

- 5.2.5.4 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 Asahi Kasei Corporation

- 6.3.2 Toray Battery Separator Film Co. Ltd

- 6.3.3 Freudenberg Performance Materials

- 6.3.4 SK ie Technology Corporation Ltd

- 6.3.5 Entek International

- 6.3.6 Sumitomo Chemical Co. Ltd

- 6.3.7 Ube Maxell Co. Ltd

- 6.3.8 W-Scope Corporation

- 6.3.9 Daramic

- 6.3.10 Amer SIL

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Enhanced Separator Materials