|

市場調査レポート

商品コード

1692445

中東・アフリカの施設管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)MEA Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカの施設管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 139 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

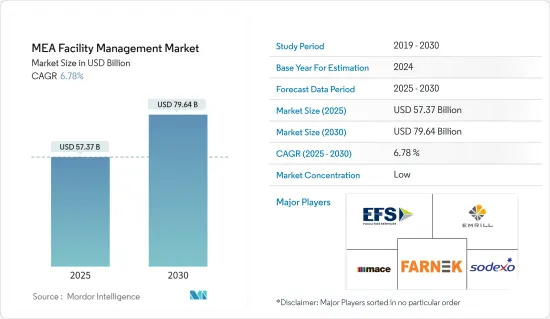

中東・アフリカの施設管理市場規模は2025年に573億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.78%で、2030年には796億4,000万米ドルに達すると予測されます。

中東では、建設、インフラ、エネルギーなどの民間プロジェクトや公共プロジェクトが、施設管理サービスに対する大規模な需要を生み出しています。この地域市場の特徴は、コンピュータ支援施設管理(CAFM)や建物管理システム(BMS)などの技術の統合です。これらの技術は、遠隔監視、モノのインターネット、モバイルソリューション、ロボット工学、AIなどとともに、FM契約、特に施設管理サービスのアウトソーシングの実行可能性を確保するために中心的な役割を果たすと予測されます。

主なハイライト

- 清掃、消毒、空間管理の実践が重視されるようになり、進行中のインフラプロジェクトもいくつかあることから、施設管理市場は予測期間中に安定した成長が見込まれます。同地域の極端な気候条件により、ハードおよびソフトの施設管理サービスの利用がさらに必要とされています。

- サウジアラビア、アラブ首長国連邦、カタールは、商業用不動産の需要が増加していることから、同地域の施設管理市場の重要な成長地域として特定できます。ドバイとサウジアラビアでは、世界企業の誘致競争が激化しているため、税制が緩和され、ビジネス・エコシステムが整備されています。企業の流入に伴い、同地域では施設管理サービスの需要が高まると予想されます。

- さらに、この地域のさまざまな国々の経済発展は、調査対象市場にプラスの影響を与えています。現在の市場力学では、施設管理サービスのアウトソーシング需要が増加しており、社内サービスからの移行が進んでいます。これに加えて、政府による好意的な支援は、資金援助や施設管理サービスの需要を誘導するための政策を通じて、大規模なインフラ開発を誘導するのに役立っています。

- 各地域の規制機関が、不動産オーナーやデベロッパーがどのように資産を最適化すべきかを概説しているため、FMサービスの需要は高まっています。しかし、雇用コストの増加や熟練労働者の不足により、地域の市場企業は、人材をプールし、長期的な契約義務を果たすために、提携や買収に取り組んでいます。

中東・アフリカの施設管理市場の動向

施設管理のアウトソーシング部門が市場の成長を牽引

- 中東・アフリカのアウトソーシング施設管理分野は、より確立された成熟市場と比べると、まだ成長段階にあります。小売業や不動産業など、各分野でグリーンビルディングの導入が重視されるようになっていることが、同地域における施設管理アウトソーシングの成長を刺激すると予想されます。例えば、EchoStoneは2023年までにナイジェリアのラゴスに182,000棟の手頃な価格の認証グリーンビルを建設する計画を発表しました。

- 商業ビルや産業プロジェクトにおける施設管理の利用拡大が、ソフトサービスを含む施設管理のアウトソーシングの成長を促進しています。中東の施設管理市場を牽引する主な要因の一つは、建設活動の拡大です。例えば、サウジアラビアは鉄道、道路、港湾、空港の建設に多額の投資を行っています。このため、施設管理サービスのアウトソーシングは、大規模プロジェクト市場に新たな機会をもたらすと期待されています。

- 同地域では現在、複数の大規模プロジェクトが進められており、施設管理アウトソーシングサービスは成長を続けています。新興諸国は、国内の商業セクターのほとんどの開発プロジェクトに取り組んでいます。継続的な投資と技術強化により、サウジアラビアは多様なプロジェクトに投資しています。サウジは2035年までに非炭化水素産業に約1兆米ドルを投資する計画です。主なプロジェクトには、キディヤ・エンターテインメント・シティ、キング・アブドラ・フィナンシャル・ディストリクト、ネオム、紅海プロジェクト、アマアラなどがあります。

- カタール・ナショナル・ビジョン(QNV)2030は、長期的な経済開発計画です。カタールは、石油・ガス以外の分野に重点を置いたインフラ計画に多額の投資を行っています。運輸通信省(MoTC)は運輸部門の主要な規制機関として機能し、各運輸事業者やプロジェクト・オーナーの業務を監督しており、ベンダーの委託施設管理サービスの機会を創出しています。

- さらに、カタールは政府と民間セクターの協力のもと、中央鉄道や高速道路プロジェクトに取り組んでおり、最近の新商業港の開港やハマド国際空港(HIA)の大幅な容量アップグレード、物流の流れ、複合一貫輸送網の開発が目覚ましいペースで進んでいます。こうした建設プロジェクトをサポートするため、施設管理サービスのアウトソーシングが期待されています。これにより、施設管理市場の新たな成長機会が促進されると思われます。

商業セグメントが市場を独占する見込み

- 地域企業がパンデミックから回復し、従業員にオフィスへの復帰を指示するにつれて、商業スペースの空室率は低下します。同地域では、オフィススペースの消毒や衛生プロトコルの維持を目的とした清掃サービスを中心に、ソフト面の施設管理サービスに対する需要が大幅に急増しています。

- 外資系企業によるさまざまな分野への投資流入は、商業用不動産セクターを後押しするオフィスへのニーズの高まりにプラスに働いています。さらに、同地域の商業不動産セクターの需要は、とりわけメンテナンスや清掃などの施設管理サービスに対する需要の高まりにつながります。

- さらに、オフィスビルの増加も施設管理を要求しています。例えば、アブダビにあるリームモールは、450以上の店舗、ハイパーマーケット、シネマコンプレックス、2つのフードコートを備え、商業用食品販売店を支援することで、商業小売部門を後押しする巨大プロジェクトの1つです。このようなプロジェクトは、GCCや北アフリカ諸国でいくつか建設中です。

- クウェートは中東・アフリカで急成長しているITハブです。2035年ビジョンを掲げるクウェートは、この地域の金融・商業の中心地になる準備が整っています。クウェートにおけるITハブの急速な発展は、施設管理サービスに対する同国の需要に直接影響を与えています。

- カイロは、エジプトの商業不動産セクター開発における主要な活動拠点であり続けています。ロックダウン規制の解除により、人や組織の移動が活発化し、オフィスから仕事を再開できるようになりました。さらに、複数の外国組織がグレーター・カイロ地域に進出したことで、オフィススペースの需要が高まっています。施設管理サービスにも強い好影響が期待されます。

- GCCの小売セクターは、最近の動向ではかつてないほどの需要に直面しており、開発業者や小売業者は力強い経済成長と入場者数の急増から恩恵を受けています。アブダビとドバイの両地域の需要は、今後も堅調に推移すると思われます。賃貸料は、アブダビ、ドバイともに緩やかな伸びが予想されます。

中東・アフリカの施設管理業界の概要

中東・アフリカの施設管理市場は細分化されており、数十年の業界経験を持つ企業が多数存在します。これらのFMベンダーは、専門知識を活用した競合戦略を取り入れ、広告に多額の投資を行っています。市場は、以下のような地域企業によって支配されています。 EFS Facilities Services Group, Emrill Services LLC, Farnek Services LLC, and Sodexo, Inc. Local players are offering competitive pricing, reducing the suppliers'bargaining power and giving buyers an option to switch their facility management vendors with minimal switching costs.

- 2023年9月アフリカにおけるモビリティ、インフラ、ヘルスケア、コンシューマー、エネルギー分野の企業であるCFAOグループは、With Africa For Africaのミッションの一環として、手頃な価格で持続可能な開発を実施することで、アフリカのインフラ分野における重要なパートナーとなりました。その目的は、同地域における持続可能なインフラ、再生可能エネルギー、施設管理ソリューションに注力することで、課題解決にさらに貢献することです。

- 2024年5月清掃サービスを提供するクリスタル・ファシリティーズ・マネジメントは、総合的な施設管理サービスとコンサルティングを推進する革新的なソリューションをKSAに導入しました。同社はサウジアラビアのリヤドで商業清掃、請負業者清掃、オフィス清掃、警備、害虫駆除、廃棄物管理、清掃サービスを提供し、顧客の目的達成を支援しています。同社は、その業界経験を活かし、施設管理サービスのコンサルティング、設計、提供を通じて、前向きな変化を促す高品質のIFMソリューションを提供すると発表しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- パイプラインにある大規模プロジェクトが建設セクターを活性化し、施設管理・サービスのニーズを促進する見通し

- ソフト施設管理サービスに対する需要の増加

- 市場抑制要因

- 同地域における市場の断片化

第6章 市場セグメンテーション

- タイプ別

- インハウス施設管理

- アウトソーシング型施設管理

- シングルFM

- バンドルFM

- 統合型FM

- エンドユーザー別

- 商業施設

- 施設

- 公共/インフラ

- 産業

- ヘルスケア

- その他のエンドユーザー

- 国別

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- 南アフリカ

- エジプト

- ナイジェリア

第7章 競合情勢

- 企業プロファイル

- Engie Cofely Energy Services LLC(Engie SA)

- EFS Facilities Services Group

- Ejadah Asset Management Group

- Emrill Services LLC

- Farnek Services LLC

- Initial Saudi Arabia Company Limited

- Kharafi National for Infrastructure Projects Developments Construction and Services SAE

- Mace Group Limited

- Serco Group PLC

- Sodexo Inc.

- Ecolab Inc.

第8章 投資分析

第9章 今後の動向

The MEA Facility Management Market size is estimated at USD 57.37 billion in 2025, and is expected to reach USD 79.64 billion by 2030, at a CAGR of 6.78% during the forecast period (2025-2030).

Private and public projects, including construction, infrastructural, and energy projects, are creating a massive demand for facility management services in the Middle East. The regional market is characterized by the integration of technologies, such as computer-aided facility management (CAFM) and building management systems (BMS), which are anticipated to take center stage along with remote monitoring, internet of things, mobile solutions, robotics, and AI to ensure the viability of FM contracts, particularly outsourced facility management services.

Key Highlights

- Driven by the growing emphasis on cleaning, disinfection, space management practices, and several ongoing infrastructural projects, the facility management market is anticipated to grow steadily during the forecast period. The region's extreme climatic conditions have further necessitated the use of hard and soft facility management services.

- Saudi Arabia, the United Arab Emirates, and Qatar can be identified as critical growth areas for the facility management market in the region, owing to their increasing demand for commercial real estate. The intensifying competition between Dubai and Saudi Arabia to host global companies has resulted in relaxing taxation and ensuring the provision of a supportive business ecosystem in the region. With the influx of businesses, the area is expected to see a boost in demand for facility management services.

- Furthermore, the economic development of various countries in the region has positively influenced the studied market. Current market dynamics highlight the increasing demand for outsourcing facility management services, moving away from in-house services. In addition to this, favorable government support is helping to induce large-scale infrastructural development through monetary aid and policies designed to steer the demand for facility management services.

- With regional regulatory bodies outlining how real estate owners and developers should optimize their assets, the demand for FM services is rising. However, with the increased cost of hiring and the lack of a skilled workforce, the regional market players are engaging in partnerships and acquisitions to pool talent and deliver long-term contractual obligations.

MEA Facility Management Market Trends

The Outsourced Facility Management Segment is Driving the Market's Growth

- The Middle East and Africa outsourced facility management segment is still in the growth stage compared to more established and mature markets. The increasing emphasis on adopting green buildings across sectors, such as retail and real estate, is expected to stimulate the growth of outsourced facility management in the region. For instance, EchoStone announced plans to build 182,000 affordable, certified green buildings in Lagos, Nigeria, by 2023.

- The growing use of facility management in commercial buildings and industrial projects is driving the growth of outsourced facility management, including soft services. One of the major factors driving the facility management market in the Middle East is growing construction activity. For instance, Saudi Arabia has invested heavily in constructing railways, roads, ports, and airports. Thus, outsourced facility management services are anticipated to bring new opportunities to the market for large-scale projects.

- Outsourced Facility management services across the region are growing owing to several megaprojects currently being undertaken. KSA is working on most development projects in the country's commercial sector. With continuing investment and technological enhancements, Saudi Arabia invests in diverse projects. Saudi plans to invest approximately USD 1 trillion in its non-hydrocarbon industry by 2035. Some key projects include Qiddiya Entertainment City, King Abdullah Financial District, Neom, the Red Sea Project, and Amaala.

- Qatar National Vision (QNV) 2030 is a long-term economic development plan. Qatar invests heavily in infrastructure programs focused on its non-oil and gas sectors. The Ministry of Transport and Communications (MoTC) functions as the primary regulator of the transportation sector, overseeing the work of individual transport operators and project owners, and creates an opportunity for the vendors' outsourced facility management services.

- Additionally, in collaboration with its government and private sector, Qatar is working on central rail and expressway projects, the recent opening of the new commercial seaport and significant capacity upgrades at Hamad International Airport (HIA), logistics flows, and multimodal transportation networks are being developed at a remarkable pace. To support these construction projects, facility management services are expected to be outsourced. This will drive new growth opportunities in the facility management market.

The Commercial Segment is Expected to Dominate the Market

- As regional companies recover from the pandemic and instruct employees to return to the office, the vacancy rate will decline in commercial spaces. The demand for soft facility management services in the region has witnessed a significant spike, focusing on cleaning services to disinfect office spaces and maintain hygiene protocols.

- The inflow of investments from foreign companies in different sectors has positively attributed to the growing need for offices boosting the commercial real estate sector. Furthermore, the demand for the commercial real estate sector in the region translates to a higher requirement for facility management services for maintenance and cleaning, among others.

- Moreover, the increase in office buildings also demands facilities management. For instance, Reem Mall in Abu Dhabi marks one of the megaprojects to boost the commercial retail sector by facilitating more than 450 stores for retail, a hypermarket, a multiplex cinema, and two food courts, supporting commercial food outlets. Several such projects are under construction in the GCC and Northern African countries.

- Kuwait is a fast-emerging IT hub in Middle East and Africa. With its 2035 Vision, Kuwait is poised to become the area's financial and commercial center. The rapid development of IT hubs in Kuwait directly influences the country's demand for facility management services.

- Cairo remains the primary activity center in developing Egypt's commercial real estate sector. The lifting of lockdown restrictions has increased the mobility of people and organizations, allowing them to re-convene work from the office, which is also set to increase the occupancy rate in the country. Furthermore, the entry of several foreign organizations into the Greater Cairo region has boosted the demand for office space. It is expected to have a strong positive impact on facility management services.

- The retail sector in the GCC has faced unprecedented levels of demand in the recent past, where developers and retailers have benefited from strong economic growth and surging footfall numbers. The demand in both Abu Dhabi and Dubai is likely to remain strong. Rental rates are anticipated to increase, with a moderate rate of rental growth in both Abu Dhabi and Dubai.

MEA Facility Management Industry Overview

The Middle East and Africa facility management market is fragmented, with many players having decades of industry experience. These FM vendors are incorporating competitive strategies by leveraging their expertise and are significantly investing in advertising. The market is dominated by regional players such as EFS Facilities Services Group, Emrill Services LLC, Farnek Services LLC, and Sodexo, Inc. Local players are offering competitive pricing, reducing the suppliers' bargaining power and giving buyers an option to switch their facility management vendors with minimal switching costs.

- September 2023: The CFAO Group, a player in the fields of mobility, infrastructure, healthcare, consumer, and energy in Africa, became a key partner in Africa's infrastructure sector by implementing affordable and sustainable development as part of its With Africa For Africa mission. The aim is to contribute more to addressing the challenges by focusing on sustainable infrastructure, renewable energy, and facility management solutions in the region.

- May 2024: Crystal Facilities Management, which delivers cleaning services, introduced innovative solutions to help drive integrated facilities management services and consultancy to the KSA. The company offers commercial cleaning, contractor cleaning, office cleaning, security, pest control, waste management, and janitorial services in Riyadh, Saudi Arabia, helping clients achieve their objectives. The company announced that it is leveraging its industry experience to deliver high-quality IFM solutions that will drive positive change through consultation, design, and delivery of facility management services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Megaprojects in the Pipeline is Expected to Boost the Construction Sector Driving the Need for Facility Management Services

- 5.1.2 Increasing Demand for Soft Facility Management Services

- 5.2 Market Restraints

- 5.2.1 Fragmented Nature of the Market in the Region

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Inhouse Facility Management

- 6.1.2 Outsourced Facility Management

- 6.1.2.1 Single FM

- 6.1.2.2 Bundled FM

- 6.1.2.3 Integrated FM

- 6.2 By End User

- 6.2.1 Commercial

- 6.2.2 Institutional

- 6.2.3 Public/Infrastructure

- 6.2.4 Industrial

- 6.2.5 Healthcare

- 6.2.6 Other End Users

- 6.3 By Country

- 6.3.1 Saudi Arabia

- 6.3.2 United Arab Emirates

- 6.3.3 Qatar

- 6.3.4 Kuwait

- 6.3.5 South Africa

- 6.3.6 Egypt

- 6.3.7 Nigeria

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Engie Cofely Energy Services LLC (Engie SA)

- 7.1.2 EFS Facilities Services Group

- 7.1.3 Ejadah Asset Management Group

- 7.1.4 Emrill Services LLC

- 7.1.5 Farnek Services LLC

- 7.1.6 Initial Saudi Arabia Company Limited

- 7.1.7 Kharafi National for Infrastructure Projects Developments Construction and Services SAE

- 7.1.8 Mace Group Limited

- 7.1.9 Serco Group PLC

- 7.1.10 Sodexo Inc.

- 7.1.11 Ecolab Inc.