|

市場調査レポート

商品コード

1636273

中国の電気自動車用電池材料:市場シェア分析、産業動向・統計、成長予測(2025~2030年)China Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の電気自動車用電池材料:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

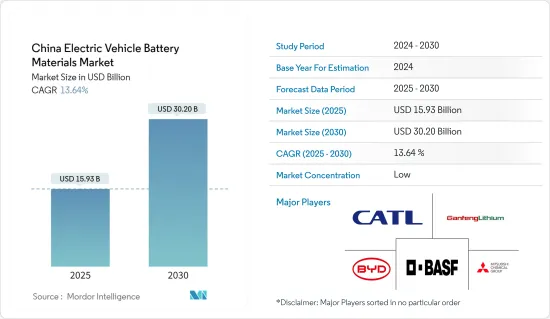

中国の電気自動車用電池材料の市場規模は2025年に159億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.64%で、2030年には302億米ドルに達すると予測されます。

主要ハイライト

- 長期的には、電気自動車販売の拡大や政府の施策と施策規制などの要因が、予測期間中の中国の電気自動車用電池材料市場の最も重要な促進要因のひとつになると予想されます。

- 一方、輸入原料に依存しているため、価格変動の影響を受けやすく、市場調査にはマイナスの影響が予想されます。

- 電池技術の進歩に対する需要は引き続き高まっています。この要因は、将来的に市場にいくつかの機会を生み出すと予想されます。

中国の電気自動車用電池材料の市場動向

市場を独占するリチウムイオン電池タイプ

- 世界のリチウムイオン電気自動車用電池市場は、機会と課題の両方が渦巻くダイナミックな市場です。リチウムイオン二次電池は、主にその有利な容量対重量比により、他の電池技術を凌いで普及しています。リチウムイオン二次電池は、長寿命、低メンテナンス、長寿命、顕著な価格低下といった優れた性能特性により、その普及にさらに拍車をかけています。

- リチウムイオン・電池は従来、同種の製品よりも高い価格帯で販売されてきたが、市場の大手企業は規模の経済を実現するために投資を行い、研究開発努力を強化してきました。このような競合の激化により、電池の性能が向上しただけでなく、リチウムイオン電池の価格も低下しています。

- 最近の動向では、リチウムイオン電池とセルパックの価格は一貫して下落しており、エンドユーザー産業にとってますます魅力的なものとなっています。2022年に一時的に上昇した後、2023年も電池価格は下落基調を続けた。重要なハイライトは、リチウムイオン電池パックのコストが14%下落し、過去最低の139米ドル/kWhに達したことです。

- 環境に対する懸念が高まる中、中国政府は電気自動車を熱烈に支持し、野心的なネット・ゼロ・カーボン排出目標に向けた取り組みを行っています。電気自動車の蓄電容量に不可欠なリチウムの需要は旺盛で、主要世界企業はリチウムの採掘を強化しています。

- 2024年7月、中国東部の山東省は1,000億元(約138億米ドル)を投資する計画を発表しました。この野心的な青写真は、電極材料、電解質、電池セル、組み立てにまたがる産業チェーンを網羅しています。山東省の戦略は、民生用電池の多様化と品質向上を目指すだけでなく、研究開発の強化にも重点を置いています。同省政府は済南市と青島市を支援し、原料生産と電池組立の企業を育成し、地元の新エネルギー車メーカーの需要に応えています。

- 2024年2月、CATLは1回の充電で1,000キロメートル(621マイル)以上という驚異的な航続距離を誇る画期的なリン酸鉄リチウム(LFP)電池を発表しました。この技術革新は、中国における原料需要を拡大する態勢を整えています。

- このような開発により、リチウムイオン電池の需要は急増し、その結果、今後数年間で様々な原料の必要性が高まることになります。

電気自動車販売の拡大

- 中国の電気自動車(EV)用電池材料市場は、EV販売台数の急増とサステイナブル輸送に対する国家的コミットメントに後押しされ、急速に拡大しています。EV普及の世界的リーダーとして、中国の必須電池材料(リチウム、ニッケル、コバルト、マンガン)に対する需要は急増しています。これらの材料は、EVの電力貯蔵の主要技術であるリチウムイオン電池を製造する上で極めて重要です。

- 中国のEV販売好調は、電池材料市場の主要起爆剤となっています。近年、政府の手厚いインセンティブや補助金、二酸化炭素排出削減や大気汚染対策を対象とした強力な施策枠組みによって、中国はEVの普及が急速に進んでいます。政府の新エネルギー車(NEV)義務化は、自動車メーカーに一定割合のEV生産を義務付けるもので、この勢いをさらに加速させています。

- この勢いはさらに加速しています。CATLは、EV用電池の需要急増に対応するため、生産能力を増強しています。さらに、CATLは研究開発に多額の投資を行い、コスト削減と同時に電池性能の向上を目指しています。

- 注目すべき動きとして、CATLは2024年6月にTeslaと戦略的提携を結び、Teslaの上海ギガファクトリーにリチウムイオン電池を供給することを約束しました。この提携は、中国の電池メーカーと国際的なEVメーカーとの関係が深まっていることを浮き彫りにしています。

- 2023年、中国の電気自動車部門は前年比約22.7%成長し、電池EVの販売台数は約540万台と、2019年の83万台から大きく飛躍しました。

- 中国政府は、税制上の優遇措置、メーカーと消費者の双方に対する補助金、充電インフラへの投資など、さまざまな施策を通じてEV部門を支援し続けています。これらの施策は、EVをより手頃な価格で便利にすることで、普及率を高め、その結果、電池材料の需要を増加させることを目的としています。電池技術の革新も市場を形成しています。BYDのような企業は、リン酸鉄リチウム(LFP)電池のような新しい電池化学品を開発しており、従来のリチウムイオン電池よりもエネルギー密度は若干低いが、安全で安価です。これらの進歩は、EVを大衆市場により身近なものにするために極めて重要です。

- 中国のEV用電池材料市場展望は非常に明るいです。政府からの継続的な支援、技術の進歩、戦略的な産業パートナーシップにより、中国は世界のEV市場におけるリーダーシップを維持する態勢が整っています。大手電池メーカーによる生産能力の拡大が続いており、サステイナブルプラクティスが重視されていることから、必要不可欠な材料の安定供給が確保され、EVセクターの急成長を支えることになりそうです。

中国の電気自動車用電池材料産業概要

中国の電気自動車用電池材料市場は半分断されています。この市場の主要企業(順不同)は、Contemporary Amperex Technology Co., Limited、BYD Auto、Ganfeng Lithium、BASF SE、Mitsubishi Chemical Group Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車販売の成長

- 政府の支援施策と施策

- 抑制要因

- 原料供給への依存

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- リチウムイオン電池

- 鉛蓄電池

- その他

- 材料

- 正極

- 負極

- 電解液

- セパレーター

- その他

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Contemporary Amperex Technology Co., Limited

- BYD Auto Co., Ltd.

- Ganfeng Lithium

- BASF SE

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- Umicore SA

- Sumitomo Chemical Co., Ltd.

- BTR New Material Group Co. Ltd.

- Shanshan Co.

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 電池技術の進歩

The China Electric Vehicle Battery Materials Market size is estimated at USD 15.93 billion in 2025, and is expected to reach USD 30.20 billion by 2030, at a CAGR of 13.64% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as growing electric vehicle sales and supportive government policies and regulations are expected to be among the most significant drivers for the China Electric Vehicle Battery Materials Market during the forecast period.

- On the other hand, the country's reliance on imported raw materials makes the industry vulnerable to price fluctuation, which is expected to negatively impact the market studied.

- Nevertheless, there is continued growing demand for advancements in battery technology. This factor is expected to create several opportunities for the market in the future.

China Electric Vehicle Battery Materials Market Trends

Lithium-ion Battery Type to Dominate the Market

- The global lithium-ion electric vehicle battery market is a dynamic arena, teeming with both opportunities and challenges. Lithium-ion rechargeable batteries are outpacing other battery technologies in popularity, primarily due to their advantageous capacity-to-weight ratio. Their adoption is further fueled by superior performance attributes, such as longevity, low maintenance, an extended shelf life, and a notable decrease in price.

- While lithium-ion batteries traditionally commanded a higher price point than their counterparts, leading market players have been channeling investments into achieving economies of scale and bolstering R&D efforts. This intensified competition has not only enhanced battery performance but also driven down lithium-ion battery prices.

- Recent trends show a consistent decline in the prices of lithium-ion batteries and cell packs, making them increasingly attractive to end-user industries. After a brief uptick in 2022, battery prices continued their downward trajectory in 2023. A significant highlight was the 14% drop in lithium-ion battery pack costs, reaching a record low of USD 139/kWh.

- Amid rising environmental concerns, the Chinese government is fervently championing electric vehicles, aligning its efforts with ambitious net-zero carbon emission targets. Lithium, a crucial component for EV storage capacity, is in high demand, prompting leading global companies to ramp up lithium extraction.

- In July 2024, Shandong province in eastern China unveiled plans for a substantial 100 billion yuan (USD 13.8 billion) investment. The ambitious blueprint encompasses an industrial chain spanning electrode materials, electrolytes, battery cells, and assembly. Shandong's strategy not only aims to diversify and enhance the quality of consumer batteries but also emphasizes bolstering R&D. The provincial government is backing Jinan and Qingdao cities to nurture companies in raw material production and battery assembly, catering to the demands of local new energy vehicle manufacturers.

- In February 2024, CATL introduced a groundbreaking lithium iron phosphate (LFP) battery boasting an impressive driving range of over 1,000 kilometers (621 miles) on a single charge. This innovation is poised to amplify raw material demand in China.

- Given these developments, the demand for lithium-ion batteries is set to surge, subsequently driving up the need for various raw materials in the coming years.

Growing Electric Vehicle Sales

- China's electric vehicle (EV) battery materials market is expanding rapidly, fueled by soaring EV sales and a national commitment to sustainable transportation. As the global leader in EV adoption, China's appetite for essential battery materials-lithium, nickel, cobalt, and manganese-has surged. These materials are pivotal for crafting lithium-ion batteries, the primary technology for EV power storage.

- China's booming EV sales are a primary catalyst for its battery materials market. In recent years, bolstered by generous government incentives, subsidies, and a robust policy framework targeting carbon emission reductions and air pollution combat, China has witnessed a meteoric rise in EV adoption. The government's New Energy Vehicle (NEV) mandate, compelling automakers to produce a specific percentage of EVs, further amplifies this momentum.

- Contemporary Amperex Technology Co. Limited (CATL), a frontrunner in battery manufacturing, is ramping up its production capacity to cater to the surging demand for EV batteries. Additionally, CATL is channeling substantial investments into research and development, aiming to boost battery performance while curtailing costs.

- In a notable move, CATL forged a strategic alliance with Tesla in June 2024, committing to supply lithium-ion batteries for Tesla's Shanghai Gigafactory. This partnership highlights the deepening ties between Chinese battery producers and international EV manufacturers.

- In 2023, China's electric vehicle sector grew by approximately 22.7% year-on-year, with battery EV sales soaring to about 5.4 million, a significant leap from 0.83 million in 2019.

- The Chinese government continues to support the EV sector through various measures, including tax incentives, subsidies for both manufacturers and consumers and investments in charging infrastructure. These policies are designed to make EVs more affordable and convenient, thereby driving higher adoption rates and, consequently, increasing the demand for battery materials. Innovations in battery technology are also shaping the market. Companies like BYD are developing new battery chemistries, such as lithium iron phosphate (LFP) batteries, which are safer and cheaper, although with slightly lower energy density than traditional lithium-ion batteries. These advancements are crucial for making EVs more accessible to the mass market.

- The outlook for the EV battery materials market in China is highly positive. With continued support from the government, technological advancements, and strategic industry partnerships, China is well-positioned to maintain its leadership in the global EV market. The ongoing expansion of production capacities by major battery manufacturers and the emphasis on sustainable practices will likely ensure a steady supply of essential materials, supporting the rapid growth of the EV sector.

China Electric Vehicle Battery Materials Industry Overview

The China Electric Vehicle Battery Materials Market is semi-fragmented. Some of the key players in this market (in no particular order) are Contemporary Amperex Technology Co., Limited, BYD Auto Co., Ltd, Ganfeng Lithium, BASF SE, and Mitsubishi Chemical Group Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Dependence on Raw Material Supply

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted byr Leading Players

- 6.3 Company Profiles

- 6.3.1 Contemporary Amperex Technology Co., Limited

- 6.3.2 BYD Auto Co., Ltd.

- 6.3.3 Ganfeng Lithium

- 6.3.4 BASF SE

- 6.3.5 Mitsubishi Chemical Group Corporation

- 6.3.6 UBE Corporation

- 6.3.7 Umicore SA

- 6.3.8 Sumitomo Chemical Co., Ltd.

- 6.3.9 BTR New Material Group Co. Ltd.

- 6.3.10 Shanshan Co.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology