|

市場調査レポート

商品コード

1636271

南米の電気自動車用電池材料:市場シェア分析、産業動向、成長予測(2025~2030年)South America Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の電気自動車用電池材料:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

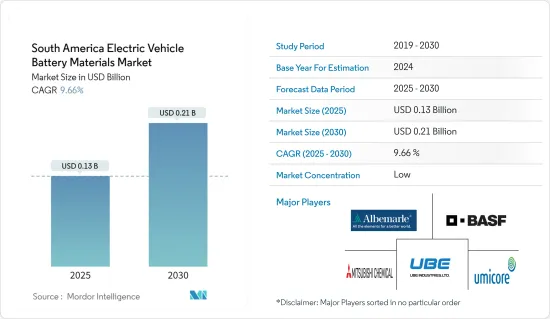

南米の電気自動車用電池材料市場規模は2025年に1億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.66%で、2030年には2億1,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車販売台数の増加や政府の支援施策と施策といった要因が、予測期間中の南米の電気自動車用電池材料市場の最も大きな促進要因のひとつになると予想されます。

- 一方、電池材料の生産設備が不足しているため、輸入への依存度が高く、予測期間中、南米の電気自動車用電池材料市場にとって脅威となります。

- 先進的な電池技術を開発するための努力は続けられています。この要因は、今後市場にいくつかの機会を生み出すと予想されます。

- ブラジルは大きな成長が見込まれ、予測期間中に最も高い成長を記録する可能性が高いです。これは、この地域に大きな自動車製造・販売産業が存在するためです。

南米の電気自動車用電池材料市場動向

リチウムイオン電池が市場を独占

- 南米の電気自動車(EV)用電池材料市場は、リチウムイオン電池に大きく依存しています。電気自動車セグメントで最も普及しているリチウムイオン電池は、エネルギー密度、効率、耐久性を兼ね備えており、現代の電気自動車技術の要となっています。

- 過去10年間で、電池技術と製造における進歩は、コスト削減だけでなく、性能と信頼性を増幅させ、メーカーと消費者に対するリチウムイオン電池の魅力を高めてきました。

- 近年、リチウムイオン電池とセルパックの価格は下落傾向にあり、エンドユーザーにとっての魅力が高まっています。2022年にわずかに上昇した後、2023年に価格は再び下落し、リチウムイオン電池パックは歴史的な安値となる139米ドル/kWhを記録し、14%の下落を示しました。

- この電池セグメントはさまざまな材料で構成され、それぞれが電池全体の性能に重要な役割を果たしています。これらの材料は、エネルギー密度、サイクル寿命、熱安定性を高める能力によって選択されます。特に、ニッケルを多く含む正極材料は、エネルギー容量が大きく、航続距離の延長に直結するため好まれます。

- この地域の電気自動車に対する意欲の高まりは、リチウムイオン電池の需要急増の引き金となり、電池メーカーに材料生産施設への投資を促しています。この戦略的転換は、国内と世界のリチウム電池の需要増に対応することを目的としています。現在進行中の電池技術の進歩と相まって、電気自動車の普及が進むにつれ、市場は持続的な成長を遂げる態勢が整っています。

- 例えば、2023年4月には、世界有数の電気自動車(EV)メーカーである中国のBYDが、2億9,000万米ドルを投じてチリのアントファガスタ地域にリチウム正極工場を建設する予定です。この発表は、チリの経済開発機関CORFOによって行われました。BYDチリは、CORFOが確認したとおり、チリ政府から公認リチウム生産者に指定されています。この認定により、同社は炭酸リチウムの優遇割り当てを受けることができます。

- こうしたことから、予測期間中、同市場ではリチウムイオン電池部門が優位を占めると予想されます。

著しい成長を遂げるブラジル

- ブラジルは、その豊富な天然資源と成長する産業能力を活用し、南米の電気自動車(EV)用電池材料市場で極めて重要な役割を果たしています。特にリチウム、ニッケル、黒鉛など、重要な電池材料の膨大な埋蔵量を誇るブラジルは、電気自動車部品の地域的・世界的サプライチェーンにおける潜在的強国として位置づけられています。

- ブラジルのリチウム鉱床はミナス・ジェライス州とセアラ州に集中しており、この重要な電池用金属の需要拡大に乗じようとする国内外の鉱山会社から大きな注目を集めています。

- Energy Institute Statistical Review of World Energyによると、2023年のリチウム埋蔵量は4,900トンとなります。これは、2022年に記録された2,600トンから大幅な増加を示し、88.5%という驚異的な成長率を反映しています。このような急増は、同国のリチウム埋蔵量の多さを強調するものであり、特に電気自動車に関連した、急成長する電池材料市場にとって良い兆しとなる要素です。

- ブラジルのニッケル埋蔵量は主にゴイアス州にあり、電気自動車用電池材料における戦略的重要性をさらに高めています。加えて、ブラジルはミナス・ジェライス州、バイーア州、セアラ州に相当量の黒鉛鉱床を有し、リチウムイオン電池用負極材の生産において重要な位置を占めています。

- ブラジル政府は、電気自動車用電池材料セグメントの戦略的重要性を認識し、その開発を促進するために様々なイニシアチブを実施しています。こうした取り組みには、投資優遇措置、研究開発支援、サステイナブル採掘プラクティスと現地での付加価値向上を促進するための規制枠組みなどが含まれます。

- 例えば、2024年4月、Sigma Lithiumは戦略的な動きとして、ブラジルのグリーンテック工業プラントのフェーズ2のために1億米ドルの資本支出を決定しました。この投資により、2025年までに五重極ゼログリーンリチウムの年間生産能力を27万トンから52万トンに増強します。シグマの取締役会が承認したこの拡大により、同社は推定180万台の電気自動車(EV)の燃料に十分なリチウム精鉱を生産する態勢が整った。

- 国家鉱業庁(ANM)は、電池材料プロジェクトの認可プロセスを合理化しました。同時に、ブラジル開発銀行(BNDES)は、電気自動車のサプライチェーンに関わる企業を支援するための融資プログラムを設立しました。このような措置により、国内外の投資が誘致され始めており、大手鉱業会社や電池メーカーがブラジルでの事業機会を模索しています。

- そのため、ブラジルは前述のように予測期間中に大きな成長を遂げると予想されます。

南米の電気自動車用電池材料産業概要

南米の電気自動車用電池材料市場は細分化されています。この市場の主要企業(順不同)は、BASF SE、Mitsubishi Chemical Group Corporation、UBE Corporation、Albemarle Corporation、Umicore SAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車販売の成長

- 政府の支援施策と施策

- 抑制要因

- 電池材料生産施設の不足

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- リチウムイオン電池

- 鉛蓄電池

- その他

- 材料

- 正極

- 負極

- 電解液

- セパレーター

- その他

- 地域

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- Umicore SA

- Sumitomo Chemical Co., Ltd.

- Albemarle Corporation

- YOUME

- BYD Co., Ltd.

- Arkema SA

- Nichia Corporation

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 電池技術の進歩

目次

Product Code: 50003558

The South America Electric Vehicle Battery Materials Market size is estimated at USD 0.13 billion in 2025, and is expected to reach USD 0.21 billion by 2030, at a CAGR of 9.66% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising growth in electric vehicle sales and supportive government policies and regulations are expected to be among the most significant drivers for the South America Electric Vehicle Battery Materials Market during the forecast period.

- On the other hand, the lack of battery material production facilities, leading to heavy reliance on imports, poses a threat to the South America Electric Vehicle Battery Materials Market during the forecast period.

- Nevertheless, continued efforts are being made to develop advanced battery technology. This factor is expected to create several opportunities for the market in the future.

- Brazil is expected to witness significant growth and will likely register the highest growth during the forecast period. This is due to the presence of a significant vehicle manufacturing and sales industry in the region.

South America Electric Vehicle Battery Materials Market Trends

Lithium-ion Batteries to Dominate the Market

- The South American electric vehicle (EV) battery materials market hinges significantly on lithium-ion batteries. These batteries, being the most prevalent in the electric vehicle realm, stand out for their blend of energy density, efficiency, and durability, making them a linchpin in modern electric vehicle technology.

- Over the past decade, strides in battery technology and manufacturing have not only cut costs but also amplified performance and reliability, heightening the appeal of lithium-ion batteries to manufacturers and consumers.

- In recent years, there has been a downward trend in lithium-ion battery and cell pack prices, enhancing their allure to end-users. After a slight uptick in 2022, prices dipped again in 2023, with lithium-ion battery packs hitting a historic low of USD 139/kWh, marking a 14% drop.

- This battery segment comprises a range of materials, each playing a vital role in the battery's overall performance. These materials are selected for their ability to boost energy density, cycle life, and thermal stability, which are crucial factors for the automotive sector. Notably, nickel-rich cathode materials are favored for their high energy capacity, directly translating to extended driving ranges-a key selling point for consumers and market competitiveness.

- The region's growing electric vehicle appetite has triggered a surge in lithium-ion battery demand, prompting battery manufacturers to invest in material production facilities. This strategic shift aims to meet the rising demand for lithium batteries, both domestically and globally. Coupled with ongoing battery tech advancements, the market is poised for sustained growth as electric vehicle adoption climbs.

- For instance, in April 2023, China's BYD Co Ltd, the world's leading electric vehicle (EV) manufacturer, is set to construct a lithium cathode factory in Chile's Antofagasta region with an investment of USD 290 million. This announcement was made by Chile's economic development agency, CORFO. BYD Chile has been designated as a recognized lithium producer by the Chilean government, as confirmed by CORFO. This recognition grants the company privileged access to preferential rates for lithium carbonate allocations.

- Given these factors, the dominance of the lithium-ion battery segment in the market is projected for the forecast period.

Brazil to Witness Significant Growth

- Brazil plays a pivotal role in the South American electric vehicle (EV) battery materials market, leveraging its abundant natural resources and growing industrial capabilities. The country's vast reserves of critical battery materials, particularly lithium, nickel, and graphite, position it as a potential powerhouse in the regional and global supply chain for electric vehicle components.

- Brazil's lithium deposits, concentrated in the states of Minas Gerais and Ceara, have attracted significant attention from both domestic and international mining companies seeking to capitalize on the growing demand for this crucial battery metal.

- The Energy Institute Statistical Review of World Energy reported that in 2023, the country's lithium reserves stood at 4.9 thousand tonnes of lithium content. This marked a significant increase from the 2.6 thousand tonnes recorded in 2022, reflecting an impressive growth rate of 88.5%. Such a surge underscores the nation's substantial lithium reserves, a factor that bodes well for the burgeoning battery material market, especially in the context of electric vehicles.

- The country's nickel reserves, primarily found in the state of Goias, further enhance its strategic importance in the electric vehicle battery materials landscape. Additionally, Brazil boasts substantial graphite resources, with significant deposits located in Minas Gerais, Bahia, and Ceara, positioning the country as a critical player in the production of anode materials for lithium-ion batteries.

- The Brazilian government has recognized the strategic importance of the electric vehicle battery materials sector and has implemented various initiatives to foster its development. These efforts include investment incentives, research and development support, and regulatory frameworks aimed at promoting sustainable mining practices and local value addition.

- For instance, in April 2024, Sigma Lithium, in a strategic move, has greenlit a USD 100 million capital expenditure for Phase 2 of its Greentech Industrial Plant in Brazil. By 2025, this investment aims to ramp up the annual production capacity of its Quintuple Zero Green Lithium from 270,000 tons to an impressive 520,000 tons. With the expansion, sanctioned by Sigma's board, the company is poised to churn out sufficient lithium concentrate to fuel an estimated 1.8 million electric vehicles (EVs).

- The National Mining Agency (ANM) has streamlined licensing processes for battery material projects. At the same time, the Brazilian Development Bank (BNDES) has established financing programs to support companies involved in the electric vehicle supply chain. These measures have begun to attract both domestic and foreign investments, with several major mining companies and battery manufacturers exploring opportunities in the country.

- Therefore, Brazil is expected to witness significant growth during the forecast period, as mentioned above.

South America Electric Vehicle Battery Materials Industry Overview

The South America Electric Vehicle Battery Materials Market is semi-fragmented. Some of the key players in this market (in no particular order) are BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Albemarle Corporation, and Umicore SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Lack of Battery Material Production Facility

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Mitsubishi Chemical Group Corporation

- 6.3.3 UBE Corporation

- 6.3.4 Umicore SA

- 6.3.5 Sumitomo Chemical Co., Ltd.

- 6.3.6 Albemarle Corporation

- 6.3.7 YOUME

- 6.3.8 BYD Co., Ltd.

- 6.3.9 Arkema SA

- 6.3.10 Nichia Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology