|

市場調査レポート

商品コード

1636276

ドイツの電気自動車用電池材料:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Germany Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツの電気自動車用電池材料:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

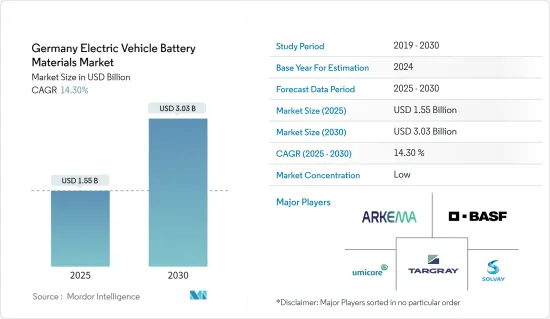

ドイツの電気自動車用電池材料市場規模は2025年に15億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは14.3%で、2030年には30億3,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車(EV)販売の伸びと政府の支援的な施策と規制が、予測期間中の電気自動車用電池材料の需要を促進すると予想されます。

- 一方、原料のサプライチェーンや価格変動に関連する問題は、市場調査にマイナスの影響を与えそうです。

- エネルギー密度の向上、充電時間の短縮、安全性の向上、寿命の延長といった電池の技術的進歩は、近い将来、電気自動車用電池材料市場の参入企業に大きなビジネス機会をもたらすと期待されています。

ドイツの電気自動車用電池材料の市場動向

電気自動車(EV)販売の伸びが市場を牽引

- ドイツにおける電気自動車(EV)販売台数の増加が、同地域におけるEV用電池材料の需要を押し上げています。EV販売の急増に伴い、リチウム、コバルト、ニッケル、黒鉛などの主要電池材料のニーズも高まっています。こうした需要の高まりは、これらの材料の現地生産と投資に拍車をかけ、ドイツの電池材料サプライチェーンの成長を後押ししています。

- ドイツは、電気自動車を中心としたクリーンエネルギーへの転換を図っています。近年、同国ではEVの販売が急増しています。例えば、国際エネルギー機関(IEA)の報告によると、2023年のドイツの電気自動車販売台数は70万台です。この数字は2022年から横ばいだったもの、2019年からは5.5倍に増加しました。欧州政府が最近発表した数多くのプロジェクトやイニシアチブにより、EVの販売台数は大幅に増加する見込みで、電池材料の需要がさらに高まっています。

- ドイツ政府はEV市場の拡大を積極的に支持し、補助金や税制優遇措置を提供し、より厳しい排ガス規制を実施しています。こうした支援策はEV市場を強化するだけでなく、電池材料産業にも及んでいます。最近、政府は野心的な奨励策を発表し、今後数年間でEVの販売台数を4倍に増やすことを目指しています。

- 2023年構想の一環として、政府は電気自動車の普及を促進するための大幅な補助金制度を展開しました。EVの新規購入者には最大6,000ユーロ(約6,500米ドル)の補助金が支給され、プラグイン・ハイブリッド車の購入者には最大4,500ユーロ(約4,900米ドル)の補助金が支給されます。このような措置により、EVの生産と販売が促進されるだけでなく、今後数年間は電池材料の需要も高まると予想されます。

- 活気に満ちたドイツのEV市場は、電池技術革新の温床となっています。ドイツの大手企業は研究機関とともに、エネルギー密度の向上、寿命の延長、優れた安全性を約束する先駆的な材料への投資を進めています。地域の主要企業間のコラボレーションが先進的な電池技術への道を開き、EV用電池需要の高まりの舞台を整えつつあります。

- 注目すべき開発では、電池会社VARTAが主導する15社の企業と学術研究者からなるコンソーシアムが、2024年5月に最先端のナトリウムイオン電池技術を発表しました。この次世代電池は、EVやその他の用途に対応し、高性能、費用対効果、環境への優しさを約束します。同コンソーシアムは、プロジェクトの集大成として2027年半ばを予定しています。このようなブレークスルーは、洗練されたEV用電池の需要を加速させるだけでなく、当面の間、この地域の電池材料に対する意欲を増幅させると考えられます。

- このような力学を考えると、EV需要とそれに対応する電池材料需要の急増の軌跡は、強固で有望であると考えられます。

リチウムイオン電池が市場を独占

- 電気自動車(EV)用リチウムイオン電池の生産量の増加が、電池材料市場を再構築しています。ドイツでは、リチウムイオン電池の生産が急増するにつれて、リチウムの需要も増加しています。この地域でのリチウムの発見は、原料コストに顕著な影響を与えています。

- 主要な市場関係者は、リチウムイオン電池の増産と電池原料の需要増に対応するため、リチウム埋蔵量と研究開発に投資を行っています。これらの埋蔵量が継続的に発見されるにつれて、リチウムイオン電池の価格は長期的に低下傾向にあります。

- 例えば、2023年の電池価格は139米ドル/kWhまで下落し、13%以上の下落を記録しました。継続的な技術革新と製造改善により、電池パック価格は2025年までに113米ドル/kWhまで、さらに2030年までに80米ドル/kWhまで下落する可能性があると予測されています。

- さらに、欧州政府は、環境問題への関心の高まりに後押しされ、EV用リチウムイオン電池の生産を積極的に支持しています。純炭素排出量ゼロの達成に熱心に取り組んでいるこれらの政府は、この地域のEV需要の増加に対応することを目的として、リチウムイオン電池の生産を促進するための複数のイニシアチブを立ち上げています。

- 例えば、2024年1月、スウェーデンのリチウムイオン電池メーカーであるNorthvoltは、ドイツからの9億200万ユーロ(9億8,643万米ドル)という多額の国家支援包装のEU承認を獲得しました。この資金は、ドイツのハイデにEV用電池生産施設を設立するためのものです。このような承認は、ドイツの取り組みを後押しするだけでなく、EU全体のネット・ゼロの野心とも一致します。こうした取り組みは、クリーンエネルギー解決策としてのリチウムイオン電池の採用を後押しし、その結果、今後数年間の電池材料の需要を押し上げることになります。

- 近年、ドイツはリチウムイオン電池の先進的リサイクル技術の先駆者として台頭してきました。企業と研究機関の共同研究は、使用済み電池からリチウム、コバルト、ニッケルなどの貴重な材料を効率的に再生することに重点を置いています。

- 例えば、2024年5月、ポーランドのElemental Strategic Metals(ESM)は、米国の新興企業Ascend Elementsと共同で、リチウムイオン電池のリサイクル施設の計画を発表しました。年間2万5,000トンの処理能力を見込み、2024年秋に着工、2026年の操業開始を目指します。このような取り組みにより、原料生産が促進され、将来的にEV用電池材料の生産量が増加すると予想されます。

- このような開発状況を踏まえると、現在進行中のプロジェクトやイニシアチブがEV電池の生産を強化し、今後数年間でEV電池材料の需要を大幅に高めることは明らかです。

ドイツの電気自動車用電池材料産業概要

ドイツの電気自動車用電池材料市場は半分断されています。主要参入企業(順不同)は、Targray Technology International Inc.、BASF SE、Arkema SA、Solvay SA、Umicore SAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車販売の成長

- 政府の支援施策と施策

- 抑制要因

- 原料需要の供給ギャップ

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- リチウムイオン電池

- 鉛蓄電池

- その他

- 材料

- 正極

- 負極

- 電解液

- セパレーター

- その他

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Targray Technology International Inc

- BASF SE

- Arkema SA

- Solvay SA

- Umicore SA

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- Johnson Matthey

- Henkel Adhesive Technologies

- Heraeus Group

- Wacker Chemie AG

- その他の著名な企業一覧

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 電池技術の進歩

目次

Product Code: 50003563

The Germany Electric Vehicle Battery Materials Market size is estimated at USD 1.55 billion in 2025, and is expected to reach USD 3.03 billion by 2030, at a CAGR of 14.3% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, growing electric vehicle (EV) sales and supportive government policies and regulations are expected to drive the demand for electric vehicle battery materials during the forecast period.

- On the other hand, issues related to the raw material supply chain and price fluctuations are likely to negatively impact the market studied.

- Nevertheless, technological advancements in batteries like higher energy density, faster charging times, improved safety, and longer lifespan are expected to create significant opportunities for electric vehicle battery materials market players in the near future.

Germany Electric Vehicle Battery Materials Market Trends

Growing Electric Vehicle (EVs) Sales Drives the Market

- Rising electric vehicle (EV) sales in Germany are driving up the demand for EV battery materials in the region. As the country sees a surge in EV sales, the need for key battery materials like lithium, cobalt, nickel, and graphite is also escalating. This heightened demand is spurring local production and investment in these materials, bolstering the growth of Germany's battery material supply chain.

- Germany is pivoting towards clean energy, with electric vehicles taking center stage. Over recent years, EV sales in the country have skyrocketed. For example, the International Energy Agency (IEA) reported that in 2023, Germany sold 0.7 million electric vehicles. While this figure remained steady from 2022, it marked a 5.5-fold increase from 2019. With numerous projects and initiatives recently unveiled by the European government, EV sales are poised for significant growth, further amplifying the demand for battery materials.

- The German government actively champions the EV market's expansion, offering subsidies, tax incentives, and enforcing stricter emission regulations. These supportive measures not only bolster the EV market but also extend to the battery material industry. Recently, the government unveiled ambitious incentives, aiming for a fourfold increase in EV sales in the coming years.

- As part of its 2023 initiatives, the government rolled out a substantial subsidy scheme to bolster electric vehicle adoption. New EV buyers were entitled to a subsidy of up to EUR 6,000 (approximately USD 6,500), while those opting for plug-in hybrids could avail up to EUR 4,500 (around USD 4,900). Such measures are anticipated to not only boost EV production and sales but also elevate the demand for battery materials in the years ahead.

- Germany's vibrant EV market is a hotbed for battery technology innovation. Major German corporations, alongside research institutions, are channeling investments into pioneering materials that promise enhanced energy density, extended lifespan, and superior safety. Collaborations among leading regional companies are paving the way for advanced battery technologies, setting the stage for heightened EV battery demand.

- In a notable development, a consortium of 15 companies and academic researchers, spearheaded by battery firm VARTA, unveiled a cutting-edge sodium-ion battery technology in May 2024. This next-gen battery promises high performance, cost-effectiveness, and environmental friendliness, catering to EVs and other applications. The consortium has earmarked mid-2027 for the project's culmination. Such breakthroughs are set to not only accelerate the demand for sophisticated EV batteries but also amplify the region's appetite for battery materials in the foreseeable future.

- Given these dynamics, the trajectory of EV demand and the corresponding surge in battery material requirements appear robust and promising.

Lithium-Ion Battery Type Dominate the Market

- The growing production of lithium-ion batteries for electric vehicles (EVs) is reshaping the battery materials market. In Germany, as lithium-ion battery production has surged, so too has the demand for lithium. Discoveries of lithium in the region are notably influencing raw material costs.

- Key market players are channeling investments into lithium reserves and R&D, aiming to boost lithium-ion battery production and meet the escalating demand for battery raw materials. As these reserves are continuously discovered, the prices of lithium-ion batteries have seen a downward trend over time.

- For instance, battery prices in 2023 fell to USD 139/kWh, marking a decline of over 13%. With ongoing technological innovations and manufacturing improvements, projections suggest battery pack prices could drop to USD 113/kWh by 2025 and further to USD 80/kWh by 2030.

- Moreover, European governments are actively championing lithium-ion battery production for EVs, spurred by mounting environmental concerns. With a keen focus on achieving net-zero carbon emissions, these governments have launched multiple initiatives to boost lithium-ion battery production, aiming to meet the region's growing EV demand.

- For instance, in January 2024, Northvolt, a Swedish lithium-ion battery manufacturer, secured EU approval for a significant EUR 902 million (USD 986.43 million) state aid package from Germany. This funding is earmarked for establishing an EV battery production facility in Heide, Germany. Such endorsements not only bolster Germany's efforts but also align with the broader EU's net-zero ambitions. These initiatives are poised to bolster the adoption of lithium-ion batteries as a clean energy solution, subsequently driving up the demand for battery materials in the years ahead.

- In recent years, Germany has emerged as a leader in pioneering advanced recycling technologies for lithium-ion batteries. Collaborations between companies and research institutions are focused on efficiently reclaiming valuable materials, including lithium, cobalt, and nickel, from spent batteries.

- For instance, in May 2024, Elemental Strategic Metals (ESM), a Polish entity, in collaboration with Ascend Elements, a US start-up, unveiled plans for a lithium-ion battery recycling facility. With a projected capacity of 25,000 tonnes annually, construction is set to commence in autumn 2024, aiming for operational status by 2026. Such endeavors are anticipated to boost raw material production and elevate the output of EV battery materials in the future.

- Given these developments, it's evident that ongoing projects and initiatives are set to bolster EV battery production and significantly heighten the demand for EV battery materials in the coming years.

Germany Electric Vehicle Battery Materials Industry Overview

Germany's electric vehicle battery materials market is semi-fragmented. Some key players (not in particular order) are Targray Technology International Inc., BASF SE, Arkema SA, Solvay SA, Umicore SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Raw Material Demand Supply Gap

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Targray Technology International Inc

- 6.3.2 BASF SE

- 6.3.3 Arkema SA

- 6.3.4 Solvay SA

- 6.3.5 Umicore SA

- 6.3.6 Mitsubishi Chemical Group Corporation

- 6.3.7 UBE Corporation

- 6.3.8 Johnson Matthey

- 6.3.9 Henkel Adhesive Technologies

- 6.3.10 Heraeus Group

- 6.3.11 Wacker Chemie AG

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology