アジア太平洋の電気自動車用電池材料:市場シェア分析、産業動向、成長予測(2025~2030年)

Asia Pacific Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636275

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

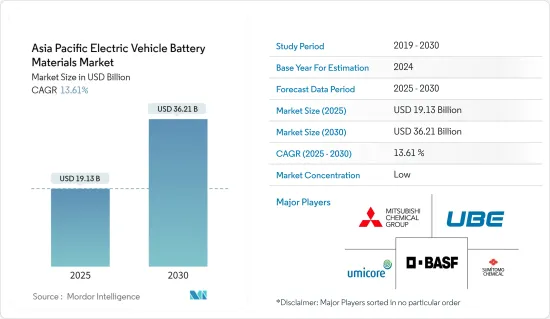

アジア太平洋の電気自動車用電池材料市場規模は2025年に191億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.61%で、2030年には362億1,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車(EV)の販売台数の伸びと政府の規制と施策が、予測期間中の電気自動車用電池材料の需要を牽引すると予想されます。

- 逆に、信頼性と費用対効果に起因する従来型自動車への嗜好の広がりは、電気自動車とその電池の販売に課題を突きつけています。

- しかし、エネルギー密度の向上、急速充電、安全性の向上、寿命の延長といった特徴を誇る電池技術の飛躍的進歩は、電気自動車用電池材料市場の参入企業にとって大きなビジネス機会となると考えられます。

- 電気自動車の急速な普及に後押しされ、インドは予測期間中、アジア太平洋の電気自動車用電池材料市場で最も急成長している地域となる展望です。

アジア太平洋の電気自動車用電池材料市場動向

リチウムイオン電池タイプが市場を独占

- 電気自動車(EV)用リチウムイオン電池の生産量の増加は、電池材料市場に顕著な影響を与えています。この電池生産の急増は、リチウム需要の顕著な増加を促しています。この地域におけるリチウムの発見は、原料コストに顕著な影響を及ぼしています。

- 主要な市場関係者は、リチウムイオン電池の生産を促進し、電池原料の需要増に対応するため、リチウム埋蔵量と研究開発への投資を行っています。こうした埋蔵量の継続的な発見は、リチウムイオン電池の価格を長期的に押し下げるのに役立っています。

- 例えば、電池価格は2023年に139米ドル/kWhに落ち着き、13%以上下落しました。技術の進歩や製造の改善により、電池パックの価格は2025年には113米ドル/kWh、2030年には80米ドル/kWhまで下がるという予測もあります。

- さらに、環境問題の高まりを受けて、アジア太平洋の政府はEV用リチウムイオン電池の生産を積極的に支持しています。純炭素排出量ゼロの達成に強い関心を寄せるこれらの政府は、EV需要の急増に対応するため、リチウムイオン電池の生産を促進する複数のイニシアチブを打ち出しています。

- 例えば、韓国は2023年12月、EV用電池に焦点を当てた電池産業を強化するため、今後5年間で290億米ドルの投資計画を発表しました。この戦略には、電池のサプライチェーンの多様化や、韓国の大手企業に対する税制優遇措置が含まれています。これらの企業は、必要不可欠な電池材料の採掘権を確保するため、海外進出を支援しています。こうした構想は、クリーンエネルギーの代替としてのリチウムイオン電池の生産を拡大するだけでなく、当面の電池材料の需要も拡大させる構えです。

- さらに、リチウムイオン電池の価格下落は、需要の急増と新しい生産工場の設立と相まって、この地域の電池原料の需要を強化しています。近年、世界の主要企業が、この地域でのEV用リチウムイオン電池の生産拡大を目指したプロジェクトに乗り出しています。

- 例えば、BMWは2024年2月、タイのラヨーンに新しい電池工場を建設する計画を発表しました。この動きは、同国の電池・サプライチェーンを強化するものと期待されています。BMWは、タイをEV用電池の重要な輸出拠点とし、アジア太平洋市場により広く対応することを構想しています。このような取り組みにより、タイでの電池生産が促進され、今後数年間でリチウムイオン電池材料の需要が高まることが予想されます。

- こうした開発を踏まえると、リチウムイオン電池の生産が進み、EV用電池材料の需要が急増することは明らかです。

著しい成長を遂げるインド

- インドは、電気自動車(EV)用電池材料のセグメントで重要な位置を占めています。同国は、必須材料の安定供給を確保しながら、戦略的に電池製造能力を強化しています。

- 近年、インドは地域のEV生産状況において圧倒的な力を持つようになりました。例えば、国際エネルギー機関(IEA)の報告によると、2023年のインドの電気自動車販売台数は8万2,000台で、2022年から70.8%急増し、2019年からは119倍という驚異的な伸びを示しました。政府がいくつかの取り組みやプロジェクトを立ち上げていることから、EV販売の勢いは今後も続くと考えられます。

- インドは、リチウム、コバルト、ニッケルといった重要な材料の安定的かつ倫理的な供給を確保することに重点を置いています。しかし、この取り組みには大きな課題があります。原料の難問に取り組むため、インドは国内の埋蔵量を掘り下げ、国際的なパートナーシップを築こうとしています。インドの焦点は、EV用電池材料の需要急増に対応するため、その鉱物資源を活用することにあります。

- 注目すべき開発として、インド地質調査所(GSI)は2023年2月、ジャンムー・カシミール州のSalal-Haimana地域で590万トンと推定されるリチウム埋蔵量を発掘しました。非鉄金属であるリチウムは、電池のエネルギー貯蔵システムやEVアプリケーションにおいて極めて重要な役割を果たしています。今回の発見は、EV向けの急成長するリチウム需要を満たし、当面EV用電池材料の生産を強化する態勢を整えています。

- インドの大手EVメーカーは、急増するEV需要に合わせて電池生産能力を増強しており、インフラと技術の両面で多額の投資が必要となっています。

- 重要な動きとして、オラ・エレクトリックは2024年7月、タミル・ナードゥ州にあるギガファクトリーの初期段階に1億米ドルを投資することを発表しました。この施設では、国産のリチウムイオン電池を生産する予定です。オラ・エレクトリックの戦略的目標は、来年初頭までに電池セルを自社製に移行し、現在の韓国と中国のサプライヤーから脱却することです。このような大胆な投資は、EV用リチウムイオン電池の生産を加速させるだけでなく、同地域におけるEV用電池材料の需要を増幅させる構えです。

- このような開発により、EV用電池の生産は大幅に増加し、今後数年間でEV用電池材料の需要が急増することが予想されます。

アジア太平洋の電気自動車用電池材料産業概要

アジア太平洋の電気自動車用電池材料市場は断片的です。主要参入企業(順不同)は、BASF SE、Mitsubishi Chemical Group Corporation、UBE Corporation、Umicore SA、Sumitomo Chemicalなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車販売の成長

- 政府の支援施策と施策

- 抑制要因

- 従来型自動車への依存

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- リチウムイオン電池

- 鉛蓄電池

- その他

- 材料

- 正極

- 負極

- 電解液

- セパレーター

- その他

- 地域

- 中国

- インド

- オーストラリア

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Sumitomo Chemical Co., Ltd.

- BASF SE

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- Umicore SA

- Contemporary Amperex Technology Co. Limited

- Nichia Corporation

- ENTEK International LLC

- LG Chem

- Kureha Corporation

- その他の著名な企業一覧

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 電池技術の進歩

目次

Product Code: 50003562

The Asia Pacific Electric Vehicle Battery Materials Market size is estimated at USD 19.13 billion in 2025, and is expected to reach USD 36.21 billion by 2030, at a CAGR of 13.61% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, growing electric vehicle (EV) sales and supportive government policies and regulations are expected to drive the demand for electric vehicle battery materials during the forecast period.

- Conversely, the widespread preference for conventional vehicles, attributed to their reliability and cost-effectiveness, poses a challenge to the sales of electric vehicles and their batteries.

- However, breakthroughs in battery technology-boasting features like enhanced energy density, quicker charging, heightened safety, and extended lifespans-are set to unlock substantial opportunities for players in the electric vehicle battery materials market.

- Driven by surging electric vehicle adoption, India is poised to lead as the fastest-growing region in Asia Pacific's electric vehicle battery materials market during the forecast period.

Asia Pacific Electric Vehicle Battery Materials Market Trends

Lithium-Ion Battery Type Dominate the Market

- The growing production of lithium-ion batteries for electric vehicles (EVs) has notably influenced the battery materials market. This surge in battery production has driven a marked increase in lithium demand. Discoveries of lithium in the region have a pronounced effect on raw material costs.

- Key market players are channeling investments into lithium reserves and R&D, aiming to boost lithium-ion battery production and meet the escalating demand for battery raw materials. Ongoing discoveries of these reserves have been instrumental in driving down lithium-ion battery prices over time.

- For instance, battery prices saw a dip in 2023, settling at USD 139/kWh, marking a decline of over 13%. With the current trajectory of technological advancements and manufacturing improvements, projections suggest battery pack prices could further drop to USD 113/kWh by 2025 and USD 80/kWh by 2030.

- Moreover, in response to escalating environmental concerns, governments in the Asia Pacific are actively championing lithium-ion battery production for EVs. With a keen focus on achieving net-zero carbon emissions, these governments have launched multiple initiatives to boost lithium-ion battery production, catering to the surging EV demand.

- For instance, in December 2023, South Korea unveiled a USD 29 billion investment plan over the next five years to bolster its battery industry, with a spotlight on EV batteries. The strategy includes diversifying battery supply chains and providing tax incentives to major South Korean firms. These firms are being supported in their overseas ventures to secure mining rights for essential battery materials. Such initiatives are poised to not only amplify lithium-ion battery production as a clean energy alternative but also escalate the demand for battery materials in the foreseeable future.

- Additionally, the declining prices of lithium-ion batteries, coupled with a surging demand and the establishment of new production plants, are bolstering the demand for battery raw materials in the region. In recent years, top global firms have embarked on projects aimed at boosting lithium-ion battery production for EVs in the region.

- For instance, in February 2024, BMW unveiled plans for a new battery factory in Rayong, Thailand. This move is anticipated to bolster the nation's battery supply chains. BMW envisions Thailand as a pivotal export hub for its EV batteries, catering to the broader Asia Pacific market. Such undertakings are set to expedite battery production in Thailand and heighten the demand for lithium-ion battery materials in the years to come.

- Given these developments, it's clear that advancements in lithium-ion battery production and the surging demand for EV battery materials will continue to grow in the coming years.

India to Witness Significant Growth

- India is positioning itself as a key player in the electric vehicle (EV) battery materials arena. The nation is strategically bolstering its battery manufacturing capabilities while ensuring a steady supply of essential materials.

- In recent years, India has emerged as a dominant force in the regional EV production landscape. For instance, the International Energy Agency (IEA) reported that in 2023, India sold 82,000 electric vehicles, marking a 70.8% surge from 2022 and an astonishing 119-fold increase since 2019. With the government launching several initiatives and projects, the momentum in EV sales is set to continue its upward trajectory.

- India is placing a strong emphasis on ensuring a consistent and ethical supply of vital materials such as lithium, cobalt, and nickel. This endeavor, however, poses significant challenges. To tackle the raw material conundrum, India is delving into its domestic reserves and forging international partnerships. The nation's focus remains on harnessing its mineral wealth to cater to the surging demand for EV battery materials.

- In a notable development, the Geological Survey of India (GSI) unearthed lithium reserves estimated at 5.9 million tonnes in the Salal-Haimana region of Jammu and Kashmir in February 2023. Lithium, a non-ferrous metal, plays a pivotal role in battery energy storage systems and EV applications. This discovery is poised to satiate the burgeoning lithium demand for EVs and bolster EV battery material production in the foreseeable future.

- Leading Indian EV manufacturers are ramping up their battery production capabilities to align with the surging EV demand, necessitating substantial investments in both infrastructure and technology.

- In a significant move, Ola Electric, in July 2024, unveiled a USD 100 million investment for the initial phase of its gigafactory in Tamil Nadu. This facility is set to produce indigenous lithium-ion batteries. Ola Electric's strategic goal is to transition to its battery cells by early next year, moving away from its current suppliers in Korea and China. Such a bold investment is poised to not only expedite lithium-ion battery production for EVs but also amplify the demand for EV battery materials in the region.

- Given these developments, the trajectory of battery production for EVs is set for a significant boost, leading to a pronounced surge in demand for EV battery materials in the coming years.

Asia Pacific Electric Vehicle Battery Materials Industry Overview

Asia Pacific's electric vehicle battery materials market is fragmented. Some key players (not in particular order) are BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Umicore SA, Sumitomo Chemical Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Dependence on Conventional Vehicle

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Australia

- 5.3.4 Japan

- 5.3.5 South Korea

- 5.3.6 Malaysia

- 5.3.7 Thailand

- 5.3.8 Indonesia

- 5.3.9 Vietnam

- 5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Sumitomo Chemical Co., Ltd.

- 6.3.2 BASF SE

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 UBE Corporation

- 6.3.5 Umicore SA

- 6.3.6 Contemporary Amperex Technology Co. Limited

- 6.3.7 Nichia Corporation

- 6.3.8 ENTEK International LLC

- 6.3.9 LG Chem

- 6.3.10 Kureha Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology

アジア太平洋の電気自動車用電池材料:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日