英国の電気自動車用リチウムイオン電池:市場シェア分析、産業動向、成長予測(2025~2030年)

United Kingdom Lithium-ion Battery For Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636222

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

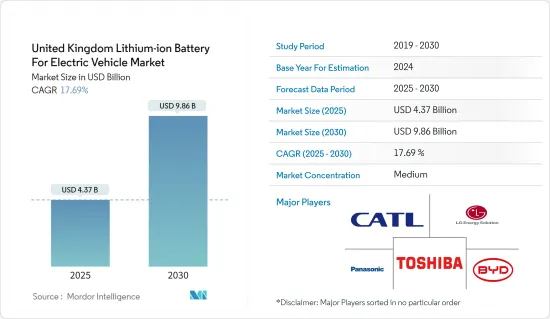

英国の電気自動車用リチウムイオン電池市場規模は2025年に43億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは17.69%で、2030年には98億6,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車導入の増加、リチウムイオン電池価格の下落、全国的な電気自動車に対する政府の支援施策や取り組みが、予測期間中の電気自動車用リチウムイオン電池需要を牽引すると予想されます。

- 一方、原料の埋蔵量不足と新興の代替電池技術が、電気自動車用リチウムイオン電池市場の成長を大幅に抑制する可能性があります。

- 電気自動車用の固体リチウムイオン電池の採用は、英国の電気自動車用リチウムイオン電池市場に膨大な機会を生み出すと予想されます。

英国の電気自動車用リチウムイオン電池市場の動向

リチウムイオン電池の価格低下が市場を牽引

- リチウムイオン電池の価格低下が、英国の電気自動車(EV)用リチウムイオン電池市場の成長を大きく牽引しています。リチウムイオン電池の生産が世界的に増加するにつれて、メーカーは規模の経済の恩恵を受け、生産コストの低下につながります。このコスト削減は消費者や企業に還元され、EVがより手頃な価格になります。

- リチウムイオン電池の価格は通常、他の電池よりも高いです。しかし、市場全体の主要企業は、スケールメリットを得るため、また性能を高めるための研究開発活動に投資しており、競争が激化し、ひいてはリチウムイオン電池の価格を引き下げています。

- 電気自動車(EV)と電池エネルギー貯蔵システム(BESS)の平均電池パック価格が上昇しているため、電池価格は2023年には139米ドル/kWhまで下落し、13%以上低下しました。技術革新と製造強化の軌跡により、電池パック価格はさらに低下し、2025年には113米ドル/kWh、2030年には80米ドル/kWhに達すると予測されます。

- さらに、技術の進歩、生産規模の拡大、サプライチェーンの効率改善により、リチウムイオン電池の価格は着実に低下しています。この動向は世界のエネルギー市場に大きな影響を与え、電気自動車(EV)や再生可能エネルギー貯蔵システムをより安価で身近なものにしています。主要企業はここ数年、著しい技術進歩を遂げています。

- 例えば2024年5月、英国のクリーン技術グループであるAltiliumは、革新的なEcoCathode(TM)湿式冶金リサイクル技術の最新の進歩を発表しました。この技術的ブレークスルーには、新しい電池化学品からのリチウム回収や、リチウムスクラップの混合フィードからの正極活物質(CAM)の生産が含まれます。このような進歩は、今後数年間、先進的なリチウムイオン電池の需要を押し上げ、国全体の電池価格を引き下げると予想されます。

- さらに、リチウムイオン電池の需要拡大を支えるため、各国政府は大規模な投資を発表し、リチウムイオン電池の生産促進に着手しています。リチウムイオン電池の価格低下、需要の増加、英国全土における新しいリチウムイオン生産工場の設立は、エネルギー産業と自動車産業に大きな変化をもたらす相互に関連した現象です。

- 例えば、英国政府は2023年11月、同国の将来のEV生産目標を支援するため、リチウムイオン電池を含む弾力性のある電池サプライチェーンを構築するために5,000万英ポンド(6,300万米ドル)を投資する計画を発表しました。電池戦略は、2030年までの5年間、新たな資本と研究開発資金を含め、ゼロ・エミッション車、電池、サプライチェーンに的を絞った支援を提供することが期待されています。このような投資やインセンティブは、今後数年間、国内での電池生産を加速させ、将来的にはリチウムイオン電池の需要を押し上げる可能性が高いです。

- したがって、このような進歩や取り組みにより、リチウムイオン電池の価格はさらに下がり、他タイプの電池よりもはるかにコスト競合性が高くなり、その結果、英国では多くの用途で採用が進むと予想されます。

電池式電気自動車(BEV)セグメントが著しい成長を遂げる

- 電池式電気自動車(BEV)セグメントは近年大きな成長を遂げているが、この動向は電気自動車(EV)におけるリチウムイオン電池の進歩と採用の増加と密接に結びついています。

- 英国では、電気自動車(EV)の導入が急増しており、これがEV充電器市場の拡大を後押ししています。同国は世界有数のEV生産国です。同国は、クリーンエネルギーへのシフトと電気自動車への移行を進めており、現在、各社がさらに注力している不可欠なセグメントです。

- 同国ではここ数年、BEVの販売台数が飛躍的に伸びています。例えば、国際エネルギー機関(IEA)によると、2023年に英国で販売される電池電気自動車の台数は、2022年から14.8%増の31万台です。電池電気自動車の販売台数は今後数年で大幅に増加すると予想され、国全体でBEV用リチウムイオン電池の需要が高まっている

- 英国は、電気自動車(EV)を推進し、低炭素交通産業への移行を支援するために、いくつかの施策を実施しています。これらの施策は、消費者の総所有コストを削減し、内燃エンジン車からBEVへの転換を促すことを目的としています。

- 例えば、英国は2023年時点で、2030年までに新車販売台数の80%、新車販売台数の70%のバンをゼロエミッション車にすることを義務付け、2035年までに100%に到達させるZEV義務化を定めています。さらに、2030年までにガソリン車とディーゼル車、バンの新車販売が禁止され、2035年までにすべての新車とバンのテールパイプがゼロエミッションになることが義務づけられるようです。このような取り組みや目標は、今後数年間、国内におけるBEVの生産と需要を加速させると考えられます。

- さらに、電気自動車へのシフトが進んでいることも大きな要因です。国内の主要企業は、今後数年間で電池電気自動車の生産台数を増やすために、数多くのプロジェクトや投資を開始しています。

- 例えば、2023年11月、Nissanとそのパートナーは、工場で3つの電気自動車モデル、つまり電気自動車のキャシュカイとジュークを生産する20億英ポンド(25億米ドル)の計画を発表しました。同社はまた、今後数年間で英国全土に新モデルを投入するため、英国の施設とサプライチェーンの準備に11億2,000万ポンド(14億米ドル)を費やしました。このようなプロジェクトは、予測期間中に英国全土でのBEV生産を押し上げると予想されます。

- したがって、こうした取り組みや計画は、予測期間中、同国全体のBEV販売を強化し、リチウムイオン電池の需要を押し上げる可能性が高いです。

英国の電気自動車用リチウムイオン電池産業概要

英国の電気自動車用リチウムイオン電池市場は半分断されています。主要参入企業(順不同)は、LG Energy Solution Ltd、Toshiba Corporation、Panasonic Holdings Corporation、BYD、Contemporary Amperex Technology Co.Ltd.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車(EV)の普及拡大

- リチウムイオン電池価格の低下

- 政府の支援施策とイニシアティブ

- 抑制要因

- 原料の埋蔵量不足

- 新たな代替電池技術

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- 車種

- 乗用車

- 商用車

- その他の車種(二輪車、スクーターなど)

- 推進タイプ

- 電池電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- ハイブリッド電気自動車(HEV)

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略とSWOT分析

- 企業プロファイル

- LG Energy Solution Ltd

- BYD Company Limited

- Toshiba Corporation

- Panasonic Holdings Corporation

- Contemporary Amperex Technology Co. Limited

- AMTE Power

- LiNa Energy

- Echion Technologies

- Saft Groupe SA

- EnerSys

- その他の著名な企業一覧(会社名、本社所在地、関連製品とサービス、連絡先など)

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 電気自動車への固体リチウムイオン電池の採用

目次

The United Kingdom Lithium-ion Battery For Electric Vehicle Market size is estimated at USD 4.37 billion in 2025, and is expected to reach USD 9.86 billion by 2030, at a CAGR of 17.69% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, increasing adoption of electric vehicles, declining lithium-ion battery prices, and supportive government policies and initiatives for electric vehicles across the country are expected to drive the demand for lithium-ion batteries for electric vehicles during the forecast period.

- On the other hand, the lack of raw material reserves and emerging alternative battery technologies can significantly restrain the growth of the lithium-ion batteries for electric vehicles market.

- Nevertheless, the adoption of solid-state lithium-ion batteries for electric vehicles is anticipated to create vast opportunities for the UK lithium-ion batteries for electric vehicles market.

United Kingdom Lithium-ion Battery For Electric Vehicle Market Trends

Declining Lithium-ion Battery Prices Driving the Market

- The declining prices of lithium-ion batteries are significantly driving the growth of the lithium-ion batteries for electric vehicles (EVs) market in the United Kingdom. As the production of lithium-ion batteries increases globally, manufacturers benefit from economies of scale, leading to lower production costs. This cost reduction is passed down to consumers and businesses, making EVs more affordable.

- The price of lithium-ion batteries is usually higher than that of other batteries. However, major players across the market have been investing to gain economies of scale and in R&D activities to enhance their performance, increasing the competition and, in turn, reducing lithium-ion battery prices.

- Owing to the increasing average battery pack prices of electric vehicles (EV) and battery energy storage systems (BESS), battery prices declined in 2023 to USD 139/kWh, a decrease of over 13%. The trajectory of technological innovation and manufacturing enhancements is anticipated to reduce battery pack prices further, with prices projected to reach USD 113/kWh in 2025 and USD 80/kWh in 2030.

- Furthermore, the price of lithium-ion batteries has been steadily decreasing due to technological advancements, increased production scale, and improved supply chain efficiencies. This trend is significantly impacting the global energy market, making electric vehicles (EVs) and renewable energy storage systems more affordable and accessible. Leading companies have made significant technological advances in the past few years.

- For instance, in May 2024, Altilium, a UK-based clean technology group, announced the latest advances in its innovative EcoCathode(TM) hydrometallurgical recycling technology. The technological breakthroughs included the recovery of lithium from new battery chemistries and the production of cathode active materials (CAM) from a mixed feed of lithium scrap. Such advancements are expected to boost the demand for advanced lithium-ion batteries over the coming years and reduce battery prices across the country.

- Additionally, to support the growing demand for lithium-ion batteries, governments have announced significant investments and initiated the promotion of lithium-ion battery production. The decreasing price of lithium-ion batteries, rising demand, and the establishment of new lithium-ion production plants across the United Kingdom are interlinked phenomena driving significant shifts in the energy and automotive industries.

- For instance, in November 2023, the UK government announced plans to invest GBP 50 million (USD 63 million) to build a resilient battery supply chain, including lithium-ion batteries, in support of the country's future aims for EV production. The Battery Strategy is expected to provide targeted support for zero-emission vehicles, batteries, and supply chains, including new capital and R&D funding for five years till 2030. Such investments and incentives are likely to accelerate battery production across the country over the coming years and boost the demand for lithium-ion batteries in the future.

- Hence, such advancements and initiatives are expected to reduce lithium-ion battery prices further, making them much more cost-competitive than other battery types and resulting in their increasing adoption across numerous applications in the United Kingdom.

Battery Electric Vehicles (BEV) Segment to Witness Significant Growth

- The battery electric vehicles (BEV) segment has experienced significant growth in recent years, a trend closely tied to the advancements and increased adoption of lithium-ion batteries in electric vehicles (EVs).

- The United Kingdom is experiencing a significant surge in the adoption of electric vehicles (EVs), which is driving the expansion of the EV charging equipment market. The country is among the leading EV producers worldwide. It has been shifting toward clean energy and transitioning to electric vehicles, which is an essential segment on which companies are currently focusing more.

- BEV sales have been rising exponentially in the country over the last few years. For instance, according to the International Energy Agency (IEA), in 2023, the number of battery electric vehicles sold in the United Kingdom was 0.31 million, up by 14.8% from 2022. The number of battery electric vehicle sales is expected to increase significantly in the coming years, raising the demand for lithium-ion batteries for BEVs across the country.

- The United Kingdom has implemented several policies to promote electric vehicles (EVs) and support the transition to a low-carbon transportation industry. These policies aim to reduce consumers' overall cost of ownership and encourage the switch from internal combustion engine vehicles to BEVs.

- For instance, as of 2023, the United Kingdom had established a ZEV mandate that requires 80% of new cars and 70% of new vans sold to be zero-emission by 2030, reaching 100% by 2035. Furthermore, the sale of new petrol and diesel cars and vans is likely to be banned by 2030, with all new cars and vans required to be zero-emission at the tailpipe by 2035. Such initiatives and targets are likely to accelerate the production and demand of BEVs across the country in the coming years.

- Furthermore, the increasing shift toward electric vehicles is a significant factor. Leading companies around the country have launched numerous projects and investments to raise the production of battery electric vehicles over the coming years.

- For instance, in November 2023, Nissan and its partners announced a GBP 2 billion (USD 2.5 billion) plan to build three electric car models, that is, electric Qashqai and Juke models, at the plant. The company also spent GBP 1.12 billion (USD 1.4 billion) on preparing its UK facilities and supply chains for launching new models across the country in the coming years. Such types of projects are expected to boost BEV production across the country during the forecast period.

- Hence, these initiatives and plans are likely to enhance BEV sales across the country and boost the demand for lithium-ion batteries during the forecast period.

United Kingdom Lithium-ion Battery For Electric Vehicle Industry Overview

The UK lithium-ion batteries for electric vehicles market is semi-fragmented. Some of the key players (not in any particular order) are LG Energy Solution Ltd, Toshiba Corporation, Panasonic Holdings Corporation, BYD, and Contemporary Amperex Technology Co. Limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles (EV)

- 4.5.1.2 Declining Lithium-ion Battery Prices

- 4.5.1.3 Supportive Government Policies and Initiatives

- 4.5.2 Restraints

- 4.5.2.1 Lack of Raw Material Reserves

- 4.5.2.2 Emerging Alternative Battery Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Commercial Vehicles

- 5.1.3 Other Vehicle Types (Bikes, Scooters, etc.)

- 5.2 Propulsion Type

- 5.2.1 Battery Electric Vehicles (BEVs)

- 5.2.2 Plug-in Hybrid Electric Vehicles (PHEVs)

- 5.2.3 Hybrid Electric Vehicles (HEVs)

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted and SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 LG Energy Solution Ltd

- 6.3.2 BYD Company Limited

- 6.3.3 Toshiba Corporation

- 6.3.4 Panasonic Holdings Corporation

- 6.3.5 Contemporary Amperex Technology Co. Limited

- 6.3.6 AMTE Power

- 6.3.7 LiNa Energy

- 6.3.8 Echion Technologies

- 6.3.9 Saft Groupe SA

- 6.3.10 EnerSys

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Adoption of Solid-state Lithium-ion Batteries for Electric Vehicles

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日