|

市場調査レポート

商品コード

1636174

電気自動車用リチウムイオン電池:市場シェア分析、産業動向、成長予測(2025~2030年)Lithium-ion Battery For Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電気自動車用リチウムイオン電池:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

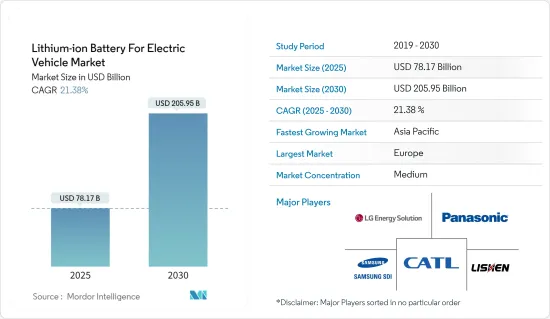

電気自動車用リチウムイオン電池市場規模は、2025年に781億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは21.38%で、2030年には2,059億5,000万米ドルに達すると予測されます。

中期的には、リチウムイオン電池の価格低下、電気自動車の普及拡大、政府の支援施策や取り組みが、予測期間中の電気自動車市場におけるリチウムイオン電池の需要を牽引すると予想されます。

一方、代替電池技術の台頭と原料の需給ミスマッチが、予測期間中の市場成長の妨げになると予想されます。電気自動車への固体リチウムイオン電池の採用は、電気自動車市場におけるリチウムイオン電池の広大な機会を創出すると予想されます。アジア太平洋では電気自動車の採用が増加しているため、電気自動車市場のリチウムイオン電池はアジア太平洋が支配的な地域になると予想されます。

電気自動車用リチウムイオン電池市場動向

電池式電気自動車(BEV)セグメントが著しい成長を遂げる

- 電池電気自動車(BEV)は、一般に電気モーターを搭載した電気自動車としても知られています。BEVは完全な電気自動車で、内燃機関車(ICE)、燃料タンク、排気管を搭載せず、推進力を電気に依存しています。車両のエネルギーは電池パックから供給され、グリッドから充電されます。BEVはゼロ・エミッション車であり、従来のガソリン車による有害なテールパイプ排出や大気汚染の危険はないです。

- 世界の自動車産業は、電気自動車、特に電池電気自動車(BEV)が勢いを増し、人気を集めるにつれ、変貌を遂げています。技術の進歩、政府の支援、環境問題への関心の高まりにより、BEVは気候変動という課題に対処し、化石燃料への依存を減らす有望なソリューションとして浮上しました。

- 近年、電池電気自動車の採用は世界的に大きく伸びています。電池技術の向上が走行距離の延長と充電インフラの急増につながり、当初の参入障壁を克服するのに役立っています。Tesla、BYD、Tata、Chevrolet、Nissan、Fordなどの自動車メーカーは、BEVの普及に欠かせない存在であり、幅広い消費者にアピールする手頃な価格のモデルを提供しています。

- 国際エネルギー機関(IEA)によると、2023年の世界の電池電気自動車(BEV)販売台数は約950万台で、2022年の約730万台から30%以上増加しました。同様に、2023年の世界のBEV車在庫総数は約2,800万台に達しました。BEVの販売台数が増え続ける中、リチウムイオン電池などのEV用電池の需要はますます重要になっています。

- 各国はBEVの普及を加速させるため、さまざまな取り組みやインセンティブを実施しています。米国では、連邦政府による税額控除、州によるリベート、補助金によって、EVが手頃な価格になり、より多くの人々が利用できるようになりました。いくつかの州は、内燃機関車(ICE)を段階的に廃止し、電気自動車の利用を促進するという野心的な目標を設定しています。そのため、BEVの採用が増加しており、予測期間中にリチウムイオン電池の需要を押し上げると予想されます。

- 今後数年間、複数の政府がEVの採用を促進する予定です。2024年5月、フランス政府は国内の自動車メーカーに対し、10年後までに200万台の電気自動車またはハイブリッド車を生産するという目標を設定しました。財務省のブリーフィングによると、政府との新たな中期計画合意の下、産業は2022年の20万台から2027年までに80万台の電気自動車販売という中間目標に合意することになっています。自動車メーカーは、2022年には1万6,500台しか販売できなかった電気自動車を、同期間に年間10万台に増やすことを目標としています。これらにより、リチウムイオン電池のようなEV用二次電池の膨大な需要が創出され、この地域の道路を走る電池式電気自動車の増加に対応することが期待されます。

- 中国の自動車メーカー数社は、販売を拡大するため、EVの製造・組立工場を世界各地に設立・拡大しようとしています。例えば、輸出台数で中国最大の自動車メーカーである奇瑞汽車(Chery Auto)は2024年4月、スペインのEVモーターズと合弁会社を設立し、カタルーニャ地方に欧州初の生産拠点を開設すると発表しました。生産開始は2024年後半を予定しており、ジュニアパートナーの奇瑞はこの工場でオモダ車を生産します。自動車メーカーは2030年までに英国に自動車工場を建設することを検討しています。

- 2024年3月、インド政府は新たに5億米ドル相当の電気自動車(EV)施策を承認し、世界のEV企業から投資を呼び込むためのさまざまなインセンティブを提供するとともに、インドを最先端のEV製造の一大拠点と位置づけた。その他の目的には、インドの消費者が最先端のEVモデルにアクセスできるようにすること、Make in Indiaのエコシステムを拡大すること、生産コストを引き下げること、競合国内自動車製造業を育成することなどが含まれます。このようなシナリオは、BEV製造産業にプラスの影響を与え、ひいてはEV用途のリチウムイオン電池の需要を押し上げると予想されます。

- 上記の要因から、予測期間中はBEVセグメントが電気自動車(EV)用リチウムイオン電池市場を独占すると予想されます。

アジア太平洋が市場を独占する見込み

- アジア太平洋は、世界最大かつ最速で成長する経済圏の本拠地であるため、世界の電気自動車(EV)用リチウムイオン電池市場を独占すると予想されます。中国、インド、日本などの国々では電気自動車の導入が急増しており、リチウムイオン電池は重要な電池化学品となっています。

- 国際エネルギー機関(IEA)の発表によると、中国における(BEVとPHEVの両方を含む)EV車の総保有台数は、2023年には約2,180万台となります。同様に、インドと日本の同年のEV車在庫台数は、それぞれ約15万台と約54万台でした。2023年の中国のEV電池需要は年間約417GWhで、2023年の世界需要の約54%を占め、2022年から32%以上の急増を記録しました。これは、EV用電池における中国の優位性の重要性を浮き彫りにしています。

- アジア太平洋も電気自動車と電池システムの製造拠点として台頭してきており、リチウムイオン電池などの二次電池の著しい開発が期待されています。中国、韓国、日本の大手自動車メーカーは、この地域のリチウムイオン電池製造能力を加速させると予想されます。

- 国際エネルギー機関(IEA)によると、アジア太平洋のリチウムイオン電池製造能力は、今後数年間で中国を筆頭に大きく成長すると予想されています。同機関は、中国のリチウムイオン電池製造能力は2022年の約1.20TWhから2030年には4.65TWhに増加すると推定しています。

- この地域では、リチウムイオン電池の開発が進んでいます。2024年6月、インドの電池メーカーAmara Raja Energy and Mobilityは、中国のGotion High Tech Co.傘下のGotion-InoBat-Batteries(GIB)と、インドでリチウムイオン電池を生産するライセンス契約を締結しました。GIBエナジーXスロバキアはGotionとスロバキアのInoBatとの合弁会社で、Gotionのリチウムイオン電池用リン酸鉄リチウム技術をAmara Rajaにライセンス供与します。

- ライセンス契約に基づき、インド企業はセル技術IPへのアクセス、ギガファクトリー施設設立のサポート、Gotionの世界サプライチェーンネットワークへの統合を得る。ドイツの自動車メーカー、Volkswagenを筆頭株主とするゴティオンは、新エネルギー車向けのリチウムイオン二次電池を専門としています。インドの自動車メーカーは主に中国と韓国からEV用電池を輸入しており、国内の電池サプライヤーは近年、国内でのリチウムイオン電池生産能力の開発に投資しています。

- アジア太平洋には、リチウム、コバルト、黒鉛など、リチウムイオン電池に使用される重要な原料の世界最大級の生産・供給地もあります。このように原料が豊富に入手可能なことと、この地域の強力な製造能力が相まって、リチウムイオン電池市場の成長にとって有利な環境を作り出しています。

- 例えば、インドネシアは世界のニッケル埋蔵量の約22%を保有しています。同様に、西オーストラリア地域は世界のリチウム埋蔵量の24%を占めており、アジア太平洋はリチウムイオン電池の開発と製造に理想的な地域となっています。

- したがって、上記の点から、予測期間中、アジア太平洋は電気自動車市場におけるリチウムイオン電池の支配的な地域になると予想されます。

電気自動車用リチウムイオン電池産業概要

電気自動車用リチウムイオン電池市場は半固体化しています。市場の主要企業には、Panasonic Corporation、SamsungSDI、Contemporary Amperex Technology(CATL)、LG Energy Solution Ltd、Tianjin Lishen Battery Joint-Stockなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- リチウムイオン電池価格の下落

- 電気自動車の普及拡大

- 政府の支援施策とイニシアティブ

- 抑制要因

- 代替電池技術の台頭

- 原料の需給ミスマッチ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 車種

- 乗用車

- 商用車

- その他(二輪車、スクーターなど)

- 推進タイプ

- 電池電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- ハイブリッド電気自動車(HEV)

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- マレーシア

- インドネシア

- ベトナム

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- ナイジェリア

- カタール

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略とSWOT分析

- 企業プロファイル

- Panasonic Corporation

- Samsung SDI Co. Ltd

- Contemporary Amperex Technology Co. Ltd(CATL)

- Tianjin Lishen Battery Joint-Stock Co. Ltd

- LG Energy Solution Ltd

- Trontek Electronics Pvt. Ltd

- Greenfuel Energy Solutions Pvt. Ltd

- Tesla Inc.

- その他の著名な企業一覧(会社名、本社所在地、関連製品およびサービス、連絡先など)

- 市場ランキング分析

第7章 市場機会と今後の動向

- 電気自動車への固体リチウムイオン電池の採用

The Lithium-ion Battery For Electric Vehicle Market size is estimated at USD 78.17 billion in 2025, and is expected to reach USD 205.95 billion by 2030, at a CAGR of 21.38% during the forecast period (2025-2030).

Over the medium term, declining lithium-ion battery prices, increasing adoption of electric vehicles, and supportive government policies and initiatives are expected to drive the demand for lithium-ion batteries in the electric vehicle market during the forecast period.

On the other hand, the emerging alternative battery technologies and the demand-supply mismatch of raw materials are expected to hinder the market's growth during the forecast period. The adoption of solid-state lithium-ion batteries for electric vehicles is anticipated to create vast opportunities for lithium-ion batteries in the electric vehicle market. Due to the increasing adoption of electric vehicles in the region, Asia-Pacific is expected to be a dominant region for lithium-ion batteries in the electric vehicle market.

Lithium-ion Battery For Electric Vehicle Market Trends

Battery Electric Vehicle (BEV) Segment to Witness Significant Growth

- Battery electric vehicles (BEVs) are also commonly known as electric vehicles with an electric motor. BEVs are fully electric vehicles that typically do not include an internal combustion engine (ICE), fuel tank, or exhaust pipe and rely on electricity for propulsion. The vehicle's energy comes from the battery pack, which is recharged from the grid. BEVs are zero-emission vehicles, as they do not generate harmful tailpipe emissions or air pollution hazards caused by traditional gasoline-powered vehicles.

- The global automotive industry has been transforming, with electric vehicles, particularly battery electric vehicles (BEVs), gaining momentum and popularity. With the growing technological advancements, government support, and increasing environmental concerns, BEVs emerged as a promising solution to address the challenges of climate change and reduce reliance on fossil fuels.

- In recent years, the adoption of battery-electric vehicles has grown significantly worldwide. Improving battery technology has led to extended driving ranges and a surge in charging infrastructure, helping overcome the initial entry barriers. Automakers such as Tesla, BYD, Tata, Chevrolet, Nissan, and Ford are vital in popularizing BEVs, offering affordable models that appeal to a broader range of consumers.

- As per the International Energy Agency (IEA), the global battery electric vehicle (BEV) cars sales were around 9.5 million units (BEV cars) in 2023, an increase of over 30% from around 7.3 million units in 2022. Similarly, the total BEV car stocks worldwide reached around 28 million units in 2023. As the sales of BEVs continue to rise, the demand for EV batteries, such as lithium-ion batteries, has become increasingly vital.

- Countries have been implementing various initiatives and incentives to accelerate the adoption of BEVs. In the United States, federal tax credits, state rebates, and subsidies helped make EVs affordable and accessible to a broader audience. Several states have set ambitious targets to phase out internal combustion engine (ICE) vehicles and promote the use of electric cars. Therefore, the growing adoption of BEVs is anticipated to boost the demand for lithium-ion batteries over the forecast period.

- Several governments plan to boost the adoption of EVs in the coming years. In May 2024, the French government set a goal for the nation's carmakers to produce two million electric or hybrid vehicles by the end of the decade. Under a new medium-term planning agreement with the government, the industry is set to agree to an interim goal of 800,000 electric vehicle sales by 2027, up from 200,000 in 2022, according to a finance ministry briefing. Carmakers aim to increase sales of electric light utility vehicles to 100,000 annually over the same period, from only 16,500 in 2022. All these are expected to create a vast demand for rechargeable EV batteries, such as lithium-ion batteries, to support the growing battery electric vehicles on the roads in the region.

- Several Chinese carmakers have been looking to set up and expand EV manufacturing and assembly plants globally to ramp up sales. For example, Chery Auto, China's largest automaker by export volume, announced on April 2024 that it signed a joint venture with Spain's EV Motors to open its first European manufacturing site in Catalonia. The production is set to start later in 2024, with junior partner Chery producing its Omoda vehicles at the plant. Carmakers are considering building car factories in Britain by 2030.

- In March 2024, the Indian government approved a new USD 500-million-worth Electric Vehicle (EV) Policy, offering a range of incentives to draw investments from global EV companies and positioning India as a prime manufacturing hub for state-of-the-art EVs. Other objectives include providing Indian consumers access to cutting-edge EV models, expanding the Make in India ecosystem, lowering production costs, and fostering a competitive domestic auto manufacturing industry. Such a scenario is expected to impact the BEV manufacturing industry positively, which, in turn, boosts the demand for lithium-ion batteries for EV applications.

- Due to the abovementioned factors, the BEV segment is expected to dominate the lithium-ion battery for electric vehicle (EV) market over the forecast period.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is expected to dominate the global lithium-ion battery for electric vehicle (EV) market, as the region is home to some of the world's largest and fastest-growing economies. Countries such as China, India, and Japan are experiencing a surge in the adoption of electric vehicles, where lithium-ion batteries are crucial battery chemistries.

- As per the International Energy Agency (IEA), the total EV car stocks, including (both BEV and PHEV) in China was around 21.8 million units in 2023. Similarly, India and Japan had approximately 0.15 million and 0.54 million units of EV car stocks in the same year, respectively. In 2023, China had an EV battery demand of about 417 GWh per year, or about 54% of the world demand in 2023, recording over 32% surge from 2022. This highlights the importance of the country's dominance in EV batteries.

- Asia-Pacific is also emerging as a manufacturing hub for electric vehicles and battery systems, which is expected to witness significant developments in rechargeable batteries such as lithium-ion batteries. Major automotive manufacturers in China, South Korea, and Japan are expected to accelerate the region's lithium-ion battery manufacturing capacity.

- As per the International Energy Agency (IEA), the lithium-ion battery manufacturing capacity in Asia-Pacific is expected to grow significantly in the coming years, with China leading the way. The agency estimated that the Chinese lithium-ion battery manufacturing capacity will rise to 4.65 TWh in 2030 from around 1.20 TWh in 2022.

- The region has been seeing developments in the lithium-ion batteries. In June 2024, Indian battery maker Amara Raja Energy and Mobility signed a licensing agreement with Gotion-InoBat-Batteries (GIB), a unit of China-based Gotion High Tech Co, to produce lithium-ion batteries in India. GIB EnergyX Slovakia, a joint venture between Gotion and Slovakia-based InoBat, will license Gotion's lithium iron phosphate technology for lithium-ion cells to a unit of Amara Raja.

- Under the licensing agreement, the Indian company will gain access to cell technology IP, support for establishing Gigafactory facilities, and integration into Gotion's global supply chain network. Gotion, whose largest shareholder is the German automaker Volkswagen, specializes in lithium-ion rechargeable batteries for new-energy vehicles. Indian automakers mainly import EV batteries from China and South Korea, and domestic battery suppliers have invested in developing lithium-ion battery production capabilities within the country in recent years.

- Asia-Pacific is also home to some of the world's largest producers and suppliers of critical raw materials used in lithium-ion batteries, such as lithium, cobalt, and graphite. This abundant availability of raw materials, coupled with the region's strong manufacturing capabilities, has created a favorable environment for the growth of the lithium-ion battery market.

- For instance, Indonesia holds approximately 22% of the global nickel reserves. Similarly, the Western Australia region has 24% of the global lithium reserves, which makes Asia-Pacific ideal for lithium-ion battery development and manufacturing.

- Therefore, as per the abovementioned points, Asia-Pacific is expected to be the dominant region for lithium-ion batteries in the electric vehicle market during the forecast period.

Lithium-ion Battery For Electric Vehicle Industry Overview

The lithium-ion battery for the electric vehicle market is semi-consolidated. Some key players in the market include Panasonic Corporation, Samsung SDI Co. Ltd, Contemporary Amperex Technology Co. Ltd (CATL), LG Energy Solution Ltd, and Tianjin Lishen Battery Joint-Stock Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Declining Lithium-ion Battery Prices

- 4.5.1.2 Increasing Adoption of Electric Vehicles

- 4.5.1.3 Supportive Government Policies and Initiatives

- 4.5.2 Restraints

- 4.5.2.1 Emerging Alternative Battery Technologies

- 4.5.2.2 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Commercial Vehicles

- 5.1.3 Other Vehicles (Bikes, Scooters, etc.)

- 5.2 Propulsion Type

- 5.2.1 Battery Electric Vehicle (BEV)

- 5.2.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.2.3 Hybrid Electric Vehicles (HEV)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Nordic

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Thailand

- 5.3.3.6 Malaysia

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Saudi Arabia

- 5.3.4.2 United Arab Emirates

- 5.3.4.3 South Africa

- 5.3.4.4 Egypt

- 5.3.4.5 Nigeria

- 5.3.4.6 Qatar

- 5.3.4.7 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Chile

- 5.3.5.4 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Corporation

- 6.3.2 Samsung SDI Co. Ltd

- 6.3.3 Contemporary Amperex Technology Co. Ltd (CATL)

- 6.3.4 Tianjin Lishen Battery Joint-Stock Co. Ltd

- 6.3.5 LG Energy Solution Ltd

- 6.3.6 Trontek Electronics Pvt. Ltd

- 6.3.7 Greenfuel Energy Solutions Pvt. Ltd

- 6.3.8 Tesla Inc.

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Adoption of Solid-state Lithium-Ion Batteries for Electric Vehicles