|

市場調査レポート

商品コード

1851508

米国の飲料用パッケージング:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)US Beverage Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の飲料用パッケージング:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月06日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

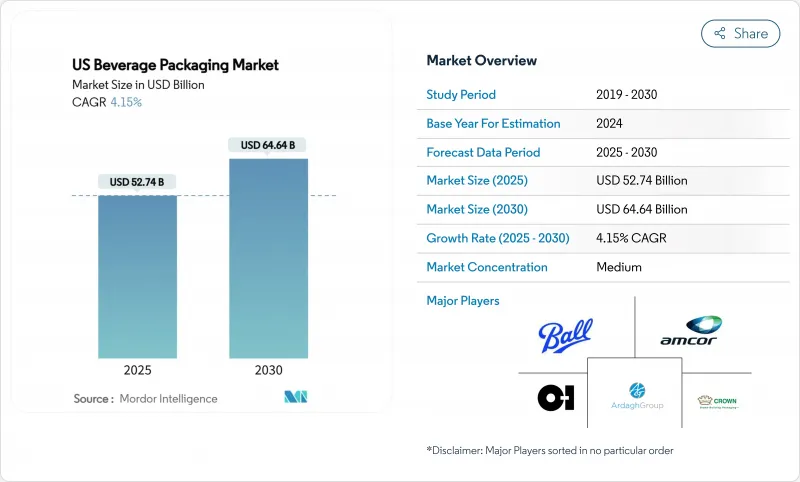

米国の飲料用パッケージング市場は2025年に527億4,000万米ドルに達し、2030年には646億4,000万米ドルに拡大し、CAGR4.15%を記録すると予測されます。

着実な価値成長は、持続可能性規制の強化、リサイクル含有量の義務化、リサイクルしやすいフォーマットへの消費者の嗜好に沿ったアルミニウム中心の戦略によって支えられています。ブランドオーナーは、包装を二酸化炭素削減目標のための費用効果の高いテコとして扱うようになっており、軽量金属容器や高バリア性フレキシブルフィルムへの需要を促進しています。ボール社が2025年1月に12オンス缶に課したサーチャージのようなサプライヤーの価格措置と最低発注量の引き上げは、クラフトビール生産者のコストカーブの形を変え続け、大手飲料メーカーと小規模飲料メーカーの間の格差を広げています。RTD(レディ・トゥ・ドリンク)コーヒー、エネルギー飲料、機能性飲料の並行拡大により、多層プラスチックボトルからアルミ缶や高級グラフィックのスリムボトルへの移行が加速しています。最後に、eコマースの成長により、二次段ボールを排除し、破損を減らし、新たなプレミアム化の道を開く「シップ・イン・オウン・コンテナー」フォーマットの設計が後押しされています。

米国の飲料用パッケージング市場動向と洞察

持続可能性主導の軽量化とrPET義務化

カリフォルニア州のAB793は、2022年にPET飲料容器の再生利用率を15%、2030年までに50%に引き上げることを定め、ニューヨーク州、ニュージャージー州、マサチューセッツ州の議員が積極的に検討している青写真を示しました。再生PETはバージン樹脂に比べて15~25%のコストプレミアがあり、各ブランドは容器1本当たり8~12%のポリマー使用量を削減する軽量化への投資を余儀なくされています。PepsiCo社は、一部の水ラインで100%rPETに切り替えることで、棚の完全性を保ちながら、二酸化炭素排出量を31%削減しました。コンプライアンス主導のライン改修は、ロジスティクスと加工のオーバーヘッドを1個当たり0.03~0.08米ドル追加するが、ブランドは低炭素包装を売り込むことで5~8%の価格上昇を獲得しています。

RTDコーヒーとエナジードリンクの発売急増

RTDエナジー飲料は、コンビニエンスストアのRTD売上高の37%を占め、2020年の28%から増加しており、ほぼすべての主要な新商品がアルミフォーマットを使用しています。モンスター・ビバレッジは、世界販売量の97%をアルミ容器から得ており、プレミアム価格設定によって商品インフレを相殺しながら、2025年の純売上高71億米ドルを可能にしています。アルミの光と酸素を遮断する特性は、コーヒーのアロマと機能性成分の安定性を維持し、チルド流通なしで賞味期限を延ばし、コールドチェーン・コストを最大30%削減するのに役立っています。新しいRTDコーヒーのストック・キープ・ユニット(SKU)は2018年から2023年にかけて73%増加し、そのうちの60%は風味の保持と装飾の汎用性から缶を使用しています。

不安定なバージン樹脂価格

モノマー価格の変動、特にエチレンとパラキシレンは、メキシコ湾岸のスポット市場で定期的に25~30 c/lbに達し、ボトル入り飲料水と炭酸飲料(CSD)製造業者のPETコスト構造を不安定にしています。フォワードヘッジは限られているため、小規模ボトラーにとっては四半期ごとにマージンが圧縮されます。

セグメント分析

2024年にはプラスチックが45.3%と最大のシェアを維持するが、金属パッケージングのCAGRは6.2%と、全素材の中で最速を記録すると予測されます。金属容器の米国の飲料用パッケージング市場規模は、2030年までに270億米ドルを超えると予測されます。これは、限りなくリサイクル可能なフォーマットに対する消費者の嗜好と、より高い消費者再利用(PCR)含有量に対する規制上の信用を反映しています。アルミニウムのバリア特性は、エナジードリンクやRTDコーヒーの風味の変動を防ぎ、単価の上昇を相殺するプレミアムな棚割りをサポートします。

ボール社は、2030年までにリサイクル率90%、リサイクル率85%を目標としており、スコープ3の排出削減を追求する小売業者と共鳴するクローズドループの物語を創造しています。ガラスは、炉の閉鎖やエネルギー多消費型の溶融による逆風に直面しているが、板紙カートンは、97%再生可能なElopak Pure-Pak構造により、大量生産でPETと同等のコストに達し、勢いを増しています。再生PETの不足は、ポリマー含有量を最大15%削減する積極的な軽量化にもかかわらず、プラスチックの普及を依然として抑制しています。

ボトルは2024年に米国の飲料用パッケージング市場の27.8%を占めたが、缶は携帯性、冷蔵効率、カスタマイズ可能な印刷に牽引され、CAGR 7.1%で推移しています。缶の積み重ね可能な形状は、ガラス瓶に比べて20~25%の運賃節約につながり、クラフトビール、フレーバー炭酸飲料、ビタミン強化水メーカーの転換を促しています。

Can Manufacturers Instituteのデータによると、2025年に発売される飲料の70%以上が缶入りです。デジタル印刷技術は、リードタイムを数週間から数日に短縮することで、SKUの普及を加速させる。ボトルの技術革新の中心は、軽量の詰め替え用PETとガラスであり、パウチとカートンは子供用飲料や無菌乳製品の代替品といったニッチな使用事例にアピールしています。

米国の飲料用パッケージング市場は素材(プラスチック、金属、ガラス、板紙)、製品タイプ(ボトル、缶、パウチ、カートン、ビール樽)、用途(アルコール飲料、牛乳・乳製品代替飲料、エネルギー・機能性飲料、炭酸飲料・水、その他飲料)、包装形態(硬質、軟質)で区分されます。市場予測は金額(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 持続可能性主導の軽量化とrPET義務化

- RTDコーヒー/エナジードリンクの発売急増

- クラフトビールのアルミ缶への転換

- Eコマース向けの『自社コンテナでの出荷』フォーマット

- テザーキャップ規制(CFR Title 21の更新)が再設計に拍車をかける

- アルミニウムのリサイクル可能性によるプレミアポジショニング

- 市場抑制要因

- 不安定なバージン樹脂価格

- ガラス炉の能力合理化

- 預金返還の拡大がコンプライアンス・コストを引き上げる

- リサイクルPET原料の不足

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 市場のマクロ経済要因の評価

第5章 市場規模と成長予測

- 材料別

- プラスチック

- 金属

- ガラス

- 板紙

- 製品タイプ別

- ボトル

- 缶

- パウチ

- カートン

- ビール樽

- 用途別

- アルコール飲料

- 牛乳・乳製品代替飲料

- エネルギー・機能性飲料

- 炭酸飲料と水

- その他飲料

- 包装形態別

- 硬質

- 軟質

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Ball Corporation

- Crown Holdings Inc.

- Owens-Illinois Inc.

- Ardagh Group

- Amcor plc

- Berry Global Inc.

- Silgan Holdings Inc.

- WestRock Co.

- Berlin Packaging

- Sonoco Products Co.

- CCL Containers Inc.

- Graphic Packaging Holding

- Tetra Pak Inc.

- SIG Combibloc

- Canpack S.A.

- Plastipak Holdings Inc.

- Novolex

- Printpack Inc.

- ProAmpac LLC

- American Canning