|

市場調査レポート

商品コード

1628779

欧州のガラス瓶と容器:市場シェア分析、産業動向、成長予測(2025~2030年)Europe Glass Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のガラス瓶と容器:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

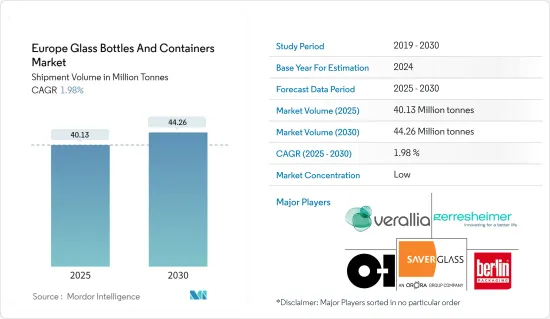

欧州のガラス瓶と容器市場規模は出荷量ベースで、2025年の4,013万トンから2030年には4,426万トンに拡大し、予測期間(2025-2030年)のCAGRは1.98%となる見込みです。

欧州のガラス瓶と容器市場は、包装業界の重要なセグメントです。持続可能性の動向、高級包装に対する消費者の需要、プラスチック廃棄物削減をターゲットとした規制などがその原動力となっています。欧州はガラス製造業が発達しており、ドイツ、イタリア、フランス、スペインがガラス生産と消費の中心地となっています。

主なハイライト

- 欧州のガラス容器市場は数十億ユーロ規模で、近年着実な成長を遂げています。飲食品、医薬品、化粧品など重要なセクターの需要がこの成長を牽引しています。市場は緩やかな成長が見込まれ、特にアルコール飲料、化粧品、グルメ食品などのプレミアムパッケージング分野の増加が顕著です。ワイン、ビール、蒸留酒などのアルコール飲料が市場の大部分を占め、ジュースや炭酸飲料など他の飲料も大きく貢献しています。

- ガラスはリサイクル可能なため、持続可能性の高い包装材料です。欧州では強固なリサイクル政策が実施されており、その結果ガラス包装のリサイクル率は高く、多くの国で70%を超えることが多いです。プラスチック廃棄物への懸念が高まる中、ガラスは環境に優しい代替品としてますます注目されています。

- 欧州の消費者はガラス包装を好み、その理由として高級品質、製品の完全性保持、リサイクル性を挙げています。ガラス包装は高級品やオーガニック製品によく使われます。EUサーキュラー・エコノミー行動計画のようなEUのイニシアティブは、リサイクル率の向上と廃棄物の削減を推進しています。ガラスはリサイクル可能な材料としてこれらの目標に合致しており、包装分野での需要をさらに高めています。

- 最大の分野は飲料で、アルコール飲料(ワイン、ビール、スピリッツ)とソフトドリンクが中心です。風味と品質を保つため、ガラス瓶や瓶が好まれます。ガラスは不活性で無菌であるため、製薬業界では医薬品、特に液体医薬品、ワクチン、シロップの包装に広くガラス容器が使用されています。化粧品業界では、その高級感と気密性の高さから、スキンケア製品、香水、化粧品の高級包装にガラスが使用されています。

- この地域はガラス瓶と容器製品の貿易にも参加しています。国際貿易センターによると、欧州諸国のガラス容器生産能力は大きく異なっています。ドイツが年間549万3,250トンでトップ、次いでイタリアが489万7,205トン、フランスが458万750トンとなっています。

- 欧州の包装業界は、従来のガラス製包装に代わるものが支持されるようになり、大きな変化を経験しています。持続可能性への懸念、費用対効果、包装材料の技術進歩がこの動向を後押ししています。その結果、既存のガラス包装市場は新たな課題に直面し、バイオプラスチック、軟包装、先進ポリマー素材などの革新的な代替品との競合にさらされています。この変化は消費者の嗜好を変化させ、ガラス包装メーカーは進化する市場環境の中で市場シェアを維持するために戦略を適応させる必要に迫られています。

欧州のガラス瓶と容器の市場動向

飲料産業が大きな市場シェアを占める

- 欧州にはフランス、イタリア、スペイン、ドイツなど世界有数のワイン生産国があり、ワインの包装はガラス瓶が主流です。ガラスは、ワインの風味、アロマ、品質を維持するのに最適な素材であると広く認識されており、高級品と密接な関係があります。ワイン産業は引き続き欧州におけるガラス容器需要の主要な牽引役であり、一部の国ではワイン包装の80%以上をガラス容器が占めています。

- フランスは欧州諸国の中でも有数のワイン消費国であり続け、2023年の消費量は約2,440万ヘクトリットルに達します。この高水準の消費は、フランスに深く根付いたワイン文化と、日常生活や社交の場におけるワインの重要性を反映しています。国際ブドウ・ワイン機構によると、英国の消費量は約1,280万ヘクトリットルです。英国のワイン消費量は、消費者の嗜好の変化やワインに対する評価の高まりに影響され、着実に伸びています。

- このような欧州全体のワイン消費動向は、包装材料としてのガラス瓶の需要が続いていることを示しています。ガラス瓶は風味を保持し、保存期間を延ばし、消費者に高級な美的魅力を提供できるため、ワインの包装オプションとして依然として好まれています。これらの重要な欧州市場におけるワイン消費の持続的な伸びは、飲料業界における高品質のガラス製パッケージング・ソリューションに対する需要の並行的な増加を示唆しています。

- ガラス容器飲料市場は、クラフトビール、オーガニックジュース、高級蒸留酒など、プレミアムでニッチな分野で強さを見せています。高品質で環境に優しいパッケージング・ソリューションへの需要が、これらのカテゴリーにおけるガラス容器の利用拡大を牽引しています。クラフトビールと少量生産飲料はガラス包装市場に大きく貢献しています。多くのクラフトビールメーカーや小規模飲料メーカーは、品質、伝統、環境への責任を顧客に伝えるためにガラス瓶を選んでいます。

- プラスチック缶やアルミ缶が優勢であるにもかかわらず、ガラス瓶は、プレミアム・ソーダ、オーガニック飲料、クラフト清涼飲料など、清涼飲料市場のニッチ分野で残っています。ナチュラル、オーガニック、健康志向の飲料ブランドの人気が高まっていることも、持続可能な包装オプションとしてガラスを使用する一因となっています。フレッシュジュース、特にコールドプレスジュースやオーガニックジュースは、製品の品質と味を保つことができるため、頻繁にガラス包装されています。

- 欧州では、プラスチック汚染に対する消費者の意識の高まりと、使い捨てプラスチックに対する規制強化により、環境に優しい包装を好む傾向が強まっています。リサイクル性が高く、品質を損なうことなく無期限に再利用可能なガラスは、飲料包装において環境意識の高い消費者にアピールしています。

- この持続可能な選択肢へのシフトは、メーカーや小売業者が飲料を含む様々な製品にガラス包装を採用することに影響を与えています。ガラスのリサイクル性と再利用性は循環型経済の原則に合致しており、欧州市場におけるガラスの魅力をさらに高めています。さらに、製品の品質を保ち、賞味期限を延ばすというガラス包装の特性も、この地域の消費者や生産者の間で人気が高まっている要因となっています。

大きな市場シェアを占めるドイツ

- ドイツは欧州におけるガラス容器の重要な市場です。堅調な産業部門、パッケージ商品の高い消費量、持続可能性の重視がこの市場を支えています。ドイツでは主に飲食品、化粧品、製薬産業がガラス容器の需要を牽引しています。

- ノンアルコール飲料の分野、特にプレミアム飲料やオーガニック飲料の分野では、ジュースや健康飲料のような製品にガラス容器が採用されています。ドイツはビールの伝統が強く、様々な飲料分野でガラス製容器が好まれ、安全で不活性な包装材を好む消費者が多いことが、同国の飲料産業におけるガラス容器の旺盛な需要につながっています。

- Statistisches Bundesamtによると、ドイツのアルコール飲料に対する消費者支出は2021年から2023年にかけて着実に増加しています。2021年には293億米ドルに達し、2022年には295億米ドルに微増しました。2023年には、この数字は307億米ドルに増加し、過去3年間におけるアルコール飲料への支出の一貫した増加傾向を反映しています。

- ドイツはまた、世界でも有数のガラスリサイクル率を維持しており、ガラス瓶の90%以上がリサイクルされています。環境意識が高まるにつれ、ドイツの消費者や企業は持続可能な包装材料としてガラスを選ぶようになっています。ガラスは品質を損なうことなく100%リサイクルできるため、環境に優しい素材として広く認知されています。このため、特にドイツの包装廃棄物に関する法律や、リサイクル可能な材料を促進する拡大生産者責任(EPR)規制を考慮して、ガラス容器への嗜好が高まっています。

- ドイツはガラス瓶と容器製品の輸出に参加しています。国際貿易センターによると、ドイツの輸出量は2021年の109万4,706トンから2022年には149万4,488トンと36.4%増と大幅に増加しました。この増加は、ドイツ製品に対する国際的な需要の高まりを示唆しています。この増加の要因としては、パンデミック後の景気回復、世界貿易の増加、あるいは自動車、化学、機械、消費財などの分野における特定の産業の好景気などが考えられます。

- 2023年の輸出量は、2022年のピークから19.4%減の120万5,642トンと、わずかに減少しました。この減少は、サプライチェーンの混乱、世界経済の課題、または重要市場における需要パターンの変化に起因すると考えられます。商品価格の変動、国際需要のシフト、ウクライナ紛争を含む地政学的緊張などの要因が、2023年のドイツの輸出実績に影響を与えた可能性があります。

欧州のガラス瓶と容器産業の概要

欧州のガラス瓶と容器市場は断片化されており、多数の企業が市場シェアを争っています。この競合環境は技術革新を促進し、多様な顧客ニーズに対応するための差別化を各社に促しています。市場には、多国籍大企業と地域の中小メーカーがあり、それぞれが業界のダイナミズムに貢献しています。O-I Glass, Inc.、SAVERGLASS Group、Berlin Packaging、Verallia Group、Gerresheimer AGなどの主要企業は、幅広い製品ポートフォリオ、技術的進歩、戦略的パートナーシップを通じて確固たる地位を築いています。

これらの企業やその他の市場参入企業は、飲食品、医薬品、化粧品、パーソナルケアなど様々な分野に対応しています。持続可能性と環境に優しいパッケージングソリューションへの継続的な注目は、これらの主要企業の市場戦略と製品開発にも大きな影響を与えています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- ガラス瓶と容器の輸出入データ

- PESTEL分析- 欧州のガラス瓶と容器産業

- 容器包装用ガラスの業界標準と規制

- 包装用ガラスの原材料分析と材料検討

- 容器包装用ガラスの持続可能性動向

- 欧州のガラス瓶と容器炉と立地

第5章 市場力学

- 市場促進要因

- 環境に優しい製品に対する需要の高まり

- 飲食品市場の需要急増

- 市場の課題

- ガラス代替品の採用増加による伝統市場の課題

- 世界のガラス瓶と容器市場における欧州の市況分析

- 貿易シナリオ-欧州のガラス瓶と容器産業における輸出入パラダイムの歴史と現状分析

第6章 市場セグメンテーション

- エンドユーザー業界別

- アルコール用

- ビールとサイダー

- ワイン・スピリッツ

- ノンアルコール

- 炭酸飲料

- 乳飲料

- 水

- その他のノンアルコール飲料

- 食品

- 化粧品

- 医薬品

- その他エンドユーザー業界別

- アルコール用

- 国別

- ドイツ

- イタリア

- フランス

- ポーランド

- 英国

- スペイン

- ロシア

第7章 競合情勢

- 企業プロファイル

- Verallia Group

- BA GLASS GROUP

- O-I Glass, Inc.

- Vidrala, S.A.

- VERESCENCE FRANCE

- Gerresheimer AG

- SAVERGLASS Group

- ALGLASS SA

- Quadpack Industries SA

- Berlin Packaging

- Wiegand-Glas Holding GmbH

- Ardagh Group S.A.

- HEINZ-GLAS GmbH & Co.

- Zignago Vetro S.p.A.

- Beatson Clark

第8章 補足:欧州の主要容器ガラス工場への主要加熱炉サプライヤーの分析

第9章 市場の将来展望

The Europe Glass Bottles And Containers Market size in terms of shipment volume is expected to grow from 40.13 million tonnes in 2025 to 44.26 million tonnes by 2030, at a CAGR of 1.98% during the forecast period (2025-2030).

The European container glass market is a crucial segment of the packaging industry. It is driven by sustainability trends, consumer demand for premium packaging, and regulations targeting plastic waste reduction. Europe boasts a well-developed glass manufacturing sector, with Germany, Italy, France, and Spain serving as central glass production and consumption hubs.

Key Highlights

- The European glass container market, valued in billions of euros, has experienced steady growth in recent years. Demand across critical sectors, including food and beverages, pharmaceuticals, and cosmetics, drives this growth. The market is expected to grow moderately, with a notable increase in the premium packaging segment, particularly for alcoholic beverages, cosmetics, and gourmet food products. Alcoholic beverages, such as wine, beer, and spirits, constitute a large portion of the market, while other beverages, like juices and carbonated drinks, also contribute significantly.

- Due to its recyclability, glass is a highly sustainable packaging material. Europe has implemented robust recycling policies, resulting in high glass packaging recycling rates, often surpassing 70% in numerous countries. As concerns about plastic waste grow, glass is increasingly considered an environmentally friendly alternative.

- European consumers prefer glass packaging, attributing it to premium quality, product integrity preservation, and recyclability. Glass packaging is frequently associated with high-end and organic products. European Union initiatives, such as the EU Circular Economy Action Plan, drive higher recycling rates and waste reduction. Glass aligns well with these objectives as a recyclable material, further increasing its demand in the packaging sector.

- The largest segment is beverages, focusing on alcoholic drinks (wine, beer, spirits) and soft drinks. Glass bottles and jars are preferred to preserve flavour and quality. Due to glass's inert nature and sterility, the pharmaceutical industry widely uses glass containers for packaging medicines, especially liquid medications, vaccines, and syrups. In cosmetics, glass is used for premium packaging of skincare products, perfumes, and cosmetics, owing to its high-end appeal and ability to provide an airtight seal.

- The region also participates in the trade of container glass products. According to the International Trade Center, European countries' glass container production capacity varies significantly. Germany leads with 5,493,250 tons per year, followed by Italy at 4,897,205 tons and France at 4,580,750 tons.

- The European packaging industry is experiencing a significant shift as alternatives to traditional glass packaging gain traction. Sustainability concerns, cost-effectiveness, and technological advancements in packaging materials drive this trend. As a result, established glass packaging markets face new challenges and competition from innovative alternatives like bioplastics, flexible packaging, and advanced polymer materials. This shift reshapes consumer preferences and forces glass packaging manufacturers to adapt their strategies to maintain market share in an evolving landscape.

Europe Glass Bottles And Containers Market Trends

Beverage Industry to Hold a Significant Market Share

- Europe hosts several of the world's leading wine-producing nations, including France, Italy, Spain, and Germany, where glass bottles remain the dominant packaging choice for wine. Glass is widely regarded as the optimal material for maintaining wine's flavour, aroma, and quality, and it is closely associated with premium products. The wine industry continues to be a primary driver of glass container demand in Europe, with glass packaging accounting for over 80% of wine packaging in certain countries.

- France remained one of the leading wine consumers among European countries, with consumption reaching approximately 24.4 million hectoliters in 2023. This high level of consumption reflects France's deep-rooted wine culture and its significance in daily life and social gatherings. According to the International Organisation of Vine and Wine, the United Kingdom consumed about 12.8 million hectoliters. The UK's wine consumption has been steadily growing, influenced by changing consumer preferences and an increasing appreciation for wine.

- This trend in wine consumption across Europe indicates continued demand for glass bottles as packaging materials. Glass bottles remain the preferred packaging option for wine due to their ability to preserve flavour, extend shelf life, and provide a premium aesthetic appeal to consumers. The sustained growth in wine consumption in these critical European markets suggests a parallel increase in the demand for high-quality glass packaging solutions in the beverage industry.

- The glass container beverage market shows strength in premium and niche sectors, such as craft beer, organic juices, and high-end spirits. The demand for high-quality, environmentally friendly packaging solutions drives growth in glass container usage for these categories. Craft beer and small-batch beverages contribute significantly to the market for glass packaging. Many craft brewers and small beverage producers choose glass bottles to communicate quality, tradition, and environmental responsibility to their customers.

- Despite the dominance of plastic and aluminium cans, glass bottles remain in niche segments of the soft drink market, including premium sodas, organic beverages, and craft soft drinks. The increasing popularity of natural, organic, and health-focused beverage brands has contributed to using glass as a sustainable packaging option. Fresh juices, particularly cold-pressed and organic varieties, are frequently packaged in glass due to their ability to preserve product quality and taste.

- Europe shows an increasing preference for environmentally friendly packaging, driven by growing consumer awareness of plastic pollution and stricter regulations on single-use plastics. Being highly recyclable and indefinitely reusable without quality loss, glass appeals to environmentally conscious consumers in beverage packaging.

- This shift towards sustainable options influences manufacturers and retailers to adopt glass packaging for various products, including beverages. Glass's recyclability and reusability align with circular economy principles, further enhancing its appeal in the European market. Additionally, glass packaging's ability to preserve product quality and extend shelf life contributes to its growing popularity among consumers and producers in the region.

Germany to Hold a Significant Market Share

- Germany represents a significant market for glass containers in Europe. Its robust industrial sector, high consumption of packaged goods, and increasing emphasis on sustainability support this market. The food and beverage, cosmetic, and pharmaceutical industries primarily drive the demand for glass containers in Germany.

- The non-alcoholic beverage segment, especially in premium and organic categories, also embraces glass packaging for products like juices and health drinks. Germany's strong beer heritage, preference for glass in various beverage sectors, and consumer inclination towards safe, inert packaging materials collectively contribute to the robust demand for glass containers in the country's beverage industry.

- According to Statistisches Bundesamt, consumer spending on alcoholic beverages in Germany has steadily increased from 2021 to 2023. In 2021, spending reached USD 29.3 billion, followed by a slight rise to USD 29.5 billion in 2022. By 2023, this figure grew to USD 30.7 billion, reflecting a consistent upward trend in the country's expenditure on alcoholic drinks over the past three years.

- Germany also maintains one of the world's highest glass recycling rates, with over 90% of glass bottles being recycled. As environmental awareness grows, German consumers and companies increasingly choose glass as a sustainable packaging material. Glass is widely recognized as eco-friendly due to its 100% recyclability without quality loss. This has led to a rising preference for glass containers, particularly in light of German packaging waste laws and Extended Producer Responsibility (EPR) regulations promoting recyclable materials.

- The country participates in the export of container glass products. According to the International Trade Center, Germany's export volume increased significantly from 1,094,706 tons in 2021 to 1,494,488 tons in 2022, a 36.4% rise. This increase suggests heightened international demand for German products. Factors contributing to this growth may include post-pandemic economic recovery, increased global trade, or specific industry booms in sectors like automotive, chemicals, machinery, or consumer goods.

- In 2023, export volume decreased slightly to 1,205,642 tons, a 19.4% reduction from the 2022 peak. This decline may be attributed to supply chain disruptions, global economic challenges, or changing demand patterns in critical markets. Factors such as commodity price fluctuations, shifts in international demand, or geopolitical tensions, including the Ukraine conflict, could have influenced Germany's export performance in 2023.

Europe Glass Bottles And Containers Industry Overview

The European container glass market is fragmented, with numerous players competing for market share. This competitive environment fosters innovation and drives companies to differentiate their offerings to meet diverse customer needs. The market includes large multinational corporations and smaller regional manufacturers, each contributing to the industry's dynamism. Key players in this market, such as O-I Glass, Inc., SAVERGLASS Group, Berlin Packaging, Verallia Group, and Gerresheimer AG, have established strong positions through their extensive product portfolios, technological advancements, and strategic partnerships.

These companies and other market participants cater to various sectors, including food and beverage, pharmaceuticals, cosmetics, and personal care. The ongoing focus on sustainability and eco-friendly packaging solutions has also significantly influenced market strategies and product development among these key players.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Export-Import Data of Container Glass

- 4.3 PESTEL ANALYSIS - Container Glass Industry in Europe

- 4.4 Industry Standard and Regulation for Container Glass Use for Packaging

- 4.5 Raw Material Analysis and Material Consideration for Packaging

- 4.6 Sustainability Trends for Glass Packaging

- 4.7 Container Glass Furnace and Location in Europe

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Eco-friendly Products

- 5.1.2 Surging Demand from the Food and Beverage Market

- 5.2 Market Challenge

- 5.2.1 Increasing Adoption of Glass Alternatives Challenges Traditional Markets

- 5.3 Analysis of the Current Positioning of Europe in the Global Container Glass Market

- 5.4 Trade Scenerio - Analysis of the Historical and Current Export Import Paradigm for Container Glass Industry in Europe

6 MARKET SEGMENTATION

- 6.1 By End-user Vertical

- 6.1.1 Alcoholic (Qualitative Analysis For Segment Analysis)

- 6.1.1.1 Beer and Cider

- 6.1.1.2 Wine and Spirits

- 6.1.2 Non-alcoholic (Qualitative Analysis For Segment Analysis)

- 6.1.2.1 Carbonated Soft Drinks

- 6.1.2.2 Dairy-based

- 6.1.2.3 Water

- 6.1.2.4 Other Non-alcoholic Beverages

- 6.1.3 Food

- 6.1.4 Cosmetics

- 6.1.5 Pharmaceutical

- 6.1.6 Other End-user Verticals

- 6.1.1 Alcoholic (Qualitative Analysis For Segment Analysis)

- 6.2 By Country

- 6.2.1 Germany

- 6.2.2 Italy

- 6.2.3 France

- 6.2.4 Poland

- 6.2.5 United Kingdom

- 6.2.6 Spain

- 6.2.7 Russia

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Verallia Group

- 7.1.2 BA GLASS GROUP

- 7.1.3 O-I Glass, Inc.

- 7.1.4 Vidrala, S.A.

- 7.1.5 VERESCENCE FRANCE

- 7.1.6 Gerresheimer AG

- 7.1.7 SAVERGLASS Group

- 7.1.8 ALGLASS SA

- 7.1.9 Quadpack Industries SA

- 7.1.10 Berlin Packaging

- 7.1.11 Wiegand-Glas Holding GmbH

- 7.1.12 Ardagh Group S.A.

- 7.1.13 HEINZ-GLAS GmbH & Co.

- 7.1.14 Zignago Vetro S.p.A.

- 7.1.15 Beatson Clark