|

市場調査レポート

商品コード

1550346

オーストラリアとニュージーランドのプラスチックキャップおよびクロージャ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Australia And New Zealand Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オーストラリアとニュージーランドのプラスチックキャップおよびクロージャ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

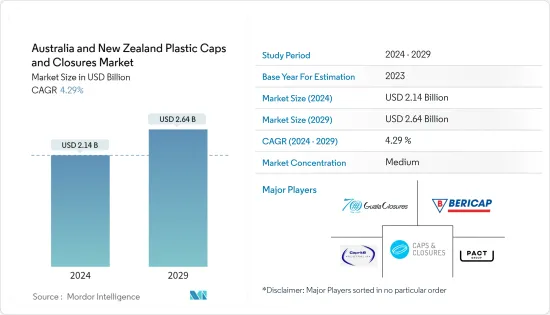

オーストラリアとニュージーランドのプラスチックキャップおよびクロージャ市場規模は、2024年に21億4,000万米ドルと推定・予測され、2029年には26億4,000万米ドルに達し、予測期間(2024-2029年)のCAGRは4.29%で成長すると予測されます。

出荷数では、2024年の127億8,000万個から2029年には152億1,000万個へと、予測期間(2024~2029年)のCAGRは3.54%で成長すると予測されます。

主なハイライト

- オーストラリアとニュージーランドでは、食品、飲料、パーソナルケア、化粧品、医薬品、工業などの分野が牽引して、プラスチックキャップおよびクロージャの需要が急増しています。オーストラリアでは、飲食品(F&B)製造部門が拡張性と競合を強化し、国のサプライチェーンの強靭性を支えています。特に、オーストラリア最大の食品加工産業は、製造業全体の3分の1を占めており、多様なプラスチック製クロージャーの必要性をさらに高めています。

- 同時に、ニュージーランドの飲料部門は、進化する消費者の嗜好と消費の高まりを反映し、プラスチックキャップの需要を促進しています。ニュージーランド飲料評議会(NZBC)のデータによると、キウイの家庭はソフトドリンクやジュースに年間7億米ドル近くを費やしており、その内訳はソフトドリンクが約2億8,400万米ドル、フルーツ・野菜ジュースが1億4,300万米ドル、エナジードリンクが2,000万米ドルとなっています。

- Bericap Holding GmbH、Guala Closures SPA、Pact Group Holdings Ltdといった主要企業が最前線に立ち、食品、飲食品、化粧品、パーソナルケアなど様々な用途に合わせた軽量クロージャーの製造に注力しています。これらのメーカーが提供する製品は、ディスペンサー用フリップトップ、ポンプ、ファインミストスプレーから、様々な業界に対応するタンパーエビデントキャップまで多岐にわたる。さらに、これらのメーカーはますますポートフォリオを多様化し、特殊キャップや特注キャップを導入しており、オーストラリアとニュージーランドの両市場をさらに促進しています。

- 市場の成長軌道とは裏腹に、オーストラリアとニュージーランドではプラスチック製キャップとクロージャーの環境への影響が懸念されています。ボトルやキャップを含むプラスチック廃棄物を埋立地に送るという一般的な慣行は、しばしば焼却につながります。このプロセスは、貴重なスペースを占有するだけでなく、有害な汚染物質を放出し、大気の質を著しく損なうため、市場の継続的拡大にとって差し迫った課題となっています。

オーストラリアとニュージーランドのプラスチックキャップおよびクロージャ市場の動向

ポリエチレン(PE)セグメントが最大の市場シェアを占めると推定される

- オーストラリアとニュージーランドでは、プラスチックキャップおよびクロージャのメーカーは主にPPとPEを主原料としています。費用対効果の高さで知られるこれらの素材は、産業界全体でよく使われる選択肢となっています。特筆すべきは、PP、HDPE、LDPEなどさまざまなプラスチック・ボトルに適合する熱誘導キャップ・ライナーで、漏れを防ぐだけでなく、耐タンパー性も備えています。このような利点を考慮すると、キャップおよびクロージャ市場は近い将来大きく成長するものと思われます。

- オーストラリアとニュージーランドの消費者は、マイペースなライフスタイルで知られ、様々な用途で軽量で使い勝手の良いクロージャーを求めるようになっています。この需要は、コンパクトさと実用性を重視したパッケージングへのシフトにつながっています。この動向に対応し、カスタムキャップやクロージャーのメーカーは、主にPE製で、軽量なだけでなく、開けやすく、扱いやすく、分配しやすいデザインを導入しています。このシフトは市場成長の重要な促進要因です。

- Bericap Holding GmbHやGuala Closures SpAなど、オーストラリアとニュージーランドのキャップおよびクロージャ市場の主要企業は技術革新の最前線にいます。彼らはPEから漏れ防止クロージャーを製造し、食品、飲料、工業用途に対応しています。これらのキャップは漏れを確実に防ぐだけでなく、ユーザーの利便性を向上させ、市場成長を促進する極めて重要な要因となっています。

- オーストラリアとニュージーランドのパーソナルケアと化粧品セクターにおけるPEキャップ、クロージャー、蓋の需要の急増は、自然派スキンケア製品への消費者の嗜好の高まりと業界の技術革新の進展に直接関連しています。国際貿易センター(ITC)のデータによると、2023年のオーストラリアの美容・メークアップ製品の輸入額は11億4,372万米ドルで、前年比17.31%増でした。同様に、ニュージーランドは1.16%増の2億4,849万米ドルとなった。

飲料セグメントが市場を独占する見込み

- キャップおよびクロージャ市場は需要の急増を目の当たりにしているが、これは主にパッケージ飲料の人気の高まりによるものです。消費者の健康意識が高まり、より健康的な飲料が好まれるようになったことが主な要因です。その結果、健康志向の代表格であるヘルシーでナチュラルなエナジードリンクが脚光を浴び、プラスチックキャップおよびクロージャー部門をさらに押し上げています。

- オーストラリアでは、炭酸清涼飲料、エナジードリンク、ジュースの需要が高まっています。特に、オーストラリア飲料評議会(Australian Beverage Council)のデータでは、9~13歳のジュースの消費量が顕著に増加しており、その割合は12%から33%に急増しています。

- 逆にニュージーランドでは、甘い飲料が好まれる傾向が強く、キャップやクロージャーの需要を大きく押し上げています。ニュージーランド飲料評議会のデータによると、炭酸飲料は同国の全飲料消費量の7.2%と控えめです。糖分が多いにもかかわらず、砂糖入り炭酸飲料の市場は増加傾向にあります。

- 国際貿易センター(ITC)の洞察によると、オーストラリアとニュージーランドはともにノンアルコール飲料の主要輸入国です。2023年には、オーストラリアのノンアルコール飲料輸入額は3億9,961万米ドル、ニュージーランドは1億4,504万米ドルでした。この大きな輸入量を考えると、キャップとクロージャーを含む飲料用パッケージの需要は、この地域で成長する準備が整っています。

オーストラリアとニュージーランドのプラスチックキャップおよびクロージャ産業の概要

オーストラリアとニュージーランドのプラスチックキャップおよびクロージャ市場は適度に統合されており、以下のような国内プレーヤーがあります。 Caprice Australia Pty Ltd and Caps and Closures Pty Ltd, and International players including Bericap Holding GmbH, Pact Group Holdings Ltd, and Guala Closures SpA operating in the market. To solidify their footprint in the market, the players focus on new product development, partnerships, participation in trade expos, mergers and acquisitions, and collaborations.

- 2023年7月オーストラリアのCaps and Closures Pty Ltdは、シドニーの国際コンベンションセンターで開催されたAustralian Waste &Recycling Expo(AWRE)に参加しました。同社は同エキスポで、飲食品業界向けの持続可能なキャップとクロージャーのソリューションを展示しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 飲食品分野の成長

- 革新的なキャップとクロージャーの需要増加

- 市場の課題

- プラスチック廃棄物に関する環境問題の高まり

第6章 業界の規制と政策と基準

第7章 市場セグメンテーション

- 樹脂別

- ポリエチレン(PE)

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- その他のプラスチック材料(ポリスチレン、PVC、ポリカーボネートなど)

- 製品タイプ別

- ネジ式

- ディスペンサー

- ネジなし

- チャイルドレジスタント

- エンドユーザー産業別

- 食品

- 飲料

- ボトル入り飲料水

- 炭酸飲料

- アルコール飲料

- ジュースとエナジードリンク

- その他の飲料

- パーソナルケアと化粧品

- 家庭用化学品

- その他のエンドユーザー産業

- 国別

- オーストラリア

- ニュージーランド

第8章 競合情勢

- 企業プロファイル

- Amcor Group GmbH

- Bericap Holding GmbH

- Pact Group Holdings Limited

- Caprite Australia Pty Ltd

- Guala Closures SPA

- Primo Plastics

- Caps and Closures Pty Ltd

- Forward Plastics Ltd

- Flexicon Plastics

第9章 リサイクルと持続可能性の展望

第10章 将来の展望

The Australia And New Zealand Plastic Caps And Closures Market size is estimated at USD 2.14 billion in 2024, and is expected to reach USD 2.64 billion by 2029, growing at a CAGR of 4.29% during the forecast period (2024-2029). In terms of shipment volume, the market is expected to grow from 12.78 billion units in 2024 to 15.21 billion units by 2029, at a CAGR of 3.54% during the forecast period (2024-2029).

Key Highlights

- Australia and New Zealand are witnessing a surge in demand for plastic caps and closures, driven by sectors like food, beverage, personal care, cosmetics, pharmaceuticals, and industry. In Australia, the food and beverage (F&B) manufacturing sector bolsters scalability and competitiveness and underpins the nation's supply chain resilience. Notably, Australia's food processing industry, the largest in the country, accounts for a significant one-third of all manufacturing activities, further fueling the need for diverse plastic closures.

- Concurrently, New Zealand's beverage sector is propelling the demand for plastic caps, reflecting the nation's evolving consumer preferences and heightened consumption. Data from the New Zealand Beverage Council (NZBC) reveals that Kiwi households collectively spend nearly USD 700 million annually on soft drinks and juices, with a breakdown of around USD 284 million on soft drinks, USD 143 million on fruit and vegetable juices, and USD 20 million on energy drinks.

- Key players like Bericap Holding GmbH, Guala Closures SPA, and Pact Group Holdings Ltd are at the forefront, focusing on crafting lightweight closures tailored for various applications, be it in food, beverages, cosmetics, or personal care. Their product offerings span from dispensing flip-tops, pumps, and fine mist sprays to tamper-evident caps catering to a spectrum of industries. Moreover, these manufacturers are increasingly diversifying their portfolio, introducing specialty and bespoke caps, further propelling the market in both Australia and New Zealand.

- Despite the market's growth trajectory, there's a looming concern over the environmental impact of plastic caps and closures in Australia and New Zealand. The prevalent practice of sending plastic waste, including bottles and caps, to landfills often leads to incineration, a process that not only occupies valuable space but also releases harmful pollutants, significantly compromising air quality, a pressing challenge for the market's continued expansion.

Australia and New Zealand Plastic Caps and Closures Market Trends

Polyethylene (PE) Segment is Estimated to Have the Largest Market Share

- In Australia and New Zealand, manufacturers of plastic caps and closures primarily rely on PP and PE as their key raw materials. These materials, known for their cost-effectiveness, have become a go-to choice across industries. Notably, heat induction cap liners, compatible with a variety of plastic bottles such as PP, HDPE, and LDPE, not only prevent leaks but also provide tamper resistance. With these benefits in mind, the caps and closures market is set for substantial growth in the near future.

- Australian and New Zealand consumers, known for their fast-paced lifestyles, are increasingly seeking lightweight, user-friendly closures for a range of applications. This demand has led to a shift in packaging, with a focus on compactness and practicality. Responding to this trend, custom caps and closures manufacturers are introducing designs, predominantly from PE, that are not only lighter but also easier to open, handle, and dispense. This shift is a key driver of market growth.

- Key players in the Australian and New Zealand caps and closures market, such as Bericap Holding GmbH and Guala Closures SpA, are at the forefront of innovation. They are crafting leak-proof closures from PE and cater to food, beverage, and industrial applications. These closures not only ensure leak protection but also enhance user convenience, a factor pivotal in driving market growth.

- The surge in demand for PE caps, closures, and lids in the personal care and cosmetics sector in Australia and New Zealand is directly linked to the increasing consumer preference for natural skincare products and growing innovation in the industry. Data from the International Trade Centre (ITC) reveals that in 2023, imports of beauty and make-up products in Australia were valued at USD 1,143.72 million, marking a 17.31% increase from the previous year. Similarly, New Zealand saw a 1.16% rise, with imports valued at USD 248.49 million.

Beverage Segment Expected to Dominate the Market

- The caps and closures market is witnessing a surge in demand, largely driven by the increasing popularity of packaged beverages. This uptick is predominantly attributed to rising awareness of health among consumers, leading to a preference for healthier beverage options. As a result, healthy and natural energy drinks, a flagship of this health-conscious trend, are gaining prominence, further boosting the plastic caps and closures segment.

- Australia is witnessing a growing appetite for carbonated soft drinks, energy drinks, and juices, largely due to a rising demand for zero-calorie, sugar-free options available in a myriad of flavors. Notably, data from the Australian Beverage Council underscores a notable uptick in juice consumption among 9 to 13-year-olds, with rates soaring from 12% to 33%.

- Conversely, New Zealand exhibits a strong affinity for sugary drinks, a trend that significantly drives the demand for caps and closures. The New Zealand Beverage Council's data reveals that carbonated soft drinks make up a modest 7.2% of the country's total beverage consumption. Despite their high sugar content, the market for sugar-sweetened carbonated soft drinks is on the rise.

- Insights from the International Trade Centre (ITC) indicate that both Australia and New Zealand are key importers of non-alcoholic beverages. In 2023, Australia's import value for such beverages stood at USD 399.61 million, while New Zealand's was at USD 145.04 million. Given this significant import volume, the demand for beverage packaging, including caps and closures, is poised for growth in the region.

Australia and New Zealand Plastic Caps and Closures Industry Overview

The Australian and New Zealand plastic caps and closures market is moderately consolidated, with domestic players such as Caprice Australia Pty Ltd and Caps and Closures Pty Ltd, and International players including Bericap Holding GmbH, Pact Group Holdings Ltd, and Guala Closures SpA operating in the market. To solidify their footprint in the market, the players focus on new product development, partnerships, participation in trade expos, mergers and acquisitions, and collaborations.

- July 2023: Caps and Closures Pty Ltd, an Australian company, participated in the Australian Waste & Recycling Expo (AWRE), an event held at the International Convention Centre in Sydney. The company showcased sustainable caps and closure solutions for the food and beverage industries at the expo.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in the Food and Beverage Sector

- 5.1.2 Rising Demand of Innovative Caps and Closures

- 5.2 Market Challenge

- 5.2.1 Rising Environmental Concerns Regarding Plastic Waste

6 INDUSTRY REGULATION, POLICY AND STANDARDS

7 MARKET SEGMENTATION

- 7.1 By Resin

- 7.1.1 Polyethylene (PE)

- 7.1.2 Polyethylene Terephthalate (PET)

- 7.1.3 Polypropylene (PP)

- 7.1.4 Other Plastic Materials (Polystyrene, PVC, Polycarbonate, etc.)

- 7.2 By Product Type

- 7.2.1 Threaded

- 7.2.2 Dispensing

- 7.2.3 Unthreaded

- 7.2.4 Child-resistant

- 7.3 By End-user Industries

- 7.3.1 Food

- 7.3.2 Beverage

- 7.3.2.1 Bottled Water

- 7.3.2.2 Carbonated Soft Drinks

- 7.3.2.3 Alcoholic Beverages

- 7.3.2.4 Juices and Energy Drinks

- 7.3.2.5 Other Beverages

- 7.3.3 Personal Care and Cosmetics

- 7.3.4 Household Chemicals

- 7.3.5 Other End-user Industries

- 7.4 By Country

- 7.4.1 Australia

- 7.4.2 New Zealand

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Amcor Group GmbH

- 8.1.2 Bericap Holding GmbH

- 8.1.3 Pact Group Holdings Limited

- 8.1.4 Caprite Australia Pty Ltd

- 8.1.5 Guala Closures SPA

- 8.1.6 Primo Plastics

- 8.1.7 Caps and Closures Pty Ltd

- 8.1.8 Forward Plastics Ltd

- 8.1.9 Flexicon Plastics