|

市場調査レポート

商品コード

1906904

北米のプラスチックキャップおよびクロージャー市場:市場シェア分析、業界動向、統計、成長予測(2026年~2031年)North America Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のプラスチックキャップおよびクロージャー市場:市場シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

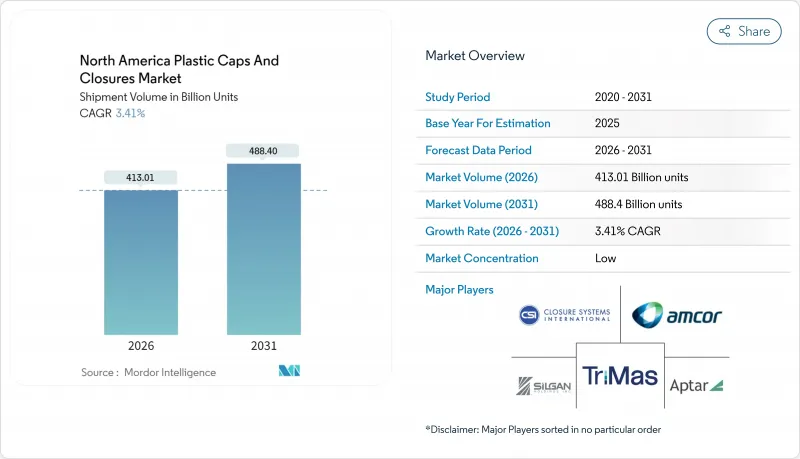

北米のプラスチックキャップおよびクロージャー市場は、2025年の3,993億9,000万個から2026年には4,130億1,000万個へ成長し、2026年から2031年にかけてCAGR 3.41%で推移し、2031年までに4,884億個に達すると予測されております。

この成長は、飲料、食品、医薬品、パーソナルケア製品における製品品質の保護と、厳格な安全性・持続可能性への期待に応える市場の役割を反映しています。機能性飲料の新製品投入、電子商取引による医薬品販売の拡大、州レベルでの再生材使用義務化が、特殊で高性能なキャップ・クロージャーへの需要を牽引し続けています。同時に、ブランドオーナーは循環型経済の目標に沿った、連結式、単一素材、チャイルドレジスタント(子供が開けにくい)ソリューションを好んでいます。バージン樹脂の価格上昇や気候変動に伴う供給混乱によるコスト圧力により、メーカーは生産の自動化と再生原料の統合を推進し、競合力の維持を図っております。業界関係者はまた、効率性向上と規模の経済確保のため、合併やAIを活用した欠陥検査システムの導入を進めております。

北米のプラスチックキャップおよびクロージャー市場の動向と洞察

ボトル入り飲料および機能性飲料の需要急増

機能性強化ウォーター、リラックスモクテル、カフェイン入りスポーツドリンクが小売チャネルへの浸透を続け、従来の水分補給カテゴリーを超えたキャップ需要を牽引しています。プレミアムポジショニングにより、最大4体積の炭酸ガスを保持しつつブランド棚差別化を実現する耐圧性・改ざん防止設計への投資が促進されています。飲料開発者はまた、敏感な栄養補助食品成分を保護し、米国食品医薬品局(FDA)のサプリメント表示基準に準拠するキャップを必要としています。さらに、メキシコにおける消費支出の増加が地域の飲料生産を支え、軽量でありながら頑丈なキャップの需要を拡大しています。高速ボトリング工程において一貫したトルクとシール性能を実現するため、メーカーが充填業者と連携する中、サプライチェーンの信頼性は依然として不可欠です。

ブランドオーナーによるテザー付き/EC対応キャップの推進

消費者直送配送の普及により、AmazonのISTA-6適合性は、パーソナルケア製品や飲料の新製品発売における必須要件となりました。そのためブランドオーナー様は、ボトルネック部に確実に固定され、漏れを軽減し、輸送用カートン内でのキャップ紛失を防ぐテザー付き仕様を優先されています。アプター社の「フューチャー・ディスクトップ」はこの好例であり、確実なロック機構と100%ポリエチレン構造を組み合わせることで、家庭でのリサイクルを簡素化しています。食料品小売業者も同様に、自動キャップ装着ラインの効率化と、キャップとボトルの不適合によるダウンタイム削減を実現するテザード設計を好みます。特許取得済みのヒンジ形状により、改ざん防止機能や消費者の利便性を損なうことなく、複数の開閉サイクルが可能となりました。

バージン樹脂に対する拡大生産者責任(EPR)費用

カリフォルニア州を含む4州では、バージン樹脂の使用量に応じて生産者負担のリサイクル料金が課され、キャップ単価を直接押し上げています。生産者は料金負担を軽減するため、再生原料やバイオベース原料への転換を進めていますが、PCRポリプロピレンの市場供給は依然として限られています。管轄区域ごとに料金体系が異なるため、複数州で操業する充填業者にとってコンプライアンス対応が複雑化しており、報告義務も新たな管理業務を生み出しています。規制対応要員を擁さない中小コンバーター企業は最大の負担に直面しており、規模の大きい企業へ資産を売却する形で業界再編が加速する可能性があります。

セグメント分析

2025年時点では、コスト効率と加工の汎用性を背景に、ポリエチレンがプラスチックキャップおよびクロージャー市場で最大の41.98%のシェアを維持しました。しかしながら、ブランドオーナーが持続可能性の公約と単一ポリマー包装ストリームを結びつけた結果、ポリエチレンテレフタレート(PET)が6.45%のCAGRで最も急速な成長を示しました。PET製キャップは、本質的なリサイクル性と成熟した再生ネットワークを活用し、飲料・パーソナルケア分野における材料循環の実現に貢献しています。結晶化制御と添加剤パッケージの革新により耐熱性が向上し、シール性能を損なうことなくホットフィルジュースの充填が可能となりました。Origin Materials社は最近、標準充填ラインに対応するポリエステル樹脂製キャップの実証に成功し、コンバーター向けの量産対応代替品が整ったことを示しています。

メーカー各社はまた、拡大生産者責任(EPR)課徴金を回避するため、使用済みPET含有率25%の目標を模索しており、食品グレード再生ペレットの需要を押し上げています。一方、ポリプロピレンは優れた耐応力割れ性により、過酷な化学薬品や医薬品用途での地位を維持しています。バイオベースポリマーはニッチ市場ながら、堆肥化義務が適用される分野で規制当局の注目を集めています。これらの変化が相まって、総所有コストとリサイクル可能性の指標を軸とした多様な材料選択肢のモザイクが形成されています。

ネジ式容器は、汎用ネック互換性により長年標準仕様として46.85%のシェアを維持(2025年時点)。しかしながら、オンライン薬局による処方薬の消費者直送増加に伴い、チャイルドレジスタントキャップ(CRC)は2031年までCAGR5.55%で全カテゴリーを凌駕。FDAの規制強化により、特定の市販栄養補助食品粉末にもCRCの採用が義務付けられ、対応可能な市場規模がさらに拡大しています。ベリー・世界の社の選択的開封設計は、継続的な研究開発の成果を示しており、二重安全機構と成人向けの使いやすさを融合させています。

個人用ケアローションや家庭用洗剤では、流量制御による無駄削減が可能なディスペンサータイプが注目を集めております。一方、乳製品など迅速な使用と経済的な金型が求められる分野では、スナップフィットや押し込み式のソリューションが依然として有用です。あらゆるタイプのキャップにおいて、真正性確認やリサイクル手順をサポートする埋め込み型QRコードは、消費者直販チャネルにおける付加価値の高い差別化要素として台頭してまいりました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ボトル入り飲料および機能性飲料の需要急増

- ブランドオーナーによる紐付き/EC対応キャップの推進

- リサイクル容易化のためPP単一素材キャップへの移行

- オンライン医薬品・栄養補助食品市場の急成長がCRC需要を牽引

- AI搭載インラインビジョンシステムにより不良率とコストを低減

- 市場抑制要因

- バージン樹脂に対する拡大生産者責任(EPR)費用

- スクリューキャップに代わるフィッティング付きスタンドアップパウチの台頭

- 米国・カナダにおける再生ポリエステル(rPET)含有率義務化がバージンポリプロピレン(PP)需要を圧迫

- 飲料ブランドによるアルミ製再封可能キャップの試験導入

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- 地政学的シナリオの影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 材料別

- ポリエチレン(PE)

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- その他の材料

- タイプ別

- ねじ込み式

- ディスペンサー

- ネジなし

- チャイルドレジスタント

- エンドユーザー産業別

- 飲料

- ボトル入り飲料水

- ソフトドリンク

- スピリッツ

- その他の飲料

- 食品

- 医薬品・ヘルスケア

- 化粧品・トイレタリー

- 家庭用化学品

- その他の産業

- 飲料

- 製造工程別

- 射出成形

- 圧縮成形

- 3Dプリント/ラピッドプロトタイピング

- その他の製造プロセス

- 国別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Silgan Holdings Inc.

- Amcor plc

- AptarGroup Inc.

- Closure Systems International Inc.

- TriMas Corporation

- Guala Closures SpA

- Tetra Pak Group

- O.Berk Company LLC

- BERICAP Holding GmbH

- Pano Cap Canada Ltd

- Erie Molded Plastics Inc.

- Crown Holdings Inc.

- Phoenix Closures Inc.

- Mold-Rite Plastics LLC

- Comar LLC

- Husky Technologies

- SACMI Imola S.C.

- Sonoco Products Company

- Plastipak Holdings Inc.

- Albea Group