|

市場調査レポート

商品コード

1689891

米国のプラスチックキャップ・クロージャ:市場シェア分析、産業動向、成長予測(2025年~2030年)United States (US) Plastic Caps and Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のプラスチックキャップ・クロージャ:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 143 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

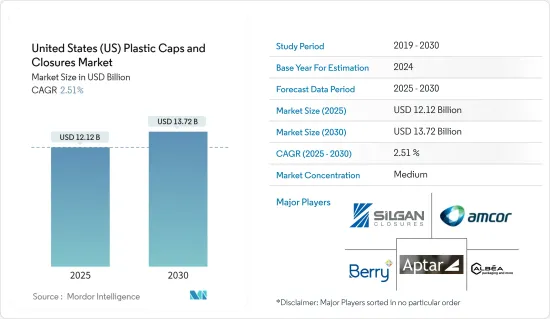

米国のプラスチックキャップ・クロージャ市場規模は2025年に121億2,000万米ドルと推定・予測され、予測期間(2025年~2030年)のCAGRは2.51%で、2030年には137億2,000万米ドルに達すると予測されます。

主なハイライト

- プラスチックキャップ・クロージャは、PPとPEを主原料として製造されます。産業界はこれらの材料に大きく依存しており、費用対効果の高い密封ソリューションを提供しています。包装食品や医薬品の需要は着実に増加しており、キャップ・クロージャ市場に影響を与えています。

- 同様に、消費者の間で健康志向が高まる中、包装飲料や医薬品の需要が急増し、キャップ・クロージャ市場を後押ししています。この上昇は、特にプラスチック製キャップ・クロージャ分野で顕著であり、健康志向の消費者に好まれるボトル入り飲料水へのアクセスが増加していることがその要因となっています。

- 特に、2023年にBeverage Marketing CorporationとInternational Bottled Water Associationは、米国で最も消費されている飲料はボトルウォーターであると報告しています。同分野の成長率は先細りしているもの、量的には主要な飲料カテゴリーであり、生産者収益と総ガロンの両方で過去最高を記録しました。具体的には、2023年のボトル入り飲料水市場は0.4%増と、2022年の1.1%増から鈍化し、2021年と2020年にそれぞれ観測された4.6%と4.1%の力強い成長率から大幅に低下しました。

- また、米国の顧客の間でボトル入り飲料水の需要が増加していることも、プラスチックキャップ・クロージャ市場を後押ししています。これらの部品は、こぼれを防ぎ、輸送を容易にし、賞味期限を延ばすために水筒を密封するために不可欠です。水の汚染や安全性への懸念に対する意識の高まりがボトル入り飲料水の需要を押し上げており、この動向は予測期間中も続くと予想されるため、市場全体でプラスチック・キャップの需要が急増する可能性があります。

- 原材料価格はプラスチックキャップ・クロージャのコストに直接影響します。プラスチック樹脂の価格が上昇すると、メーカーはこれらの材料を調達し、加工し、パッケージング製品に変える際のコスト増に直面します。原材料費の高騰は、特にメーカーがコスト増を顧客に転嫁できない場合、利益率を圧迫する可能性があります。その結果、技術革新や事業拡大への投資が抑制されたり、あるいは規模が縮小されたりして、市場の成長が抑制される可能性があります。

米国のプラスチックキャップ・クロージャ市場の動向

ポリエチレン(PE)が最も急成長する原料セグメントになる見込み

- ポリエチレン(PE)は最も耐久性のあるプラスチックのひとつで、化学薬品に強く、低コストです。石油ポリマーに由来するPEは、様々な環境上の危険に耐えることができ、通常、高密度ポリエチレン(HDPE)と低密度ポリエチレン(LDPE)に分類されます。

- HDPEとLDPEは、キャップやクロージャに使用される主な材料です。HDPEは、水、乳製品、ジュースなどのボトルに幅広く使用されており、特に水筒のキャップは、その優れた有機的特性から長年愛用されています。強度と耐久性で有名なHDPEプラスチックは、カラーマッチが可能で、一般的に白色を見かける。その適応性と耐久性により、HDPEは化粧品用ボトルの最も有力な選択肢となっています。

- ボレアリスは、HDPEキャップとクロージャの成長は、ガラス瓶の金属キャップが(PET製に)取って代わられたことと、軽食用の小型ボトルを好む消費パターンの変化に大きく起因していると指摘しています。

- 米国化学工業協会によると、2023年には米国でHDPE、LDPE、LLDPEを含む70億5,000万ポンドのポリエチレンが生産されます。射出成形技術は、特にLDPE分野で大きな影響力を持ち、医療機器、キャップ、クロージャの生産に貢献しています。

- その強度とコスト効率の高さから、米国の多くの産業ではLDPEよりもHDPEが好まれています。HDPEは剛性が高いため、衝撃に強い商品の包装に最適です。化学産業が主要な消費者として浮上し、市場の成長を後押ししています。

- 米国のプラスチックキャップ・クロージャ市場は、ポリエチレン産業の輸出イニシアティブに戦略的重点が置かれていることから、顕著な伸びを示しています。アジアはこうした輸出の重要な市場として浮上しています。米国商務省のデータによると、2023年第1四半期の米国PE輸出出荷量は前年比30%増の3兆1,964億3,700万トン(70億5,000万ポンド)でした。

飲料分野が大きな市場シェアを占める見込み

- キャップ・クロージャは、炭酸飲料と非炭酸飲料を含む飲料産業において、容器、パウチ、ボトルを密封する上で極めて重要です。異物混入から保護し、飲料の風味と味を保つ。飲料分野には、ボトル入り飲料水、フルーツジュース、レディ・トゥ・ドリンク飲料、エナジードリンクなどが含まれます。

- シングルサーブ飲料の需要の高まりと、パッケージ飲料の賞味期限を延長するホットフィルプロセスが相まって、米国のキャップ・クロージャ市場の成長を促進するものと思われます。ペットボトルは防腐剤の必要がなく、飲料の健康指数を高めるため、企業はホットフィルプロセスを好んでいます。特に、ホットフィルプラスチックボトルの利点には、製品の賞味期限延長と防腐剤フリー、軽量構成、プラスチック構成による費用対効果などがあります。

- 様々なホットフィルプロセスが飲料業界で一般的になるにつれて、ホットフィルプラスチックボトルはますます普及しています。特にレディ・トゥ・ドリンク・セグメントにおけるホットフィル・アプリケーションの台頭は、市場成長の原動力になると予想されます。

- スポーツキャップ市場は、ボトル入り飲料水やエナジードリンクの需要増加とともに拡大しています。スポーツキャップは重量があるにもかかわらず、改ざん防止機能を備えています。スポーツ用キャップは、美観、ネック径、タンパーエビデント・ソリューションが多様で、コールド、ドライ、ウェットの無菌充填要件に対応しています。Beverage Digestによると、2023年、米国の炭酸飲料(CSD)市場におけるコカ・コーラの小売数量シェアは40%を超えました。同期間中、北米はコカ・コーラ社の総収益の37%近くを占めました。2023年の同社の世界純営業収益は約460億米ドルでした。

- 飲料用クロージャに影響を与えるもう一つの有力な動向は、eコマースの台頭です。オンライン・ショッピングの利便性は、企業にとって新たな消費者にアクセスし、増大する宅配需要に応える機会となります。その結果、より多くの飲食品販売が消費者直販のeコマース・プラットフォームに移行しつつあります。

米国のプラスチックキャップ・クロージャ市場の概要

米国のプラスチックキャップ・クロージャ市場は半固定構造を維持しており、この傾向は予測期間中も続くとみられます。この市場の主な特徴には、緩やかな撤退障壁、確立されたブランドへの嗜好、活発な合併・買収活動が含まれます。この市場で注目すべき企業は、Silgan Closures(Silgan Holdings Inc.)、Amcor Ltd.、Aptargroup Inc.、Berry Global Inc.、Albea Services SASです。

2024年3月-世界のレストランブランドであるサブウェイは、2025年1月1日から米国のレストランで飲料を供給するため、ペプシコと10年間の契約を結んだと発表しました。サブウェイの長年にわたるフリトレーとのパートナーシップは2030年まで延長され、米国のスナックと飲料のポートフォリオは1つのサプライヤーのもとにまとめられ、システム全体の効率化が促進されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

- 産業バリューチェーン分析

- COVID-19パンデミックの市場への影響評価

第5章 市場力学

- 市場促進要因

- 包装食品と医薬品への需要

- 中小規模のエンドユーザー産業からの需要増加

- 市場の課題

- 原材料コストの変動

第6章 市場セグメンテーション

- 原材料別

- ポリエチレン(PE)

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- その他の素材(ポリスチレン、PVC)

- タイプ別

- ネジ式

- ディスペンサー

- ネジなし

- 小児用

- 用途別

- 食品

- 医薬品・ヘルスケア

- 飲料

- 化粧品・トイレタリー

- 家庭用化学品

- その他の用途

第7章 競合情勢

- 企業プロファイル

- Silgan Closures(Silgan Holdings Inc.)

- Amcor Ltd

- Aptargroup Inc.

- Berry Global Inc.

- Albea Services SAS

- Trimas Corporation

- Tetra Pak International SA

- Guala Closures Group(Guala Pack SPA)

- MJS Packaging

- O Berk Company LLC

- Closure Systems International Inc.

- Bericap Holding

第8章 投資分析

第9章 市場機会と今後の動向

The United States Plastic Caps and Closures Market size is estimated at USD 12.12 billion in 2025, and is expected to reach USD 13.72 billion by 2030, at a CAGR of 2.51% during the forecast period (2025-2030).

Key Highlights

- Plastic caps and closures utilize PP and PE as primary raw materials for manufacturing. Industries heavily rely on these materials, providing a cost-effective sealing solution. The demand for packaged food and pharmaceutical drugs has been steadily increasing, consequently impacting the caps and closures market, which is expected to see a rise in demand during the forecast period.

- Similarly, amid a growing trend of health-consciousness among consumers, the demand for packaged beverages and pharmaceutical drugs is surging, propelling the caps and closures market. This rise is particularly pronounced in the plastic caps and closures segment, driven by the increasing accessibility of bottled water, which is a favored choice for health-conscious consumers.

- Notably, in 2023, the Beverage Marketing Corporation and the International Bottled Water Association reported that bottled water claimed the top spot as the most consumed beverage in the United States. While the growth rate in the sector has tapered, the leading beverage category, in terms of volume, marked record highs in both producer revenues and total gallons. Specifically, in 2023, the bottled water market saw a modest increase of 0.4%, a slowdown from the 1.1% growth in 2022 and a significant decline from the robust growth rates of 4.6% and 4.1% observed in 2021 and 2020, respectively.

- Also, the rise in bottled water demand among customers in the United States is propelling the plastic caps and closures market. These components are essential for sealing water bottles to prevent spills, facilitate transportation, and enhance shelf life. The growing awareness of water contamination and safety concerns is driving up the demand for bottled water, a trend expected to continue during the forecast period, potentially spiking the demand for plastic caps across the market.

- Raw material prices directly impact the cost of plastic caps and closures. When the price of plastic resins rises, manufacturers face increased costs in sourcing, processing, and transforming these materials into packaging products. The escalation in raw material costs can strain profit margins, particularly if manufacturers cannot pass on the increased costs to customers. Consequently, this may result in reduced investments in innovation, expansion, or even downsizing, thus restraining the market's growth.

United States (US) Plastic Caps and Closures Market Trends

Polyethylene (PE) is expected to be the Fastest Growing Raw Material Segment

- Polyethylene (PE) is one of the most durable plastics available, exhibiting resistance to chemicals and boasting a low cost. Derived from petroleum polymers, PE can withstand various environmental hazards, typically categorized as high-density polyethylene (HDPE) and low-density polyethylene (LDPE).

- HDPE and LDPE represent the primary materials used in caps and closures. HDPE variants find extensive use in water, dairy, and juice bottles, favored for their excellent organoleptic properties, particularly in water bottle closures, due to their longstanding preference. Renowned for strength and durability, HDPE plastics can be color-matched and commonly found in white. Its adaptability and durability position HDPE as a top choice for cosmetic bottles.

- Borealis notes that the growth in HDPE caps and closures is largely attributed to the replacement of metal caps on glass bottles (by PET) and shifting consumption patterns favoring smaller bottles for refreshments.

- According to the American Chemistry Council, in 2023, the United States produced 7.05 billion pounds of polyethylene, including HDPE, LDPE, and LLDPE. Injection molding technology, particularly influential in the LDPE segment, contributes to the production of medical devices, caps, and closures.

- Due to its strength and cost-effectiveness, many industries in the United States prefer HDPE over LDPE. HDPE's rigidity makes it an ideal packaging choice for impact-resistant goods. The chemical industry emerges as a major consumer, propelling the market's growth.

- The US plastic caps and closures market is experiencing a notable increase, driven by a strategic emphasis on the polyethylene industry's export initiatives. Asia has emerged as a critical market for these exports. According to data from the US Commerce Department, US PE export shipments in the first quarter of 2023 increased by 30% compared to the previous year, totaling 3,196,437 million metric tons (mt) or 7.05 billion pounds.

The Beverage Segment is expected to Hold Major Market Share

- Caps and closures are crucial in sealing containers, pouches, and bottles in the beverage industry, encompassing carbonated and non-carbonated drinks. They safeguard against foreign particles and preserve the flavor and taste of beverages. The beverage segment encompasses bottled water, fruit juices, ready-to-drink beverages, and energy drinks.

- The escalating demand for single-serve beverages, coupled with the hot fill process that extends the shelf life of packaged drinks, is set to propel growth in the US caps and closures market. Companies favor plastic bottles for hot fill processes as they eliminate the need for preservatives, enhancing the drink's health quotient. Notably, the advantages of hot-fill plastic bottles include extended product shelf life and preservative-free content, their lightweight composition, and their cost-effectiveness due to their plastic composition.

- Hot-fill plastic bottles are increasingly prevalent as various hot-fill processes become commonplace in the beverage industry. The rising prominence of hot-fill applications, particularly in the ready-to-drink segment, is anticipated to drive market growth.

- The market for sports caps is expanding alongside the increasing demand for bottled water and energy drinks. Despite their weight, sports closures offer tamper-evident features. Diverse sports closure designs vary in aesthetics, neck diameters, and tamper-evident solutions catering to cold, dry, or wet aseptic filling requirements. According to Beverage Digest, in 2023, Coca-Cola's retail volume share of the US carbonated soft drink (CSD) market exceeded 40%. North America accounted for nearly 37% of the Coca-Cola Company's total revenue during the same period. The company's global net operating revenue in 2023 was approximately USD 46 billion.

- Another influential trend impacting beverage closures is the rise of e-commerce. The convenience of online shopping presents an opportunity for companies to access new consumers and cater to the growing demand for at-home delivery. Consequently, more food and beverage sales are transitioning to direct-to-consumer e-commerce platforms.

United States (US) Plastic Caps and Closures Market Overview

The plastic caps and closures market maintains a semi-consolidated structure in the United States, a trend expected to continue during the forecast period. Key characteristics of this market include moderate exit barriers, a preference for established brands, and significant merger and acquisition activities. Noteworthy players in this market landscape are Silgan Closures (Silgan Holdings Inc.), Amcor Ltd, Aptargroup Inc., Berry Global Inc., and Albea Services SAS.

In March 2024 - Subway, a global restaurant brand, announced a 10-year agreement with PepsiCo to supply beverages in US restaurants beginning January 1, 2025. Subway's longstanding partnership with Frito-Lay will extend through 2030, bringing the brand's US snack and beverage portfolio together under one supplier and driving more efficiency across the system.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of the COVID-19 Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Packaged Food and Pharmaceutical Drugs

- 5.1.2 Increasing Demand from Small and Medium-Scale End-user Industries

- 5.2 Market Challenges

- 5.2.1 Fluctuation in the Cost of Raw Materials

6 MARKET SEGMENTATION

- 6.1 By Raw Material

- 6.1.1 Polyethylene (PE)

- 6.1.2 Polyethylene Terephthalate (PET)

- 6.1.3 Polypropylene (PP)

- 6.1.4 Other Materials (Polystyrene and PVC)

- 6.2 By Type

- 6.2.1 Threaded

- 6.2.2 Dispensing

- 6.2.3 Unthreaded

- 6.2.4 Child-resistant

- 6.3 By Application

- 6.3.1 Food

- 6.3.2 Pharmaceutical and Healthcare

- 6.3.3 Beverage

- 6.3.4 Cosmetics and Toiletries

- 6.3.5 Household Chemicals

- 6.3.6 Other Applications

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Silgan Closures (Silgan Holdings Inc.)

- 7.1.2 Amcor Ltd

- 7.1.3 Aptargroup Inc.

- 7.1.4 Berry Global Inc.

- 7.1.5 Albea Services SAS

- 7.1.6 Trimas Corporation

- 7.1.7 Tetra Pak International SA

- 7.1.8 Guala Closures Group (Guala Pack SPA)

- 7.1.9 MJS Packaging

- 7.1.10 O Berk Company LLC

- 7.1.11 Closure Systems International Inc.

- 7.1.12 Bericap Holding