中国のプラスチックキャップおよびクロージャ:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

China Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 101 Pages

- 納期

- 2~3営業日

- 商品コード

- 1639367

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

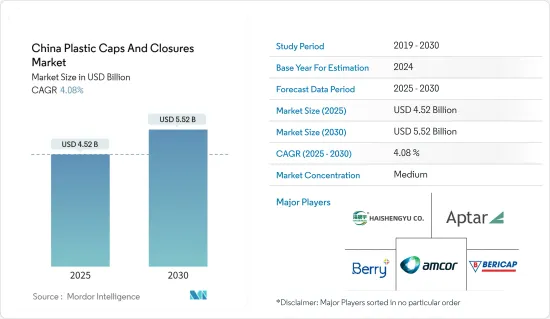

中国のプラスチックキャップおよびクロージャ市場規模は2025年に45億2,000万米ドルと推定・予測され、予測期間(2025-2030年)のCAGRは4.08%で、2030年には55億2,000万米ドルに達すると予測されます。

生産量では、2025年の1,013億7,000万個から2030年には1,256億1,000万個に成長し、予測期間(2025~2030年)のCAGRは4.38%と予測されます。

2023年、中国のGDPは前年比5.2%増となり、これは人口の着実な増加、急速な都市化、技術進歩に牽引されたものです。さらに、国民の飲料に対する意欲の高まりが包装業界の成長を後押ししています。

主なハイライト

- 中国は世界のプラスチック消費において圧倒的な存在感を示しています。豊富な原材料の埋蔵量とコスト効率を特徴とする生産環境により、中国はプラスチック生産の大幅な急増を目の当たりにしてきました。

- 中国では飲食品産業が急成長しており、プラスチックキャップおよびクロージャの需要が急増しています。消費者が調理済みのミールパックにますます傾倒する中、USDAが報告した中国の食品加工産業は、2023年に安定した成長を見せただけでなく、食品輸入量の増加に後押しされ、さらなる拡大が見込まれています。

- USDAはさらに、消費者の需要が進化し、より健康的な食事や家庭での食事に焦点を当てたライフスタイル中心のものになるにつれて、半調理済みの食事、植物由来の製品、軽食などの新しい食品分野が支持を集め、中国のプラスチックキャップおよびクロージャの市場を大幅に強化していることを強調しています。

- 中国では、プラスチックキャップおよびクロージャ市場は製品のイノベーションで繁栄し、多様な最終用途産業に対応しています。プラスチック包装の技術的進歩は業界革新の波をもたらしました。多くの中国企業が独自の費用対効果の高いソリューションの研究開発に多額の投資を行っており、技術革新のペースは加速しています。例えば、米国を拠点とするAptar Group Inc.は2024年4月、蘇州に「Aptar China Intelligent Production and Research &Development Base(Aptar中国インテリジェント生産・研究開発基地)」を開設し、アジア太平洋の極めて重要な製造拠点としました。

- しかし、市場はプラスチック廃棄物をめぐる環境問題の深刻化という大きなハードルに直面しています。中国の人口が増加し、飲食品の需要が急増するにつれて、この課題はますます大きくなっています。ACS出版によると、中国で年間2,600万トンものプラスチック廃棄物が発生しているが、リサイクルされているのはごく一部に過ぎないです。

中国のプラスチックキャップおよびクロージャ市場の動向

飲料セグメントが市場成長を牽引

- 2023年、米国農務省(USDA)は、中国で急増する中間所得層がますます健康を優先するようになっており、約57%が食品や飲飲料を購入する前に脂肪、糖分、カロリーなどの栄養の詳細を吟味していると報告しました。こうした意識の高まりにより、輸入品、特に食品サプリメントや高級乳製品の売上が急増し、市場の大幅な成長を牽引しています。

- 中国の飲料事情が進化するにつれ、メーカーは現地生産を強化しています。2023年9月、コカ・コーラの主要ボトラーであるスワイヤー・コカ・コーラ社は、20億人民元(約2億8,000万米ドル)を投資し、中国東部に最新鋭の工場を開設しました。

- 中国の小売シーンでは、砂糖不使用の選択肢、特にティーベースのミックスジュースへの意欲が高まっています。若い層をターゲットに、健康飲料に様々なフレーバーを導入することが、この市場拡大に拍車をかけています。コカ・コーラは2023年9月、AIを活用した「コカ・コーラY3000砂糖ゼロ」飲料を発表しました。

- 中国ではノンアルコール飲料産業が急成長しており、今後数年間はプラスチック容器の需要が高まるとみられます。中国国家統計局のデータによると、生産量は2024年3月の1,787万トンから2024年6月には1,954万トンに急増します。

ポリエチレン(PE)セグメントが最も高い市場シェアを記録する

- 耐久性のあるプラスチックであるポリエチレン(PE)は、耐薬品性とコストパフォーマンスに優れています。石油ポリマーに由来するポリエチレンは、環境の危険にも耐えることができます。主に高密度ポリエチレン(HDPE)と低密度ポリエチレン(LDPE)に分類されます。

- 一般的に、HDPEとLDPEはキャップやクロージャの主要素材です。特に、HDPEキャップはノンアルコール飲料ボトル業界を支配しています。その優れた特性により、ポリエチレンは水筒のキャップに最適な素材となっています。石油由来の熱可塑性ポリマーであるHDPEは、その適応性と堅牢性から、中国の多様な産業にとって最良の選択肢として際立っています。

- 世界第2位の美容市場である中国では、化粧品とパーソナルケア産業においてPEキャップおよびクロージャの動向が高まっています。この急成長の背景には、スキンケアへの消費支出の増加、セルフケアの重視、天然成分やオーガニック成分への嗜好の高まりがあります。さらに、中国における化粧品のeコマース販売ブームが、この市場拡大に拍車をかけています。

- プラスチックキャップおよびクロージャは、製品をほこりやこぼれ、汚染から守る包装において重要な役割を果たしています。耐久性、リサイクル性、費用対効果に優れているため、メーカーの間で好んで選ばれています。中国では、PEがキャップやクロージャの素材としてトップに君臨しています。中国国家統計局のデータによると、2024年6月までに中国のプラスチック製品の生産量は約659万トンに上ります。中国は世界最大のプラスチック生産国であり、世界のプラスチック生産量の3分の1近くを占めています。

中国のプラスチックキャップおよびクロージャ産業の概要

中国のキャップおよびクロージャ市場は、飲料需要の急増と多数の国内外のベンダーが市場に進出していることから、適度に統合されています。この競合情勢を乗り切り、市場での存在感を高めるため、これらのベンダーは水平統合と垂直統合の両方への傾斜を強めています。同市場の主要企業は、Bericap Holding GmbH、Aptar Group、Berry Global Inc.、Shangdong Haishengyu Plastic Industryなどです。

- 2024年4月ドイツに本社を置くBericap Holding GmbHは、中国の昆山に新しい製造工場を設立しました。中国顧客からの需要急増に対応するため、生産能力を50%増強します。上海近郊の戦略的な立地である昆山は、ベリカップに現地での足場を提供し、迅速な顧客サポートと効率的な製品物流を促進します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- 国内における飲食品消費の拡大

- 市場における製品イノベーションの増加

- 市場の課題

- プラスチック包装に対する環境問題の高まり

第6章 業界の規制と政策、規格

第7章 市場セグメンテーション

- 樹脂別

- ポリエチレン(PE)

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- その他の樹脂(ポリスチレン、PVC、ポリカーボネートなど)

- 製品タイプ別

- ネジ式- スクリューキャップ、真空など

- ディスペンサー

- ネジなし- オーバーキャップ、リッド、エアゾールベースクロージャ

- チャイルドレジスタント

- 最終用途産業別

- 食品

- 飲料

- ボトル入り飲料水

- 炭酸飲料

- アルコール飲料

- ジュースとエナジードリンク

- その他の飲料

- パーソナルケアと化粧品

- 家庭用化学品

- その他の最終用途産業

第8章 競合情勢

- 企業プロファイル

- Shangdong Haishengyu Plastic Industry Co. Ltd

- Bericap Holding GmbH

- Berry Global Inc.

- Silgan Holdings Inc.

- Taizhou Huangyan Baitong Plastic Co. Ltd

- Ningbo Kinpack Commodity Co. Ltd

- Amcor GmbH

- Aptar Group Inc.

- Heat Map Analysis

- Competitor Analysis-Emerging vs. Established Players

第9章 リサイクルと持続可能性の展望

第10章 将来の展望

目次

The China Plastic Caps And Closures Market size is estimated at USD 4.52 billion in 2025, and is expected to reach USD 5.52 billion by 2030, at a CAGR of 4.08% during the forecast period (2025-2030). In terms of production volume, the market is expected to grow from 101.37 billion units in 2025 to 125.61 billion units by 2030, at a CAGR of 4.38% during the forecast period (2025-2030).

In 2023, China's GDP grew by 5.2% Y-o-Y, driven by a steadily growing population, swift urbanization, and technological progress. Additionally, the nation's rising appetite for beverages fuels growth in the packaging industry.

Key Highlights

- China stands out as a dominant player in global plastic consumption. With its rich reserves of raw materials and a production landscape characterized by cost efficiency, the nation has witnessed a significant surge in plastic production.

- The burgeoning food and beverage industries in China are driving swift demand for plastic caps and closures. As consumers increasingly lean toward pre-cooked meal packs, the food processing industry in China, as reported by USDA, not only showcased steady growth in 2023 but is also poised for further expansion, buoyed by rising food product import volumes.

- USDA further highlights that as consumer demands evolve and become more lifestyle-centric with a focus on healthier eating and at-home dining, new food segments such as semi-prepared meals, plant-based products, and light snacks are gaining traction, significantly bolstering the market for plastic caps and closures in China.

- In China, the plastic caps and closures market thrives on product innovation, catering to diverse end-use industries. Technological strides in plastic packaging have ushered in a wave of industry innovations. With many Chinese firms channeling substantial investments into research and development for unique, cost-effective solutions, the pace of innovation is accelerating. For instance, in April 2024, US-based Aptar Group Inc. inaugurated its 'Aptar China Intelligent Production and Research & Development Base' in Suzhou, marking it as a pivotal manufacturing hub for Asia-Pacific.

- Yet, the market grapples with a significant hurdle: mounting environmental concerns surrounding plastic waste. As China's population grows and the demand for food and beverage takeaways surges, the challenge intensifies. ACS Publications reports a staggering 26 million tons of plastic waste generated annually in China, with only a mere fraction undergoing recycling.

China Plastic Caps And Closures Market Trends

The Beverages Segment to Drive the Growth of the Market

- In 2023, the USDA reported that a burgeoning middle-income group in China is increasingly prioritizing health, with around 57% scrutinizing nutritional details such as fat, sugar, and calorie content before purchasing food or beverages. This heightened awareness has led to a surge in sales of imported items, particularly food supplements and premium dairy products, driving significant market growth.

- As China's beverage landscape evolves, manufacturers are ramping up local production. In September 2023, Swire Coca-Cola Ltd, a key bottler for Coca-Cola, invested CNY 2 billion (approximately USD 280 million) to inaugurate a state-of-the-art factory in eastern China.

- China's retail scene has long showcased a rising appetite for sugar-free options, especially tea-based mixes. Catering to the younger demographic, introducing varied flavors in healthy beverages is fuelling this market expansion. Highlighting this trend, Coca-Cola unveiled its AI-assisted 'Coca-Cola Y3000 Zero Sugar' drink in September 2023.

- China's burgeoning non-alcoholic beverages industry is set to bolster demand for plastic containers over the coming years. Data from the National Bureau of Statistics of China revealed a production leap from 17.87 million tons in March 2024 to 19.54 million tons by June 2024.

The Polyethylene (PE) Segment to Register the Highest Market Share

- Polyethylene (PE), a durable plastic, offers chemical resistance and cost-effectiveness. Derived from petroleum polymers, PE can endure environmental hazards. It is primarily categorized into high-density polyethylene (HDPE) and low-density polyethylene (LDPE).

- Commonly, HDPE and LDPE are the go-to materials for caps and closures. Specifically, HDPE caps dominate the non-alcoholic beverage bottle industry. Due to its superior properties, polyethylene has been the top choice for water bottle closures. Given its adaptability and robustness, HDPE, a thermoplastic polymer from petroleum, stands out as a prime choice for diverse industries in China.

- China, the world's second-largest beauty market, sees a rising trend in PE caps and closures within its cosmetics and personal care industries. This surge is driven by heightened consumer spending on skincare, a growing emphasis on self-care, and a growing preference for natural and organic ingredients. Additionally, the boom in e-commerce sales of cosmetics in China is fueling this market expansion.

- Plastic caps and closures play a crucial role in packaging, shielding products from dust, spills, and contamination. Their durability, recyclability, and cost-effectiveness make them a favored choice among manufacturers. In China, PE reigns as the top material for crafting caps and closures. Data from the National Bureau of Statistics of China revealed that by June 2024, the nation produced approximately 6.59 million tons of plastic products. Dominating the global scene, China is the largest plastic producer, responsible for nearly a third of the global plastic output, propelling the growth of the plastic caps and closures market.

China Plastic Caps And Closures Industry Overview

The Chinese caps and closures market is moderately consolidated due to a surge in demand for beverages and a multitude of domestic and international vendors operating in the market. To navigate this competitive landscape and bolster their market presence, these vendors are increasingly leaning toward both horizontal and vertical integration. Key players in the market encompass Bericap Holding GmbH, Aptar Group, Berry Global Inc., and Shangdong Haishengyu Plastic Industry Co. Ltd.

- April 2024: Bericap Holding GmbH, a Germany-based company, established a new manufacturing plant in Kunshan, China. This move aims to boost its production capacity by 50% in response to the surging demand from Chinese customers. Strategically located near Shanghai, Kunshan offers Bericap a local foothold, facilitating prompt customer support and efficient product logistics.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Consumption of Food and Beverages in the Country

- 5.1.2 Increasing Product Innovation in the Market

- 5.2 Market Challenge

- 5.2.1 Growing Environmental Concerns Over Plastic Packaging

6 INDUSTRY REGULATION, POLICY, AND STANDARDS

7 MARKET SEGMENTATION

- 7.1 By Resin

- 7.1.1 Polyethylene (PE)

- 7.1.2 Polyethylene Terephthalate (PET)

- 7.1.3 Polypropylene (PP)

- 7.1.4 Other Resins (Polystyrene, PVC, Polycarbonate, etc.)

- 7.2 By Product Type

- 7.2.1 Threaded - Screw Caps, Vacuum, etc.

- 7.2.2 Dispensing

- 7.2.3 Unthreaded - Overcaps, Lids, Aerosol-based Closures

- 7.2.4 Child-resistant

- 7.3 By End-use Industry

- 7.3.1 Food

- 7.3.2 Beverage**

- 7.3.2.1 Bottled Water

- 7.3.2.2 Carbonated Soft Drinks

- 7.3.2.3 Alcoholic Beverages

- 7.3.2.4 Juices and Energy Drinks

- 7.3.2.5 Other Beverages

- 7.3.3 Personal Care and Cosmetics

- 7.3.4 Household Chemicals

- 7.3.5 Other End-use Industries

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Shangdong Haishengyu Plastic Industry Co. Ltd

- 8.1.2 Bericap Holding GmbH

- 8.1.3 Berry Global Inc.

- 8.1.4 Silgan Holdings Inc.

- 8.1.5 Taizhou Huangyan Baitong Plastic Co. Ltd

- 8.1.6 Ningbo Kinpack Commodity Co. Ltd

- 8.1.7 Amcor GmbH

- 8.1.8 Aptar Group Inc.

- 8.2 Heat Map Analysis

- 8.3 Competitor Analysis - Emerging vs. Established Players

9 RECYCLING & SUSTAINABILITY LANDSCAPE**

10 FUTURE OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 101 Pages

- 納期

- 2~3営業日