|

市場調査レポート

商品コード

1550333

中国の業務用HVAC:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)China Commercial HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の業務用HVAC:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

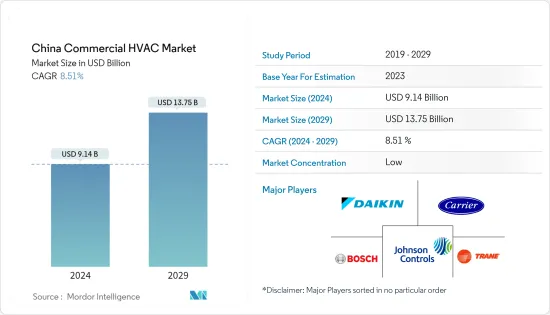

中国の業務用HVAC市場規模は2024年に91億4,000万米ドルと推定され、2029年には137億5,000万米ドルに達し、予測期間中(2024-2029年)にCAGR 8.51%で成長すると予測されます。

主なハイライト

- HVACシステムは、どのような商業施設にとっても、居住者に快適な雰囲気を提供するために重要かつ不可欠です。例えば、HVACシステムは多くのオフィスで頻繁に利用され、適切な温度と換気設定を提供することで、従業員の生産性と労働条件を改善し、不十分な湿度レベルがもたらす健康リスクを最小限に抑えるのに役立っています。中国におけるこのようなHVACソリューションのニーズは、エアハンドリングユニットなどのHVAC機器に対する需要を増加させると予想されます。

- HVAC機械・部品の主要製造拠点である中国は、市場成長の推進において極めて重要です。強固な製造インフラを持つ中国は、HVAC機器に特化した数多くの工場を擁しています。この生産規模は規模の経済を保証し、競争力のある価格設定につながります。例えば、HVAC機器の一種であるヒートポンプは、2030年までにCO2排出量をピークアウトさせ、2060年までにカーボンニュートラルを達成するという中国の取り組みにおいて、極めて重要な役割を果たすと考えられています。

- 中国では、中国グリーンビルディング評価ラベル(GBEL)をはじめとする環境法が普及しつつあります。その結果、同国のHVAC業界は、地球温暖化係数(GWP)が低く、エネルギー効率の高い、環境に優しいAHUに目を向けています。

- 商業環境では、HVAC機器は冷暖房システムに不可欠なさまざまな部品を含んでいます。HVAC機器の部品が増えるごとに、部品故障のリスクは高まり、中国のHVAC機器市場拡大の障害となっています。さらに、HVAC機器が故障すると、エンドユーザーの運転コストが上昇し、代替製品を検討するようになるため、HVAC機器の需要が減退します。

- 中国の商業用HVAC市場は、インフレや金利上昇といったマクロ経済要因による課題が続いています。さらに、設備や設置のコストが上昇するにつれて、消費者は買い替えよりも修理を選ぶ可能性があります。さらに、中国は2035年までにHFCの生産と消費の70%を占めると予測されており、HVAC部門は潜在的な不足と顕著な価格高騰に直面しています。

中国の商業用HVAC市場の動向

商業用ビルが大幅な成長を遂げる見込み

- 中国は世界のHVAC市場において重要な地位を占めており、暖房は世界のHVAC総売上の42%を占めています。中国政府は、2060年までにカーボンニュートラルを達成するため、国の商業活動によって悪化する大気質の懸念に対抗する取り組みを強化しています。例えば、中国国家統計局によると、2023年、中国で販売された商業化された不動産からの総売上高は約11兆7,000億人民元(1兆6,100億米ドル)に達しました。

- 2023年11月、Carrier Corporationは長沙で開催された年次会議において、中国各地から300社以上の業務用HVACディーラーを招いた。業務用機器市場の機会」イベントでは、キャリアの首脳部が新エネルギー、データセンター、農業、ヘルスケアといった急成長分野への戦略的投資を強調しました。このイベントでは、インテリジェントでグリーンなビルディング・ソリューションの採用により、中国のデュアル・カーボン戦略を支えるHVAC業界の役割が強調されました。

- 業務用エアコン業界は今後数年間、中国で大きな成長が見込まれています。自動化システムや環境に優しい技術など、様々な動向が市場に大きな影響を与えると予測されます。エネルギー効率の高いエアコンへのニーズの高まりが、この分野の拡大を後押ししています。さらに、商業建設業界の成長は、中国におけるエアコン需要の急増に重要な役割を果たしています。

- さらに、データセンターにはデリケートな電子部品が配置されており、重要な機械の故障を避けるために温度、湿度、換気、清浄度を毎日維持しなければならないです。データセンターの成長は、業務用換気装置の需要を促進する重要な要因です。さらに、データセンターの管理者は、サーバールームが適切な温度と湿度に保たれていることを確認するために、AHUのような堅牢なHVACツールを使用することができます。

HVAC機器が大きな市場シェアを占める見込み

- 中国の建築部門では、空間冷却のためのエネルギー需要が急速に急増し、電力網に圧力がかかっています。この急増は地域の大気汚染を悪化させ、二酸化炭素(CO2)排出量を増大させています。過去20年間、中国は世界中で最も急速に建物の冷房エネルギー需要が増加してきました。IEAが報告しているように、世界的に3%減少する中、中国は2023年にヒートポンプ販売台数が増加する唯一の主要市場として際立っています。暖房を石炭に依存し続けているにもかかわらず、この変化は中国のエネルギー情勢における注目すべき動向を浮き彫りにしています。

- 中国はヒートポンプの最大の製造・輸出国であり、世界の生産量の約40%を占めています。特筆すべきは、中国のヒートポンプ輸出の大半が欧州向けであることです。中国は、ヒートポンプの設置に特化した世界最大の労働力を誇り、ヒートポンプ製造において40%を超える圧倒的な市場シェアを誇っています。この地域の製造能力は、市場の成長を高めると思われます。

- 空調(AC)システムは、レストラン、病院、学校、ホテル、オフィスビルなど、さまざまな商業ビルの居住者にとって快適な環境を維持する上で極めて重要です。例えば、オフィスでは、最適な温度と換気を確保するために業務用AC(エアコン)に頼ることが多く、不適切な湿度レベルに関連する問題を回避することで、従業員の生産性、労働条件、健康状態の改善につながります。

- 例えば、2023年9月、キャリア・世界・コーポレーションの一部門である東芝HVACは、中国本土で最新のデジタル・インバーター(DI)シリーズを発表しました。この新しい小型業務用ダクトレス・スプリット空調システムは、設置が簡単で、エネルギー効率が高く、スマートな機能を誇る。DIシリーズの特長は以下の通り:エネルギー効率は、負荷管理と正確な温度制御を保証し、エネルギーを節約しながらユーザーの快適性を高めます。

中国商業用HVAC産業の概要

中国の業務用HVAC市場は断片化されており、ダイキン工業、キャリア、ロバート・ボッシュ、ジョンソンコントロールズ・インターナショナル、三菱電機ハイドロニクス&ITクーリングシステムズ、システムエアABといった大手企業が存在します。同市場のプレーヤーは、パートナーシップ、合併、技術革新、投資、買収などの戦略を採用し、製品提供を強化し、持続可能な競争優位性を獲得しています。

- 2024年3月、サムスン電子はジョンソンコントロールズ・インターナショナルのHVAC資産(60億米ドル以上)の買収を競った。この潜在的な取引は、サムスンにとって7年ぶりの重要な買収を意味し、急成長するHVAC市場への戦略的進出を示唆するものです。HVAC市場は、今後数年間で大幅な成長が見込まれています。一方、ジョンソンコントロールズは、アドバイザーとともに軽商用事業の売却を積極的に進めています。

- 2024年2月キャリア・チャイナは中国東方航空投資(CESインベストメント)と1,700万米ドル(1億人民元)の契約を結び、中国の商業オフィス向けにXCT7可変冷媒フロー(VRF)システムを提供。これらのシステムは、中国の国家エネルギー効率基準レベルiを上回り、最大10という驚異的な積算部分負荷値(IPLV)を誇る。わずか23デシベルという、ささやき声よりも静かな超静音運転を誇り、空間を素早く冷却または加熱することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- エネルギー効率の高い機器に対する需要の増加

- 交換・レトロフィットサービスへの需要の高まり

- 市場の課題

- エネルギー効率の高いシステムの初期コストの高さ

- 熟練労働者の不足

- 厳しい規制遵守と安全基準

第6章 市場セグメンテーション

- 部品タイプ別

- HVAC機器

- 暖房機器

- 空調・換気機器

- HVACサービス

- HVAC機器

- エンドユーザー産業別

- ホスピタリティ

- 商業ビル

- 公共施設

- その他

第7章 競合情勢

- 企業プロファイル

- Daikin Industries Ltd

- Carrier Corporation

- Robert Bosch GmbH

- Johnson Controls International PLC

- Trane Technologies Plc

- Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A.

- LG Electronics Inc.

- Danfoss Inc.

- System Air AB

- Midea Group

第8章 投資分析

第9章 市場の将来

The China Commercial HVAC Market size is estimated at USD 9.14 billion in 2024, and is expected to reach USD 13.75 billion by 2029, growing at a CAGR of 8.51% during the forecast period (2024-2029).

Key Highlights

- HVAC systems are crucial and essential for any commercial structure to provide occupants with a comfortable atmosphere. For instance, HVAC systems are frequently utilized in many offices to offer suitable temperature and ventilation settings, which helps to improve employee productivity and working conditions and minimize health risks brought on by inadequate humidity levels. This need for HVAC solutions in China is anticipated to increase demand for HVAC equipment such as air handling units.

- China, a key manufacturing hub for HVAC machinery and components, is pivotal in driving market growth. With a robust manufacturing infrastructure, China hosts numerous factories specializing in HVAC equipment. This scale of production ensures economies of scale and translates into competitive pricing. For instance, Heat pumps, a type of HVAC equipment, are poised to be pivotal in China's efforts to peak CO2 emissions by 2030 and attain carbon neutrality by 2060.

- Environmental laws, including the China Green Building Evaluation Label (GBEL), are becoming more prevalent in China. As a result, the country's HVAC industry is turning toward environmentally friendly AHUs with low Global Warming Potential (GWP) and energy-efficient technology.

- In commercial settings, HVAC equipment encompasses an array of components vital for heating and cooling systems. With each additional part in an HVAC unit, the risk of component failure rises, presenting a hurdle to China's HVAC equipment market expansion. Furthermore, when HVAC equipment fails, it raises operating costs for end-users and prompts them to consider alternative products, dampening the demand for HVAC equipment.

- Continuing challenges from macroeconomic factors such as inflation and elevated interest rates persist for the commercial HVAC market in China. Moreover, as equipment and installation costs rise, consumers may opt for repairs over replacements. Furthermore, with China projected to account for 70% of HFC production and consumption by 2035, the HVAC sector faces potential shortages and notable price escalations.

China Commercial HVAC Market Trends

Commercial Buildings is Expected to Witness a Significant Growth

- China holds a significant position in the global HVAC market, with heating accounting for 42% of total HVAC sales worldwide. The government of China is intensifying efforts to combat air quality concerns exacerbated by the nation's commercial activities to achieve carbon neutrality by 2060. For instance, according to the National Bureau of Statistics of China, in 2023, the total sales revenue from commercialized real estate sold in China amounted to around CNY 11.7 trillion (USD 1.61 trillion).

- In November 2023, Carrier Corporation hosted over 300 commercial HVAC dealers from various regions of China at its annual conference in Changsha. At the Commercial Equipment Market Opportunities event, Carrier's leadership highlighted the company's strategic investments in burgeoning sectors such as new energy, data centers, agriculture, and healthcare. The event highlighted the role of the HVAC industry in supporting China's dual carbon strategy by adopting intelligent and green building solutions.

- The commercial air conditioner industry is expected to experience significant growth in China in the coming years. Various trends, such as automated systems and environmentally friendly technology, are projected to impact the market substantially. The growing need for energy-efficient air conditioners is driving the expansion of this sector. Additionally, the growth of the commercial construction industry is playing a crucial role in the surging demand for air conditioners in China.

- Moreover, sensitive electronic components are located in data centers, and temperature, humidity, ventilation, and cleanliness must be maintained daily to avoid the breakdown of critical machinery. The growth in data centers is a crucial factor driving the demand for commercial ventilation equipment. Additionally, data center managers can use robust HVAC tools like AHUs to ensure that server rooms are kept at the right temperature and humidity.

HVAC Equipment is Expected to Hold Significant Market Share

- China's building sector is witnessing a rapid surge in energy demand for space cooling, exerting pressure on its electricity grid. This surge exacerbates local air pollution and escalates carbon dioxide (CO2) emissions. Over the past two decades, China has experienced the swiftest escalation in building cooling energy demand globally. China stands out as the sole primary market to witness growth in heat pump sales in 2023 amidst a global decline of 3%, as reported by the IEA. Despite its continued reliance on coal for heating, this shift underscores a notable trend in China's energy landscape.

- China is the largest manufacturer and exporter of heat pumps, accounting for approximately 40% of the global production. Notably, most of China's heat pump exports are directed towards Europe. China boasts the largest workforce globally specializing in heat pump installations, commanding a dominant market share exceeding 40% in heat pump manufacturing. The region's manufacturing capabilities will enhance the market's growth.

- Air conditioning (AC) systems are crucial in maintaining a comfortable environment for occupants in various commercial buildings, including restaurants, hospitals, schools, hotels, and office buildings. For instance, offices often rely on commercial AC (air conditioners) to ensure optimal temperature and ventilation, leading to improved employee productivity, working conditions, and health outcomes by avoiding issues related to improper humidity levels.

- For instance, in September 2023, Toshiba HVAC, a Carrier Global Corporation division, introduced its latest Digital Inverter (DI) series in mainland China. This new light commercial ductless split air-conditioning system boasts easy installation and energy-efficient, smart features. The DI series highlights the following: Energy Efficiency ensures load management and precise temperature control, enhancing user comfort while conserving energy.

China Commercial HVAC Industry Overview

The Chinese commercial HVAC market is fragmented, with the presence of major players like Daikin Industries Ltd, Carrier Corporation, Robert Bosch GmbH, Johnson Controls International PLC, Mitsubishi Electric Hydronics & IT Cooling Systems SpA, and System Air AB. Players in the market are adopting strategies such as partnerships, mergers, innovations, investments, and acquisitions to enhance product offerings and gain sustainable competitive advantage.

- In March 2024, Samsung Electronics Co. vied to acquire Johnson Controls International's HVAC assets, valued at over USD 6 billion. This potential deal would signify Samsung's first significant acquisition in seven years and signal its strategic move into the burgeoning HVAC market. It is expected to witness substantial growth in the years ahead. Meanwhile, Johnson Controls is actively pursuing the divestment of its light commercial businesses in tandem with its advisors.

- February 2024: Carrier China signed a USD 17 million (RMB 100 million) deal with China Eastern Airlines Investment Co., Ltd. (CES Investment) to provide XCT7 variable refrigerant flow (VRF) systems for commercial offices in China. These systems surpass China's national Level I energy efficiency standard, boasting an impressive integrated part load value (IPLV) of up to 10. It can rapidly cool or heat spaces, boasting an ultra-quiet operation at just 23 decibels, quieter than a whisper.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand For Energy-Efficient Devices

- 5.1.2 Growing Demand for Replacement and Retrofit Services

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Energy-Efficient Systems

- 5.2.2 Shortage of Skilled Labour

- 5.2.3 Stringent Regulatory Compliance and Safety Standards

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning /Ventillation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End-User Industry

- 6.2.1 Hospitality

- 6.2.2 Commercial Buildings

- 6.2.3 Public Buildings

- 6.2.4 Others

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Daikin Industries Ltd

- 7.1.2 Carrier Corporation

- 7.1.3 Robert Bosch GmbH

- 7.1.4 Johnson Controls International PLC

- 7.1.5 Trane Technologies Plc

- 7.1.6 Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A.

- 7.1.7 LG Electronics Inc.

- 7.1.8 Danfoss Inc.

- 7.1.9 System Air AB

- 7.1.10 Midea Group