|

市場調査レポート

商品コード

1550312

フランスの商用HVAC:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)France Commercial HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フランスの商用HVAC:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

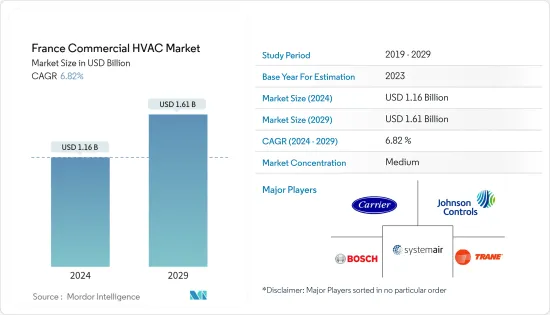

フランスの商用HVAC市場規模は2024年に11億6,000万米ドルと推定予測され、2029年には16億1,000万米ドルに達し、予測期間(2024-2029年)のCAGRは6.82%で成長すると予測されます。

主なハイライト

- フランスでは、気候変動、都市化、生活水準の向上に後押しされ、HVACシステムの需要が高まっています。小売スペースやオフィスビルを含む商業セクターは、この需要拡大において極めて重要です。既存の建造物の改築や改修に向けた顕著なシフトは、特に現代の省エネソリューションと連携したHVACアップグレードの必要性を強調しています。

- エネルギー効率の高い機器の導入に向けた政府の取り組みや投資の増加は、市場の成長を促進します。例えば、フランスでは2027年末までに100万台のヒートポンプの製造が義務付けられています。これらのヒートポンプは、暖房関連の排出を抑制する上で極めて重要であり、ガスボイラーや電気ラジエーターよりも約3倍優れたエネルギー効率レベルを誇っています。

- HVAC機器の初期コストの高さは、その需要にとって課題となり得る。なぜなら、価格の高さがシステムの購入やアップグレードを躊躇させる顧客もいるからです。これは、予算が限られており、新しいシステムの初期費用を支払うための支援を必要とすることができないかもしれない中小企業の所有者に特に当てはまります。第二に、HVAC機器のコストが高いため、顧客の投資回収期間が長くなる可能性があります。これは、新システムのエネルギー効率向上によるコスト削減が、数年間は初期投資を相殺できない可能性があることを意味します。

- フランスのマクロ経済情勢は、高金利、インフレ、地政学的緊張の高まりによる景気後退懸念など、依然として不安定な状況が続いています。この不確実な環境は、さまざまな分野の消費者に慎重な姿勢をとらせることになった。市場回復の兆しは見えているもの、その正確な時期や道筋は不透明です。さらに、古くなったHVACシステムをより効率的にアップグレードするための経済的インセンティブを提供するイニシアチブが、市場の成長を後押ししています。

フランスの商用HVAC市場動向

商業用ビルは大幅な成長が見込まれる

- 商業ビル分野は、オフィスビル、小売店、ショールーム、倉庫などのインフラを含みます。フランスにおける商業建築の増加は、調査された市場を牽引すると予想されます。例えば、Inseeによると、2023年には倉庫が床面積で非住宅建築をリードしました。また、この年には約310万平方メートルのオフィスと290万平方メートルのオフィスが建設されました。

- HVAC(暖房、換気、空調)システムは、小売業の成功に不可欠です。これらのシステムは、快適な買い物環境を作り、維持し、顧客や従業員の健康を確保し、温度に敏感な商品の品質を維持する役割を担っています。アレルゲンやホコリの蓄積を防ぎ、空気の質やシステムの効率に影響を与えないためには、頻繁かつ徹底したメンテナンスが重要です。FEVADによると、2023年のフランスのeコマース売上高は約1,600億ユーロに達し、前年の1,447億ユーロから約10.5%の伸びを示します。

- 換気設備は、そのサイズや機能の幅広さから、1つの空間から建物全体まで利用されることがあります。これらのシステムは、商業規模の建物の地下や屋上に設置されることが多いです。これらのシステムは、暖房や冷房のために、特定の建物の領域に割り当てることができます。

- これらの構造は、商業用オフィスビルの冷暖房に必要なエネルギーの約45%を使用しています。オフィスビルで使われるエネルギーの大半は無駄であることが判明しました。オフィスビルにおける冷暖房エネルギー消費の効率は概して大きく伸びているにもかかわらず、熱エネルギーと機械エネルギーの全体的な需要は変わっていないです。オフィスビルの建築面積が拡大するにつれ、ビルのエネルギー消費量の増加傾向は続き、国内の室内空気品質を維持するための換気装置の需要が生まれます。

暖房機器が最大の市場シェアを占める見通し

- ヒートポンプは、暖房に関連する排出量を削減する重要なソリューションと考えられています。特定の地域にもよるが、このシステムはガスボイラーや電気ラジエーターに比べて約3倍のエネルギーを消費します。多くのヒートポンプが生産されることで、産業分野全体のHVAC機器の需要が刺激されます。例えばフランスでは、再生可能エネルギーへの転換を促進するための明確な目標と政策が確立されています。また、EUのREPowerEUイニシアチブは、ヒートポンプの年間設置台数を増加させ、EU圏のガス輸入への依存を軽減することを目指しています。

- フランスでは、エネルギー効率と経済効率の両方に優れた空調・換気システムに対するニーズが高まっているため、HVAC機器市場が急速に拡大しています。可処分所得の増加、建設活動の拡大、エネルギー効率の重視により、同国は今後数年間で大きな成長を遂げると予想されます。

- 業務用ACシステムは、かなりの冷却を必要とするため、極めて重要なエネルギー効率を必要とします。これに対処するため、メーカーは可変速コンプレッサーやファン、エネルギー回収システム、高度な制御アルゴリズムなど、さまざまな省エネ要素をこれらのシステムに組み込んでいます。例えば、業務用空調システムは、複数のエアダクトを利用して、調整された空気をさまざまなエリアに効率的に分配します。

- 国内の規制の変化に伴い、各社は同市場において新サービスの導入、合併、買収に投資しています。例えば、2023年11月、ソネパールは、空調・空気処理用の機器とソリューションを販売するフランスの専門企業Hydeclimの買収を発表しました。アリアンツ(太陽光発電)やCDスッドなど、ソネパール・グループが最近フランスで行った買収に続き、この買収によってソネパールはHVAC市場を拡大し、特にフランス西部と北部の空調・暖房設備業者へのサービス提供を拡大することができます。

フランス商用HVAC業界の概要

フランスの商用HVAC市場は断片化されており、Carrier Corporation、Johnson Controls International PLC、Robert Bosch GmbH、System Air AB、Tran Technologies PLC、Flaktgroup Inc.、LG Electronics Inc.などの大手企業が存在します。同市場のプレーヤーは、パートナーシップ、合併、技術革新、投資、買収などの戦略を採用し、製品提供の強化と持続可能な競争優位の獲得を目指しています。

- 2024年4月三菱電機は、フランスを拠点とする著名な空調機器グループであるAircaloを買収することで、欧州におけるHVACRのプレゼンスを強化しました。この戦略的な動きは三菱のポートフォリオを強化し、より広範なハイドロニックシステムへの対応を可能にしました。これらのシステムは、温室効果ガスの排出削減に焦点を当てた、効率的で環境に優しい冷暖房ソリューションに対する市場の需要の高まりに対応するために設計されています。

- 2023年11月持続可能なソリッドステート冷却ソリューションのプロバイダーであるPhononic社と、HVACと室内空気質の革新者であるHalton社は、新たな商業プロジェクトである「TTAP」ペルチェによる空気のターミナル治療を発表しました。パリ中心部にある8,500平方メートルの歴史的建造物に設置されたこの先進的な設備は、最大のソリッドステートHVACプラットフォームとして世界のマイルストーンとなった。その主な目的は、温室効果ガスの排出を大幅に削減し、同時にビルの居住者の快適性を高めることです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 税額控除プログラムによる省エネ奨励を含む政府の支援規制

- エネルギー効率の高い機器に対する需要の増加

- 市場の課題

- エネルギー効率の高いシステムの初期コストの高さ

- 熟練労働者の不足

- 厳しい規制遵守と安全基準

第6章 市場セグメンテーション

- コンポーネントタイプ別

- HVAC機器

- 暖房機器

- 空調/換気機器

- HVACサービス

- HVAC機器

- エンドユーザー産業別

- ホスピタリティ

- 商業ビル

- 公共施設

- その他のエンドユーザー産業

第7章 競合情勢

- 企業プロファイル

- Carrier Corporation

- Johnson Controls International PLC

- Robert Bosch GmbH

- System Air AB

- Trane Technologies PLC

- Flaktgroup Inc.

- LG Electronics Inc.

- BDR Thermea Group

- Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A.

- Danfoss Inc.

- Panasonic Corporation

第8章 投資分析

第9章 市場の将来

The France Commercial HVAC Market size is estimated at USD 1.16 billion in 2024, and is expected to reach USD 1.61 billion by 2029, growing at a CAGR of 6.82% during the forecast period (2024-2029).

Key Highlights

- France is witnessing a rising demand for HVAC systems, propelled by climate change, urbanization, and improving living standards. The commercial sector, encompassing retail spaces and office buildings, is pivotal in this escalating demand. A pronounced shift towards renovating and retrofitting existing structures underscores the imperative for HVAC upgrades, particularly in alignment with contemporary energy-saving solutions.

- Rising government initiatives and investments in adopting energy-efficient equipment will drive market growth. For instance, by the end of 2027, France is mandated to manufacture 1 million heat pumps. These heat pumps are pivotal in curbing heating-related emissions, boasting energy efficiency levels approximately three times superior to gas boilers or electric radiators, varying slightly based on the local setting.

- The high initial cost of HVAC equipment can be challenging for its demand because the high price may deter some customers from purchasing or upgrading their systems. This is especially true for small business owners who may have limited budgets and be unable need help to afford the upfront costs of a new system. Secondly, the high cost of HVAC equipment can result in long customer payback periods. This means that the cost savings resulting from the new system's improved energy efficiency may not offset the initial investment for several years.

- France's macroeconomic landscape remained turbulent, characterized by high interest rates, inflation, and concerns over a looming recession, exacerbated by rising geopolitical tensions. This environment of uncertainty has led consumers in diverse sectors to adopt a cautious approach. Although a market recovery is on the horizon, the exact timing and path are uncertain. Furthermore, initiatives providing financial incentives to upgrade outdated and more efficient HVAC systems fuel market growth.

France Commercial HVAC Market Trends

Commercial Buildings is Expected to Witness a Significant Growth

- The commercial building segment compromises infrastructures like office buildings, retail, showrooms, and warehouses. The rise in commercial construction in France is expected to drive the studied market. For instance, according to Insee, in 2023, warehouses led non-residential construction in terms of floor space. The year also saw the construction of approximately 3.1 million sq m of office space and 2.9 million square.

- HVAC (heating, ventilation, air conditioning) systems are critical to the success of a retail business. These systems are responsible for creating and maintaining a comfortable shopping environment, ensuring the well-being of customers and employees, and maintaining the quality of temperature-sensitive products. Frequent and thorough maintenance is crucial to prevent the buildup of allergens and dust, affecting air quality and system efficiency. According to FEVAD, In 2023, France's e-commerce sales hit around EUR 160 billion, marking a growth of about 10.5% from the previous year's EUR 144.7 billion.

- Ventilation equipment may be utilized for either a single space or an entire building due to its wide range of size and functionality. These systems are frequently located in the basement or on the roof of commercial-sized buildings. These systems can then be allocated to particular building regions for heating or cooling.

- These structures use about 45% of the energy required to heat and cool commercial office buildings. The majority of the energy spent in office buildings was discovered to be wasted. The overall demand for thermal and mechanical energy has remained the same, even though the efficiency of heating and cooling energy consumption in office buildings has generally grown significantly. The increasing building energy consumption trend will continue as the office-built area expands, creating a demand for ventilation equipment to maintain indoor air quality in the country.

Heating Equipment is Expected to Hold Largest Market Share

- Heat pumps are seen as a significant solution in lowering emissions related to heating. Depending on the specific area, the systems use about three times less energy than gas boilers or electric radiators. The production of many heat pumps stimulates demand for HVAC equipment across industry segments. For instance, France has established clear objectives and policies to expedite its shift towards renewable energy sources. The EU's REPowerEU initiative also aims to ramp up annual heat pump installations, lessening the bloc's dependence on gas imports.

- The market for HVAC equipment is expanding quickly in France because of the rising need for air conditioning and ventilation systems that are both energy and financially efficient. The country is anticipated to experience significant growth in the upcoming years because of rising disposable incomes, expanding construction activity, and a greater emphasis on energy efficiency

- Due to the substantial cooling requirements, commercial AC systems require a crucial amount of energy efficiency. To address this, manufacturers integrate various energy-saving elements into these systems, including variable-speed compressors and fans, energy recovery systems, and advanced control algorithms. For example, commercial air conditioning systems utilize multiple air ducts to distribute conditioned air across different areas effectively.

- In line with the changing regulations in the country, the companies have been investing in introducing new services, mergers, and acquisitions in the market. For instance, in November 2023, Sonepar announced the acquisition of Hydeclim, a French specialist distributing equipment and solutions for AC and air treatment. Following the Group's recent French acquisitions, notably Alliantz (photovoltaics) and CD Sud, this operation would enable Sonepar to expand in the HVAC market and extend its offering to AC and heating installers, particularly in Western and Northern France.

France Commercial HVAC Industry Overview

The France Commercial HVAC market is fragmented, with the presence of major players like Carrier Corporation, Johnson Controls International PLC, Robert Bosch GmbH, System Air AB, Trane Technologies PLC, Flaktgroup Inc., and LG Electronics Inc. Players in the market are adopting strategies such as partnerships, mergers, innovations, investments, and acquisitions to enhance product offerings and gain sustainable competitive advantage.

- April 2024: Mitsubishi Electric bolstered its European HVACR presence by acquiring Aircalo, a prominent air conditioning group based in France. This strategic move enhanced Mitsubishi's portfolio, enabling it to cater to a broader spectrum of hydronic systems. These systems are designed to address the rising market demand for heating and cooling solutions that are both efficient and environmentally friendly, focusing on reducing greenhouse gas emissions.

- November 2023: Phononic, a provider of sustainable solid-state cooling solutions, and Halton, an innovator in HVAC and indoor air quality, introduced a new commercial project: the 'TTAP' Terminal Treatment of Air with Peltier. This advanced installation in a historic 8,500 m2 building in central Paris marked a global milestone as the largest solid-state HVAC platform. Its primary goal is to markedly cut greenhouse gas emissions, all while enhancing the comfort of the building's occupants.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Supportive Government Regulations, Including Incentives for Saving Energy through Tax Credit Programs

- 5.1.2 Increasing Demand For Energy-efficient Devices

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Energy-Efficient Systems

- 5.2.2 Shortage of Skilled Labor

- 5.2.3 Stringent Regulatory Compliance and Safety Standards

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning/Ventilation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End-user Industry

- 6.2.1 Hospitality

- 6.2.2 Commercial Buildings

- 6.2.3 Public Buildings

- 6.2.4 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Carrier Corporation

- 7.1.2 Johnson Controls International PLC

- 7.1.3 Robert Bosch GmbH

- 7.1.4 System Air AB

- 7.1.5 Trane Technologies PLC

- 7.1.6 Flaktgroup Inc.

- 7.1.7 LG Electronics Inc.

- 7.1.8 BDR Thermea Group

- 7.1.9 Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A.

- 7.1.10 Danfoss Inc.

- 7.1.11 Panasonic Corporation