|

市場調査レポート

商品コード

1550310

ドイツの商用HVAC:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Germany Commercial HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツの商用HVAC:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

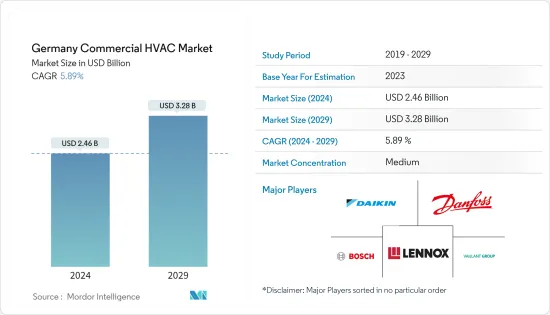

ドイツの商用HVAC市場規模は2024年に24億6,000万米ドルと推定され、2029年には32億8,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは5.89%で成長する見込みです。

主なハイライト

- HVACシステムは、商業ビル内で快適な環境を構築するのに役立っています。特にオフィススペースでは、温度調節や適切な換気を行うだけでなく、従業員の生産性や福利厚生も向上させる。さらに、湿度管理の不備に伴う健康リスクの軽減にも役立っています。

- ドイツにおける商用HVACの拡大は、現在の設備をよりエネルギー効率の高いオプションにアップグレードする傾向の高まりと、税額控除イニシアチブなど省エネを促進する政府規制の実施によって推進されています。

- 例えば、国家政府は、2025年1月1日以降に設置されるすべての暖房システムに再生可能エネルギー源の利用を義務付ける暖房ガイドラインを導入しました。こうした規制措置により、HVAC分野の進歩が促され、ガスボイラーからヒートポンプへの移行ニーズが高まると予想されます。

- 同国では、エネルギー効率の高いソリューションへの嗜好の高まり、高層ビルの増加、既存の商業施設の改築・改装活動の増加により、商用HVAC機器とサービスに対する需要が急増しています。

- さらに、スマートビル制御システムのニーズは、その利点から高まっています。パンデミック(世界的大流行)によって、ビル管理やソリューションへの取り組み方が大きく変化し、新しい手法が迅速に採用されるようになったことは重要です。

- さらに、HVACの進歩に関しては、室内空気品質(IAQ)とカーボンニュートラルの達成に重点が置かれるようになり、その結果、特に教育機関では空気品質制御システムの需要が大幅に増加しています。

- さらに、小売業者数社が同国でのプレゼンス拡大に注力し、市場の成長をさらに後押ししていることから、同市場は高い成長を示すことになると思われます。例えば、C&Aは2024年2月、ドイツ国内に約400店舗を展開する計画だが、戦略的な立地であれば正確な店舗数はある程度自由です。

- エネルギー価格の上昇により、エネルギー効率の高いHVACシステムはコスト削減につながるため、同国では魅力的なものとなりつつあります。しかし、設置に伴う初期費用が高いため、普及が制限され、市場成長の妨げになる可能性があります。

- ドイツの商用HVAC市場は断片化されており、多数のプレーヤーが小さな市場シェアを占めています。同市場で事業を展開する様々なプレーヤーは、顧客からの需要の高まりに対応するため、新製品開発、戦略的提携、買収、事業拡大に注力しており、市場の成長をさらに後押ししています。

- 例えば、2024年1月、アプレオナは、シュトゥットガルト近郊のゲルリンゲンを拠点とする換気・空調会社エアフォーオールの買収を発表しました。この買収により、アプレオナは技術システムのポートフォリオを拡大し、ドイツ南西部での足跡を強化することができます。

- さらに、同国ではデータセンターの拡張が進んでおり、市場の成長をさらに後押ししています。HVACシステムは、あらゆる空間や建物でコンピューター・サーバーの最適な環境を維持するために使用されます。空気の質、温度、湿度を調整することで、インターネットを支えるサーバーのスムーズな動作を保証します。

- さらに、ドイツの商用HVAC市場は、政府の規制やエネルギー効率の高い機器の導入を促進するための新たな取り組みといったマクロ経済要因の影響を強く受けています。例えば、ドイツは2022年9月1日から2023年2月末まで有効な新しい省エネ規制を実施しました。この法律により、公共施設のホールや廊下は摂氏19度以上では暖房されなくなる可能性が高いです。

ドイツの商用HVAC市場動向

HVAC機器が大きな市場シェアを占める

- HVACシステムは、その多くの利点から商業ビルで広く利用されています。そのひとつが、さまざまな理由から商業ビルにおける空調システムの人気が高まっていることです。現代の商業ビルでは、快適な環境を維持するために空調設備が欠かせないです。

- これらのユニットは、冷媒または水冷システムを通じて空気を循環させることで効率的に温度を下げると同時に、空気中の余分な水分を除去します。ショッピングモール、オフィスビル、病院、ホテルなどの商業ビルに対する需要の高まりが、ドイツにおけるHVACシステムの必要性を大きく後押ししています。

- ヒートポンプは、従来の冷暖房システムとは対照的な利点を備えているため、商業施設にとって説得力のある選択肢となります。これらの先進技術は、エネルギー効率の改善、運用コストの削減、環境の持続可能性と脱炭素化の支持において極めて効率的です。

- 商業スペースは、ヒートポンプを統合し、持続可能な取り組みに積極的な役割を果たすことで、二酸化炭素排出量を大幅に削減することができます。これらのシステムを導入することは、生産性を向上させ、コストを削減し、商業施設をより環境に優しく持続可能なエネルギー環境へのシフトの先駆者として確立する戦略的決定です。

- さらに、ドイツのホスピタリティは非常にダイナミックな産業であり、国の経済と社会で重要な役割を果たしています。経済的重要性に加え、ホスピタリティは観光エコシステムにおいても重要な役割を果たしています。

- HVACシステムに関しては、ホテルは他のどの業界よりも多くのニーズと考慮事項を持っています。宿泊客の快適性や信頼性から、全体的な効率やエネルギーの節約まで、業務用ホテルの暖房と換気の複雑なニーズを満たすには、包括的なアプローチが必要です。

- したがって、国内のホテル数の増加は、HVACシステムのニーズを生み出し、市場の成長をさらに促進します。例えば、2024年2月、プレミア・インは4日以内に3つの新拠点を立ち上げ、ドイツでの足跡を増やしました。新たにオープンしたプレミア・イン・ミュンヘン・シティ・オストは、ニュー・ミュンヘン見本市会場の近くに位置し、ダブルルーム74室、ツインルーム37室、トリプルルーム32室、クアドラプルルーム16室、バリアフリールーム2室、プレミア・プラスルーム7室(うち1室はバリアフリー)の合計167室を有します。

- さらに、2023年には、B&Bホテルズグループは全世界で760軒以上のホテルを経営していました。この期間、ドイツには合計182のホテルがあった。

商業ビル部門が大きな市場シェアを占める

- ドイツのHVAC市場における商業ビルセグメントは、オフィスビル、小売店、ショールーム、倉庫などのインフラを構成しています。冷暖房設備は、居住者に快適な環境を提供するため、あらゆる商業ビルにとって不可欠です。

- これらのシステムは多くのオフィスで一般的に使用され、適切な温度と換気条件を提供することで、従業員の生産性と労働条件を向上させ、不適切な湿度レベルによって引き起こされる健康上の問題を防止します。

- 効率的なHVACシステムは、商業施設では非常に重要です。居住者の幸福と生産性は、システムの性能に直接影響されます。さらに、よく機能するHVACシステムは、健康と安全性の懸念を最小限に抑えることができ、その結果、HVACサービスの必要性を高める。

- 国内におけるオフィス/商業スペースの拡大により、HVAC機器とサービスの需要は予測されるタイムライン中に促進されます。例えば、2024年3月、IFZAは、その野心的な世界的拡大戦略の一環として、ドイツに最新の事務所を開設することを宣言しました。この行動は、UAEとドイツ間の強いつながりを強化し、両国間の事業開発と投資の促進を目指すものです。

- 2023年には、ドイツ、英国、フランスが欧州の商業用不動産市場の上位3カ国となり、合計で市場のほぼ半分を占めていました。ドイツだけで、商業用不動産市場規模は約1兆9,000億米ドルを占めています。

- さらに、同国における小売店舗の拡大も市場成長の原動力となっています。空調設備は、小売店舗の繁栄に重要な役割を果たします。快適なショッピングの雰囲気を確立し維持し、顧客とスタッフ双方の健康と快適さを守り、温度に敏感な商品の完全性を維持するために不可欠です。

ドイツの商用HVAC産業の概要

ドイツの商用HVAC市場は断片化されており、複数のプレーヤーで構成されています。市場に参入している企業は、新製品の投入、事業の拡大、戦略的買収や合併、提携、協力関係の締結などにより、市場での存在感を高めようと絶えず努力しています。主なプレーヤーには、ダイキン工業、ROBERT Bosch GmbH、Valliant Group、BDR Thermea Group、Lennox International Inc.、Danfoss A/Sなどがあります。

- 2024年7月、LGグループはフランクフルトにHVAC研究開発ラボを開設すると発表しました。新しい研究所の最初の焦点は、欧州の多様な地域の気候に合わせた高効率の暖房、換気、空調(HVAC)ソリューションの開発です。ヒートポンプ、エネルギー監視システム、エネルギー管理プラットフォームに関する調査と試験が行われます。さらに、同研究所はLGの欧州先進ヒートポンプ研究コンソーシアムと連携し、北欧の厳しい冬でも安定した暖かさを提供できるヒートポンプの開発を目指します。

- 2024年7月、ドーバーの一部門であるSWEPは、低GWP(地球温暖化係数)と自然冷媒用に特別に設計されたSWEP 190シリーズのろう付けプレート式熱交換器を発表しました。このシリーズには単回路と二重回路のオプションがあり、60kWから150kWまでの容量があります。これらの190シリーズユニットは汎用性が高く、さまざまなHVACR環境で蒸発器としても凝縮器としても機能し、R32、R454B、R290冷媒に適合するよう調整されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 国内における商業建築の増加

- エネルギー効率の高い機器に対する需要の増加

- 市場の課題

- エネルギー効率の高いシステムの初期コストの高さ

第6章 市場セグメンテーション

- コンポーネントタイプ別

- HVAC機器

- 暖房機器

- 空調・換気機器

- HVACサービス

- HVAC機器

- エンドユーザー産業別

- ホスピタリティ

- 商業ビル

- 公共施設

- その他

第7章 競合情勢

- 企業プロファイル

- Johnson Controls International PLC

- Midea Group Co., Ltd.

- Daikin Industries, Ltd.

- Robert Bosch GmbH

- Carrier Corporation

- Carrier Corporation

- Valliant Group

- LG Electronics Inc.

- Lennox International Inc.

- BDR Thermea Group

- Panasonic Corporation

- Danfoss A/S

第8章 投資分析

第9章 市場の将来

The Germany Commercial HVAC Market size is estimated at USD 2.46 billion in 2024, and is expected to reach USD 3.28 billion by 2029, growing at a CAGR of 5.89% during the forecast period (2024-2029).

Key Highlights

- HVAC systems are instrumental in establishing comfortable environments within commercial buildings. Specifically, in office spaces, they not only control temperatures and provide proper ventilation but also enhance employee productivity and well-being. Additionally, they help reduce health risks associated with poor humidity control.

- The expansion of the commercial HVAC in Germany is driven by the rising trend of upgrading current equipment to more energy-efficient options and the implementation of government regulations that promote energy conservation, such as tax credit initiatives.

- For instance, the national government has introduced heating guidelines mandating that all heating systems installed post-January 1, 2025, must utilize renewable energy sources. These regulatory measures are anticipated to encourage advancements in the HVAC sector and boost the need for transitioning from gas boilers to heat pumps.

- The country is experiencing a surge in demand for commercial HVAC equipment and services due to a growing preference for energy-efficient solutions, the rise of high-rise buildings, and an increase in renovation and remodeling activities for existing commercial structures.

- Additionally, the need for smart building control systems has increased due to their advantages. It is important to highlight that the pandemic has significantly altered how building management and solutions are approached, with a swift adoption of new practices.

- Furthermore, regarding HVAC advancements, the emphasis has moved towards Indoor Air Quality (IAQ) and achieving carbon neutrality, resulting in a substantial demand for air quality control systems, particularly in educational institutions.

- Moreover, the market will witness high growth as several retailer players focus on expanding their presence in the country, further fueling the market growth. For instance, in February 2024, C&A plans to have approximately 400 stores in Germany in the future, with the exact number being somewhat flexible as long as they are strategically located.

- Energy-efficient HVAC systems are becoming more appealing in the country due to rising energy prices, as they offer cost savings. However, the high initial costs associated with installation may restrict widespread adoption and impede market growth.

- The commercial HVAC market in Germany is fragmented, with a large number of players occupying a small market share. Various players operating in the market are focusing on new product development, strategic partnerships, acquisition, and expansion to meet the growing demand from customers, further supporting market growth.

- For instance, in January 2024, Apleona has announced the acquisition of Air for All, a ventilation and air conditioning company based in Gerlingen near Stuttgart. This deal will enable Apleona to broaden its technical systems portfolio and bolster its footprint in the southwestern region of Germany.

- Furthermore, the country is witnessing the expansion of data centers, further supporting the market growth. HVAC systems are used to maintain the optimal environment for computer servers in any space or building. By regulating the air quality, temperature, and humidity, they ensure the smooth operation of the servers that support the Internet.

- Moreover, the commercial HVAC market in Germany is highly affected by macroeconomic factors such as government regulations and new initiatives to boost the adoption of energy-efficient equipment. For instance, Germany has implemented a new energy-saving regulation that is effective from September 1, 2022, until the end of February 2023. Under this law, public buildings' halls and corridors will likely not be heated above 19 degrees Celsius.

Germany Commercial HVAC Market Trends

HVAC Equipment Holds the Significant Market Share

- HVAC systems are extensively utilized in commercial buildings because of their many advantages. One of these is the increasing popularity of AC systems in commercial buildings for various reasons. Air conditioning units are essential in modern commercial buildings for maintaining a comfortable environment.

- These units efficiently reduce the temperature by circulating air through refrigerant or water-cooled systems while also removing excess moisture from the air. The growing demand for commercial buildings, such as malls, office buildings, hospitals, and hotels, has greatly driven the need for HVAC systems in Germany.

- Heat pumps present a convincing alternative for commercial establishments because of the benefits they provide in contrast to traditional heating and cooling systems. These advanced technologies are remarkably efficient in improving energy efficiency, lowering operational costs, and endorsing environmental sustainability and decarbonization.

- Commercial spaces can significantly decrease their carbon footprint by integrating heat pumps and playing a proactive role in sustainability initiatives. Implementing these systems is a strategic decision that improves productivity, reduces costs, and establishes commercial properties as pioneers in the shift towards a more environmentally friendly and sustainable energy environment.

- Moreover, German hospitality is a highly dynamic industry that plays an important role in the country's economy and society. In addition to its economic importance, hospitality also plays a significant role in the tourism ecosystem.

- When it comes to HVAC systems, hotels have more needs and considerations than almost any other industry. From guest comfort and reliability to overall efficiency and energy savings, meeting the complex needs of commercial hotel heating and ventilation requires a comprehensive approach.

- Thus, the growing number of hotels in the country will create the need for the HVAC system, further propelling the market growth. For instance, in February 2024, Premier Inn increased its footprint in Germany by launching three new locations within four days. The latest addition, Premier Inn Munich City Ost, situated near the New Munich Trade Fair Centre hotel, boasts a total of 167 rooms, comprising 74 double rooms, 37 twin rooms, 32 triple rooms, 16 quadruple rooms, two rooms equipped for disabled guests, and seven Premier Plus rooms, one of which is also accessible.

- Furthermore, in 2023, B&B Hotels Group managed more than 760 hotels globally. During that period, Germany had a total of 182 hotels.

Commercial Building Segment Holds the Significant Market Share

- The commercial building segment in the Germany HVAC market compromises infrastructures, such as office buildings, retail, showrooms, and warehouses, among others. Heating and cooling equipment are essential to any commercial building, as they provide occupants with a comfortable environment.

- These systems are commonly used in many offices to provide appropriate temperature and ventilation conditions, which helps improve employees' productivity and working conditions and prevent health issues caused by improper humidity levels.

- Efficient HVAC systems are crucial in commercial establishments. The occupants' well-being and productivity are directly impacted by the system's performance. Furthermore, a well-functioning HVAC system can minimize health and safety concerns, consequently driving up the need for HVAC services.

- The rising expansion of office/commercial space in the country will propel the demand for HVAC equipment and services during the projected timeline. For instance, in March 2024, IFZA declared the inauguration of its most recent office in Germany as a component of its ambitious global expansion strategies. This action enhances the strong connections between the UAE and Germany and seeks to promote business development and investments between the two nations.

- In 2023, Germany, the UK, and France were the top three European commercial real estate countries, collectively representing nearly half of the market. Germany alone accounted for approximately USD 1.9 trillion in commercial real estate market size.

- Furthermore, the rising expansion of retail outlets in the country will also drive market growth. HVAC plays an important role in the prosperity of a retail establishment. They are essential for establishing and upholding a pleasant shopping atmosphere, safeguarding the health and comfort of both customers and staff and preserving the integrity of items sensitive to temperature.

Germany Commercial HVAC Industry Overview

The Germany commercial HVAC market is fragmented and consists of several players. Companies in the market continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic acquisition and mergers, partnerships, and collaborations. Some of the major players are Daikin Industries Ltd, ROBERT Bosch GmbH, Valliant Group, BDR Thermea Group, Lennox International Inc.,Danfoss A/S, and many more.

- In July 2024, LG Group announced to open HVAC R&D lab in Frankfurt. The initial focus of the new laboratory is the development of high-efficiency heating, ventilation, and air conditioning (HVAC) solutions tailored to the diverse local climates of Europe. Research and testing will be conducted on heat pumps, energy monitoring systems, and energy management platforms. Additionally, the lab will work in partnership with LG's European Consortium for Advanced Heat Pump Research, with the goal of creating heat pumps capable of delivering consistent warmth during the severe winters of Northern Europe.

- In July 2024, SWEP, a division of Dover, has introduced the SWEP 190 series of brazed plate heat exchangers, specifically engineered for low-global warming potential (GWP) and natural refrigerants. This range includes single-circuit and dual-circuit options, with a capacity ranging from 60kW to 150kW. These 190 series units are versatile, serving as both evaporators and condensers in various HVACR settings, and are tailored for compatibility with R32, R454B, and R290 refrigerants.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Commercial Construction in the country

- 5.1.2 Increasing Demand For Energy Efficient Devices

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Energy Efficient Systems

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning /Ventillation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End User Industry

- 6.2.1 Hospitality

- 6.2.2 Commercial Buildings

- 6.2.3 Public Buildings

- 6.2.4 Others

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Johnson Controls International PLC

- 7.1.2 Midea Group Co., Ltd.

- 7.1.3 Daikin Industries, Ltd.

- 7.1.4 Robert Bosch GmbH

- 7.1.5 Carrier Corporation

- 7.1.6 Carrier Corporation

- 7.1.7 Valliant Group

- 7.1.8 LG Electronics Inc.

- 7.1.9 Lennox International Inc.

- 7.1.10 BDR Thermea Group

- 7.1.11 Panasonic Corporation

- 7.1.12 Danfoss A/S