アジア太平洋地域の商用HVAC:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

Asia Pacific Commercial HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549964

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

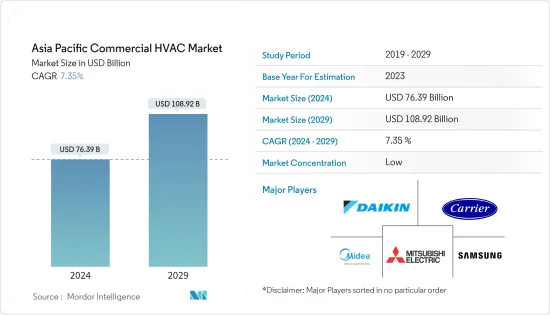

アジア太平洋地域の商用HVAC市場規模は2024年に763億9,000万米ドルと推定され、2029年には1,089億2,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは7.35%で成長する見込みです。

主なハイライト

- アジア太平洋地域の商用HVAC市場は、新興経済諸国における商業用建設活動への投資の増加により、堅調に成長すると予測されます。加えて、同地域の力強い経済成長、都市化、消費者市場の拡大が商業空間の需要を牽引しており、革新的で高品質なHVAC機器とサービスへの需要が高まると予測されます。

- 同地域のHVAC機器市場が予測期間中に商業産業で成長する重要な促進要因には、エネルギー効率の高い持続可能な技術に対する需要の急増が含まれます。IEAによると、東南アジアの電力消費量は2040年までに倍増すると予想されており、空調システムは全体的な電力需要およびピーク電力需要に大きく寄与するものとなっています。IEAの調査は、この地域で増大するエネルギー需要を満たすための持続可能な解決策を見出すことが急務であることを強調しています。

- いくつかの地域政府は、持続可能性とエネルギー効率を遵守する規則や規制を市場に設けており、これが市場の技術開発を促進しています。例えば、2024年2月、パナソニックは2024年版エアコンのラインアップを発表し、Matter対応のルームエアコン製品群を大きくフィーチャーしました。Matterは、スマート家電のための最先端の接続規格で、ブランドにとらわれないモバイルアプリによるシームレスな相互運用性を促進します。パナソニックは、このプロトコルに準拠したACをインドで初めて発売したパイオニアです。パナソニックは、1トン、1.5トン、2トンにわたる60機種の多様なラインナップを取り揃え、全機種にMatterテクノロジーを搭載しています。

- 商業空間の暖房、換気、空調の分野は変化しています。冷暖房ユニットはこれまで以上に小型化、コンパクト化、高効率化しています。しかし、メーカーやサービス・プロバイダーは、こうした技術開発に遅れをとらないようにしなければならないです。より熟練した労働者の必要性は、いくつかの地域企業にとって重要な問題です。HVACサービスは、必要な機器を設置する人とは別に、プロセス全体と終了段階を監督するスーパーバイザーが必要であり、時間がかかり、興ざめすることが多いです。複数のプロジェクトを同時に処理する場合、チーム管理は本当に難しいです。

- この地域には、業務用セグメントのHVACメーカーやサービスプロバイダーがいくつかあります。これらのメーカーは、競争力を維持するために国内製造施設を設立し、市場での存在感を高めることに注力しています。例えば、日本のダイキン工業は、2025年までに海外で販売されるメイド・イン・インディア製品を3倍近くに増やすため、インドを輸出の中心拠点にすることを目指しています。ダイキンはインドに新工場を建設し、ルームエアコンとコンプレッサーを主要部品としています。同社はまた、2025年に100市場に向けてメイド・イン・インディアのエアコン製品の輸出を推進します。

- ロシアとウクライナの紛争は、地域のサプライチェーンに大きな問題を引き起こしています。COVID-19の大流行後、この地域はロジスティクスとサプライチェーンの回復に取り組んでいたが、この紛争は新たな市場問題を引き起こしました。商品輸出のような既存のサプライチェーン問題を悪化させる一因となっています。一方、日本の工場はウクライナからの原材料や部品の不足の影響を直接受けています。

アジア太平洋地域の商用HVAC市場動向

商業ビルセグメントが大きなシェアを占める見込み

- HVACシステムは、レストラン、病院、学校、ホテル、オフィスビルなど、あらゆる商業ビルにおいて、居住者に快適な環境を提供するために不可欠です。例えば、HVACシステムは多くのオフィスで一般的に使用されており、適切な温度と換気条件を提供することで、従業員の生産性と労働条件を向上させ、不適切な湿度レベルに起因する健康問題を防止するのに役立っています。

- この地域の商業セクターのHVAC市場は、自動化システムからグリーンテクノロジーやスマートテクノロジーに至るまで、商用HVAC市場の方向性を決定する上で極めて重要であると予測されるいくつかの動向により、予測期間を通じて増加すると予測されています。環境に優しくエネルギー効率の高いHVACシステムに対する需要の高まりが、同分野の拡大を牽引しています。商業建築部門の発展は、ヒートポンプ、AC、エアハンドラー、その他のHVAC機器の台頭に重要な役割を果たしています。

- 例えば、小売店、教育施設、中堅病院などの低層ビル向けの業務用ルーフトップ・エアコン、ヒートポンプ、温風システムは、RTU効率を高め、エネルギー使用量と無駄を削減するために、いくつかの規則によって設計が変更されています。いくつかのメーカーがフロン(クロロフルオロカーボン)やHCFC(ハイドロクロロフルオロカーボン)を段階的に廃止しているため、時代遅れのモデルを置き換えるソリューションへの需要が高まり、ヒートポンプの使用が増加しています。

- 商業部門におけるエネルギー消費は、いくつかの地域諸国で徐々に増加しており、エネルギー効率の高いHVAC製品の革新に向けた市場の成長を後押ししています。例えば中国では、商業・工業部門を含む第二次産業部門の電力消費量が6,070テラワット時を占めています。

中国は市場の著しい成長が期待される

- この地域における商用HVAC機器の需要は、過去数年にわたって大きな成長機会を目の当たりにしてきました。中国は、データセンター数の急激な増加や、エネルギー効率の高いインフラを支援する政府の政策により、データセンターの冷却に不可欠な市場の1つとなっています。Cloudsceneによると、中国のデータセンター数は448で、アジアで最も多いです。

- 2024年3月、中国工業情報化部(MIIT)の関係者は、中国がインターネット・データセンターの試験的開放に向けて準備を進めていると発表しました。中国が新産業化を推し進めるなか、改革を深化させ、開放の範囲を広げることは不可欠です。注目すべきは、中国が製造業への外資規制の完全撤廃を宣言したことです。これと並行して、中国情報通信部(MIIT)は、インターネット・データセンターに特化した付加価値通信サービスを開放することで、水面下で試験的な準備を進めています。この拡大は、調査対象市場のベンダーにとって大きなチャンスとなります。

- 中国の建設業界は、持続可能な建設政策と過去数年間のサービス主導型経済へのシフトにより、大規模な成長を目の当たりにしてきました。大規模なインフラ・プロジェクトへの投資は、成長を後押しする中国政府の戦略の重要な一部となっています。EPRAによると、2023年12月時点で、中国の商業用不動産市場規模はアジア太平洋地域全体を合わせた5兆6,000億米ドルにほぼ匹敵します。

- 商業ビルの増加は国のエネルギー消費に直接影響すると推定されるため、中国政府はエネルギー管理に真剣に取り組んでいます。省エネ法と再生可能エネルギー法という2つの法律が、建物のエネルギーシステムとHVAC産業に対する主なガイドラインを提供しています。

アジア太平洋地域の商用HVAC産業の概要

アジア太平洋地域の商用HVAC市場は競争が激しく、世界的・地域的なプレーヤーが複数存在します。プレーヤーは、商業分野におけるHVAC市場の急増する需要を満たすために、技術革新、提携、合併、買収などの戦略的イニシアティブを重視しています。グローバル企業の他に、地域企業は高度な技術を備えたHVAC機器とサービスを競争力のある価格で提供しています。主な市場プレーヤーには、ダイキン工業、Carrier Corporation、Midea Group、三菱電機、Samsung HVAC LLCが含まれます。

- 2024年1月Carrierは、健康的な室内環境と高効率空気濾過の要件を満たすカスタムソリューションを提供することで、商業ビルの多様なニーズに対応するエアハンドリングユニット(AHU)とファンコイルユニット(FCU)の製品群で、インド製のHVAC製品を拡大しました。FCUとAHUへの拡張は、インドにおける50年以上の製造プレゼンスを確認するものです。

- 2023年8月ダイキン工業は、茨城県つくばみらい市に土地を取得し、エアコンの新たな生産拠点を設立することを決定。同社は、関東地方に新工場を立地することで、日本国内における空調製品の供給を最適化し、さらなる拡大を目指します。ダイキンにとって関東地方初のエアコン工場となります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- エネルギー効率と持続可能技術に対する需要の増加

- 地域における商業用不動産への投資の増加

- 市場抑制要因

- 設置や修理のような日常作業を行う熟練労働力と訓練の不足

第6章 市場セグメンテーション

- コンポーネントタイプ別

- HVAC機器

- 暖房機器

- 空調/換気機器

- HVACサービス

- HVAC機器

- エンドユーザー産業別

- ホスピタリティ

- 商業ビル

- 公共施設

- その他エンドユーザー産業

- 国別

- 中国

- インド

- 日本

第7章 競合情勢

- 企業プロファイル

- Daikin Industries Ltd

- Carrier Corporation

- Johnson Controls International PLC

- Mitsubishi Electric

- Trane Technologies

- Samsung HVAC LLC

- LG Electronics

- Panasonic Corporation

- Lennox International Inc.

- Midea Group Co. Ltd

第8章 投資分析

第9章 市場の将来

目次

The Asia Pacific Commercial HVAC Market size is estimated at USD 76.39 billion in 2024, and is expected to reach USD 108.92 billion by 2029, growing at a CAGR of 7.35% during the forecast period (2024-2029).

Key Highlights

- The APAC commercial HVAC market is predicted to rise steadily due to increasing investments in commercial construction activity in developing economies in the region. In addition, the region's strong economic growth, urbanization, and expanding consumer market drive demand for commercial spaces, which is expected to increase the demand for innovative and high-quality HVAC equipment and services.

- Significant drivers of the regional HVAC equipment market's growth in the commercial industry over the forecast period include the surging demand for energy-efficient and sustainable technologies. According to the IEA, electricity consumption in Southeast Asia is expected to double by 2040, with air conditioning systems becoming a significant contributor to overall and peak electricity requirements. The study by the IEA highlights the urgent need to find sustainable solutions for meeting growing energy demand in the region.

- Several regional governments have established rules and regulations in the market that adhere to sustainability and energy efficiency, which expedites technological developments in the market. For instance, in February 2024, Panasonic unveiled its 2024 air conditioner lineup, prominently featuring its range of Matter-enabled room ACs. Matter, a cutting-edge connectivity standard for smart home appliances, facilitates seamless interoperability via brand-agnostic mobile apps. This move positions Panasonic as the pioneer in India, being the first to introduce ACs adhering to this protocol. The brand's launch encompasses a diverse portfolio, with 60 models spanning 1.0-ton, 1.5-ton, and 2.0-ton variants, all equipped with Matter technology.

- The commercial space's heating, ventilation, and air conditioning sectors are changing. The cooling and heating units are smaller, more compact, and more efficient than ever. However, manufacturers and service providers must keep pace with these technological developments. The need for more skilled workers is a significant problem for several regional companies. The HVAC services are often time-consuming and entertaining and need a supervisor to supervise the entire process and closing phase, apart from those installing the necessary equipment. Team management is a real challenge when handling several projects simultaneously.

- The region is home to several HVAC manufacturers and service providers in the commercial segment. They focus on enhancing their market presence by establishing domestic manufacturing facilities to remain competitive. For instance, Japan's Daikin Industries aims to make India a central export hub to nearly triple the Made in India products sold abroad by 2025. Daikin has built a new plant in India, making room air conditioners and compressors a key component. The company will also pursue exports of Made in India aircon products to 100 markets in 2025.

- The conflict between Russia and Ukraine has caused significant problems with regional supply chains. After the COVID-19 pandemic, the region was recovering logistics and supply chains, and this conflict created new market problems. It has contributed to exacerbating existing supply chain problems like commodity exports. On the other hand, Japanese factories are directly affected by the lack of raw materials and components from Ukraine.

Asia Pacific Commercial HVAC Market Trends

Commercial Buildings Segment is Expected to Hold Significant Share

- HVAC systems are essential to any commercial building, such as restaurants, hospitals, schools, hotels, office buildings, etc., to provide occupants with a comfortable environment. For instance, HVAC systems are commonly used in many offices to provide appropriate temperature and ventilation conditions, which helps improve employee productivity and working conditions and prevent health issues caused by improper humidity levels.

- The regional commercial sector's HVAC market is predicted to increase throughout the forecast period owing to several trends, from automated systems to green and smart technology, which are anticipated to be crucial in determining the direction of the commercial HVAC market. The increasing demand for environmentally friendly and energy-efficient HVAC systems drives the segment's expansion. The development of the commercial construction sector plays a significant role in the rise of heat pumps, ACs, air handlers, and other HVAC equipment.

- For instance, several rules have altered the engineering of commercial rooftop air conditioners, heat pumps, and warm-air systems for low-rise buildings like retail outlets, educational facilities, and mid-level hospitals to increase RTU efficiency and reduce energy use and waste. The phasing out of CFC (chlorofluorocarbon) and HCFC (hydrochlorofluorocarbon) by several manufacturers has increased the demand for solutions to replace outdated models, which has increased the use of heat pumps.

- Energy consumption in the commercial sectors is gradually increasing in several regional countries, fueling the market's growth to innovate energy-efficient HVAC products. For instance, in China, the secondary sector, which includes commercial and industrial sectors, accounted for 6,070 terawatt hours of electricity consumption.

China is Expected to Witness Significant Growth in the Market

- The demand for commercial HVAC equipment in the region has witnessed significant growth opportunities over the past few years. China is one of the essential markets for data center cooling due to the exponential growth in the number of data centers and the government's policies to support more energy-efficient infrastructure in the country. According to Cloudscene, China has the most significant number of data centers in Asia, with 448.

- In March 2024, an official from China's Ministry of Industry and Information Technology (MIIT) announced that China is gearing up to pilot the opening-up of internet data centers. As China pushes for new industrialization, it is imperative to deepen reforms and broaden its scope of opening-up. Notably, China has made headlines by declaring a complete removal of restrictions on foreign investments in manufacturing. In tandem, the MIIT is gearing up to test the waters by opening up value-added telecommunications services, with a specific focus on internet data centers. This expansion offers a massive opportunity for the vendors in the market studied.

- The construction industry in China has witnessed massive growth due to sustainable construction policies and a shift toward a service-led economy over the past few years. Investing in large-scale infrastructure projects has been a vital part of the Chinese government's strategy to boost growth. According to EPRA, as of December 2023, China's commercial real estate market was worth nearly as much as all Asia-Pacific combined, which was USD 5.6 trillion.

- The increase in commercial buildings is estimated to affect national energy consumption directly, which is why the Chinese government has taken energy management seriously. Two laws, the Energy Saving Law and Renewable Energy Law, provide the main guidelines for building energy systems and HVAC industries.

Asia Pacific Commercial HVAC Industry Overview

The Asia-Pacific commercial HVAC market is highly competitive, with several global and regional players. The players are emphasizing strategic initiatives like innovations, partnerships, mergers, and acquisitions to fulfill the surging demand of the HVAC market in the commercial sectors. Besides global players, the regional players offer HVAC equipment and services with highly advanced technologies at competitive prices. The key market players include Daikin Industries Ltd, Carrier Corporation, Midea Group Co. Ltd, Mitsubishi Electric, and Samsung HVAC LLC.

- January 2024: Carrier expanded its HVAC products made in India with a range of air handling units (AHUs) and fan coil units (FCUs) that meet the diverse needs of commercial buildings by providing custom solutions for healthy indoor environments and high-efficiency air filtration requirements. The expansion to FCUs and AHUs affirms more than a five-decade manufacturing presence in India.

- August 2023: Daikin Industries Ltd decided to acquire land in Tsukubamirai City, Ibaraki Prefecture, Japan, to establish a new production base for air conditioners. The company intends to optimize the domestic supply of air conditioning products in Japan to expand further when it locates its new factory in the Kanto region. It will be Daikin's first air conditioning plant in the Kanto region.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Energy Efficiency and Sustainable Technology

- 5.1.2 Increasing Investment Toward Commercial Real-Estate in the Region

- 5.2 Market Restraints

- 5.2.1 Lack of Skilled Workforce and Training to Perform Routine Tasks like Installations and Repair

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning/Ventilation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End-user Industry

- 6.2.1 Hospitality

- 6.2.2 Commercial Buildings

- 6.2.3 Public Buildings

- 6.2.4 Other End-user Industries

- 6.3 By Country

- 6.3.1 China

- 6.3.2 India

- 6.3.3 Japan

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Daikin Industries Ltd

- 7.1.2 Carrier Corporation

- 7.1.3 Johnson Controls International PLC

- 7.1.4 Mitsubishi Electric

- 7.1.5 Trane Technologies

- 7.1.6 Samsung HVAC LLC

- 7.1.7 LG Electronics

- 7.1.8 Panasonic Corporation

- 7.1.9 Lennox International Inc.

- 7.1.10 Midea Group Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日