|

市場調査レポート

商品コード

1550306

英国の業務用HVAC:市場シェア分析、産業動向、成長予測(2024年~2029年)United Kingdom Commercial HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の業務用HVAC:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

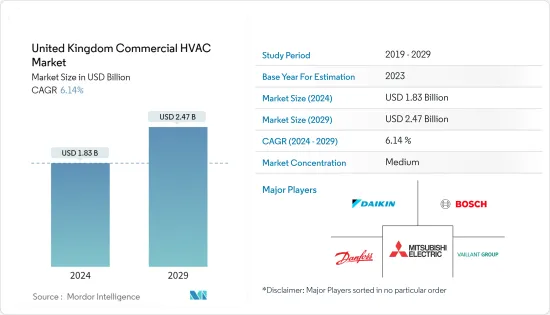

英国の業務用HVAC市場規模は2024年に18億3,000万米ドルと推定され、2029年には24億7,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは6.14%で成長すると予測されます。

主なハイライト

- 英国では、主に空調システムの普及に後押しされ、業務用分野でHVAC機器の需要が急増しています。このような需要の増加は、気候変動、都市化、ライフスタイルの進化、技術の進歩といった様々な要因が重なっているためです。さらに、商業スペースの建設活動の活発化、グリーンビルディングへの取り組みに対する政府の支援、都市化の急速な進展が市場をさらに押し上げています。

- 各国政府は厳しい規制の導入に前向きであるため、ヒートポンプの導入が義務付けられ、市場調査にプラスの影響を与えています。例えば欧州連合(EU)は、EUの目標に沿って2030年までに6,000万台以上のヒートポンプを設置すると発表しており、これにより2030年までに建物内のガス需要を2022年比で40%削減し、エネルギー輸入額を600億ユーロ(653億1,000万米ドル)削減するとしています。

- 建設業界の隆盛は、ショッピングセンター、複合商業施設、駐車場、ホテルなどの商業施設に冷暖房目的で設置されるエアコンの大きなビジネスチャンスを引き出しています。

- 不動産デベロッパーのランドセックは、2023年1月にフォージ・バンクサイドを完成させました。この商業オフィス開発は、新たに建設された9階建てのビル2棟で構成され、合わせて約14万平方フィートの内部空間を提供しています。特筆すべきことに、フォージは、UKグリーンビルディング評議会(UKGBC)のネット・ゼロ・カーボン・ビルディングの枠組みに準拠した最初の商業オフィスプロジェクトです。政府の方針は英国のHVAC市場に影響を与え、2050年までに二酸化炭素排出量を大幅に削減するという欧州連合の野心的な目標に裏付けがあります。

- HVAC業界は、AIとIoTの高度な統合により先端技術へとシフトしています。さらに、人工知能(AI)もHVACシステムにおける注目すべき動向です。AIを搭載した冷暖房技術は、室内温度、設定温度、外気温などの要素を自動的に管理することができます。主要なHVACシステムプロバイダーは、最新の先端技術を取り入れており、これが今後数年間の市場成長を後押しすると思われます。

- 世界のメーカーは、エネルギー効率を重要な関心事の一つとして重視しています。ダイキン、Carrier、Robert Bosch Gmbh、Danfoss A/s、Mitsubishi Electric Europe Bv、Lennox International Inc.などの多くのメーカーは、すでにエネルギー効率の高いHVAC製品の発売を開始しており、そのため彼らは市場の価格決定者となっています。そのため、比較的小規模なプレーヤーは、これらの製品に盛り込まれた技術革新のレベルに見合う資金力を持たず、低価格帯で製品を販売せざるを得ないです。競争の激化は、今後数年間の成長を制限すると思われます。

- さらに、現在進行中のロシアとウクライナの戦争は、政治的・経済的に不安定な状況をもたらし、その結果、同地域内の消費者の購買力が低下しています。軍事衝突は、英国の日本、韓国、台湾との貿易を混乱させる可能性があり、これらすべてが潜在的な米中敵対行為に巻き込まれる可能性があります。いくつかの消費財は品不足に直面する可能性があり、英国の製造業は必需品の不足により苦戦を強いられるかもしれないです。製造品や中間投入物の深刻な不足は、英国および世界の大幅なインフレ高騰の引き金となる可能性があります。

英国の業務用HVAC市場の動向

暖房機器は大幅なCAGRで成長する見込み

- 暖房機器は今後数年間、商業ビルで牽引力を増すと思われます。商業分野では、暖房機器はレストラン、住宅ロッジ、複合ショッピング施設、オフィスなど様々な場面で利用されています。商業施設ではヒートポンプが好まれ、従来の冷暖房システムを上回る利点を提供しています。これらの先進技術は、エネルギー効率を高め、運用コストを削減し、環境の持続可能性と脱炭素化への取り組みをサポートします。

- 商業施設は、ヒートポンプを採用することで、二酸化炭素排出量を削減し、持続可能性を高めることができます。この戦略的な動きは、効率を改善しコストを削減するだけでなく、より持続可能なエネルギー環境への移行におけるリーダーとしての地位を確立します。

- 業務用ヒートポンプは、さまざまなタイプの物件で多様な用途に使用され、多くの役割を果たしています。業務用ヒートポンプの導入急増は、主に政府のイニシアティブの高まりによって大きく後押しされることになりそうです。例えば、英国政府はヒートポンプ技術を、従来の化石燃料ボイラーに代わる環境に優しい商業施設として積極的に推進しています。この移行をスムーズにするため、英国は企業がヒートポンプシステムに移行するのを支援するよう設計されたさまざまなプログラムを提供しています。

- 2024年5月、MCSは英国における空気熱源ヒートポンプの設置台数4,849台を報告し、過去2番目に多い月となった。この記録は2022年3月に抜かれ、助成金支給期限に間に合わせるために設置台数が急増し、合計6,335台となった。2024年5月、MCS認証を受けた空気熱源ヒートポンプの設置台数は、2023年の同時期から64%増と大幅に増加しました。特に2023年は、年間3万6,799台の空気熱源ヒートポンプが設置され、過去最高を記録しました。

- 政府の取り組みと補助金がこのセグメントの成長を後押ししています。同時に、継続的な研究開発の努力により、効率の向上を誇り、エンドユーザーの特定の要件に対応する最先端のヒートポンプ技術が生み出されています。メーカーは、消費者の要求を満たす経済的なヒートポンプを熱心に設計しています。

商業ビルのエンドユーザーが大きな市場シェアを占める

- 商業ビル分野は、継続的な建設活動や空調、ヒートポンプ、その他のHVACシステムの需要増加により、今後数年間で大きな成長が見込まれます。

- 2023年の課題後、商業用不動産セクターは投資活動の復活を経験しています。2023年の英国の総取引額は、10年平均の534億ユーロ(676億米ドル)に大きく遅れをとった。しかし、2023年第4四半期には回復が見られ、前四半期比14%増となった。この好傾向は2024年に入っても続いており、国全体で活動量と取引量の両方が増加しています。この成長は、地政学的な不確実性が続いているにもかかわらず、インフレ圧力の緩和や将来の金利引き下げの可能性にも助けられて生じています。

- 主要企業は、商業ビル分野での暖房システム需要に対応する様々な製品の導入に絶えず投資しています。例えば、ダイキンは最近、2023年11月に、2024年前半に発売予定の2つのVRV 51ヒートポンプシステムに関する情報を開示しました。これらの新システム、すなわちMini-VRVとTop-blowシリーズは、商業ビルにおける脱炭素化の需要の高まりに対応するように設計されています。ダイキンは、エネルギー効率の高い、より持続可能なソリューションへのシフトをサポートするため、製品ポートフォリオをさらに強化しています。このようなベンダーの活動は、市場の潜在力を高めると予想されます。

- ダクトレス・ミニスプリット・エアコンの一般的な商業用途には、空調設備のない倉庫に併設されたオフィススペースや、商業ビルのロビーなどがあります。さらに、ミニスプリットはサイズが小さく、ゾーニングや暖房、個別の冷房室にも柔軟に対応できます。このような利点が、商業分野での市場の成長を促進すると思われます。

- HVACシステム・アプリケーションはここ数年、商業ビル所有者の間で人気が高まっています。商業用不動産市場は急成長しており、HVACシステムに大きなビジネスチャンスをもたらすと期待されています。欧州公共不動産協会(The European Public Real Estate Association)によると、欧州の商業用不動産市場は2023年に9兆米ドルを超えると予測されており、ドイツ、英国、フランスを合わせると市場全体の50%以上を占める。

- ダクトレス・ミニスプリット・エアコンは、商業ビルにも応用できる可能性があります。商業ビルは大規模で、冷暖房に大量のエネルギーを必要とすることが多いが、ダクトが使えないという問題があります。これらのシステムは、暖房システムやセントラル・エアコンのための配電ダクトの敷設や設置が不可能な、小規模なアパートや部屋の増築にも適した選択肢です。このような利点により、商業スペースにおけるダクトレス・ミニスプリット・エアコンの採用が増加すると予想されます。

英国の商業用HVAC産業の概要

英国の商業用HVAC市場は細分化されており、競争が激しく、有力企業が複数存在します。市場参入企業は、海外の消費者基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的な共同イニシアティブを活用しています。シーメンスAG、ハネウェル・インターナショナル、ダイキン工業、三菱電機欧州BVなど、同市場で事業を展開する企業は、生産能力を強化するため、HVAC技術に取り組む新興企業を買収しています。

2024年3月、三菱電機欧州BVは、住宅用空対水ヒートポンプという形で最新の製品を発表しました。同社のHydrolution EZYモノブロックは、-25℃まで下がる屋外条件でも60℃まで達する温水を生成する能力で際立っています。このモデルには2つの出力オプションがあります:10 kWと14 kWがあります。

2023年12月、ダイキン工業株式会社は、新しい住宅用空気対空気ヒートポンプシリーズであるNepuraの導入を発表しました。この製品シリーズにより、ダイキン欧州は、30℃までの温度で動作し、最高A+++の暖房効率値を達成する信頼性の高い暖房ソリューションを提供することを目指しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 主要新興国における商業建築の増加

- エネルギー効率の高いデバイスに対する需要の増加

- 市場の課題

- エネルギー効率の高いシステムの初期コストの高さ

第6章 市場セグメンテーション

- 部品タイプ別

- HVAC機器

- 暖房機器

- 空調・換気機器

- HVACサービス

- HVAC機器

- エンドユーザー産業別

- ホスピタリティ

- 商業ビル

- 公共施設

- その他

第7章 競合情勢

- 企業プロファイル

- Johnson Controls International PLC

- Midea Group Co., Ltd.

- Daikin Industries, Ltd.

- Robert Bosch GmbH

- Carrier Corporation

- LG Electronics Inc.

- Lennox International Inc

- BDR Thermea Group

- Panasonic Corporation

- Danfoss A/S

第8章 投資分析

第9章 市場の将来

The United Kingdom Commercial HVAC Market size is estimated at USD 1.83 billion in 2024, and is expected to reach USD 2.47 billion by 2029, growing at a CAGR of 6.14% during the forecast period (2024-2029).

Key Highlights

- The United Kingdom is witnessing a surge in demand for HVAC equipment in the commercial sector, primarily fueled by the increasing embrace of air conditioning systems. This uptick can be attributed to a confluence of factors: climate change, urbanization, evolving lifestyles, and technological advancements. Moreover, the market is further bolstered by enhanced commercial space construction activities, governmental support for green building endeavors, and the swift pace of urbanization.

- Governments are looking forward to introducing stringent regulations, thus mandating the incorporation of heat pumps and positively impacting the market studied. For instance, the European Union also announced the installation of 60 million more heat pumps by 2030, in line with the EU targets, which would reduce the gas demand in buildings by 40% by 2030 compared to 2022 and decrease its energy import bill by EUR 60 billion (USD 65.31 billion).

- The flourishing construction industry has unlocked substantial business opportunities for air conditioners installed for heating and cooling purposes in commercial facilities such as shopping centers, commercial complexes, parking units, and hotels.

- Landsec, a property developer, completed the Forge Bankside in January 2023. This commercial office development consists of two newly constructed 9-story buildings, offering a combined internal space of approximately 140,000 sq. ft. Notably, the Forge is the first commercial office project to comply with the UK Green Building Council's (UKGBC) net-zero carbon buildings framework. Governmental policies influence the HVAC market in the UK and find support in the European Union's ambitious target to slash carbon emissions significantly by 2050.

- The HVAC Industry is shifting towards advanced technologies due to a high level of AI and IoT integrations. Further, Artificial Intelligence (AI) is also a noteworthy trend in HVAC Systems. AI-powered heating and cooling technologies can automatically manage factors such as indoor temperature, set temperatures, outdoor temperature, and others. The leading HVAC system providers are incorporating the latest advanced technologies, which will boost the market growth in the coming years.

- Global manufacturers are focusing on energy efficiency as one of their key concerns. Many players, such as Daikin, Carrier, Robert Bosch Gmbh, Danfoss A/s, Mitsubishi Electric Europe Bv, and Lennox International Inc., have already started launching energy-efficient HVAC products, and hence, they have become price setters in the market. Thus, comparatively smaller players lack the financial capacity to match the level of technological innovations incorporated in these products, and they have to sell their products at a lower price point. Growing competition will limit the growth in coming years.

- Moreover, the ongoing war between Russia and Ukraine has brought instability in a political and economic situation that results in a decline in consumer purchasing power within the region. Military conflicts could disrupt the UK's trade with Japan, South Korea, and Taiwan, all of which might find themselves entangled in potential Sino-U.S. hostilities. Several consumer goods could face shortages, and UK manufacturing might struggle due to a lack of essential supplies. Severe shortages of manufactured goods and intermediate inputs could trigger a significant inflation surge in the UK and globally.

United Kingdom Commercial HVAC Market Trends

Heating Equipment is Expected to Grow with Significant CAGR

- Heating equipment will gain traction in commercial buildings in the coming years. In the commercial sector, heating equipment is utilized in various settings, including restaurants, residential lodges, shopping complexes, and offices. Heat pumps are preferred for commercial properties, offering advantages that exceed those of traditional heating and cooling systems. These advanced technologies enhance energy efficiency, reduce operational costs, and support environmental sustainability and decarbonization efforts.

- Commercial properties can reduce carbon footprint and enhance sustainability by adopting heat pumps. This strategic move not only improves efficiency and reduces costs but also establishes these properties as leaders in the transition to a more sustainable energy landscape.

- Commercial heat pumps find diverse applications in various property types, serving many purposes. The surge in commercial heat pump adoption is set to receive a significant push, primarily driven by heightened government initiatives. For instance, the UK government actively promotes heat pump technology as a green alternative to traditional fossil fuel boilers in commercial setups. To smoothen this shift, the UK offers an array of programs designed to aid companies in transitioning to heat pump systems.

- In May 2024, MCS reported 4,849 installations of air-sourced heat pumps in the United Kingdom, marking the second-highest month on record. The record was surpassed by March 2022, which saw a surge in installations to meet a grant funding deadline, totaling 6,335 units. In May 2024, installations of MCS-certified air-sourced heat pumps saw a significant 64% increase from the same period in 2023. Notably, 2023 marked a record high, with 36,799 air-sourced heat pumps installed yearly.

- Government initiatives and subsidies boost the segment's growth. Concurrently, continuous research and development endeavors are yielding cutting-edge heat pump technologies that boast enhanced efficiency and cater to the specific requirements of end users. Manufacturers are diligently designing economical heat pumps to fulfill the requirements of consumers.

Commercial Buildings End-Users Hold Signficant Market Share

- The commercial buildings segment is expected to witness significant growth in coming years owing to ongoing construction activities and increasing demand for air conditioning, heat pumps, and other HVAC systems.

- After a challenging 2023, the commercial property sector is experiencing a resurgence in investment activity. In 2023, the UK's total deal volume significantly lagged behind the 10-year average of EUR 53.4 billion (USD 67.6 billion). However, the fourth quarter of 2023 indicated a recovery, with a 14% increase quarter-on-quarter. This positive trend has continued into 2024, with both activity and deal volumes rising across the country. This growth is occurring despite ongoing geopolitical uncertainties, aided by easing inflationary pressures and the potential for future interest rate cuts.

- Leading companies are constantly investing in introducing various products catering to the demand for these heating systems in the commercial buildings segment. For instance, in November 2023, Daikin recently disclosed information regarding two upcoming VRV 51) heat pump systems scheduled to be released in the first half of 2024. These new systems, namely the Mini-VRV and the Top-blow series, are designed to cater to the growing demand for decarbonization in commercial buildings. Daikin is further enhancing its product portfolio to support the shift toward energy-efficient and more sustainable solutions. Such vendor activities are expected to increase the market's potential.

- The common commercial applications of Ductless mini-split air conditioners include office spaces attached to unconditioned warehouses or in the lobbies of commercial buildings. Moreover, mini-splits are smaller in size and are flexible for zoning or heating and individual cooling rooms. Such benefits are likely to propel the market's growth within the commercial segment.

- HVAC system applications have been growing in popularity among commercial building owners for the past few years. The commercial real estate market grows at a rapid rate, which is expected to create significant opportunities for HVAC systems. The European commercial real estate market was projected at over USD 9 trillion in 2023, according to The European Public Real Estate Association, with Germany, the UK, and France together accounting for more than 50% of the total market.

- Ductless mini-split air conditioners also have several potential applications in commercial buildings. Commercial buildings are most likely large and need substantial amounts of energy to heat and cool the areas, but they face issues due to the unavailability of ducts. These systems are also good options for small apartments and room additions, where spreading or installing distribution ductwork for a heating system and central air conditioner is not feasible. Such benefits are expected to augment the adoption of ductless mini-split air conditioners in commercial spaces.

United Kingdom Commercial HVAC Industry Overview

The United Kingdom commercial HVAC market is fragmented, favorably competitive, and has several prominent players. The market performers are focusing on expanding their consumer base across foreign countries. These enterprises leverage strategic collaborative initiatives to boost their market share and profitability. Companies such as Siemens AG, Honeywell International Inc., Daikin Industries Ltd, and Mitsubishi Electric Europe BV, among others operating in the market, are also acquiring start-ups working on HVAC technologies to strengthen their production capacities.

In March 2024, Mitsubishi Electric Europe BV unveiled its latest offering in the form of residential air-to-water heat pumps. The company's Hydrolution EZY monoblock stands out for its ability to generate hot water, reaching temperatures as high as 60°C, even in outdoor conditions plummeting to -25°C. This model comes in two power options: 10 kW and 14 kW.

In December 2023, Daikin Industries Ltd announced the introduction of Nepura, the new residential air-to-air heat pump range. With this product range, Daikin Europe aims to offer a reliable heating solution that works at temperatures down to 30°C and achieves heating efficiency values of up to A+++.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Commercial Construction in Major Emerging Economies

- 5.1.2 Increasing Demand For Energy Efficient Devices

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Energy Efficient Systems

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning /Ventillation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End User Industry

- 6.2.1 Hospitality

- 6.2.2 Commercial Buildings

- 6.2.3 Public Buildings

- 6.2.4 Others

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Johnson Controls International PLC

- 7.1.2 Midea Group Co., Ltd.

- 7.1.3 Daikin Industries, Ltd.

- 7.1.4 Robert Bosch GmbH

- 7.1.5 Carrier Corporation

- 7.1.6 LG Electronics Inc.

- 7.1.7 Lennox International Inc

- 7.1.8 BDR Thermea Group

- 7.1.9 Panasonic Corporation

- 7.1.10 Danfoss A/S