イタリアの業務用HVAC:市場シェア分析、産業動向、成長予測(2024年~2029年)

Italy Commercial HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1550307

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

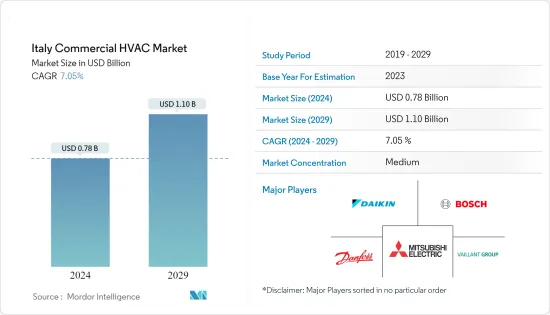

イタリアの業務用HVAC市場規模は2024年に7億8,000万米ドルと推定され、2029年には11億米ドルに達し、予測期間(2024-2029年)のCAGRは7.05%で成長すると予測されます。

主なハイライト

- イタリアの商業セクターでは、空調システムとヒートポンプへの嗜好の高まりが主な要因となって、HVAC機器の需要が顕著に増加しています。この動向は、気候変動、都市化、ライフスタイルの変化、技術の進歩など、いくつかの要因によるものです。この市場は、商業スペースの建設増加、環境に優しい建設に対する政府の支援、急速な都市化などから恩恵を受けています。例えば、2024年初頭には、イタリアの人口の72.1%が都市部に居住し、残りの27.9%は農村部に居住しています。

- 各国政府は厳しい規制の導入に前向きで、ヒートポンプの導入やボイラーの禁止を義務付けています。こうした取り組みが市場の成長を後押ししています。例えば、EUはグリーン・ホームズ指令に沿って、2029年からガスボイラーの使用を禁止する方向で準備を進めています。この指令は、エコデザイン規則813/2013/EUの改正案の一部であり、空間暖房器具の設計・販売基準を定めています。

- イタリアのいくつかの地域では、冷房需要が暖房需要を上回っています。その結果、冷暖房ソリューションの一般的な選択肢は、空気対空気のリバーシブルヒートポンプです。ヒートポンプは主に冷房用として使用されるが、寒い時期には暖房需要にも効果的に対応し、国土の大部分をカバーしています。

- 市場の主要企業は、消費者の需要を満たすため、新製品の発売に注力しています。例えば、LGエレクトロニクスは2024年3月、イタリアのミラノで開催されたMCE 2024で、最新の住宅用エアコン「DUALCOOL」を発表しました。MCE 2024は、欧州有数のHVAC展示会です。3月12日から15日まで開催された同展示会では、LGの最先端の空調技術革新が紹介され、特に、年間を通じて室内の快適性を高めるように設計された「ソフトエア(TM)」機能が強調されました。

- 建設業界はイタリア経済にとって不可欠な産業であり、300万人以上の従業員を雇用し、1,100億ユーロ(1,197億3,000万米ドル)以上のGDPに貢献しています。イタリアでは商業ビルの建設が増加しており、多くの商業ビルが存在することから、カーボンフットプリントとCO2排出量を削減するHVACシステムの需要が高まっています。

- 例えば、2023年には、イタリア南部地域が約260万戸と最大の商業ビルストックを誇っています。北西部地域と中部地域が僅差で続き、それぞれ約250万戸と200万戸の商業ビルがあります。この商業用不動産には、小売スペース、研究所、信用機関、倉庫、ホテル、官公庁、農業施設など、さまざまな非住宅建築物が含まれます。

- イタリアの商業用HVAC市場では、多くの既存ベンダーが存在するため、競争企業間の敵対関係は高いです。世界のメーカーは、エネルギー効率を重要な関心事の1つとしています。ダイキン、キャリア、ロバート・ボッシュGmbh、ダンフォスAS、三菱電機欧州BV、レノックス・インターナショナルInc.など多くの企業が、すでにエネルギー効率の高いHVAC製品の発売を開始しています。それゆえ、彼らは市場の価格決定者となっています。そのため、比較的小規模なプレーヤーは、これらの製品に盛り込まれた技術革新の水準に見合うだけの資金力を持たず、製品を低価格で販売しなければならないです。

- 現在進行中のロシア・ウクライナ戦争は政治的・経済的混乱につながり、この地域の消費者の購買力を低下させています。ロシアのウクライナ侵攻は、イタリアを含む多くのEU諸国のエネルギー部門に大きな影響を与えています。欧州委員会によると、イタリアのエネルギー価格の下落により、2024年のインフレ率は1.6%に低下し、2025年には1.9%に若干上昇すると予想されています。実質可処分所得が回復しているにもかかわらず、家計は金利上昇を利用して貯蓄を増やすと予想されます。これらの要因は、同国の市場成長を短期間阻害すると予測されます。

イタリアの業務用HVAC市場の動向

暖房機器は大幅なCAGRで成長する見込み

- 商業用HVAC市場では、ボイラー/ラジエーター/暖炉やヒートポンプなどの暖房機器が大きなシェアを占めると予想されます。イタリアの商業ビルでは、ヒートポンプの需要が大きく伸びています。ヒートポンプは商業施設に、従来の冷暖房システムを上回る多くの利点を提供します。これらの技術は、エネルギー効率を高め、運用コストを削減し、環境の持続可能性を支持します。

- 商業施設は、ヒートポンプを採用し、持続可能なイニシアチブをサポートすることで、二酸化炭素排出量を削減します。これらのシステムに投資することで、効率を高め、コストを削減し、商業施設をよりクリーンで持続可能なエネルギー環境への移行のリーダーとして位置づけることができます。

- いくつかの企業は、商業セグメントにおけるこれらの暖房システムの需要に応える様々な製品の導入に絶えず投資しています。例えば、ダイキンは2023年11月に、2024年前半に発売予定の2つのVRV 51ヒートポンプ・システムに関する情報を開示しました。これらの新システム、すなわちMini-VRVとTop-Blowシリーズは、商業ビルにおける脱炭素化の需要の高まりに対応するよう設計されています。

- 2023年11月、アイラはイタリアでデビューしました。同社が提供するのは、スマートヒートポンプやソーラーパネルから、蓄電池やオーダーメイドの電気料金プランまで、幅広いクリーンエネルギー・ソリューションです。Airaを選択することで、イタリアの家庭はエネルギー料金を55%削減し、CO2排出量を大幅に抑制することができます。

商業ビルのエンドユーザーが大きな市場シェアを占める

- 商業用ビル分野は、商業用不動産市場の成長と、オフィスビル、ショッピングセンター、その他の商業スペースにおける空調やヒートポンプの需要増加により、大きく成長すると予測されています。

- 富士通によると、イタリア市場では年間180万台以上の空調需要があるといいます。ますます厳しくなる環境規制に対応するため、富士通は2024年3月、イタリアにGENERALブランドを導入し、商業部門での販売拡大に注力しました。2024年には、エネルギー効率を高めた壁掛けエアコン、環境に優しい冷媒R32を使用したVRFシステム、デザイン性を重視したモデルなどの新製品を発売する予定です。富士通は大規模施設の空調用に設計されたチラーを展示し、包括的な空調ポートフォリオへのコミットメントを強調しています。

- イタリアではここ数年、商業ビルのオーナーの間でHVACシステムの利用が盛んになっています。イタリアでは商業用不動産セクターが急激に増加しており、HVACシステムに大きなビジネスチャンスが生まれると期待されています。欧州の商業用不動産市場は、2023年には9兆米ドルを超えると予測されています。商業用不動産投資総額は、2022年には2,530億ユーロであったが、2023年には約1,330億ユーロに減少しました。

- 欧州公的不動産協会によると、ドイツ、英国、フランス、イタリアが商業用不動産投資市場の上位4カ国です。イタリアの商業用不動産市場は2023年に9,408億4,000万米ドルと評価されました。商業セクターへの投資の増加は、市場の成長をさらに促進すると予想されます。

- *イタリアの商業部門では、ダクトレス・ミニスプリット・エアコンの人気が高まっています。これらのシステムは、大幅な冷暖房が必要でありながら従来のダクトがない大型ビルで特に好まれています。さらに、セントラル・エア・システムのための配電ダクトを設置することが現実的でない、小規模なアパートや部屋の増築に理想的なソリューションでもあります。こうした利点が、市場の成長を後押しします。

- イタリアの商業部門では、ダクトレス・ミニスプリット・エアコンの人気が高まっています。これらのシステムは、大幅な冷暖房が必要でありながら従来のダクトがない大型ビルで特に好まれています。さらに、セントラル・エア・システムのための配電ダクトを設置することが現実的でない、小規模なアパートや部屋の増築に理想的なソリューションでもあります。このような利点が、市場の成長を促進する態勢を整えています。

イタリアの業務用HVAC産業概要

イタリアの業務用HVAC市場は細分化されており、競争が激しく、有力企業が複数存在します。市場参入企業は、海外の消費者基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的な共同イニシアティブを活用しています。イタリアの商業用HVAC市場で事業を展開しているシーメンスAG、ハネウェル・インターナショナル、ダイキン工業、三菱電機欧州BV、ダンフォスAS、ロバート・ボッシュGmBHなどの企業は、生産能力を強化するためにHVAC技術に取り組む新興企業の買収にも注力しています。

2024年7月イタリアの暖房メーカーであるRhossは、商業用および工業用に調整された非可逆水源ヒートポンプを発売しました。この革新的な製品は、85℃という高温の温水を実現し、ピーク時の季節性能係数(SCOP)は5.04という驚異的な数値です。

2023年12月住宅用空冷ヒートポンプ「Nepura」を発売。この製品シリーズにより、ダイキン欧州は、30℃までの温度で作動し、最高A+++の暖房効率値を達成する信頼性の高い暖房ソリューションを提供することを目指しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 主要新興国における商業建築の増加

- エネルギー効率の高い機器に対する需要の増加

- 異常気象による冷暖房機器需要の増加

- 市場の課題

- エネルギー効率の高いシステムの初期コストの高さ

第6章 市場セグメンテーション

- 部品タイプ別

- HVAC機器

- 暖房機器

- 空調・換気機器

- HVACサービス

- HVAC機器

- エンドユーザー産業別

- ホスピタリティ

- 商業ビル

- 公共施設

- その他のエンドユーザー産業

第7章 競合情勢

- 企業プロファイル

- Johnson Controls International PLC

- Midea Group Co. Ltd

- Daikin Industries Ltd

- Robert Bosch GmbH

- Carrier Corporation

- LG Electronics Inc.

- Lennox International Inc.

- BDR Thermea Group

- Panasonic Corporation

- Danfoss AS

第8章 投資分析

第9章 市場の将来

目次

The Italy Commercial HVAC Market size is estimated at USD 0.78 billion in 2024, and is expected to reach USD 1.10 billion by 2029, growing at a CAGR of 7.05% during the forecast period (2024-2029).

Key Highlights

- The commercial sector in Italy is experiencing a notable rise in demand for HVAC equipment, driven largely by a growing preference for air conditioning systems and heat pumps. This trend results from several factors, including climate change, urbanization, changing lifestyles, and technological advancements. The market is benefiting from increased construction in commercial spaces, government backing for eco-friendly construction, and rapid urbanization. For instance, at the beginning of 2024, 72.1% of Italy's population resided in urban areas, with the remaining 27.9% in rural regions.

- Governments are looking forward to introducing stringent regulations, thus mandating the incorporation of heat pumps and a ban on boilers. Such initiatives are driving the market's growth. For instance, the EU is gearing up to enforce a ban on gas boilers starting in 2029, aligned with the Green Homes Directive. This directive is part of the proposed amendments to the Ecodesign Regulation 813/2013/EU, which delineates the standards for designing and marketing space heating appliances.

- Across several regions in Italy, the demand for cooling surpasses that for heating. As a result, the prevalent choice for heating and cooling solutions is the reversible air-to-air heat pump. While primarily employed for cooling purposes, these systems also effectively meet heating requirements during the colder months, covering a significant portion of the nation.

- Key market players are focusing on new product launches to meet consumer demand. For instance, in March 2024, LG Electronics unveiled its latest residential air conditioner, the DUALCOOL, at MCE 2024 in Milan, Italy. MCE 2024 stands as one of Europe's premier HVAC exhibitions. Running from March 12-15, the event showcased LG's cutting-edge air conditioning innovations, notably highlighting the Soft Air(TM) feature, designed to elevate indoor comfort throughout the year.

- The construction industry is vital to the Italian economy, employing over three million people and contributing more than EUR 110 billion (USD 119.73 billion) to the country's GDP. The growing construction of commercial buildings and the presence of many commercial buildings in Italy drive demand for HVAC systems to reduce carbon footprint and CO2 emission.

- For instance, in 2023, the Southern region of Italy boasted the largest stock of commercial buildings, with approximately 2.6 million units. The North-West and Central regions followed closely, with around 2.5 million and 2 million commercial units, respectively. This commercial real estate encompasses a variety of non-residential structures, including retail spaces, labs, credit institutions, warehouses, hotels, public offices, and agricultural units.

- The competitive rivalry in the Italian commercial HVAC market studied is high due to its many established vendors. Global manufacturers are focusing on energy efficiency as one of their key concerns. Many players, such as Daikin, Carrier, Robert Bosch Gmbh, Danfoss AS, Mitsubishi Electric Europe BV, and Lennox International Inc., have already started launching energy-efficient HVAC products. Hence, they have become price setters in the market. Thus, comparatively smaller players lack the financial capacity to match the level of technological innovations incorporated in these products and must sell their products at a lower price point.

- The ongoing Russia and Ukraine War has led to political and economic turbulence, diminishing consumer purchasing power in the region. Russia's invasion of Ukraine has significantly impacted the energy sector in many EU countries, including Italy. According to the European Commission, the decline in energy prices in Italy is expected to reduce inflation to 1.6% in 2024, with a slight increase to 1.9% anticipated in 2025. Despite the recovery in real disposable incomes, households are expected to increase their savings, leveraging higher interest rates. These factors are projected to hamper the market's growth for a short period of time in the country.

Italy Commercial HVAC Market Trends

Heating Equipment is Expected to Grow with Significant CAGR

- Heating equipment such as boilers/radiators/furnaces and heat pumps are expected to hold a significant share in the commercial HVAC market. The demand for heat pumps is growing significantly in commercial buildings in Italy. Heat pumps offer commercial properties and many advantages that surpass traditional heating and cooling systems. These technologies boost energy efficiency, cut operational costs, and champion environmental sustainability.

- Commercial properties shrink their carbon footprint by adopting heat pumps and supporting sustainability initiatives. Investing in these systems enhances efficiency, cuts costs, and positions commercial properties as leaders in transitioning to a cleaner, sustainable energy landscape.

- Several companies are constantly investing in introducing various products catering to the demand for these heating systems in the commercial segment. For instance, in November 2023, Daikin disclosed information regarding two VRV 51 heat pump systems that were scheduled to be released in the first half of 2024. These new systems, namely the Mini-VRV and the Top-Blow series, are designed to cater to the growing demand for decarbonization in commercial buildings.

- In November 2023, Aira made its debut in Italy with a clear goal to lead Europe away from gas dependency and hasten the process of decarbonization. The company's offerings span a range of clean energy solutions, from smart heat pumps and solar panels to battery storage and tailored electricity tariffs. By opting for Aira, Italian households stand to slash their energy bills by 55% and significantly curb their CO2 emissions, a stark contrast to traditional fossil fuel approaches.

Commercial Buildings End Users Hold Significant Market Share

- The commercial buildings segment is projected to rise significantly due to the growing commercial real estate market and rising demand for air conditioning and heat pumps in office buildings, shopping centers, and other commercial spaces.

- According to Fujitsu, the Italian market experiences an annual demand exceeding 1.8 million air conditioning units. In response to increasingly stringent environmental regulations, in March 2024, Fujitsu introduced its GENERAL brand in Italy, focusing on expanding sales in the commercial sector. In 2024, the company plans to launch new products, including wall-mounted air conditioners with enhanced energy efficiency, VRF systems utilizing the eco-friendly refrigerant R32, and models emphasizing design excellence. Fujitsu showcases a chiller designed for large-scale facility air conditioning, highlighting its commitment to a comprehensive air conditioning portfolio.

- HVAC system applications have become popular among commercial building owners in Italy for the past few years. The commercial real estate sector is rising exponentially in Italy, which is expected to create significant opportunities for HVAC systems. The European commercial real estate market was projected at over USD 9 trillion in 2023. The total commercial real estate investment volume was EUR 253 billion in 2022, which dropped to about 133 billion in 2023.

- According to the European Public Real Estate Association, Germany, the United Kingdom, France, and Italy are the top four commercial real estate investment markets. Italy's commercial real estate market was valued at USD 940.84 billion in 2023. Rising investment in the commercial sector is expected to further drive the market's growth.

- * In Italy's commercial sector, ductless mini-split air conditioners are increasingly popular. These systems are particularly favored in large buildings that demand substantial heating and cooling yet lack traditional ductwork. Moreover, they are ideal solutions for small apartments and room extensions, where installing distribution ductwork for a central air system is impractical. These advantages are poised to propel the market's growth.

- In Italy's commercial sector, ductless mini-split air conditioners are increasingly popular. These systems are particularly favored in large buildings that demand substantial heating and cooling yet lack traditional ductwork. Moreover, they are ideal solutions for small apartments and room extensions, where installing distribution ductwork for a central air system is impractical. These advantages are poised to propel market growth.

Italy Commercial HVAC Industry Overview

The Italian commercial HVAC market is fragmented, favorably competitive, and has several prominent players. The market performers are focusing on expanding their consumer base across foreign countries. These enterprises leverage strategic collaborative initiatives to boost their market share and profitability. Companies such as Siemens AG, Honeywell International Inc., Daikin Industries Ltd., Mitsubishi Electric Europe BV, Danfoss AS, and Robert Bosch GmBH, operating in the Italian commercial HVAC market, are also focusing on the acquisition of start-ups working on HVAC technologies to strengthen their production capacities.

July 2024: Rhoss, an Italian heating manufacturer, launched a non-reversible water-source heat pump tailored for commercial and industrial use. This innovative product can achieve hot water temperatures as high as 85°C, coupled with an impressive seasonal coefficient of performance (SCOP) peaking at 5.04.

December 2023: Daikin introduced Nepura, the new residential air-to-air heat pump range. With this product range, Daikin Europe aimed to offer a reliable heating solution that works at temperatures down to 30 degrees Celcius and achieves heating efficiency values of up to A+++.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Commercial Construction in Major Emerging Economies

- 5.1.2 Increasing Demand For Energy Efficient Devices

- 5.1.3 Extreme Climate Conditions Fuel Heating and Cooling Equipment Demand

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Energy Efficient Systems

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 HVAC Equipment

- 6.1.1.1 Heating Equipment

- 6.1.1.2 Air Conditioning /Ventillation Equipment

- 6.1.2 HVAC Services

- 6.1.1 HVAC Equipment

- 6.2 By End-user Industry

- 6.2.1 Hospitality

- 6.2.2 Commercial Buildings

- 6.2.3 Public Buildings

- 6.2.4 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Johnson Controls International PLC

- 7.1.2 Midea Group Co. Ltd

- 7.1.3 Daikin Industries Ltd

- 7.1.4 Robert Bosch GmbH

- 7.1.5 Carrier Corporation

- 7.1.6 LG Electronics Inc.

- 7.1.7 Lennox International Inc.

- 7.1.8 BDR Thermea Group

- 7.1.9 Panasonic Corporation

- 7.1.10 Danfoss AS

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日