北米のパウチ包装:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

North America Pouch Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 124 Pages

- 納期

- 2~3営業日

- 商品コード

- 1550001

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

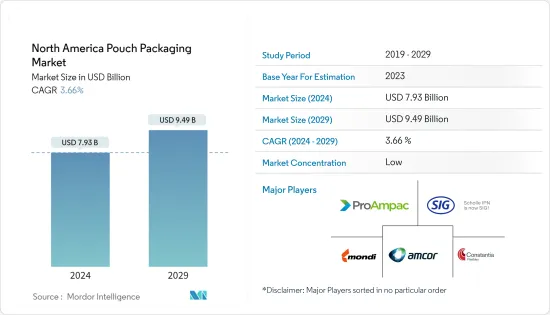

北米のパウチ包装市場規模は2024年に79億3,000万米ドルと推定され、2029年には94億9,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは3.66%で成長する見込みです。

主なハイライト

- パウチは、一般的にプラスチック、紙、ホイル、またはこれらの組み合わせなどの材料で作られた袋状の容器で構成される、柔軟で軽量なタイプの包装として広く使用されています。パウチは食品、化粧品、医薬品を含む様々な製品を密封して保護し、リシーラブルクロージャーや簡単に分注できるスパウトなどの機能を備えて設計されます。パウチには、紫外線や酸素などの要因からデリケートな製品を保護し、製品の品質を維持するために、アルミ箔や金属化層などの特殊なバリアフィルムが組み込まれていることが多いです。

- パウチ包装は、北米の調理済み食品(RTE)や冷凍食品市場セグメントで重要な関連性を見出しています。パウチは開封、再密封、保存が容易なため、手軽な食事やスナックに最適です。これに加えて、パウチはポーションコントロールを可能にし、これは正確な分量が望まれるRTEや冷凍食品分野では不可欠です。また、パウチは電子レンジ対応に設計することもできるため、消費者はパウチの中ですぐに食べられる食事を直接温めることができ、調理器具を追加する必要性を減らすことができます。パウチ包装のこうした特徴は、市場の成長にプラスに働く。

- パウチは一般的に、その軽量な性質と材料の効率的な使用により、製造・輸送コストが低いです。これは小売業者だけでなく製造業者にとってもコスト削減につながります。パウチは、缶やボトルなどの他の包装形態よりも廃棄物が少なく、リサイクル可能な場合が多いため、廃棄物削減の取り組みに貢献します。さらに、パウチにはブランディングや製品情報のための十分なスペースがあり、マーケティングやブランディングのための優れた選択肢となります。人目を引くグラフィックやラベルをデザインすることもできます。

- しかし、北米では持続可能性への関心が高まっています。パウチは、環境に優しい素材を使用して製造され、リサイクル可能なデザインにすることができ、より環境に配慮したパッケージングを選択する傾向に沿っています。

- 北米の食品業界やペットフード業界における分量規制の動向の高まりは、パウチ包装ソリューションの需要を促進しており、消費者の鮮度と利便性を確保しつつ、便利な分量にすることを容易にしています。このように、消費者の嗜好の変化、サプライチェーンの力学、包装業界における持続可能性への配慮が、変化する市場の需要や安全要件に対応した技術革新と適応を促しています。

北米のパウチ包装市場の動向

レトルトパウチが市場で最も高い成長を遂げる見込み

- 北米のレトルトパウチ包装市場は、コンビニエンス食品に対する需要の増加と、保存料を使用せずに賞味期限を長くしたいという要望が主な要因となっています。レトルトパウチは様々な食品の賞味期限を延ばすために設計されています。その効果の鍵はレトルト処理にあり、レトルトパウチを高温に加熱して微生物や酵素などを死滅させる。この工程により、製品の安全性と品質が長期間保たれます。

- レトルトパウチは、使い方が簡単で場所を取らないため、食品包装に広く使われています。レトルトパウチは、スパウト、リリースバルブ、ティアノッチ、エンドクリップ付きスライダークロージャー、リシーラブルジッパー、ハンドルなどの追加機能により、人気も高まっています。これらのパウチは一般的に、優れたバリア性を提供する柔軟な多層素材で作られています。ポリエステル、ナイロン、アルミ箔、ポリエチレンの組み合わせで作られています。この組み合わせは、食品を劣化させる主な要因である酸素、湿気、光を効果的に遮断します。

- レトルト食品は汎用性が高く、調理済み食品、ソース、離乳食、ペットフード、飲食品など、さまざまな種類の食品に使用できます。さらに、レトルトパウチは、缶やガラス瓶のような従来の硬質包装に比べ、驚くほど軽量でスペース効率に優れています。そのため、製造業者や小売業者にとっては、輸送コストの削減や保管スペースの最適化に一役買っています。

- 2023年2月、カナダ政府はプラスチック包装と使い捨てプラスチックの表示規則を導入する計画を明らかにしました。生産者がこれらの製品のリサイクル可能性を評価しない限り、この表示規則では、消費者向け包装や使い捨てプラスチックに追いかけ矢印マークやその他のリサイクル可能性を謳う表示を使用することが禁止されます。現在、プラスチック包装はプラスチック廃棄物の約半分を占めているが、リサイクルされているプラスチック包装は全体の15%未満です。このイニシアチブは、2030年までにプラスチック廃棄物ゼロを目指すカナダの計画の一環です。カナダの製造業者は、自社製品の包装材料や包装システムの改善を求めてきました。

- カナダ統計局によると、2023年7月の加工肉の消費者物価指数(CPI)は195.3でした。カナダでは加工肉の消費が増加しているため、レトルトパウチへの需要に拍車がかかっています。レトルトパウチは、製品の保存と調理の容易さを保証する便利な包装ソリューションを提供し、消費者の多忙なライフスタイルに合致しているからです。

米国が最大の市場シェアを占める見込み

- 米国では、外出先での消費や冷凍食品などの需要が高く、加工食品の成長を促進しています。

- フレキシブル・パッケージング・アソシエーションによると、リサイクル可能なフィルムとパウチは現在主流になりつつあります。国内外からの圧力や、より環境に優しい選択肢を求める消費者の声が、廃棄物やリサイクルの問題に目を向け、実現可能な解決策を見出すよう各国を駆り立てています。

- フレキシブル・パッケージング・アソシエーション(FPA)によると、生産工程と材料革新の分野で行われた開発により、一部のフレキシブル・パッケージングの重量は約50%減少しました。さらに、パウチ包装は省スペース化も可能にするため、より少ない燃料とエネルギーでかなりの割合の製品を出荷することができます。

- 米国のパウチ包装市場は、利便性、持続可能性、製品の鮮度を求める消費者の需要に応えるため、近年いくつかのイノベーションが起きています。2023年6月、イスラエルを拠点とする堆肥化可能な包装のスペシャリストであるティパ社は、米国最大の包装メーカーであるPPCフレキシブル・パッケージング社とクリアビュー・パッケージング社の2社と提携しました。イリノイ州とユタ州に米国の主要施設を持つPPCフレキシブル・パッケージング社は、ティパのコンポスタブル・ラミネートを製造ポートフォリオに加え、焼き菓子、乾燥食品、サプリメント、ビタミン剤などの包装用パウチを製造する予定です。

- Appinioのデータによると、2023年には米国の消費者の24%が週に数回冷凍食品を好むようになります。同国では冷凍食品の消費量が多いため、冷凍食品の保管や輸送に便利でスペース効率の高いソリューションを提供するパウチ包装の需要が高まっています。

北米のパウチ包装産業の概要

北米のパウチ包装市場は、世界的に複数の市場プレーヤーが存在するため断片化されています。主なプレーヤーは、Amcor PLC、Mondi Group、ProAmpac Intermediate Inc.、SIG Group AG、Constantia Flexibles Group GmbHなどです。市場プレーヤーは、複数の最終用途分野の成長機会を活用し、市場でのプレゼンスを拡大するために革新的な取り組みを行っています。

- 2024年2月-Amcor社は、国内有数のオーガニックヨーグルトメーカーであるStonyfield Organic社、スパウトパウチ包装の大手メーカーであるCheer Pack North America社と共同で、初のオールポリエチレン(PE)スパウトパウチを発売しました。この革新的なパウチは、Stonyfield Organic社のYoBaby冷蔵ヨーグルト用に、従来のマルチラミネート構造から、より責任あるパウチデザインに置き換わったものです。

- 2023年8月-TCトランスコンチネンタルパッケージングは、先進の単一素材リサイクル可能なフレキシブルプラスチック包装ソリューションの開発に向けて6,000万米ドルを投資し、より耐熱性の高い高性能ポリエチレンフィルムを提供すると発表しました。TCトランスコンチネンタルパッケージングは、ロールストック、袋、パウチ、シュリンクフィルムと袋、先進コーティングを含む様々なフレキシブルプラスチック製品を提供し、乳製品、コーヒー、食肉と鶏肉、ペットフード、農業、飲食品、家庭用品とパーソナルケア、工業、消費者製品、医療を含む様々な市場にサービスを提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 地域全体における調理済み食品の高い消費量

- 軽量包装ソリューションへの需要の高まり

- 市場の課題

- プラスチック包装の使用に関する懸念の高まり

第6章 市場セグメンテーション

- タイプ別

- 標準タイプ

- アセプティック

- レトルト

- ホットフィル

- クロージャータイプ別

- ジッパー

- スパウト

- ティアノッチ

- エンドユーザー産業別

- 飲食品

- パーソナルケア

- ヘルスケア

- その他エンドユーザー産業

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Amcor Group GmbH

- ProAmpack Intermediate Inc.

- Mondi Group

- Constantia Flexibles Group GmbH

- Flair Flexible Packaging Corporation

- Sealed Air Corporation(SEE)

- Sonoco Products Company

- Toyo Seikan Co. Ltd

- Smurfit Kappa Group PLC

- SIG Group AG

第8章 投資分析

第9章 市場機会と今後の動向

目次

The North America Pouch Packaging Market size is estimated at USD 7.93 billion in 2024, and is expected to reach USD 9.49 billion by 2029, growing at a CAGR of 3.66% during the forecast period (2024-2029).

Key Highlights

- Pouches are widely used as a flexible and lightweight type of packaging that typically consists of a bag-like container made from materials such as plastic, paper, foil, or a combination of these. Pouches are sealed to enclose and protect various products, including food, cosmetics, and pharmaceuticals, and can be designed with features like resealable closures or spouts for easy dispensing. Pouches often incorporate specialized barrier films, such as aluminum foil or metalized layers, to protect sensitive products from factors like UV light and oxygen, maintaining product quality.

- Pouch packaging has found significant relevance in the North American ready-to-eat (RTE) and frozen food market segments. Pouches are easy to open, reseal, and store, thus making them ideal for quick meals or snacks. In addition to this, pouches allow for portion control, which is essential in the RTE and frozen food sectors where precise servings are desirable. Pouches can also be designed to be microwave-safe, allowing consumers to heat their ready-to-eat meals directly in the pouch, reducing the need for additional cookware. Such features of pouch packaging positively affect the growth of the market.

- Pouches are typically less expensive to produce and transport due to their lightweight nature and efficient use of materials. This leads to cost savings for manufacturers as well as the retailers. Pouches generate less waste than other packaging forms, such as cans or bottles, and they are often recyclable, contributing to waste reduction efforts. Furthermore, pouches offer ample space for branding and product information, making them an excellent choice for marketing and branding efforts. They can be designed with eye-catching graphics and labels.

- However, sustainability is a growing concern in North America. Pouches can be manufactured using eco-friendly materials and designed to be recyclable, aligning with the trend toward more environmentally conscious packaging choices.

- The surge in portion control trends within the food and pet food industries in North America is driving the demand for pouch packaging solutions, facilitating convenient serving sizes while ensuring freshness and convenience for consumers. Thus, changing consumer preferences, supply chain dynamics, and sustainability considerations in the packaging industry are driving innovation and adaptation in response to changing market demands and safety requirements.

North America Pouch Packaging Market Trends

Retort Pouches are Anticipated to Witness the Highest Growth in the Market

- The market for retort pouch packaging in North America is majorly driven by the increasing demand for convenience foods and the desire for longer shelf life without preservatives. Retort pouches are designed to extend the shelf life of various food products. The key to their effectiveness is the retort process, which involves heating the pouches to high temperatures to kill microorganisms, enzymes, and others. This process ensures that the product remains safe and retains its quality for an extended period.

- Retort pouches are widely used in food packaging since they are simple to use and take up little space. Retort pouches are also becoming more popular because of their extra features, including spouts, release valves, tear notches, slider closures with end clips, resealable zippers, and handles. These pouches are typically made from flexible, multi-layer materials that provide excellent barrier properties. The layers often include a combination of polyester, nylon, aluminum foil, and polyethylene. This combination effectively blocks out oxygen, moisture, and light, which are the primary factors that can lead to food deterioration.

- Retort pouches are versatile and can be used for various types of foods, including ready-to-eat meals, sauces, baby food, pet food, and even beverages. Additionally, retort pouches are incredibly lightweight and space-efficient compared to traditional rigid packaging like cans or glass jars. This further helps reduce transportation costs and optimize storage space for manufacturers and retailers.

- In February 2023, the Canadian Government revealed its plan to introduce labeling rules for plastic packaging and single-use plastics. Unless producers have assessed these products for recyclability, the labeling rules prohibit using the chasing-arrows symbol and other recyclability claims on consumer packaging and single-use plastics. Currently, plastic packaging makes up approximately half of all plastic waste, but less than 15% of plastic packaging is recycled. This initiative was part of Canada's plan to move toward zero plastic waste by 2030. Canadian manufacturers have sought to adopt enhanced packaging materials and systems for their products.

- As per Statistics Canada, in July 2023, the consumer price index (CPI) for processed meat was 195.3. The increasing consumption of processed meat in Canada has spurred a corresponding demand for retort pouches, as they offer convenient packaging solutions that ensure product preservation and ease of preparation, aligning with consumers' busy lifestyles.

The United States is Expected to Hold the Largest Market Share

- The United States is witnessing a high demand for on-the-go consumption and frozen food, among others, which is driving the growth of processed food, which, in turn, is boosting the pouch packaging market.

- According to the Flexible Packaging Association, recyclable films and pouches are currently becoming more mainstream. Foreign and domestic pressures, as well as consumers' demand for more eco-friendly options, are spurring countries to look at the issue of waste and recycling and find feasible solutions.

- The Flexible Packaging Association (FPA) indicates that the developments made in the areas of production processes and material innovation have decreased the weight of some flexible packaging by approximately 50%. Moreover, pouch packaging also permits space-saving opportunities, which means that substantial ratios of products could be shipped utilizing less fuel and energy.

- The pouch packaging market in the United States has seen several innovations in recent years to meet consumer demand for convenience, sustainability, and product freshness. In June 2023, Israel-based compostable packaging specialist Tipa partnered with two of the largest packaging manufacturers in the United States, PPC Flexible Packaging and Clearview Packaging. With main US facilities in Illinois and Utah, PPC Flexible Packaging is set to add Tipa's compostable laminates to its manufacturing portfolio to produce pouches for packaging baked goods, dry food, supplements, vitamins, and other products.

- As per Appinio data, in 2023, 24% of consumers in the United States preferred frozen food several times a week. As frozen food consumption in the country is high, there is an increased demand for pouch packaging, which offers convenient and space-efficient solutions for storing and transporting frozen foods.

North America Pouch Packaging Industry Overview

The North American pouch packaging market is fragmented due to the presence of several market players globally. Some major players are Amcor PLC, Mondi Group, ProAmpac Intermediate Inc., SIG Group AG, and Constantia Flexibles Group GmbH. The market players are expected to leverage the opportunity posed by the growth of several end-use verticals and are innovating to expand their market presence.

- February 2024 - Amcor collaborated with Stonyfield Organic, the country's leading organic yogurt maker, and Cheer Pack North America, a leading manufacturer of spouted pouch packaging, to launch the first all-polyethylene (PE) spouted pouch. The innovative pouch replaces Stonyfield Organic's prior multi-laminate structure with a more responsible pouch design for its YoBaby refrigerated yogurt.

- August 2023 - TC Transcontinental Packaging announced an investment of USD 60 million toward developing advanced mono-material recyclable flexible plastic packaging solutions, providing high-performance polyethylene films with more heat resistance. TC Transcontinental Packaging offers a variety of flexible plastic products, including rollstock, bags, and pouches, shrink films and bags, and advanced coatings, servicing a variety of markets, including dairy, coffee, meat and poultry, pet food, agriculture, beverage, home and personal care, industrial, consumer products, and medical.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Consumption of Ready-to-Eat Foods Across the Region

- 5.1.2 Increasing Demand for Light Weight packaging Solution

- 5.2 Market Challenges

- 5.2.1 Rising Concerns Regarding the Use of Plastic Packaging

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Standard

- 6.1.2 Aseptic

- 6.1.3 Retort

- 6.1.4 Hot-Fill

- 6.2 By Closure Type

- 6.2.1 Zipper

- 6.2.2 Spout

- 6.2.3 Tear Notch

- 6.3 By End-user Industry

- 6.3.1 Food and Beverage

- 6.3.2 Personal Care

- 6.3.3 Healthcare

- 6.3.4 Other End-user industries

- 6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 ProAmpack Intermediate Inc.

- 7.1.3 Mondi Group

- 7.1.4 Constantia Flexibles Group GmbH

- 7.1.5 Flair Flexible Packaging Corporation

- 7.1.6 Sealed Air Corporation (SEE)

- 7.1.7 Sonoco Products Company

- 7.1.8 Toyo Seikan Co. Ltd

- 7.1.9 Smurfit Kappa Group PLC

- 7.1.10 SIG Group AG

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 124 Pages

- 納期

- 2~3営業日