アジア太平洋地域のパウチ包装:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

Asia-Pacific Pouch Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1550236

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

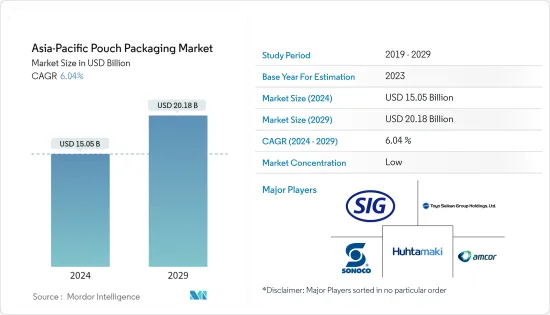

アジア太平洋地域のパウチ包装市場規模は、2024年に150億5,000万米ドルと推定され、予測期間(2024-2029年)のCAGRは6.04%で成長し、2029年には201億8,000万米ドルに達すると予測されます。

出荷数では、2024年の1,806億3,000万枚から2029年には2,302億8,000万枚へと、予測期間(2024~2029年)のCAGRは4.98%で成長すると予測されます。

主なハイライト

- プラスチックフィルム、アルミ箔、ラミネートなどの素材を利用したパウチ包装は、バリア性、耐久性、視覚的アピールなどの特定のニーズに対応します。スタンドアップパウチは、スナックや液体などの製品用に設計されており、自立性のあるベースが特徴です。また、スパウト付きパウチは、ソースや離乳食などの液体を注ぎやすいです。ヒートシールのような密封方法は、外的要因からきめ細かく保護します。パウチの中にはジッパーで開閉できるものもあり、利便性を高め、製品の鮮度を保つことができます。

- アジア太平洋地域では、ますます忙しくなるライフスタイルに後押しされ、すぐに食べられる食事やスナックなどの加工食品が人気を集めています。世界保健機関(WHO)は、東南アジアにおける食事パターンの大きな変化を指摘しており、高度に加工された家庭外食品への嗜好が高まっています。そのバリア特性とリシーラブル機能を考慮すると、パウチ包装はこうした利便性主導の加工食品に最適な選択肢として浮上しています。1回分ずつ包装されたパウチは、ポーションコントロールが可能なスナックに特に人気があり、外出の多い消費者のニーズに合致しています。

- 特にアジア太平洋地域では、アセプティック・パウチと並んでレトルト・パウチの人気が急上昇しています。加工食品からペットフードまで幅広い製品向けに設計されたこれらのパウチは、高温処理に耐えるように設計されており、鮮度と品質を長持ちさせる。その多層構造は様々なレベルの保護を提供し、しばしば缶や瓶のような従来の包装を凌駕します。

- 消費者の嗜好は、パウチ包装の需要増加の主な要因です。デザインと素材における継続的な技術革新は、パウチの進化を確実にし、機能性と利便性の向上を提供します。例えば、2023年3月、ライオン株式会社傘下の日本のビューティケアブランドである植物物語は、シャワークリームの詰め替え用として100%リサイクル可能なパウチを発表しました。この革新的なパウチは、テンターフレームの二軸延伸によって製造されたポリエチレンフィルムを使用したモノマテリアルから作られています。

- 優れたバリア性を持つパウチは、内容物を湿気、酸素、光、汚染物質から効果的に遮断し、食品、医薬品、化粧品などの製品の保存期間を延ばします。その軽量性は輸送コストを削減するだけでなく、特にパウチがリサイクル可能な素材を利用するようになっていることから、持続可能性の目標にも合致しています。さらに、パウチには十分なブランド表示スペースがあるため、ブランド・アイデンティティが強化され、棚で製品が目立つようになります。

アジア太平洋地域のパウチ包装市場の動向

無菌パウチ包装が最も速い成長を遂げる

- 飲食品業界からの需要が急増していることが、無菌パウチ包装のニーズを後押しする要因のひとつです。持続可能な包装と賞味期限の延長は、飲食品業界の消費者にとって不可欠です。その結果、飲食品ベンダーは無菌包装に傾斜しています。無菌包装はeコマースの可能性を秘めており、保存期間の延長は消費量の増加と拡大した場所での使用を促進するのに役立ちます。

- 製薬業界は液体薬、点滴薬、その他の無菌製品の包装に無菌パウチを利用しています。需要は主に、無菌状態を維持し、保存期間を延長するための要件によるものです。

- 例えば、2023年2月、無菌バリア包装ソリューションのサプライヤーであるオリバー・ヘルスケア・パッケージング・カンパニーは、マレーシアのジョホール州に新たな製造施設を設立する計画を明らかにしました。この12万2,000平方フィートの施設は、急速に拡大するアジア太平洋地域の顧客基盤に対応するためのものです。パウチ、リッド、ロールストックに特化したこの工場は高度な印刷技術を特徴としており、主にこの地域で急成長している医療機器と製薬の顧客をサポートします。東南アジアにおけるこの戦略的な動きは、シンガポールとマレーシアに製薬会社や医療機器会社が集中していることを利用したもので、オリバー・ヘルスケア・パッケージングの地域的プレゼンスを強化し、ヘルスケア分野におけるサプライチェーンの潜在的課題に積極的に取り組んでいます。

- パウチ包装は小売消費者にとって便利で持ち運びしやすい包装形態であり、重い硬い代替品よりもカーボンフットプリントが低く、eコマース業界でも好まれています。同市場では、牛乳やその他の乳飲料の無菌包装への投資が増加しています。

- 中国国家統計局によると、2023年の中国の牛乳生産量は4,200万トンを記録しました。この生乳生産量の大幅な増加が、乳製品の品質保持と保存期間延長に不可欠なパウチ包装の需要拡大を牽引しています。生乳生産量の増加は、酪農実践の進歩と酪農部門への投資の増加を反映しており、業界全体の成長に寄与しています。

最も高い成長が見込まれるインド

- 食糧生産が不足から余剰へと移行しつつあるインドでは、食品加工を拡大する可能性が大きいです。同国の食品加工部門は最近、目覚ましい成長と利益を経験しており、世界の食品貿易の貢献度を毎年高めています。インベスト・インディアの報告書によると、インドが現在加工しているのは農産物生産量の10%未満であり、加工レベルを向上させ、投資を誘致する大きな機会が生まれています。同報告書はさらに、インドの食品産業は所得の増加、都市化、組織小売の成長などの要因によって、2025~2026年までに5,350億米ドルの生産高を達成すると予測されていると述べています。

- 特に都市部では、調理済み製品やスナック菓子のような加工食品の人気が急上昇しています。2030年までに、インドの加工食品の世帯年間消費量は3倍になると予想され、同国は有利な市場として確立されます。

- 組織化された食品小売店の拡大は極めて重要な役割を果たしており、消費者に魅力的な割引価格で多様な製品を提供しています。インドの食品加工産業は変革期を迎えており、技術的・社会的進歩を取り入れています。したがって、便利ですぐに消費できる製品への需要は、パウチのような効率的で革新的なパッケージング・ソリューションの重要性を強調しています。

- インドの食品加工セクターがこの変革の旅に乗り出す中、先進パッケージング技術の統合は、消費者の進化する需要に応え、同セクターの持続的成長を確保する上で不可欠なものとなっています。

- カナダ農業・農業食品省によると、インドの健康食品・飲食品の小売売上高は2023年に130億米ドルを突破しました。特筆すべきは、自然健康食品(NH)の分野が市場をリードし、金額で60億米ドルを超えたことです。インドの消費者の間で健康食品と飲料が急増していることから、近い将来パウチ包装の需要が高まるとみられます。

アジア太平洋地域のパウチ包装産業の概要

APACでは、パウチ包装セクターは細分化されており、Toppan Holdings Inc.や東洋製罐のような著名な国内企業が、以下のような世界企業と並んで先陣を切っています。 Amcor Group GmbH and Sonoco Products Company. These frontrunners actively pursue strategies like mergers, acquisitions, and product launches to fortify their foothold in the region.

- 2023年8月世界有数の材料科学企業であるダウは、中国の乳製品業界のトップ企業であるMengniuと共同で、リサイクル可能なように特別に作られた先駆的なオールポリエチレン(PE)ヨーグルトパウチを発表しました。この共同努力は、中国の循環型経済を推進する両社の献身を強調するものです。イネートTF-BOPE樹脂によって実現したオールPEパッケージは、乳製品セクターにとって重要なマイルストーンとなります。これは、従来リサイクルが困難であったパッケージをクローズド・ループ・リサイクル・システムに統合することを促進するだけでなく、責任あるリサイクルと機械的リサイクル技術へのコミットメントを強調するものです。最終的に、この動きはより持続可能なパッケージング・ソリューションへの消費者の選択肢を広げることになります。

- 2023年4月インドのパルガールに2つ目の生産工場を設立。この工場は、SIGのバッグ・イン・ボックスとスパウトパウチの製造に特化しており、以前はScholle IPN社やBossar社と提携していました。ムンバイの北90kmに位置する新工場は、様々な生産設備を備えています。これらの設備には、ブローフィルム押出機、射出成形セル、バッグ・イン・ボックス製造機、専用の金型製造設備が含まれます。後者では、バッグ・イン・ボックスとスパウト付きパウチの両方のフィットメントとクロージャーの製造に重点を置いています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 費用対効果の高い包装ソリューションに対する需要の高まり

- 消費者の間での加工インスタント食品の採用増加

- 市場の課題

- 環境に対する関心の高まりとリサイクル施設の不足

- 貿易シナリオ

- EXIMデータ

- 貿易分析(輸出入上位5カ国、価格分析、主要港など)

- 業界の規制と政策、規格

- 技術情勢

- 価格動向分析

- プラスチック樹脂(現在の価格と過去の動向)

- 製品タイプ(主な包装形態)

第6章 市場セグメンテーション

- 材料別

- プラスチック

- ポリエチレン

- ポリプロピレン

- PET

- PVC

- EVOH

- その他樹脂

- 紙

- アルミ

- プラスチック

- タイプ別

- スタンダード

- アセプティック

- レトルト

- ホットフィル

- 製品別

- フラット(ピロー&サイドシール)

- スタンドアップ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品

- 医療・医薬品

- パーソナルケアと家庭用品

- その他のエンドユーザー産業(自動車、化学、農業)

- 食品

- 国別

第1章 中国

第2章 インド

第3章 日本

第4章 タイ

第5章 オーストラリア・ニュージーランド

第6章 インドネシア

第7章 ベトナムベトナム

第8章 その他アジア太平洋地域

第7章 競合情勢

- 企業プロファイル

- Amcor Group GmbH

- Constantia Flexibles Group GmbH

- Scholle IPN Corporation(SIG)

- Sealed Air Corporation(SEE)

- Sonoco Products Company

- Walki Group

- Packman Indsutries

- Logos Packaging Holdings Ltd

- Toppan Package Products Co. Ltd

- Toyo Seikan Co. Ltd

- Huhtamaki Oyj

- Heat Map Analysis

- Competitor Analysis-Emerging vs. Established Players

第8章 リサイクルと持続可能性の展望

第9章 将来の展望

目次

The Asia-Pacific Pouch Packaging Market size is estimated at USD 15.05 billion in 2024, and is expected to reach USD 20.18 billion by 2029, growing at a CAGR of 6.04% during the forecast period (2024-2029). In terms of shipment volume, the market is expected to grow from 180.63 billion units in 2024 to 230.28 billion units by 2029, at a CAGR of 4.98% during the forecast period (2024-2029).

Key Highlights

- Pouch packaging, utilizing materials like plastic films, aluminum foil, or laminates, caters to specific needs such as barrier properties, durability, and visual appeal. Stand-up pouches, designed for products like snacks and liquids, boast a self-supporting base. Conversely, flat pouches cater to compact items like spices, while spouted pouches facilitate easy pouring for liquids such as sauces or baby food. Sealing methods, like heat sealing, ensure meticulous protection from external elements. Some pouches even sport zipper closures, enhancing user convenience and preserving product freshness, all in line with the rising consumer demand for convenience.

- Across the Asia-Pacific region, processed foods, including ready-to-eat meals and snacks, are gaining traction, driven by the region's increasingly busy lifestyles. The World Health Organization notes a significant shift in dietary patterns in Southeast Asia, with a growing preference for highly processed and out-of-home foods. Given their barrier properties and resealable features, pouch packaging emerges as the go-to choice for these convenience-driven processed foods. Single-serving pouches are particularly popular for portion-controlled snacks, aligning well with the needs of on-the-go consumers.

- Notably, in the Asia-Pacific region, retort pouches, alongside aseptic pouches, are witnessing a surge in popularity. These pouches, designed for products ranging from processed meals to pet food, are engineered to endure high-temperature processing, ensuring prolonged freshness and quality. Their multi-layered construction offers varying levels of protection, often outperforming traditional packaging like cans or jars.

- Consumer preferences are a key driver for the rising demand for pouch packaging. Ongoing innovations in design and materials ensure pouches evolve, offering enhanced functionality and convenience. For instance, in March 2023, Shokubutsu Monogatari, a Japanese beauty care brand under Lion Corp., unveiled a 100% recyclable pouch for its shower cream refills. This innovative pouch, crafted from a mono-material, features a polyethylene film produced through tenter-frame biaxial orientation.

- With superior barrier properties, pouches effectively shield their contents from moisture, oxygen, light, and contaminants, extending the shelf life of products like food, pharmaceuticals, and cosmetics. Their lightweight nature not only reduces transportation costs but also aligns with sustainability goals, especially as pouches increasingly utilize recyclable materials. Additionally, the ample branding space on pouches aids in reinforcing brand identity, helping products stand out on shelves.

Asia-Pacific Pouch Packaging Market Trends

Aseptic Pouch Packaging Set to Witness the Fastest Growth

- The rapidly increasing demand from the food and beverage industry is one of the factors expected to drive the need for aseptic pouch packaging. Sustainable packaging and longer shelf life are essential to the consumers of the food and beverage industry. As a result, food and beverage vendors are inclining toward aseptic packaging. Aseptic packaging has the potential for e-commerce, while extended shelf life helps drive higher consumption and use in expanded locations.

- The pharmaceutical industry utilizes aseptic pouches for packaging liquid medications, IV drugs, and other sterile products. The demand is primarily due to the requirement for maintaining sterility and extending shelf life.

- For instance, in February 2023, Oliver Healthcare Packaging Company, a supplier of sterile barrier packaging solutions, revealed plans for establishing a new manufacturing facility in Johor, Malaysia. The 122,000-square-foot facility is set to cater to the rapidly expanding Asia-Pacific customer base. Specializing in pouches, lids, and roll stock, the plant features advanced printing technology, primarily supporting the region's burgeoning medical device and pharmaceutical clients. This strategic move in Southeast Asia capitalizes on the concentration of pharmaceutical and medical device companies in Singapore and Malaysia, reinforcing Oliver Healthcare Packaging's regional presence and proactively addressing potential supply chain challenges in the healthcare sector.

- Pouch packaging offers a convenient and portable package format for retail consumers, which renders a lower carbon footprint than heavy rigid alternatives and is also preferred in the e-commerce industry. The market is witnessing increasing investments in the aseptic packaging of milk and other dairy beverages.

- According to the National Bureau of Statistics of China, in 2023, China produced a record 42 million metric tons of cow's milk. This significant increase in milk production is driving a higher demand for pouch packaging, which is essential for preserving the quality and extending the shelf life of dairy products. The rise in milk output reflects advancements in dairy farming practices and increased investments in the dairy sector, contributing to the overall growth of the industry.

India Anticipated to Witness the Highest Growth

- With India transitioning from scarcity to surplus in food production, the potential for expanding food processing is vast. The country's food processing sector has recently experienced remarkable growth and profits, amplifying its global food trade contribution annually. According to the Invest India report, India currently processes less than 10% of its agricultural output, creating significant opportunities for increased processing levels and attracting investments. The report further stated that the Indian food industry is projected to achieve a USD 535 billion output by 2025-2026, driven by factors like rising incomes, urbanization, and the growth of organized retail.

- Urban areas, particularly, witness a surge in the popularity of processed foods like ready-to-eat products and snacks. By 2030, the annual household consumption of processed foods in India is expected to triple, establishing the country as a lucrative market.

- The expansion of organized food retail outlets plays a pivotal role, offering consumers diverse products with enticing discounts. The food processing industry in India is undergoing a transformative phase, embracing technological and social advancements. Thus, the demand for convenient and ready-to-consume products underscores the significance of efficient and innovative packaging solutions like pouches.

- As the food processing sector in India embarks on this transformative journey, the integration of advanced pouch packaging technologies becomes instrumental in meeting the evolving demands of consumers and ensuring the sector's sustained growth.

- According to Agriculture and Agri-Food Canada, India's retail sales of health and wellness foods and beverages surpassed USD 13 billion in 2023. Notably, the segment of naturally healthy (NH) foods and beverages led the market, exceeding USD 6 billion in value. This surge in healthy food products and drinks among Indian consumers is poised to drive a heightened demand for pouch packaging in the near future.

Asia-Pacific Pouch Packaging Industry Overview

In APAC, the pouch packaging sector is fragmented, spearheaded by prominent domestic entities like Toppan Holdings Inc. and Toyo Seikan Co. Ltd, alongside global players such as Amcor Group GmbH and Sonoco Products Company. These frontrunners actively pursue strategies like mergers, acquisitions, and product launches to fortify their foothold in the region.

- August 2023: Dow, a prominent global materials science firm, collaborated with Mengniu, a top player in China's dairy industry, to introduce a pioneering all-polyethylene (PE) yogurt pouch specifically crafted for recyclability. This joint effort underscores both companies' dedication to advancing China's circular economy. The all-PE packaging, made possible by INNATE TF-BOPE resins, marks a significant milestone for the dairy sector. It not only facilitates the integration of traditionally hard-to-recycle packaging into closed-loop recycling systems but also underscores a commitment to responsible recycling and mechanical recycling technologies. Ultimately, this move broadens consumer choices toward more sustainable packaging solutions.

- April 2023: SIG unveiled its second production facility in Palghar, India. This plant specializes in crafting SIG's bag-in-box and spouted pouch packaging, which were formerly associated with Scholle IPN and Bossar. Situated 90 km north of Mumbai, the new plant is equipped with a range of production assets. These assets include blown film extruders, injection molding cells, bag-in-box manufacturing machines, and a dedicated mold-making facility. The latter focuses on creating fitments and closures for both bag-in-box and spouted pouches.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Cost-effective Packaging Solutions

- 5.1.2 Rising Adoption of Processed Instant Food Among Consumers

- 5.2 Market Challenges

- 5.2.1 Growing Environmental Concern and Lack of Recycling Facilities

- 5.3 Trade Scenario

- 5.3.1 EXIM Data

- 5.3.2 Trade Analysis (Top 5 Import-Export Countries, Price Analysis, and Key Ports, among others.)

- 5.4 Industry Regulations, Policies, and Standards

- 5.5 Technology Landscape

- 5.6 Pricing Trend Analysis

- 5.6.1 Plastic Resins (Current Pricing and Historic Trends)

- 5.6.2 Product Type (Key Packaging Formats)

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastic

- 6.1.1.1 Polyethylene

- 6.1.1.2 Polypropylene

- 6.1.1.3 PET

- 6.1.1.4 PVC

- 6.1.1.5 EVOH

- 6.1.1.6 Other Resins

- 6.1.2 Paper

- 6.1.3 Aluminum

- 6.1.1 Plastic

- 6.2 By Type

- 6.2.1 Standard

- 6.2.2 Aseptic

- 6.2.3 Retort

- 6.2.4 Hot Fill

- 6.3 By Product

- 6.3.1 Flat (Pillow & Side-Seal)

- 6.3.2 Stand-up

- 6.4 By End-User Industry

- 6.4.1 Food

- 6.4.1.1 Candy & Confectionery

- 6.4.1.2 Frozen Foods

- 6.4.1.3 Fresh Produce

- 6.4.1.4 Dairy Products

- 6.4.1.5 Dry Foods

- 6.4.1.6 Meat, Poultry, and Seafood

- 6.4.1.7 Pet Food

- 6.4.1.8 Other Food Products

- 6.4.2 Medical and Pharmaceutical

- 6.4.3 Personal Care and Household Care

- 6.4.4 Other End user Industries (Automotive, Chemical, Agriculture)

- 6.4.1 Food

- 6.5 ByCountry

1 China

2 India

3 Japan

4 Thailand

5 Australia and New Zealand

6 Indonesia

7 Vietnam

8 Rest of Asia-Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Constantia Flexibles Group GmbH

- 7.1.3 Scholle IPN Corporation (SIG)

- 7.1.4 Sealed Air Corporation (SEE)

- 7.1.5 Sonoco Products Company

- 7.1.6 Walki Group

- 7.1.7 Packman Indsutries

- 7.1.8 Logos Packaging Holdings Ltd

- 7.1.9 Toppan Package Products Co. Ltd

- 7.1.10 Toyo Seikan Co. Ltd

- 7.1.11 Huhtamaki Oyj

- 7.2 Heat Map Analysis

- 7.3 Competitor Analysis - Emerging vs. Established Players

8 RECYCLING & SUSTAINABILITY LANDSCAPE

9 FUTURE OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日