ANZパウチ包装:市場シェア分析、産業動向、成長予測(2024~2029年)

ANZ Pouch Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1550284

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

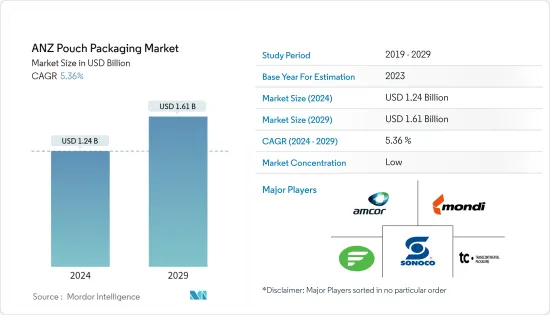

ANZパウチ包装市場規模は2024年に12億4,000万米ドルと推定・予測され、予測期間(2024-2029年)にCAGR 5.36%で成長し、2029年には16億1,000万米ドルに達すると予測されます。

出荷量では、2024年の118億9,000万個から2029年には157億7,000万個に拡大し、予測期間(2024~2029年)のCAGRは5.81%と予測されます。

オーストラリアとニュージーランドのパウチ包装市場は、食品産業からの需要増に牽引され、著しい成長を遂げています。従来の包装と比較したパウチ包装のコスト効率が市場成長を牽引しています。

主なハイライト

- パウチ包装は、輸送中や保管中に温度を調節し、酸素を排除し、湿気を吸収することで製品の鮮度を維持します。ポリエチレンやポリプロピレンのような一般的に使用される素材は、包装の迅速な分解を保証します。その多用途性により、フレキシブル・パッケージングは食品、飲料、パーソナルケア、医薬品など、様々な業界で利用できます。

- 過去10年間で、オーストラリアの人口は急増し、特にプラスチック包装を好む消耗品の需要増につながりました。この嗜好は主にプラスチックの軽量な性質によるもので、携帯性を高めています。消耗品には、飲料、パック詰めされた食事、電子レンジやオーブン対応のオプションを含むコンビニエンス・パッケージが含まれます。このような消費者の嗜好は、パウチ包装の必要性を押し上げるかもしれません。

- オーストラリアは、こうした動向を受けて、野心的な2025年国家包装目標を発表しました。これらの目標は、より持続可能な包装アプローチへの大きな前進であり、市場関係者や政府からの広範な支持を必要としています。2025年目標は包括的なもので、国内のすべての包装活動を対象としており、オーストラリア包装規約機構(APCO)がその実行を主導しています。

- ニュージーランドでは、食料品・食品小売部門が拡大を続けています。米国からの輸入品には、包装食品、ペットフード、食肉などがあります。これにより、同地域のパウチ包装市場のニーズが高まっています。

- さらに、ニュージーランドの小売市場は堅調な売上を維持し、スーパーマーケットと食料品部門が、国のインフレの優勢に後押しされ、主導権を握っています。同地域では、包装市場に課題も見られました。ニュージーランドは2023年、持続的な物流のハードル、金利の上昇、家計支出の増加に直面し、個人消費は減速の兆しを見せました。食料品セクターの収益は2023年に減少しました。

ANZパウチ包装市場の動向

便利なパッケージ製品に対するeコマースからの需要の高まり

- ライフスタイルの変化が同地域のパウチ包装市場を後押ししています。同市場では、シングルサーブや便利な携帯用パックの需要が増加しています。オーストラリアの食品輸出の隆盛は、eコマースの急増とロジスティクスの強化に起因しています。包装市場のブランドは、利便性を重視したブランド体験の強化に軸足を移しています。

- Australia Postの調査によると、eコマース部門は急成長を遂げ、その中には食品と酒類が含まれ、オンライン購入の20.6%のシェアを占め、前年比11.4%増となりました。また、大規模小売店やオンラインマーケットプレースを含む店舗は、オンライン購入の18.1%を占め、前年比8.6%増となりました。

- オーストラリアの製造業者は、便利でフレキシブルなパッケージング・ソリューションを採用するようになってきています。eコマースの急増は、パッケージング市場を再構築し、ゲームチェンジャーとなっています。メーカー各社は、より迅速で安全な製品配送を約束するフレキシブル・パッケージングに関心を寄せています。

- Retail NZによると、2030年までにニュージーランドの小売売上高全体の20%をオンライン購入が占めると予測されています。消費者は、シームレスなショッピング・ジャーニーを期待し、オムニチャネル・リテイリングをますます求めるようになっています。従来の小売企業は、競争力を維持するために、オンライン・プラットフォームを優先し、マーケティングを行う必要があります。顧客とのエンゲージメントに多様なコミュニケーション・チャネルを取り入れることは、標準的な慣行となりつつあります。

- National Australia Bankによると、2024年4月時点の国内小売業者によるオンライン小売支出の年間成長率では、百貨店が38.7%でトップ、次いで個人・娯楽産業が12.6%、食料品・酒類が10.7%となっています。家計は、進化するライフスタイルに合わせるため、硬い包装よりも軟らかい包装を好みます。少人数世帯の増加に伴い、1回分ずつの包装に対する需要が高まっています。

調理済み食品と食品産業が大きな成長を遂げる見込み

- オーストラリアでは、労働人口の増加とワークライフダイナミクスの進化に後押しされて、すぐに食べられる包装食品が人気です。CSIROの報告書によると、調理済みおよび冷凍の包装食の国内消費額は、消費パターンと人口動態の変化を反映して、2030年までに37億米ドルに達すると予測されています。

- オーストラリアが簡便食の生産を拡大するにつれて、フレキシブル包装の需要が急増し、市場の成長に拍車がかかります。スパウトとクロージャーを備えた軟包装パウチは鮮度と風味を保持し、固形・液体食品を幅広く収容します。

- オーストラリアの包装市場は、主にライフスタイルの変化によって後押しされており、携帯用食品パックの需要が顕著に急増しています。さらに、eコマースの台頭も追い風となり、オーストラリアは食品取引における重要なプレーヤーとしての地位を固めつつあります。オーストラリア統計局によると、2020年の食品小売業界の年間売上高は1,515億5,000万豪ドルで、2023年には1,684億5,000万豪ドルに増加します。2004年以降、オーストラリアの食品小売業の売上高は前年比で着実に増加しています。

- 国際通貨基金(IMF)によると、同国の雇用者数は2021年の279万人から297万人に達する見込みです。ニュージーランドの食料品セクターは、3つの主要企業によって支配されています:Foodstuffs New Zealand、Progressive Enterprises(Countdownとして営業)、Warehouse Groupです。これら3社は、国内の食料品小売の90%という驚異的なシェアを占めています。特筆すべきは、独立系、八百屋、小規模コンビニエンスストアが混在していることです。

- 米国農務省によると、物価上昇率が7%と急騰しているため、ニュージーランドの消費者は、食費のかなりの部分を裁量的なものから主食にシフトしています。この調整により、高級品に対する目が肥えてきています。消費者は、ユニークなセールスポイントを提供する商品や、実際の栄養状態や認知された健康状態など、特筆すべき健康上のメリットを誇る商品に引き寄せられるようになっています。ニュージーランドの小売市場は、好調な売上を続けています。ニュージーランドの現在のインフレ環境により、スーパーマーケットや食料品の売上は急速に伸びており、市場の成長も牽引しています。

オーストラリアとニュージーランドのパウチ包装市場

オーストラリアとニュージーランドのパウチ包装市場は断片化されており、Amcor PLC、Mondi PLC、Sonoco Products Company、Transcontinental Packaging New Zealand、Filton Packagingなど多くの国内大手企業が存在します。この地域で事業を展開する企業は、技術革新、提携、買収、合併などを通じて事業の拡大に注力しています。

- 2023年9月、オーストラリアを拠点とする軟包装会社Filton Packagingは、輪郭のあるスリーブや袋のソリューションを国内で提供するAustralian Contour Packaging(ACP)を買収しました。この買収により、Filton Packagingは袋、コンタースリーブ、印刷の製造能力を強化することが期待されます。ACPはフィルトンの広範な製品とサービスを活用し、顧客の要求を満たすことが期待されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- eコマースと便利なパッケージ製品による需要の高まり

- 市場抑制要因

- 包装材料に対するダイナミックで厳しい規制

第6章 業界の規制と政策、規格

第7章 市場セグメンテーション

- 素材タイプ別

- プラスチック

- 紙

- アルミ箔

- 樹脂タイプ別- プラスチック

- ポリエチレン

- ポリプロピレン

- ペット

- PVC

- EVOH

- その他樹脂

- タイプ別

- スタンダード

- アセプティック

- レトルト

- ホットフィル

- 製品別

- フラット(ピロー&サイドシール)

- スタンドアップ

- エンドユーザー産業別

- 食品

- 菓子類

- 冷凍食品

- 生鮮食品

- 乳製品

- 乾物

- 肉、鶏肉、魚介類

- ペットフード

- その他食品(調味料、スパイス、スプレッド類、ソース、コンディメントなど)

- 医療・医薬品

- パーソナルケアと家庭用品

- その他エンドユーザー産業(自動車、化学、農業)

- 食品

- 国別

- オーストラリア

- ニュージーランド

第8章 競合情勢

- 企業プロファイル

- Amcor PLC

- Sonoco Products Company

- Favourite Packaging

- ePac Holdings LLC

- Mondi Plc

- Caspack New Zealand

- Transcontinental Packaging New Zealand

- TotalPak Ltd

- Filton Packaging

- Allflex Packaging

第9章 リサイクルと持続可能性の展望

第10章 将来の展望

目次

The ANZ Pouch Packaging Market size is estimated at USD 1.24 billion in 2024, and is expected to reach USD 1.61 billion by 2029, growing at a CAGR of 5.36% during the forecast period (2024-2029). In terms of shipment volume, the market is expected to grow from 11.89 billion units in 2024 to 15.77 billion units by 2029, at a CAGR of 5.81% during the forecast period (2024-2029).

The pouch packaging market in Australia and New Zealand is witnessing significant growth, driven by increasing demand from the food industry. The cost efficiency of pouch packaging compared to traditional packaging is driving the market growth.

Key Highlights

- Pouch packaging maintains product freshness by regulating temperature, eliminating oxygen, and absorbing moisture during transit or storage. Commonly used materials like polyethylene and polypropylene ensure the packaging breaks down quickly. Its versatility makes flexible packaging accessible across various industries, including food, beverage, personal care, pharmaceutical, and others.

- Over the last decade, Australia's population surged, leading to increased demand for consumables, particularly favoring plastic packaging. This preference is primarily attributed to the lightweight nature of plastic, which bolsters their portability. The consumables include beverages, packaged meals, and convenience packages, including microwave and oven-safe options. Such consumer preferences in the country might push the need for pouch packaging.

- Australia unveiled its ambitious 2025 National Packaging Targets in response to these trends. These targets represent a significant stride toward a more sustainable packaging approach, requiring widespread backing from market players and the government. The 2025 Targets are comprehensive, covering all packaging activities in the nation, with the Australian Packaging Covenant Organisation (APCO) leading the charge in their execution.

- The grocery and food retail sector continues to expand in New Zealand. Imports from the United States include packaged food, pet food, and meat, among others. This would leverage the need for the pouch packaging market in the region.

- Additionally, the retail market in New Zealand sustained robust sales, with supermarkets and grocery segments leading the charge, buoyed by the nation's prevailing inflation. The region also witnessed challenges in the packaging market. New Zealand grappled with persistent logistical hurdles, elevated interest rates, and increased household expenses in 2023, and consumer spending showed signs of moderation. The grocery sector's revenue declined in 2023.

ANZ Pouch Packaging Market Trends

Rising Demand From E-commerce for Convenient Packaging Products

- Lifestyle changes are propelling the pouch packaging market in the region. The market witnessed an increase in demand for single-serve and convenient portable packs. Australia's rising prominence in food exports can be attributed to the surge in e-commerce and enhanced logistics. Brands in the packaging market are pivoting toward enhancing brand experiences, with a notable emphasis on convenience.

- According to a survey by Australia Post, the e-commerce sector witnessed rapid growth, including food and liquor, which accounted for a 20.6% share of online purchases and an 11.4% Y-o-Y increase. Additionally, stores encompassing large retailers and online marketplaces accounted for an 18.1% share of online purchases, marking an 8.6% Y-o-Y increase.

- Manufacturers in Australia are increasingly adopting convenient and flexible packaging solutions. The surge in e-commerce has been a game-changer, reshaping the packaging market. Manufacturers are gravitating toward flexible packaging primarily for its promise of swifter and more secure product deliveries.

- According to Retail NZ, by 2030, online purchases are projected to account for 20% of all retail sales in New Zealand. Consumers increasingly demand omnichannel retailing, expecting a seamless shopping journey. Traditional retailers must pivot, prioritizing and marketing their online platforms to stay competitive. Embracing diverse communication channels for customer engagement is set to become standard practice.

- According to the National Australia Bank, in the annual growth in online retail spending by domestic merchants as of April 2024, the departmental stores took the top position with 38.7%, followed by the personal and recreational industry with 12.6% and grocery and liquor with 10.7%. Households prefer more flexible packaging over rigid options to align with their evolving lifestyles. With the rise of smaller households, the demand for single-serve packaging is increasing.

Ready-to-eat Meals and the Food Industry are Expected to Witness Significant Growth

- Ready-to-eat packaged meals are popular in Australia, driven by the growing working population and evolving work-life dynamics. As per a CSIRO report, the domestic consumption of prepared and frozen packaged meals is projected to be valued at USD 3.7 billion by 2030, reflecting spending patterns and demographic shifts.

- As Australia ramps up its production of convenient meals, the demand for flexible packaging is set to soar, fueling market growth. Flexible packaging pouches equipped with spouts and closures preserve freshness and flavor and accommodate a wide array of solid and liquid food products.

- Australia's packaging market is primarily propelled by shifting lifestyles, with a notable surge in demand for portable food packs. Additionally, bolstered by a rise in e-commerce, Australia is solidifying its position as a critical player in the food trade. According to the Australian Bureau of Statistics, the annual revenue of the food retail industry in 2020 was AUD 151.55 billion, which increased to AUD 168.45 billion in 2023. Since 2004, Australia's food retail revenue has witnessed steady year-on-year growth.

- According to the International Monetary Fund (IMF), the country's employment is expected to reach 2.97 million from 2.79 million in 2021. New Zealand's grocery sector is dominated by three key players: Foodstuffs New Zealand, Progressive Enterprises (operating as Countdown), and the Warehouse Group, the latter resembling a Walmart, with a significant focus on groceries. These three entities command a staggering 90% share of the nation's grocery retail landscape. Notably, the sector is further diversified by a mix of independents, greengrocers, and small convenience stores.

- According to the US Department of Agriculture, with price inflation soaring 7%, consumers in New Zealand are shifting a significant portion of their food spending from discretionary items to staples. This adjustment has led to a more discerning approach to luxury goods. Consumers are gravitating toward products that offer a unique selling point or boast notable health benefits, whether in actual nutrition or perceived well-being. The retail market in New Zealand has continued to show strong sales. Due to New Zealand's current inflationary environment, supermarkets and grocery sales are witnessing rapid growth, driving the market growth as well.

ANZ Pouch Packaging Industry Overview

The pouch packaging market in Australia and New Zealand is fragmented, with the presence of many domestic and major players, such as Amcor PLC, Mondi PLC, Sonoco Products Company, Transcontinental Packaging New Zealand, and Filton Packaging. Companies operating in the region are focused on expanding their business through innovations, collaborations, acquisitions, mergers, etc.

- September 2023: Australia-based flexible packaging company Filton Packaging acquired Australian Contour Packaging (ACP), a domestic provider of contoured sleeves and bag solutions. The deal was expected to help Filton Packaging bolster its manufacturing capacity to produce bags, contour sleeves, and printing work. ACP was expected to leverage Filton's extensive range of products and services to fulfill its customers' requirements.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand from E-commerce and Convenient Packaging Products

- 5.2 Market Restraints

- 5.2.1 Dynamic and Stringent Regulations Against Packaging Materials

6 INDUSTRY REGULATION, POLICY AND STANDARDS

7 MARKET SEGMENTATION

- 7.1 By Material Type

- 7.1.1 Plastic

- 7.1.2 Paper

- 7.1.3 Aluminum Foil

- 7.2 By Resin Type - Plastic

- 7.2.1 Polyethylene

- 7.2.2 Polypropylene

- 7.2.3 PET

- 7.2.4 PVC

- 7.2.5 EVOH

- 7.2.6 Other Resins

- 7.3 By Type

- 7.3.1 Standard

- 7.3.2 Aseptic

- 7.3.3 Retort

- 7.3.4 Hot Fill

- 7.4 By Product

- 7.4.1 Flat (Pillow & Side-Seal)

- 7.4.2 Stand-up

- 7.5 By End-User Industry

- 7.5.1 Food

- 7.5.1.1 Candy & Confectionery

- 7.5.1.2 Frozen Foods

- 7.5.1.3 Fresh Produce

- 7.5.1.4 Dairy Products

- 7.5.1.5 Dry Foods

- 7.5.1.6 Meat, Poultry, And Seafood

- 7.5.1.7 Pet Food

- 7.5.1.8 Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)

- 7.5.2 Medical and Pharmaceutical

- 7.5.3 Personal Care and Household Care

- 7.5.4 Other End user Industries ( Automotive, Chemical, and Agriculture)

- 7.5.1 Food

- 7.6 By Country

- 7.6.1 Australia

- 7.6.2 New Zealand

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Amcor PLC

- 8.1.2 Sonoco Products Company

- 8.1.3 Favourite Packaging

- 8.1.4 ePac Holdings LLC

- 8.1.5 Mondi Plc

- 8.1.6 Caspack New Zealand

- 8.1.7 Transcontinental Packaging New Zealand

- 8.1.8 TotalPak Ltd

- 8.1.9 Filton Packaging

- 8.1.10 Allflex Packaging

9 RECYCLING & SUSTAINABILITY LANDSCAPE

10 FUTURE OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日