アジア太平洋地域の医薬品プラスチックボトル:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

Asia-Pacific Pharmaceutical Plastic Bottles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 121 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549969

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

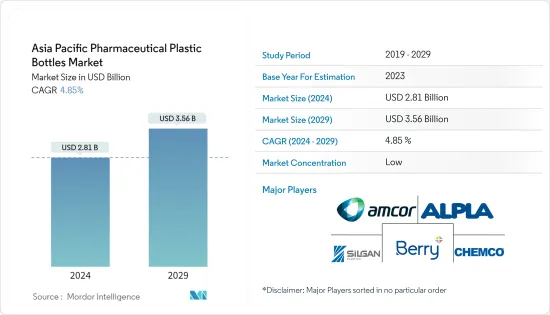

アジア太平洋地域の医薬品プラスチックボトルの市場規模は2024年に28億1,000万米ドルと推定され、2029年には35億6,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは4.85%で成長する見込みです。

主なハイライト

- 中国の医療体制の転換を促進する政策が、医薬品プラスチックボトル市場の成長に寄与すると予想されます。さらに、中国は医薬品包装のインフラと材料を近代化し、医薬品プラスチックボトルの範囲を拡大しており、医薬品包装企業に新たな展望を開く可能性が高いです。例えば、中国政府はいくつかのハイテク分野で世界のリーダーになるための10ヵ年戦略計画を策定する意向です。

- さらに、これらの分野には、従来中国の製造業では重要な分野ではなく、ジェネリック医薬品の生産に関連するバイオテクノロジーも予想外に含まれています。政府はイノベーションを奨励するため、バイオテクノロジーへの投資を大幅に増やし、推進しています。現在、細胞治療や遺伝子治療を含む生物学的に高度な生産は中国東部に限られており、上海、浙江、江蘇の各省にある米国FDA認可の拠点が中心となっています。

- インドは最も人口の多い国で、人口14億人、経済規模は第5位です。製薬産業が発達し、この分野への投資が増加し、人口が拡大し、健康意識が高まり、平均寿命が延びていることから、インドの医薬品包装ソリューション用プラスチックボトル市場は大きく成長すると予想されます。

- 政府は医薬品包装にペットボトルを使用することに厳しい規則を課しています。これはしばらくの間、大きな制約となる可能性があります。これは生産者の利益率に悪影響を及ぼします。しかし、生分解性のために使用される原材料は、非生分解性に比べて高価であり、全体的な生産コストを増加させる。したがって、コスト圧力の増大も市場成長の足かせとなります。

アジア太平洋地域の医薬品プラスチックボトル市場動向

ポリエチレンテレフタレート(PET)が著しい成長を遂げる見込み

- PETボトルは、他のプラスチックに比べて製造工程で処理する原料の量が最も少なくて済むため、メーカーはPETボトルを好みます。PETボトルは色やデザインに多様性があるため、業界関係者の間で人気の選択肢となっています。PETボトルはまた、最高の安全性と品質を提供するため、製薬業界で使用されることが増えています。

- さらに、PETはガラスに比べて製品の重量を最大90%削減できるため、コスト効率の高い輸送プロセスを実現できます。PETボトルは、アジア太平洋地域の医薬品分野で使用されているかさばりやすく壊れやすいガラス瓶に取って代わりつつあります。例えば、PACEとNCLが示しているように、100mlのPETボトル3万本をトラック1台で輸送することが可能であるのに対し、ガラス瓶は1万8千本しか輸送できないです。これは輸送コストと環境負荷を大幅に削減します。

- 中国国家統計局によると、2023年12月現在、中国では毎月およそ698万トンのプラスチック製品が生産されており、2023年4月には639万トンだった。

- プラスチック製品の利用可能性の拡大は、アジア太平洋地域における製薬産業の拡大を支えることができます。製薬会社が事業の拡大や新市場への参入を目指す中、包装資材の安定的かつ潤沢な供給を確保することは極めて重要です。これは、製薬会社が需要の増加に対応し、新たな成長機会を探るのに役立ちます。

大幅な市場成長を占める中国

- 中国の医薬品プラスチックボトル事業は、同国の堅調な医薬品セクターの成長により、多くのビジネスチャンスが期待されます。さらに、中国政府のヘルスケアシステム改革を加速させる取り組みが、医薬品プラスチックボトル事業の成長を促すと予想されています。

- 例えば、中国薬局方2025年版の作成計画により、中国薬局方委員会は2022年6月に46の医薬品包装基準の草案を発表しました。

- 人口の高齢化、ライフスタイルの選択に関連する慢性疾患の有病率の増加、パッケージ化されたヘルスケアの利点に対する国民の意識の高まり、ヘルスケアおよび製薬業界におけるプラスチック包装の需要の高まりが、中国のプラスチック製医薬品包装市場の成長促進要因となっています。

- 中国疾病予防管理センター(CCDC)によると、中国の60歳以上の人口の76.35%が少なくとも1つの慢性疾患を抱えており、37.2%が複数の慢性疾患を抱えています。これらの要因によって国内の医薬品生産が促進され、革新的なプラスチック包装ソリューションの必要性が高まる。

- 最先端の、環境に優しく、安全で、役に立つ、持続可能な包装材料と製品を調査するため、中国の医薬品プラスチックボトル企業による独立研究開発チームの開発が奨励されています。医薬品製造業界における技術革新、協力、買収、生産の増加により、市場価値は上昇しています。

- 中国国家統計局によると、2023年4月の74億1,000万米ドルに対し、2023年12月には96億4,000万米ドルとなった。医薬品小売売上高の増加に伴い、製薬会社は新製品を導入したり、既存の製品ラインを拡大したりする可能性があります。

- また、これには様々な形態や用量の医薬品が含まれる可能性があり、プラスチックボトルを含む様々な包装オプションが必要となります。多様なパッケージング・ソリューションのニーズは、プラスチックボトル市場の成長に貢献する可能性があります。

アジア太平洋地域の医薬品プラスチックボトル産業概要

アジア太平洋地域の医薬品プラスチックボトル市場は断片化されており、Amcor Group GmbH、Silgan Holdings Inc.、Chemco Groupなど多くのプレーヤーが存在します。これらのプレーヤーは、市場を独占するために、M&A、パートナーシップ、新製品の発売、コラボレーションなど、様々な有機的・無機的戦略を採用しています。

2024年1月製薬、バイオテクノロジー、化粧品業界向けのシステムとソリューションの大手プロバイダーであるGerresheimer社は、Software as a Medical Device(SaMD)とデジタル患者支援プログラム(PSP)の世界的スペシャリストであるAptar Digital Health社と提携し、統合がん治療管理ソリューションを共同で開発。

2023年1月Amcorは、上海を拠点とするMDKの買収に合意。MDKの年間売上高は約5,000万米ドルで、主な収益セグメントは医療機器パッケージの供給であり、アムコーにとって重要な成長分野です。現在、中国、インド、日本、東南アジア市場向けに製品を提供する4つの製造拠点から成るアムコーのアジア太平洋地域ヘルスケア包装業界におけるリーダー的地位は、MDK社を加えることで強化されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 医薬品包装の採用拡大が市場の成長を促進

- 小児用包装の需要増加

- 市場抑制要因

- 代替包装ソリューションへのシフト

第6章 市場セグメンテーション

- 原材料別

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- 低密度ポリエチレン(LDPE)

- 高密度ポリエチレン(HDPE)

- タイプ別

- スポイトボトル

- 点鼻薬ボトル

- 液体ボトル

- オーラルケア

- その他のタイプ

- 国別

- 中国

- インド

- 日本

- オーストラリアとニュージーランド

第7章 競合情勢

- 企業プロファイル

- Amcor Group GmbH

- Gerresheimer AG

- Berry Global Inc.

- AptarGroup Inc.

- Alpha Packaging Pvt. Ltd

- ALPLA Werke Alwin Lehner GmbH & Co. KG

- Silgan Holdings Inc.

- Chemco Group

- Supple Pack(India)Private Limited

- LOG Pharma Packaging

- Dongguan Fukang Plastic Products Co. Ltd

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Asia Pacific Pharmaceutical Plastic Bottles Market size is estimated at USD 2.81 billion in 2024, and is expected to reach USD 3.56 billion by 2029, growing at a CAGR of 4.85% during the forecast period (2024-2029).

Key Highlights

- China's policies to expedite the transformation of its medical regime are anticipated to contribute to the growth of the market for pharmaceutical plastic bottles. Additionally, China is modernizing its pharmaceutical packaging infrastructure and materials and expanding its pharmaceutical plastic bottle range, likely opening up new prospects for pharmaceutical packaging companies. For instance, the Government of China intends to develop a 10-year strategic plan to become a world leader in several high-tech sectors.

- Further, these sectors unexpectedly include biotech, which is not traditionally a vital area of Chinese manufacturing, being more associated with generic production. The government has significantly increased its investments in and promoting biotech to encourage innovation. Currently, biologically advanced output, including cell and gene therapy, is limited in Eastern China, focusing on the US FDA-approved sites in the provinces of Shanghai, Zhejiang, and Jiangsu.

- India is the most populous nation, with 1.4 billion inhabitants and the fifth-largest economy. Due to the well-established pharmaceutical industry, rising investments in the sector, the expanding population, increasing health awareness, and rising life expectancy, the market for plastic bottles for pharmaceutical packaging solutions in India is anticipated to grow significantly.

- The government has imposed stringent rules for using plastic bottles in pharmaceutical packaging. This may be a significant constraint for some time. It has a negative effect on the profit margins of the producers. However, the raw materials used for biodegradability are costly compared to non-biodegradability, increasing the overall production cost. Therefore, increasing cost pressures will also hold back the market growth.

Asia-Pacific Pharmaceutical Plastic Bottles Market Trends

Polyethylene Terephthalate (PET) is Expected to Witness Significant Growth

- Manufacturers prefer PET plastic bottles because they require the least amount of raw material to be processed in the manufacturing process compared to other plastics. Due to its versatility in color and design, PET plastic bottles have become a popular choice among industry players. PET plastic bottles also offer the highest safety and quality, so they are increasingly used in the pharmaceutical industry.

- In addition, PET can reduce the product's weight by up to 90% compared to glass, resulting in a more cost-effective transportation process. PET plastic bottles are replacing the bulky and fragile glass bottles used in the pharmaceutical sector in Asia-Pacific. For instance, as indicated by the PACE and the NCL, it is feasible to transport 30,000 100-ml PET bottles in a single truck, compared to only 18,000 glass bottles. This significantly reduces transportation costs and environmental impact.

- According to the National Bureau of Statistics of China, as of December 2023, China produced roughly 6.98 million metric tons of plastic products every month, compared to 6.39 million metric tons in April 2023.

- The growing availability of plastic products can support the expansion of the pharmaceutical industry in Asia-Pacific. As pharmaceutical companies look to expand their operations and enter new markets, ensuring a stable and ample supply of packaging materials is crucial. This can help pharmaceutical companies meet increasing demand and explore new growth opportunities.

China to Account for Significant Market Growth

- Pharmaceutical plastic bottle businesses in China are expected to have many business opportunities due to the country's robust pharmaceutical sector growth. Additionally, the Chinese government's initiatives to quicken the nation's healthcare system reform are anticipated to encourage the growth of the pharmaceutical plastic bottle business.

- For instance, by the plan for creating the Chinese Pharmacopoeia 2025 Edition, the Chinese Pharmacopoeia Commission published the drafts of 46 pharmaceutical packaging standards in June 2022.

- The aging population, the increasing prevalence of chronic diseases associated with lifestyle choices, the growing public awareness of packaged healthcare benefits, and the growing demand for plastic packaging within the healthcare and pharmaceutical industries are the key drivers of the Chinese plastic pharmaceutical packaging market growth.

- According to the China Center for Disease Control and Prevention (CCDC), 76.35% of China's population aged 60 or over had at least one chronic disease, while 37.2% had multiple chronic diseases. These factors will drive domestic pharmaceutical production, thus increasing the need for innovative plastic packaging solutions.

- The development of independent research and development teams by China's pharmaceutical plastic bottle companies is encouraged to investigate cutting-edge, environmentally friendly, secure, helpful, and sustainable packaging materials and products. The market value has increased due to the growing innovation, collaboration, acquisition, and production in the drug manufacturing industry.

- According to the National Bureau of Statistics of China, retail trade medicine revenue in China was USD 9.64 billion in December 2023, compared to USD 7.41 billion in April 2023. With the growth in retail trade medicine revenue, pharmaceutical companies may introduce new products or expand their existing product lines.

- Also, this could include medications in various forms and dosages, which would require a range of packaging options, including plastic bottles. The need for diverse packaging solutions can contribute to the growth of the plastic bottles market.

Asia-Pacific Pharmaceutical Plastic Bottles Industry Overview

The Asia-Pacific pharmaceutical plastic bottles market is fragmented, with many players like Amcor Group GmbH, Silgan Holdings Inc., and Chemco Group. These players have adopted various organic and inorganic strategies to dominate the market, such as mergers and acquisitions, partnerships, new product launches, and collaborations.

January 2024: Gerresheimer, a leading provider of systems and solutions for the pharma, biotech, and cosmetics industries, partnered with Aptar Digital Health, a global specialist in Software as a Medical Device (SaMD) and digital Patient Support Programs (PSPs), to jointly create an integrated cancer therapy management solution.

January 2023: Amcor agreed to acquire MDK, based in Shanghai. MDK's yearly sales amount to around USD 50 million, and its primary revenue segment is the supply of medical device packaging, a critical growth area for Amcor. Amcor's leadership position in a broader Asian-Pacific healthcare packaging industry, now consisting of four manufacturing sites offering products to China, India, Japan, and Southeast Asia markets, will be strengthened by adding MDK.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyer

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Expanding Pharmaceutical Packaging Adoption Fuels Growth of the Market

- 5.1.2 Rising Demand for Child-Resistant Packaging

- 5.2 Market Restraints

- 5.2.1 Shifting Towards Alternative Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Raw Material

- 6.1.1 Polyethylene Terephthalate (PET)

- 6.1.2 Polypropylene (PP)

- 6.1.3 Low-density Polyethylene (LDPE)

- 6.1.4 High-density Polyethylene (HDPE)

- 6.2 By Type

- 6.2.1 Dropper Bottles

- 6.2.2 Nasal Spray Bottles

- 6.2.3 Liquid Bottles

- 6.2.4 Oral Care

- 6.2.5 Other Types

- 6.3 By Country

- 6.3.1 China

- 6.3.2 India

- 6.3.3 Japan

- 6.3.4 Australia and New Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Gerresheimer AG

- 7.1.3 Berry Global Inc.

- 7.1.4 AptarGroup Inc.

- 7.1.5 Alpha Packaging Pvt. Ltd

- 7.1.6 ALPLA Werke Alwin Lehner GmbH & Co. KG

- 7.1.7 Silgan Holdings Inc.

- 7.1.8 Chemco Group

- 7.1.9 Supple Pack (India) Private Limited

- 7.1.10 LOG Pharma Packaging

- 7.1.11 Dongguan Fukang Plastic Products Co. Ltd

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 121 Pages

- 納期

- 2~3営業日