|

市場調査レポート

商品コード

1549883

アジア太平洋地域のデータセンター向けストレージ:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Asia-Pacific Data Center Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のデータセンター向けストレージ:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

アジア太平洋地域のデータセンター向けストレージ市場規模は、2024年に158億米ドルと推定され、2029年には228億米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは7.80%で成長する見込みです。

アジアのデジタル環境は近年成長し、製造自動化からeコマース・プラットフォーム、デジタル決済に至るまで、幅広いイノベーションを包含しています。COVID-19の大流行直前には、この地域がデジタル・コンピュータ技術の特許の60%を占め、20年前の40%から上昇しました。東南アジアのデジタル経済は、4億6,000万人を超えるデジタル消費者、テクノロジーに精通した若年層、インターネット普及率の上昇など、強力なファンダメンタルズに支えられ、成長の可能性を十分に秘めています。全体として、デジタル化の進展は大規模なデータセンター建設につながり、ストレージ需要を牽引しています。

主なハイライト

- アジア太平洋地域のデータセンター市場の今後のIT負荷容量は、2029年までに2万3,000万kWに達すると予想されます。

- 同地域の床面積は2029年までに7,450万平方フィートに増加する見込み。

- 同地域で設置されるラックの総数は、2029年までに420万ユニットに達する見込みです。2029年までに最大数のラックが設置されるのはインドです。

- アジア太平洋地域を結ぶ海底ケーブルシステムは160近くあり、その多くが建設中です。2024年にサービス開始が予定されているそのような海底ケーブルのひとつが、東南アジア-日本ケーブル2(SJC2)で、中国、台湾、日本、韓国、タイ、ベトナムを陸揚げ点とする10,500km以上に及ぶ。

アジア太平洋地域のデータセンター向けストレージ市場動向

ITと電気通信が大きなシェアを占める

- 5Gネットワークの展開によりデジタル経済が強化され、高容量データセンター向けストレージ・インフラへの需要が高まると予想されます。5Gの登場により、通信速度の大幅な向上、低遅延、予想外のレベルのネットワーク機能がもたらされると期待されています。

- アジア太平洋地域では、ハイパーコネクティビティ環境は、消費者や企業のコネクティビティとコラボレーションのニーズをサポートする上で基礎的な役割を果たす通信事業者の重要性を強化しています。アジア太平洋地域全体では、通信事業者の75%がプラス成長を記録しました。韓国は、通信市場の成熟度ランキングで香港に次いで世界第2位です。

- 韓国はまた、6Gを含む最新の通信技術開発の最先端を走っています。2022年11月、マレーシアの通信会社CelcomとDiGiは合併契約を承認しました。両社が完全に合併すれば、新会社は2,000万人以上の加入者を抱えるマレーシア最大級の通信事業者となります。

- アジア太平洋地域における5Gの登場は、高速ネットワーク接続のためのスモールセル展開を加速させました。多くの国が、新しいスモールセルを展開する際に適用できる免責基準を設けています。最もエネルギーを消費するデータセンターのいくつかは、ユーザーとウェブサービス間の通信を促進するサーバーファームです。APACでは現在、ほとんどのストレージ・サーバーがソリッド・ステート・ドライブ(SSD)を使用しており、フラッシュ・ストレージを使用して高速で高スループットのデータ要求に対応しています。

- 5Gは4Gに比べてスループットが7倍近く向上しており、1.45Gbsに対して10Gbsです。HDDを超えるNVMeまたはSSDでは、このようなエンタープライズレベルの技術により、大幅なI/Oスループットが可能になります。NVMeの需要は、SSDサーバーやストレージアプライアンスで増加しており、予測期間中に市場を牽引すると予想されます。

著しい成長を遂げる中国

- 近年、中国はデータセンター分野に大きな関心を寄せています。これにより、経済的なインパクトと技術的な先進性を併せ持つデータセンター・エコシステムが形成されています。ユーザーがクラウドサービスを選ぶ理由は、ビジネス要件に応じてネットワーク・ストレージの数を増やせる拡張性の高さにあります。例えば、中国の独身の日のようなお祭りでは、ウェブサイトが掲載する魅力的なオファーによって、膨大な量のウェブサイト・トラフィックと金融取引が誘引されます。

- クラウド・コンピューティングはウェブベースのインフラを提供し、追加コンピューティングや情報ストレージなどのサービスがクライアントに提供されます。クラウド・インフラストラクチャは、データセンターに大規模なサーバー・ファームやストレージ・システムを配置する従来のシステムよりも比較的安価です。

- 銀行のデータセンターは生命線です。金融サービスを提供するための重要なインフラです。コア・システムとフロント・エンド・システム、決済の維持、カード交換、モバイル・バンキング、Eバンキング、カウンター・サービス、クレジットカード・システムなどが含まれます。金融機関はフラッシュディスクを好んで情報化に取り組んでいます。

- 最近、中国中信銀行(CCB)は、従来のストレージをファーウェイのハイエンド・ストレージ「OceanStor Dorado」に置き換えました。

- 多くの企業がデータセンターの拡張に絶えず投資しており、データセンター・アプリケーションで使用されるフラッシュ・メモリー・デバイスの市場機会を生み出すと期待されています。例えばGLP Pteは、デジタルインフラ資産に対する投資家の需要が高まる中、中国におけるデータセンター・プラットフォームの拡大を支援するため、2022年2月に5億米ドルの新規資金を調達しました。同社によると、この取引によって中国のデータセンターは40億米ドルから50億米ドルの価値を持つ可能性があるといいます。このような投資は、市場を前進させると予測されます。

- さらにチャイナモバイルは2022年12月、1,000社以上のパートナーを獲得した後、データセンターへの投資を拡大すると発表しました。また、深センの中国科学院計算技術研究所や彭城研究所と協力してデータセンター・インフラを構築しています。このような投資は、国のデータセンター・インフラ活動を推進し、ストレージベースのデバイスの設置を必要とすると予想されています。

アジア太平洋地域のデータセンター向けストレージ産業の概要

アジア太平洋地域のデータセンター向けストレージ市場は、プレーヤー間で細分化されており、近年競争力を増しています。主なプレイヤーには、Dell Inc.、Hewlett Packard Enterprise、NetApp Inc.などがいます。市場シェア上位の大手企業は、アジア全域での顧客基盤の拡大に注力しています。戦略的な協業イニシアティブを活用し、市場シェアと収益性を高めています。例えば

- 2024年3月ピュア・ストレージは先進的なデータ・ストレージ・テクノロジーとサービスを発表しました。同社は、Pure1ストレージ管理プラットフォームとEvergreenポートフォリオに新たなセルフサービス機能を追加し、単一のプラットフォーム・エクスペリエンスを通じてソフトウェアベースのソリューションを世界顧客に提供すると発表しました。

- 2023年2月NetApp Inc.は、低価格なオールフラッシュストレージを実現する新しい容量型フラッシュストレージファミリ「NetApp AFF C-Series」と、オールフラッシュシステムファミリ「AFF A-Series」の新しいエントリレベルストレージシステム「NetApp AFF A150」の提供を開始すると発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- デジタル化の進展とデータ中心アプリケーションの出現

- エンドユーザーにおけるクラウドアプリケーションの増加

- 市場抑制要因

- 互換性と最適ストレージ性能の問題

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- ストレージ技術別

- ネットワーク接続ストレージ(NAS)

- ストレージ・エリア・ネットワーク(SAN)

- ダイレクト・アタッチド・ストレージ(DAS)

- その他の技術

- ストレージタイプ別

- 従来型ストレージ

- オールフラッシュ・ストレージ

- ハイブリッド・ストレージ

- エンドユーザー別

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他エンドユーザー

- 国別

- インドネシア

- インド

- 中国

- オーストラリア

- 韓国

- フィリピン

- タイ

- シンガポール

- ニュージーランド

- 日本

- マレーシア

- ベトナム

- 香港

- 台湾

第6章 競合情勢

- 企業プロファイル

- Dell Inc.

- Hewlett Packard Enterprise

- NetApp Inc.

- Hitachi Vantara LLC

- Kingston Technology Company Inc.

- Pure Storage Inc.

- Lenovo Group Limited

- Fujitsu Limited

- Oracle Corporation

- Seagate Technology LLC

- Huawei Technologies Co. Ltd

- KIOXIA Singapore Pte. Ltd

- Nutanix Inc.

- Western Digital Corporation

第7章 投資分析

第8章 市場機会と今後の動向

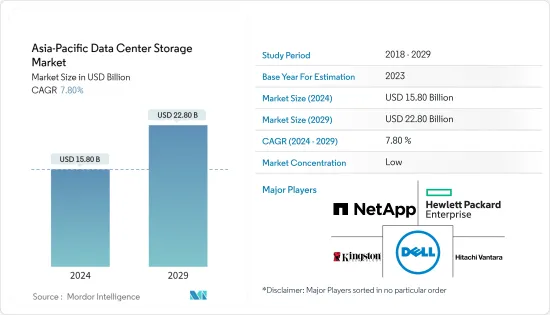

The Asia-Pacific Data Center Storage Market size is estimated at USD 15.80 billion in 2024, and is expected to reach USD 22.80 billion by 2029, growing at a CAGR of 7.80% during the forecast period (2024-2029).

Asia's digital landscape has grown in recent years, encompassing a broad range of innovations, from manufacturing automation to e-commerce platforms, all the way to digital payments. The region accounted for 60% of patents in digital and computer technologies right before the COVID-19 pandemic, up from 40% two decades earlier. Southeast Asia's digital economy has plenty of growth potential, backed by strong fundamentals including over 460 million digital consumers, young and tech-savvy populations, as well as rising internet penetration. Overall, the increasing digitization is leading to major data center construction, driving the demand for storage.

Key Highlights

- The upcoming IT load capacity of the Asia-Pacific data center market is expected to reach 23k MW by 2029.

- The region's construction of raised floor area is expected to increase to 74.5 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 4.2 million units by 2029. India is expected to house the maximum number of racks by 2029.

- There are close to 160 submarine cable systems connecting the Asia-Pacific, and many are under construction. One such submarine cable that is estimated to start service in 2024 is Southeast Asia-Japan Cable 2 (SJC2), which stretches over 10,500 kilometers with landing points in China, Taiwan, Japan, South Korea, Thailand, and Vietnam.

Asia-Pacific Data Center Storage Market Trends

IT and Telecom to Hold Significant Share

- The rollout of 5G networks is expected to strengthen the digital economy and increase demand for high data center storage infrastructure. The arrival of 5G is expected to bring a major increase in speeds, low latencies, and an unforeseen level of network capabilities.

- In Asia-Pacific, the hyper-connectivity environment has reinforced the importance of telcos, which play a foundational role in supporting consumers' and enterprises' connectivity and collaboration needs. Across Asia-Pacific, 75% of the operators registered positive revenue growth. South Korea is second only to Hong Kong in the world rankings of telecom market maturity.

- South Korea is also on the leading edge of the latest telecom technology developments, including around 6G. In November 2022, Malaysian telcos Celcom and DiGi approved the merger agreement. Once the two companies are fully merged, the new entity will be one of the largest carriers in Malaysia, with over 20 million subscribers.

- The advent of 5G in Asia-Pacific accelerated small-cell deployment for high-speed network connectivity. Many nations have created exemption standards that can be applied when deploying new small cells. Some of the most energy-intensive data centers are server farms facilitating communication between users and web services. In APAC, most storage servers now use solid-state drives (SSDs), which use flash storage to handle high-throughput data requests at high speeds.

- 5G is close to seven times better in terms of throughput compared to 4G, at 10 Gbs compared to 1.45 Gbs. With NVMe or SSD over HDD, such enterprise-level technology allows significant I/O throughput. The demand for NVMe is increasing in SSD servers and storage appliances which is expected to drive the market during the forecast period.

China to Witness Significant Growth

- In recent years, China has focused much attention on its data center sector. This has given rise to a data center ecosystem that is both economically impactful and technologically advanced. Users opt for cloud services due to increased scalability, wherein they can increase the number of network storage based on the business requirement. For instance, during festivals such as China Singles Day, the attractive offers listed by the websites entice huge amounts of website traffic and financial transactions, which are easily managed, and the cloud infrastructure ensures performance.

- Cloud computing provides web-based infrastructure, wherein services such as additional computing and information storage are delivered to the clients. The cloud infrastructure is comparatively cheaper than the traditional system, wherein sizeable server farms and storage systems are allocated in a data center.

- A bank's data center is its lifeline. It is a key infrastructure for carrying financial services. It includes the core and front-end systems, keeping payments, card exchanges, mobile banking, e-banking, counter services, and the credit card system. Financial institutions prefer flash disks to undertake informatization.

- Recently, China CITIC Bank (CCB) replaced its traditional storage with Huawei's high-end OceanStor Dorado all-flash storage system, marking the beginning of CCB's journey to building an advanced digital commercial bank.

- Many businesses are constantly investing in data center expansion, which is expected to create market opportunities for flash memory devices used in data center applications. GLP Pte, for example, raised USD 500 million in new funds in February 2022 to help expand its data center platform in China amid rising investor demand for digital infrastructure assets. According to the company, the transaction could value China data centers between USD 4 billion and USD 5 billion. Such investments are projected to propel the market forward.

- Furthermore, China Mobile announced in December 2022 that it is increasing its investments in data centers after gaining over 1,000 partners. It has also worked with the Chinese Academy of Sciences' Institute of Computing Technology and Peng Cheng Laboratory in Shenzhen to build data center infrastructure. Such investments are anticipated to propel the nation's data center infrastructure activities, necessitating the installation of storage-based devices.

Asia-Pacific Data Center Storage Industry Overview

The data center storage market in Asia-Pacific is fragmented among the players and has gained a competitive edge in recent years. Some of the major players are Dell Inc., Hewlett Packard Enterprise, and NetApp Inc. Major players with a prominent market share focus on expanding their customer base across the region. They leverage strategic collaborative initiatives to increase their market share and profitability. For instance,

- March 2024: Pure Storage launched advanced data storage technologies and services. The company announced new self-service capabilities across its Pure1 storage management platform and Evergreen portfolio, offering software-based solutions, all via a single platform experience, to global customers.

- February 2023: NetApp Inc. announced the upcoming availability of the NetApp AFF C-Series, a new family of capacity flash storage options that deliver lower-cost all-flash storage, and NetApp AFF A150, a new entry-level storage system in the AFF A-Series family of all-flash systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Digitalization and Emergence of Data-centric Applications

- 4.2.2 Rising Cloud Applications Among End-Users

- 4.3 Market Restraints

- 4.3.1 Compatibility and Optimum Storage Performance Issues

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Storage Technology

- 5.1.1 Network Attached Storage (NAS)

- 5.1.2 Storage Area Network (SAN)

- 5.1.3 Direct Attached Storage (DAS)

- 5.1.4 Other Technologies

- 5.2 By Storage Type

- 5.2.1 Traditional Storage

- 5.2.2 All-Flash Storage

- 5.2.3 Hybrid Storage

- 5.3 By End User

- 5.3.1 IT & Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Media & Entertainment

- 5.3.5 Other End Users

- 5.4 By Country

- 5.4.1 Indonesia

- 5.4.2 India

- 5.4.3 China

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 Philippines

- 5.4.7 Thailand

- 5.4.8 Singapore

- 5.4.9 New Zealand

- 5.4.10 Japan

- 5.4.11 Malaysia

- 5.4.12 Vietnam

- 5.4.13 Hong Kong

- 5.4.14 Taiwan

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Hewlett Packard Enterprise

- 6.1.3 NetApp Inc.

- 6.1.4 Hitachi Vantara LLC

- 6.1.5 Kingston Technology Company Inc.

- 6.1.6 Pure Storage Inc.

- 6.1.7 Lenovo Group Limited

- 6.1.8 Fujitsu Limited

- 6.1.9 Oracle Corporation

- 6.1.10 Seagate Technology LLC

- 6.1.11 Huawei Technologies Co. Ltd

- 6.1.12 KIOXIA Singapore Pte. Ltd

- 6.1.13 Nutanix Inc.

- 6.1.14 Western Digital Corporation