|

市場調査レポート

商品コード

1549857

中東のデータセンター向けストレージ:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Middle East Data Center Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東のデータセンター向けストレージ:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

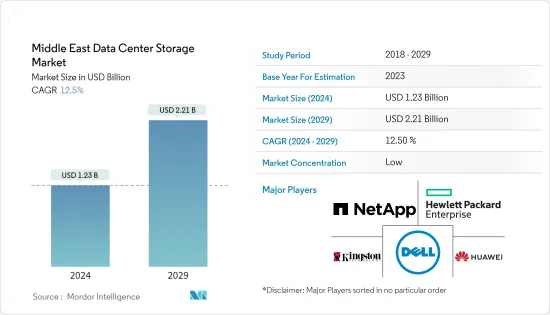

中東のデータセンター向けストレージ市場規模は2024年に12億3,000万米ドルと推定され、2029年には22億1,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは12.5%で成長する見込みです。

中東のデジタル経済は2030年までに約7,800億米ドルまで成長すると予測されており、10年後までの世界平均を大きく上回ると思われます。アラブ首長国連邦は中東最大のデータセンター・ハブの1つであり、さらなるデータセンターの建設が計画されています。2026年までに最大10億米ドルの追加投資が予測されています。2019年、Microsoft Azureはドバイとアブダビで2つのクラウド地域を立ち上げました。クラウドベースのモデルであるSaaSは、柔軟性、拡張性、コスト効率に優れたソフトウェア・ソリューションを提供し、中東の進化するビジネス要件に合わせて迅速に展開することができます。このような要因が市場の需要拡大につながっています。

主なハイライト

- 中東のデータセンター市場の今後のIT負荷容量は、2029年までに2,059.5MWに達すると予想されます。

- 同地域の床面積は2029年までに970万平方フィートに増加すると予想されます。

- 同地域の総設置ラック数は2029年までに49万6,000ユニットに達する見込みです。サウジアラビアは2029年までに最大数のラックを設置する見込みです。

- 中東を結ぶ海底ケーブルシステムは26近くあり、その多くが建設中です。2024年にサービス開始が見込まれる海底ケーブルのひとつがBlueで、テルアビブを陸揚げ点とする全長4,696キロメートルに及ぶ。

中東のデータセンター向けストレージ市場動向

ITと電気通信が大きなシェアを占める

- 同市場の特徴は、スケーラビリティと俊敏性を高めるソフトウェア定義インフラへのシフトです。シームレスな接続性への需要が高まる中、通信事業者はストレージ機器の持続的な拡大を図っています。

- 5Gネットワークの展開によりデジタル経済が強化され、データセンター向けストレージ・インフラへの需要が高まると予想されます。5Gの登場により、通信速度の大幅な向上、低遅延、予想外のレベルのネットワーク機能がもたらされると予想されます。これにより、さらに高度で斬新なアプリケーションが登場し、あらゆるものがリアルタイムでよりつながるようになると思われます。

- テレコム・サプライヤーは、4Gの急速な普及と差し迫った5Gの波によって、データセンター事業への投資を後押しされています。アラブ首長国連邦(UAE)の通信規制庁によると、2022年3月現在の携帯電話加入者数は約1,870万人。この数字は、2020年12月からわずかに増加しています。

- エリクソンのMobility 2020の試算によると、2025年までにMENAで8,000万人の5G顧客が存在する可能性があります。このような普及は、この地域の企業やその他の技術進歩に恩恵をもたらし、スマートシティや世界の通信の基礎を築く。さらに、アラブ首長国連邦の通信当局は、ネットワーク・システムで中東の技術的に卓越したプレーヤーになるために、2025年までに同国で5Gを100%普及させるという野心的な目標を設定しました。

- 5Gは4Gに比べてスループットが7倍近く向上し、1.45Gbsに対して10Gbsとなります。NVMeやSSD over HDDでは、このようなエンタープライズ・レベルの技術によって、大幅なi/Oスループットが可能になります。NVMeの需要は、SSDサーバーやストレージアプライアンスで増加することが予想され、予測期間中の市場の牽引役となることが期待されます。

著しい成長を遂げるサウジアラビア

- 企業で生成されるデータの増加とクラウド技術の採用拡大が、サウジアラビアでの市場調査を促進すると予測されます。クラウドベースの急速な技術導入は、同国のデジタル移行を加速させるとともに、膨大なデータの保護にも貢献すると予測されます。

- グーグルやオラクルといったクラウドプロバイダーからの魅力的な投資により、データセンター事業は活気を取り戻し始めています。例えば、オラクルはNEOM Tech &Digital Holding Co.と共同で、サウジ・ビジョン2030に対応するNEOMのハイパースケール・データセンターの最初のテナントとして入居します。このデータセンターにはオラクル・クラウド・インフラストラクチャー(OCI)が設置され、クラウドサービスのための高性能で弾力性のあるプラットフォームが提供されます。

- サウジアラビア政府はこの需要を認識し、ビジョン2030の柱としてAIを掲げています。これは、知識集約型社会への進化、石油ベースの経済の多様化、技術開発の世界的ハブとなることを目指す同国の戦略の一環です。

- ビジョン2030の戦略目標の約70%はAIと密接に関連しています。その使命を達成するため、サウジアラビアは技術力を向上させ、2030年までにAIを活用した国内のデジタルエコシステムを構築するための協調的な取り組みを主導しています。データと人工知能のための国家戦略(NSDAI)は、2030年までに200億米ドルの海外および国内投資の誘致を目指します。

- サウジ・ビジョン2030では、特にテクノロジー分野での外国投資が奨励されています。2019年のクラウドファースト戦略の実施により、インダストリアル4.0のためのAIなどの革新的技術の導入も加速しました。通信技術情報委員会が採択したクラウド・コンピューティング規制枠組みは、国内のクラウド・コンピューティング・サービスを改善し、規制の開放性を促進することを意図しています。全体として、AIやその他の技術によるビッグデータ量の増加に伴い、データセンター建設の需要が増加し、ストレージ機器の主要な採用につながると予想されます。

中東のデータセンター向けストレージ産業の概要

中東のデータセンター向けストレージ市場はプレイヤー間で細分化されており、近年は競争力を獲得しています。主なプレイヤーとしては、Dell Inc.、Hewlett Packard Enterprise、NetApp Inc.などが挙げられます。圧倒的な市場シェアを誇るこれらの大手企業は、地域全体の顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的な協業イニシアティブを活用しています。例えば

- 2024年3月:ウエスタンデジタルは、NAS(ネットワーク接続ストレージ)用途に特化した24TB WD Red Proメカニカル・ハードディスク・ドライブのイントロダクションを発表し、製品ラインアップを拡充しました。同社は先に、エンタープライズおよびデータセンターでの使用をターゲットとした24TBモデルを発売しています。

- 2024年3月ピュア・ストレージが先進のデータ・ストレージ・テクノロジーとサービスを発表。Pure1ストレージ管理プラットフォームとEvergreenポートフォリオに新たなセルフサービス機能を追加し、単一のプラットフォーム・エクスペリエンスを通じてソフトウェアベースのソリューションを世界中の顧客に提供すると発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- デジタル化の進展とデータ中心アプリケーションの出現

- エンドユーザーにおけるクラウドアプリケーションの増加

- 市場抑制要因

- 互換性と最適ストレージ性能の問題

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- ストレージ技術別

- ネットワーク接続ストレージ(NAS)

- ストレージ・エリア・ネットワーク(SAN)

- ダイレクト・アタッチド・ストレージ(DAS)

- その他の技術

- ストレージタイプ別

- 従来型ストレージ

- オールフラッシュ・ストレージ

- ハイブリッド・ストレージ

- エンドユーザー別

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他エンドユーザー

- 国別

- イスラエル

- サウジアラビア

- アラブ首長国連邦

第6章 競合情勢

- 企業プロファイル

- Dell Inc.

- Hewlett Packard Enterprise

- NetApp Inc.

- Huawei Technologies Co. Ltd

- Kingston Technology Company Inc.

- Pure Storage Inc.

- Nutanix Inc.

- Lenovo Group Limited

- IBM Corporation

- SMART Modular Technologies Inc.

- Infinidat Ltd

- IBM Corporation

- Zadara Inc.

- Western Digital Corporation

第7章 投資分析

第8章 市場機会と今後の動向

The Middle East Data Center Storage Market size is estimated at USD 1.23 billion in 2024, and is expected to reach USD 2.21 billion by 2029, growing at a CAGR of 12.5% during the forecast period (2024-2029).

The Middle East digital economy is projected to grow to about USD 780 billion by 2030, which would significantly outpace the global average through the end of the decade. The United Arab Emirates is one of the largest data center hubs in the Middle East, with the construction of more data centers planned. Upto USD 1 billion in additional investments are projected by 2026. In 2019, Microsoft Azure launched two cloud regions in Dubai and Abu Dhabi. SaaS, being a cloud-based model, provides flexible, scalable, and cost-effective software solutions that can be quickly deployed and aligned with evolving business requirements in the Middle East. Such factors are leading to the growth in market demand.

Key Highlights

- The upcoming IT load capacity of the Middle East data center market is expected to reach 2,059.5 MW by 2029.

- The region's construction of raised floor area is expected to increase to 9.7 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 496K units by 2029. Saudi Arabia is expected to house the maximum number of racks by 2029.

- There are close to 26 submarine cable systems connecting the Middle East, and many are under construction. One such submarine cable that is estimated to start service in 2024 is Blue, which stretches over 4,696 kilometers with a landing point in Tel Aviv.

Middle East Data Center Storage Market Trends

IT and Telecom to Hold Significant Share

- The market is characterized by a shift toward software-defined infrastructure, enhancing scalability and agility. As the demand for seamless connectivity rises, telecom companies are poised for sustained expansion in storage equipment.

- The rollout of 5G networks is expected to strengthen the digital economy and increase demand for data center storage infrastructure. The arrival of 5G is expected to bring a major increase in speeds, low latencies, and an unforeseen level of network capabilities. This will set the stage for even more advanced and novel applications, enabling everything to be more connected in real-time.

- Telecom suppliers are encouraged to invest in the data center business by quickly rising 4G adoption and the impending 5G wave. In the United Arab Emirates, there were about 18.7 million active mobile phone subscribers as of March 2022, according to the UAE Telecommunications Regulatory Authority. This figure shows a slight rise from December 2020.

- According to an Ericsson Mobility 2020 estimate, there are likely to be 80 million 5G customers in MENA by 2025. This widespread use benefits companies and other technological advancements in the region and lays the groundwork for smart cities and worldwide communication. Furthermore, the telecom authority in the United Arab Emirates set an ambitious objective of 100% 5G penetration in the country by 2025 in order to become the Middle East's technically prominent player in the networking system.

- 5G is close to seven times better in terms of throughput compared to 4G, at 10 Gbs compared to 1.45 Gbs. With NVMe or SSD over HDD, such enterprise-level technology allows significant I/O throughput. The demand for NVMe is expected to increase in SSD servers and storage appliances, which is expected to drive the market during the forecast period.

Saudi Arabia to Witness Significant Growth

- The growth in data generated by the enterprise, coupled with the growing adoption of cloud technology, is expected to drive market studied in Saudi Arabia. Rapid cloud-based technology adoption is projected to help accelerate the country's digital transition while protecting mountains of data.

- With enticing investments from cloud providers such as Google and Oracle, the data center business has started to pick up steam. For instance, Oracle will work with NEOM Tech & Digital Holding Co. as the first tenant in the hyperscale data center at NEOM to serve Saudi Vision 2030. The data center will house Oracle Cloud Infrastructure (OCI), which would offer a high-performing, resilient platform for cloud services.

- The Saudi government has recognized the demand and accordingly outlined AI as a pillar of Vision 2030. This is part of the country's strategy to evolve into a knowledge-based society, diversify its oil-based economy, and become a global hub for technological development.

- Around 70% of Vision 2030 strategic goals are closely related to AI. To achieve its mission, Saudi Arabia has led a concerted effort to advance its technological capabilities and to create a domestic AI-enabled digital ecosystem by 2030. The National Strategy for Data and Artificial Intelligence (NSDAI) will seek to attract USD 20 billion in foreign and local investments by 2030.

- Under Saudi Vision 2030, foreign investment is encouraged, particularly in the technology sector. The implementation of the cloud-first strategy in 2019 also accelerated the uptake of innovative technologies such as AI for Industrial 4.0. The Cloud Computing Regulatory Framework, which was adopted by the Communications and Technology Information Commission, intends to improve cloud computing services in the country and promote regulatory openness. Overall, it is expected that with an increase in big data volume through AI and other technology, the demand for data center construction will increase, leading to the major adoption of storage equipment.

Middle East Data Center Storage Industry Overview

The Middle East data center storage market is fragmented among the players and has gained a competitive edge in recent years. Some of the major players are Dell Inc., Hewlett Packard Enterprise, and NetApp Inc., among others. These major players, with a prominent market share, focus on expanding their customer base across the region. These companies leverage strategic collaborative initiatives to increase their market share and profitability. For instance,

- March 2024: Western Digital expanded its product lineup with the introduction of a 24 TB WD Red Pro mechanical hard drive designed specifically for NAS (network attached storage) applications. The company launched a 24TB model earlier, targeted at enterprise and data center use.

- March 2024: Pure Storage launched advanced data storage technologies and services. The company announced new self-service capabilities across its Pure1 storage management platform and Evergreen portfolio, offering software-based solutions, all via a single platform experience, to global customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Digitalization and Emergence of Data-centric Applications

- 4.2.2 Rising Cloud Applications Among End Users

- 4.3 Market Restraints

- 4.3.1 Compatibility and Optimum Storage Performance Issues

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Storage Technology

- 5.1.1 Network Attached Storage (NAS)

- 5.1.2 Storage Area Network (SAN)

- 5.1.3 Direct Attached Storage (DAS)

- 5.1.4 Other Technologies

- 5.2 By Storage Type

- 5.2.1 Traditional Storage

- 5.2.2 All-Flash Storage

- 5.2.3 Hybrid Storage

- 5.3 By End User

- 5.3.1 IT & Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Media & Entertainment

- 5.3.5 Other End Users

- 5.4 By Country

- 5.4.1 Israel

- 5.4.2 Saudi Arabia

- 5.4.3 United Arab Emirates

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Hewlett Packard Enterprise

- 6.1.3 NetApp Inc.

- 6.1.4 Huawei Technologies Co. Ltd

- 6.1.5 Kingston Technology Company Inc.

- 6.1.6 Pure Storage Inc.

- 6.1.7 Nutanix Inc.

- 6.1.8 Lenovo Group Limited

- 6.1.9 IBM Corporation

- 6.1.10 SMART Modular Technologies Inc.

- 6.1.11 Infinidat Ltd

- 6.1.12 IBM Corporation

- 6.1.13 Zadara Inc.

- 6.1.14 Western Digital Corporation