欧州のデータセンター向けストレージ:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

Europe Data Center Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549854

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

欧州のデータセンター向けストレージ市場規模は2024年に198億米ドルと推定され、2029年には275億米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは6.60%で成長する見込みです。

欧州のデータセンターは、フランクフルト、ロンドン、アムステルダム、パリなどのFLAP市場に集まっています。しかし、スペース、コスト、エネルギーの制約から、これらの高価な都市部では拡張の余地が限られています。このため、他の欧州諸国でも大規模なDC建設が行われています。同地域では、効率的なインフラ支出の増加に伴い、ストレージも力強い成長を遂げています。欧州各国でデータセンター建設への投資が増加しているため、コスト効率が高く、高性能を実現し、スペースと電力を節約し、ハードディスクよりも優れた信頼性を提供するフラッシュメモリへの需要が高まっています。

主なハイライト

- 欧州のデータセンター市場の今後のIT負荷容量は、2029年までに18K MWに達する見込み。

- 同地域の床面積は、2029年までに8,760万平方フィートに増加すると予想されます。

- 同地域に設置されるラックの総数は、2029年までに430万ユニットに達する見込みです。2029年までに最大数のラックが設置されるのは英国です。

- 欧州を結ぶ海底ケーブルシステムは210近くあり、その多くが建設中です。2025年にサービス開始が見込まれる海底ケーブルのひとつがSeaMeWe-6で、フランスのマルセイユを陸揚げ点とする全長1万9,200キロメートルに及ぶ。

欧州のデータセンター向けストレージ市場動向

ITと電気通信が大きなシェアを占める

- 欧州では、通信業界のプレーヤーが収益と収益性の縮小、規制による価格介入と統合の影響に直面しています。急速に普及が進む4Gと5Gの波は、通信ベンダーにデータセンター市場への投資を促しています。スウェーデンのネットワーク・プロバイダーNet4Mobilityは、地元キャリアのTele2とTelenorの合弁会社で、2023年末までに国民の90%を5Gネットワークに接続する計画を持っていました。

- オランダもまた、最先端技術で急速に近代化を進め、欧州有数の通信市場としての地位を固めています。EUのギガビット社会の目標には、すべての家庭が少なくとも100Mbpsの速度でブロードバンドネットワークにアクセスできるようにすることが含まれており、2023年までに大多数が1Gbpsを利用できるようにする必要があります。この目標はオランダ政府も支持しています。

- 5Gは4Gに比べてスループットが7倍近く向上し、1.45Gbsに対して10Gbsとなります。NVMeやSSD over HDDを使えば、このようなエンタープライズ・レベルの技術でもかなりのi/Oスループットが可能になります。NVMeの需要は、SSDサーバーやストレージ・アプライアンスで増加しており、予測期間中に市場を牽引すると予想されます。

- PCIe 4.0技術への移行は本格化しており、KIOXIA Europe GmbHがその先頭に立っています。同社は最近、CM6およびCD6 SeriesPCIe 4.0 NVM Express(NVMe)エンタープライズおよびデータセンター・ソリッド・ステート・ドライブのラインナップが、Ultra、WIO、BigTwin、FatTwin、SuperBlade、1U/2U NVMeオールフラッシュ・アレイ、GPUアクセラレーション・システム、Super Workstationsを含む幅広いエンタープライズ対応ラックマウント・システムなど、Super Micro Computer Inc.のPCIe 4.0ベース・プラットフォームとの互換性承認を取得したと発表しました。

- また最近の動向として、ExascendとGLYNは共同で、Exascendの最先端フラッシュ・ストレージ・ソリューションを欧州に提供し、GLYNが北欧、中欧、東欧、ベネルクス諸国で製品を販売することになりました。この提携により、欧州全域の企業が次世代フラッシュストレージ技術の可能性を活用できるようになります。

著しい成長を遂げる英国

- ブレグジットは英国のクラウド市場を揺るがし、クラウドプロバイダーにとって顧客データの保存と検索に関する不確実性を引き起こしました。その結果、英国のデータセンターに依存していた欧州企業は、事業を英国や他のEU諸国に移行しつつあります。にもかかわらず、英国のクラウド市場は活況を呈しています。2020年のクラウド・サービス需要の急増により、マイクロソフトによるサイバーセキュリティ・サービスを含む10の新サービスが開始されました。AWSとMicrosoft Azureは、この成長市場における主要企業であり続けています。

- 英国では商用5Gネットワークの導入に伴い、エッジデータセンターの需要が高まっています。英国は最もデジタル化が進んだ国のひとつです。政府は5Gや次世代デジタル技術に投資し、ビジネスをサポートしています。消費者の需要に伴い、クラウド・コンピューティング分野は、企業におけるマルチクラウドの利用を含むように本質的にシフトしていくと予想されます。

- 中小企業連盟(FSB)によると、2022年現在、英国には550万社の中小企業があり、同地域のビジネス全体の99.2%を占めています。さらに、中小企業は同国の雇用の5分の3と民間部門の売上高の約半分を占めています。堅牢でスケーラブルなアプリケーションを効率的にサポートするため、ハイパースケールデータセンターへのシフトが進んでおり、英国のデータセンター向けストレージ市場を促進すると予想されます。

- データセンター・プロバイダーがデジタル・インフラを増強していることから、ストレージ機器に対する需要も増加すると予想されます。デジタルインフラ企業であるエクイニクスは、マンチェスターのサルフォードに新しいInternational Business Exchange(IBX)データセンターを建設する計画を発表しました。エクイニクスはまた、総額1億6,500万米ドルの投資と、デジタルインフラへの10億米ドルの追加投資も発表しました。

欧州のデータセンター向けストレージ業界の概要

欧州のデータセンター向けストレージ市場は断片化されており、近年競争力を増しています。主なプレーヤーとしては、Dell Inc.、Hewlett Packard Enterprise、NetApp Inc.などが挙げられます。圧倒的な市場シェアを誇るこれらの大手企業は、地域全体の顧客基盤の拡大に注力しています。これらの企業は、戦略的協業イニシアティブを活用して市場シェアと収益性を高めています。

- 2023年2月:NetApp Inc.は、低価格なオールフラッシュ・ストレージを実現する大容量フラッシュ・ストレージ・オプションの新ファミリ、NetApp AFF Cシリーズと、オールフラッシュ・システムのAFF Aシリーズ・ファミリの新しいエントリーレベル・ストレージ・システム、NetApp AFF A150の提供を開始すると発表しました。

- 2022年7月:Dell Technologiesは、自動化、セキュリティ、マルチクラウド環境への適応性を重視したストレージソリューションの進化を発表。同社のDell PowerFlex Software-Defined Infrastructureは、新しいファイルサービスを提供することで、従来のワークロードと最新のワークロードの両方に対応します。このイノベーションにより、ブロック・ストレージとファイル・ストレージの機能が統合プラットフォーム上に集約されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- デジタル化の進展とデータ中心アプリケーションの出現

- エンドユーザーにおけるクラウドアプリケーションの増加

- 市場抑制要因

- 互換性と最適ストレージ性能の問題

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- ストレージ技術別

- ネットワーク接続ストレージ(NAS)

- ストレージ・エリア・ネットワーク(SAN)

- ダイレクト・アタッチド・ストレージ(DAS)

- その他の技術

- ストレージタイプ別

- 従来型ストレージ

- オールフラッシュ・ストレージ

- ハイブリッド・ストレージ

- エンドユーザー別

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他エンドユーザー

- 国別

- フランス

- 英国

- スウェーデン

- オーストリア

- ベルギー

- ドイツ

- アイルランド

- イタリア

- ノルウェー

- ポーランド

- スペイン

- スイス

- オランダ

- デンマーク

第6章 競合情勢

- 企業プロファイル

- Dell Inc.

- Hewlett Packard Enterprise

- NetApp Inc.

- Huawei Technologies Co. Ltd

- Hitachi Vantara LLC

- Kingston Technology Company Inc.

- Pure Storage Inc.

- Infinidat Ltd

- Lenovo Group Limited

- Fujitsu Limited

- Zadara Inc.

- Nutanix Inc.

- Oracle Corporation

- KIOXIA Europe GmbH

- Commvault Systems Inc.

第7章 投資分析

第8章 市場機会と今後の動向

目次

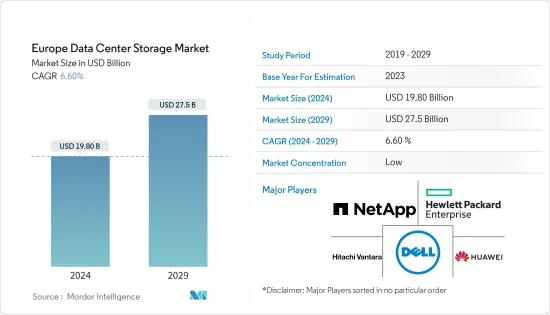

The Europe Data Center Storage Market size is estimated at USD 19.80 billion in 2024, and is expected to reach USD 27.5 billion by 2029, growing at a CAGR of 6.60% during the forecast period (2024-2029).

European data centers are clustered around FLAP markets, such as Frankfurt, London, Amsterdam, and Paris. However, there is limited scope for expansion in these expensive urban locations due to constraints on space, cost, and energy. This has also led to major DC construction in other European countries. The region has also been witnessing strong growth in storage with an increase in efficient infrastructure spending. The increasing investment to build data centers across European countries creates demand for flash memory as it is cost-effective, delivers high performance, is integrated with space and power savings, and provides better reliability than hard disks.

Key Highlights

- The upcoming IT load capacity of the European data center market is expected to reach 18K MW by 2029.

- The region's construction of raised floor area is expected to increase to 87.6 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 4.3 million units by 2029. The United Kingdom is expected to house the maximum number of racks by 2029.

- There are close to 210 submarine cable systems connecting Europe, and many are under construction. One such submarine cable that is estimated to start service in 2025 is SeaMeWe-6, which stretches over 19,200 kilometers with a landing point in Marseille, France.

Europe Data Center Storage Market Trends

IT and Telecom to Hold Significant Share

- In Europe, players in the telecommunications industry are faced with shrinking revenues and profitability, as well as the effects of regulatory pricing intervention and consolidation. The rapidly increasing 4G penetration and the 5G wave are encouraging telecom vendors to invest in the data center market. Swedish network provider Net4Mobility, a joint venture between local carriers Tele2 and Telenor, had plans to connect 90% of the nation's population to its 5G network by the end of 2023.

- The Netherlands has also quickly modernized with cutting-edge technology, solidifying its position as one of Europe's leading telecom markets. The goals of the EU Gigabit Society include providing all homes access to broadband networks with speeds of at least 100 Mbps, and the vast majority should be taking advantage of 1 Gbps by 2023. These goals are supported by the Dutch government as well.

- 5G is close to seven times better in terms of throughput compared to 4G, at 10 Gbs compared to 1.45 Gbs. With NVMe or SSD over HDD, such enterprise-level technology allows significant I/O throughput. The demand for NVMe is increasing in SSD servers and storage appliances, which is expected to drive the market during the forecast period.

- The transition to PCIe 4.0 technology is in full swing, and KIOXIA Europe GmbH is leading the way forward. Recently, the company announced that its lineup of CM6 and CD6 SeriesPCIe 4.0 NVM Express (NVMe) enterprise and data center solid state drives gained compatibility approval with Super Micro Computer Inc.'s PCIe 4.0-based platforms, including a wide range of enterprise-ready rackmount systems encompassing Ultra, WIO, BigTwin, FatTwin, SuperBlade, 1U/2U NVMe all flash arrays, GPU accelerated systems, and Super Workstations.

- In another recent development, Exascend and GLYN joined forces to bring Exascend's cutting-edge flash storage solutions to Europe, with GLYN distributing products in Northern, Central, Eastern Europe, and Benelux countries. This collaboration empowers businesses throughout Europe to leverage the potential of next-generation flash storage technology.

United Kingdom to Witness Significant Growth

- Brexit has shaken the UK cloud market, causing uncertainty for cloud providers regarding customer data storage and retrieval. As a result, European companies reliant on UK data centers are migrating their operations to the United Kingdom and other EU countries. Despite this, the cloud market in the United Kingdom is thriving. The surge in demand for cloud services in 2020 led to the launch of 10 new services, including cybersecurity offerings by Microsoft. AWS and Microsoft Azure remain the leading players in this growing market.

- The demand for edge data centers is growing with the implementation of commercial 5G networks in the United Kingdom. The United Kingdom is one of the most digitally advanced economies. The government invests in 5G and next-generation digital technologies to support businesses. In line with consumer demand, the cloud computing segment is expected to shift inherently to include the use of multi-cloud in enterprises.

- According to the Federation of Small Businesses (FSB), as of 2022, there were 5.5 million small businesses in the United Kingdom, accounting for 99.2% of the total business in the region. In addition, SMEs account for three-fifths of the employment and around half of the private sector turnover in the country. A growing shift toward hyperscale data centers to efficiently support robust, scalable applications is anticipated to propel the data center storage market in the United Kingdom.

- With data center providers increasing their digital infrastructure, the demand for storage equipment is expected to increase. Equinix Inc., a digital infrastructure company, announced its plans to build a new International Business Exchange (IBX) data center in Salford, Manchester. Equinix also announced a total investment of USD 165 million and an additional USD 1 billion in the digital infrastructure.

Europe Data Center Storage Industry Overview

Europe's data center storage market is fragmented and has gained a competitive edge in recent years. Some of the major players are Dell Inc., Hewlett Packard Enterprise, and NetApp Inc., among others. These major players, with a prominent market share, focus on expanding their customer base across the region. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

- February 2023: NetApp Inc. announced the upcoming availability of the NetApp AFF C-Series, a new family of capacity flash storage options that deliver lower-cost all-flash storage, and NetApp AFF A150, a new entry-level storage system in the AFF A-Series family of all-flash systems.

- July 2022: Dell Technologies unveiled advancements in storage solutions, emphasizing automation, security, and adaptability for multi-cloud environments. The company's Dell PowerFlex software-defined infrastructure caters to both traditional and modern workloads by offering new file services. This innovation brings together block and file storage functionalities on a unified platform.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Digitalization and Emergence of Data-centric Applications

- 4.2.2 Rising Cloud Applications Among End Users

- 4.3 Market Restraints

- 4.3.1 Compatibility and Optimum Storage Performance Issues

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Storage Technology

- 5.1.1 Network Attached Storage (NAS)

- 5.1.2 Storage Area Network (SAN)

- 5.1.3 Direct Attached Storage (DAS)

- 5.1.4 Other Technologies

- 5.2 By Storage Type

- 5.2.1 Traditional Storage

- 5.2.2 All-Flash Storage

- 5.2.3 Hybrid Storage

- 5.3 By End User

- 5.3.1 IT & Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Media & Entertainment

- 5.3.5 Other End Users

- 5.4 By Country

- 5.4.1 France

- 5.4.2 United Kingdom

- 5.4.3 Sweden

- 5.4.4 Austria

- 5.4.5 Belgium

- 5.4.6 Germany

- 5.4.7 Ireland

- 5.4.8 Italy

- 5.4.9 Norway

- 5.4.10 Poland

- 5.4.11 Spain

- 5.4.12 Switzerland

- 5.4.13 Netherlands

- 5.4.14 Denmark

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Hewlett Packard Enterprise

- 6.1.3 NetApp Inc.

- 6.1.4 Huawei Technologies Co. Ltd

- 6.1.5 Hitachi Vantara LLC

- 6.1.6 Kingston Technology Company Inc.

- 6.1.7 Pure Storage Inc.

- 6.1.8 Infinidat Ltd

- 6.1.9 Lenovo Group Limited

- 6.1.10 Fujitsu Limited

- 6.1.11 Zadara Inc.

- 6.1.12 Nutanix Inc.

- 6.1.13 Oracle Corporation

- 6.1.14 KIOXIA Europe GmbH

- 6.1.15 Commvault Systems Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日