|

市場調査レポート

商品コード

1549855

アフリカのデータセンターストレージ:市場シェア分析、産業動向、成長予測(2024年~2029年)Africa Data Center Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカのデータセンターストレージ:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

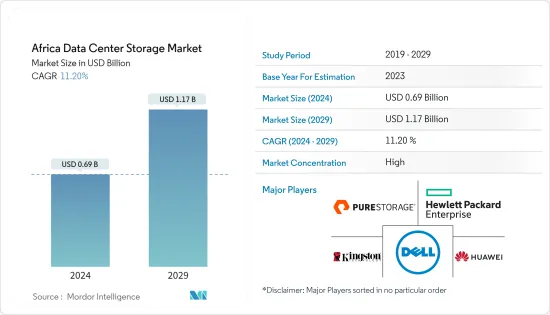

アフリカのデータセンターストレージ市場規模は、2024年に6億9,000万米ドルと推定され、2029年には11億7,000万米ドルに達すると予測され、市場推定・予測期間(2024~2029年)のCAGRは11.20%で成長する見込みです。

アフリカでは、スマートシティの発展によりデータ生成量が増加し、データストレージと計算機能に対する需要が高まると予想されます。HPC(ハイパフォーマンス・コンピューティング)用のエッジデータセンターの需要は、今後数年間で増加すると予想されます。さらに、アフリカ大陸ではスマートフォンの普及とビジネスソフトウェアの大量導入が進み、その技術を支えるデータセンターの需要が急増しているため、国際的な投資家がアフリカのクラウドコンピューティング市場の活況に資金提供を急いでいます。例えば、ロンドンを拠点とするプライベートエクイティ企業Actisは、今後3年間でアフリカのデータセンターに2億5,000万米ドルを投資することを決定しています。

主要ハイライト

- アフリカのデータセンター市場における今後のIT負荷容量は、2029年までに1,226MWに達すると予想されます。

- 同地域の床面積は2029年までに520万平方フィートに増加する見込み。

- 同地域に設置されるラックの総数は、2029年までに26万個に達する見込みです。2029年までに最大数のラックが設置されるのは南アフリカです。

- アフリカを結ぶ海底ケーブルシステムは70近くあり、その多くが建設中です。2024年にサービス開始が予定されているそのような海底ケーブルのひとつがAfrica-1で、エジプトのポートサイドとラス・ガレブを陸揚げ点とする1万km以上に及びます。

アフリカのデータセンターストレージ市場動向

ITと電気通信が大きなシェアを占める

- 5Gネットワークの展開により、国のデジタル経済が強化され、高容量データセンターストレージインフラへの需要が高まると予想されます。5Gの登場により、通信速度の大幅な向上、低遅延、予想外のレベルのネットワーク機能が期待されます。

- ナイジェリアは、南アフリカに次ぐアフリカ大陸第2位の経済規模に支えられ、アフリカ最大級の通信市場を有しています。2023年2月、ナイジェリアの通信規制当局であるナイジェリア通信委員会は、2022年12月に同国におけるアクティブなモバイル通信プランの契約数が約2,225億7,100万件に達したと報告し、同国におけるモバイルサービスの需要を示しています。全体として、ネットワーク・トラフィックの増加は、大規模なデータセンター投資とDCストレージの採用につながっています。

- NCC(ナイジェリア通信委員会)によると、2022年6月現在、ナイジェリアのブロードバンド普及率は44.30%で、契約数は8,400万件を超えている(2021年は約7,600万件、2020年は約7,800万件)。

- 急速に普及が進む4Gと来るべき5Gの波は、通信ベンダーに南アフリカのデータセンターへの投資を促しています。2022年10月、南アフリカの通信事業者Telkomは、中国のHuawei Technologiesの協力を得て、5G高速インターネット・ネットワークを確立しました。Huaweiは南アフリカの5Gネットワーク開発を引き続き支援しています。アフリカ大陸の著名な5Gネットワークには2,800以上の基地局が配備されています。

- このような要因から、電気通信セグメントからのデータセンター需要は絶えず増加しており、データセンターストレージの急速な増加に反映されています。データセンターメーカーは、通信産業からの高まる需要を満たすため、拡大性と安全性を備えた最先端で手頃な価格のソリューションを開発しています。

著しい成長を遂げる南アフリカ

- 南アフリカで調査された市場は、金融機関などの革新的な大企業が牽引しています。金融サービスは市場で提供するサービスを多様化しており、そのためには弾力性、低レイテンシー、一貫したパフォーマンスを提供するインフラが必要です。

- Pure Storageのような市場参入企業は、南アフリカのローカル市場でその焦点を広げています。リソース投資は、複数の市場セグメントでリーチを拡大するために行われています。価格に敏感な南アフリカ市場では、顧客に競合をもたらす価値と長期的な持続可能モデルが重要です。

- オールフラッシュ・アレイは、クラウドのようなアプリケーション統合と俊敏性の向上を提供し、データセンターストレージ市場に革命をもたらしていることは明らかです。企業がますます多くのデータを作成し、クラウド技術にますます目を向けるようになるにつれ、南アフリカのデータセンターストレージ市場は拡大すると予想されます。

- 中国のハイテク大手HuaweiとAlibabaも、積極的な戦略で南アフリカでの市場シェア拡大に注力しています。Huaweiは、2023年末までに市場の15%以上を獲得するという野心的な目標を掲げ、包括的な「何でもサービス」パッケージを提供して顧客を引き付けています。Alibabaも同様のアプローチをとっており、2022年後半にBCXと提携し、SaaS(Software-as-a-Service)ソリューションに重点を置いて、同国におけるクラウドのプレゼンスを拡大しています。

- サハラ以南のアフリカでは最近、データセンターインフラへの投資が進んでいるもの、同大陸の容量の多くは南アフリカにとどまっており、現地のプロバイダーは2017~2019年にかけて50MW以上のデータセンター専用IT負荷容量をオンライン化しました。データセンター投資の増加に伴い、データセンターストレージの市場も大きく成長すると予想されます。

アフリカのデータセンターストレージ産業概要

アフリカのデータセンターストレージ市場は参入企業間で統合されており、近年は競合を獲得しています。主要参入企業には、Dell Inc、Hewlett Packard Enterprise、Pure Storage Inc.などがあります。圧倒的な市場シェアを誇るこれらの大手企業は、地域全体の顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために戦略的な共同イニシアティブを活用しています。

- Seagateは2024年3月、10枚のプラッタを搭載したExos X24 CMR 7,200 rpm Helium SATAとSAS 3.5インチ24 TB HDDを発売しました。これらは、最大のストレージ容量と最高のラックスペース効率を実現するよう設計されています。Exos X24は、ハイパースケール向けに設計され、パフォーマンスと実証済みの技術を備えています。ヘリウム3.5インチ7,200 rpmニアライン・ドライブは、SATAとSASの両方のインターフェースを備え、リード・キャッシングまたはライト・キャッシングのみを利用するソリューションよりも最大3倍優れた性能を発揮する強化キャッシングを実現します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- デジタル化の進展とデータ中心アプリケーションの出現

- エンドユーザーにおけるフラッシュアレイの需要

- 市場抑制要因

- 互換性と最適なストレージ性能の問題

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- ストレージ技術別

- ネットワーク接続ストレージ(NAS)

- ストレージ・エリア・ネットワーク(SAN)

- ダイレクト・アタッチドストレージ(DAS)

- その他

- ストレージタイプ別

- 従来型ストレージ

- オールフラッシュストレージ

- ハイブリッドストレージ

- エンドユーザー別

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他

- 国別

- 南アフリカ

- ナイジェリア

第6章 競合情勢

- 企業プロファイル

- Dell Inc.

- Hewlett Packard Enterprise

- Pure Storage Inc.

- Huawei Technologies Co. Ltd

- Kingston Technology Company Inc.

- Infinidat Ltd

- Lenovo Group Limited

- Fujitsu Limited

- Nutanix Inc.

- Oracle Corporation

- QSAN Technology Inc.

- ADATA Technology Co. Ltd

- SMART Modular Technologies Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The Africa Data Center Storage Market size is estimated at USD 0.69 billion in 2024, and is expected to reach USD 1.17 billion by 2029, growing at a CAGR of 11.20% during the forecast period (2024-2029).

In Africa, the development of smart cities is expected to enable more data generation, leading to higher demand for data storage and computation capabilities. The demand for edge data centers for HPC (high-performance computing) is anticipated to increase over the years. Moreover, international investors are rushing to fund a boom in the African cloud computing market, as the proliferation of smartphones and mass adoption of business software on the continent lead to soaring demand for data centers to power the technology. For instance, London-based private equity firm Actis has decided to invest USD 250 million into African data centers over the next three years.

Key Highlights

- The upcoming IT load capacity of the African data center market is expected to reach 1226 MW by 2029.

- The region's construction of raised floor area is expected to increase to 5.2 million sq. ft by 2029.

- The region's total number of racks to be installed is expected to reach 260K units by 2029. South Africa is expected to house the maximum number of racks by 2029.

- There are close to 70 submarine cable systems connecting Africa, and many are under construction. One such submarine cable that is estimated to start service in 2024 is Africa-1, which stretches over 10,000 kilometers with a landing point in Port Said and Ras Ghareb in Egypt.

Africa Data Center Storage Market Trends

IT and Telecom to Hold Significant Share

- The rollout of 5G networks is expected to strengthen the nation's digital economy and increase the demand for high data center storage infrastructure. The arrival of 5G is expected to bring a major increase in speeds, low latencies, and an unforeseen level of network capabilities.

- Nigeria has one of the largest telecom markets in Africa, supported by the second-largest economy on the continent after South Africa. In February 2023, the Nigerian Communications Commission, the Nigerian telecom regulator, reported that the number of active mobile telecommunication plan subscriptions in the country reached about 222,571 million in December 2022, which shows the demand for mobile services in the country. Overall, the increasing network traffic is leading to major data center investments and the adoption of DC storage.

- According to NCC (Nigerian Communications Commission), as of June 2022, Nigeria's broadband penetration was 44.30%, with more than 84 million subscriptions, compared to about 76 million in 2021 and 78 million in 2020.

- The rapidly increasing 4G penetration and the upcoming 5G wave are encouraging telecom vendors to invest in South African data centers. In October 2022, the South African telecom provider Telkom established the 5G high-speed internet network with the help of Huawei Technologies from China. Huawei continues to assist South Africa in developing its 5G networks. The prominent 5G network on the African continent has more than 2,800 base stations deployed.

- Owing to such factors, the demand for data centers from the telecom segment is constantly rising, mirrored by a rapid rise in data center storage. The manufacturers of data centers are developing cutting-edge, affordable solutions that are scalable and secure to fulfill the rising demand from the telecom industries.

South Africa to Witness Significant Growth

- The market studied in South Africa is led by large, innovative enterprises, such as financial institutions. Financial services are diversifying their market offerings, and this requires an infrastructure that provides resiliency, low latency, and consistent performance.

- Players like Pure Storage are widening their focus in the local market of South Africa. The resource investment is being made to expand reach across multiple market segments. In the price-sensitive South African market, the value and long-term sustainable models are important, as they provide a competitive edge to their clients.

- All-flash arrays are evidently revolutionizing the data center storage market, offering cloud-like application consolidation and enhanced agility. As enterprises create more and more data and increasingly turn to cloud technology, the data center storage market in South Africa is expected to expand.

- Chinese tech giants Huawei and Alibaba are also focusing on increasing their market shares in South Africa with aggressive strategies. Huawei set an ambitious goal of capturing at least 15% of the market by the end of 2023, offering a comprehensive "everything-as-a-service" package to attract customers. Alibaba has taken a similar approach, partnering with BCX in late 2022 and focusing on software-as-a-service (SaaS) solutions to expand its cloud presence in the country.

- Despite recent investments in data center infrastructure in Sub-Saharan Africa, much of the continent's capacity remains in South Africa, where local providers brought more than 50 MW of dedicated data center IT load capacity online between 2017 and 2019. With increasing data center investment, the market for data center storage is expected to grow significantly.

Africa Data Center Storage Industry Overview

Africa's data center storage market is consolidated among the players and has gained a competitive edge in recent years. Some of the major players include Dell Inc., Hewlett Packard Enterprise, and Pure Storage Inc., among others. These major players, with a prominent market share, focus on expanding their customer base across the region. They leverage strategic collaborative initiatives to increase their market share and profitability. For instance,

- In March 2024, Seagate launched Exos X24 CMR 7,200 rpm Helium SATA and SAS 3.5-inch 24 TB HDD with 10 platters. They are designed for maximum storage capacity and the highest rack-space efficiency. Exos X24 is purpose-built for hyperscale with performance and proven technology. The helium 3.5-inch 7,200 rpm nearline drive offers both SATA and SAS interfaces and delivers enhanced caching that performs up to 3x better than solutions that only utilize read or write caching.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Digitalization and Emergence of Data-centric Applications

- 4.2.2 Demand of Flash Arrays in End Users

- 4.3 Market Restraints

- 4.3.1 Compatibility and Optimum Storage Performance Issues

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Storage Technology

- 5.1.1 Network Attached Storage (NAS)

- 5.1.2 Storage Area Network (SAN)

- 5.1.3 Direct Attached Storage (DAS)

- 5.1.4 Other Technologies

- 5.2 By Storage Type

- 5.2.1 Traditional Storage

- 5.2.2 All-Flash Storage

- 5.2.3 Hybrid Storage

- 5.3 By End User

- 5.3.1 IT & Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Media & Entertainment

- 5.3.5 Other End Users

- 5.4 By Country

- 5.4.1 South Africa

- 5.4.2 Nigeria

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Hewlett Packard Enterprise

- 6.1.3 Pure Storage Inc.

- 6.1.4 Huawei Technologies Co. Ltd

- 6.1.5 Kingston Technology Company Inc.

- 6.1.6 Infinidat Ltd

- 6.1.7 Lenovo Group Limited

- 6.1.8 Fujitsu Limited

- 6.1.9 Nutanix Inc.

- 6.1.10 Oracle Corporation

- 6.1.11 QSAN Technology Inc.

- 6.1.12 ADATA Technology Co. Ltd

- 6.1.13 SMART Modular Technologies Inc.