|

市場調査レポート

商品コード

1690699

塩化アリル- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Allyl Chloride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 塩化アリル- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

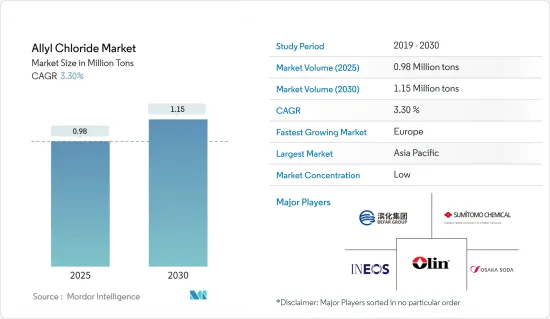

塩化アリルの市場規模は2025年に98万トンと予測され、予測期間(2025年~2030年)のCAGRは3.3%で、2030年には115万トンに達すると予測されます。

主なハイライト

- COVID-19の発生により、2020年の市場は世界各地でロックダウン、製造活動やサプライチェーンの混乱、生産停止などの悪影響を受けました。しかし、2021年には状況が回復し始め、市場の成長軌道が回復しました。

- 中期的には、いくつかの用途で塩化アリル誘導体の使用が増加していることが、調査期間中の市場需要を牽引する主要因となると思われます。

- その反面、厳しい政府規制やバイオベースのエピクロルヒドリンに関する知識の増加といった要因は、市場成長の妨げになると予想されます。可塑剤や乳化剤として様々な塩化アリルポリマーやコポリマーが出現していることは、調査した市場にとって好機として作用すると予想されます。

- アジア太平洋は、中国、韓国、インド、日本などの国々からの消費により、最大の市場を占めています。

塩化アリルの市場動向

エピクロロヒドリン製造における塩化アリルの使用の増加

- 塩化アリルは通常、プロピレンと塩素を反応させて製造されるが、エピクロロヒドリンは通常、塩化アリルと次亜塩素酸および水酸化ナトリウムのような塩基を反応させて製造されます。しかし、グリセリンに塩酸を加えてエピクロルヒドリンを製造する例も増えています。

- 塩化アリルの主な需要は、エピクロルヒドリンの製造からもたらされます。この化合物は、塩化アリルをエポキシ化プロセスで変換するか、塩化アリルと次亜塩素酸を反応させることで得られます。

- エピクロルヒドリンは主にエポキシ樹脂の製造に使用され、塗料、接着剤、プラスチックに広く使用されています。また、合成グリセリン、繊維、製紙、インク・染料、溶剤、界面活性剤、医薬品の製造にも役立っています。

- エピクロロヒドリンの主要メーカーには、Olin Corporation、Shandong Haili Chemical、Vinythai AGC Groupなどがあります。塩化アリル市場の需要に対応するため、エピクロルヒドリンの生産プラント・プロジェクトを開始した企業もあります。

- 2023年3月、シノペックは中国北部の製油所で15億6,000万米ドルのプロジェクトを開始し、エピクロルヒドリン生産をアップグレードに組み込みました。この拡張は、生産能力を増強し、雇用創出を通じて中国経済を強化し、化学部門を発展させることを目的としています。このプロジェクトには、年産300万トンの接触分解装置、年産70万トンのガソリン水素化分解装置、年産10万トンのエピクロルヒドリン装置など、複数の設備が含まれます。

- エピクロルヒドリンの製造に塩化アリルを使用することがグリセリンに取って代わられた例もあるが、オリン、ソルベイ、ENEOSのような特定のメーカーは従来の方法を使い続けており、これが今後の市場を形成すると予想されます。

- さらに、エポキシ樹脂の生産量の増加が、エピクロルヒドリンと塩化アリルの需要を牽引しています。

- 2023年5月、山東省東営経済技術開発区は東営益瑞全新材料技術による新プロジェクトの承認を発表しました。このプロジェクトは年産20万トンの電子グレードのエポキシ樹脂と新しい特殊樹脂材料を開発することを目的としています。

- アルコ・ノーベルは2022年2月、Grow &Deliver戦略の一環として、自社での樹脂製造を拡大する投資計画を発表しました。この継続的な規模拡大プログラムは、供給の途絶に対する耐性を強化し、同社の財務目標と上流の炭素削減の野心に大きく貢献することを目的としています。

- したがって、これらの要因を考慮すると、エピクロルヒドリン製造における塩化アリルの用途が、予測期間中に市場を独占すると予想されます。

市場を独占するアジア太平洋

- アジア太平洋は、エピクロルヒドリン(ECH)、グリシジルエーテル、アリルアミン、ポリアクリロニトリルモノマー、各種水処理薬品、アリルスルホン酸ナトリウムなどのアリル化合物など、様々な産業における急速な拡大と消費のため、塩化アリルの需要が最も高いです。この需要は主に、中国、韓国、日本、インドといった国々から生じています。

- 中国はアジア全体のECH生産量の60%近くを占め、エピクロロヒドリン生産能力を一貫して拡大しており、世界の銘板生産能力の約半分を占めています。例えば、シノペックは2023年3月、主にエピクロロヒドリンの生産を可能にするため、中国北部の製油所の15億6,000万米ドルのアップグレードを開始しました。このプロジェクトには12の設備が含まれ、年産10万トン(TPA)のエピクロルヒドリンユニットを備えています。

- さらに、中国は世界最大のエポキシ樹脂生産国であり、輸出国トップ5に入っています。Nan Ya Epoxy Resin(Kunshan)、Sanmu Group、Kingboard Chemical Holdings Ltdは、中国のエポキシ樹脂業界の主要メーカーの一部です。

- 中国の製薬業界は、ジェネリック医薬品、治療用医薬品、原薬、伝統的な漢方薬を製造しており、世界最大級の規模を誇っています。国内で登録されている医薬品の90%以上がジェネリック医薬品です。中国国家統計局によると、2022年の製薬業界の営業収入は3兆3,600億元(4,590億米ドル)を超え、前年比0.5%の伸びを示し、2021年には3兆3,300億元(4,510億米ドル)を超えます。

- Aatma Nirbhar Bharat」改革の下で、インド製薬省は、重要な原薬と主要出発原料(KSM)/医薬品中間体(DI)および原薬の国内製造を促進するための生産連動インセンティブ(PLI)スキームのようなスキームを実施しており、2020-21年度から2028-29年度にかけて15,000カロールインドルピー(18億米ドル)を割り当てています。さらに、2020-21年度から2024-25年度にかけて3,000カロールインドルピー(3億6,250万米ドル)相当のバルク・ドラッグ・パーク促進スキームがあり、3つの州でバルク・ドラッグ・パークを設立するための資金援助を提供することを目的としています。

- インドは、2023年までに国内の医薬品原料製造を強化するため、約1,000億インドルピー(13億米ドル)の基金を設立する予定です。さらに、インド政府は、簡単に入手できることによる誤用の可能性を抑制するため、新たな政策のもと、オンライン薬局を規制する電子プラットフォームを設置する意向です。

- これらの要因を考慮すると、この地域の塩化アリル需要は予測期間中に増加すると予想されます。

塩化アリル産業の概要

世界の塩化アリル業界は細分化されており、どの企業も大きな市場シェアを占めていないです。この業界の主要企業は、INEOS、鹿島ケミカル、オリン・コーポレーション、大阪ソーダ、ソルベイ、住友化学、BefarGroupです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- いくつかの用途における塩化アリル誘導体の使用増加

- 抑制要因

- バイオベースのエピクロルヒドリンに関する知識の増加

- 厳しい環境規制

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 用途

- アリルアミン

- アリルスルホン酸塩

- エピクロルヒドリン

- グリシジルエーテル

- 水処理薬品

- その他の用途(接着剤、香料、医薬品)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AccuStandard

- Befar Group Co.ltd.

- Gelest, Inc.

- INEOS

- Kashima Chemical Co.,LTD.

- Olin Corporation

- OSAKA SODA

- Solvay

- Sumitomo Chemical Co., Ltd

- Thermo Fisher Scientific Inc

- Vizag Chemical

第7章 市場機会と今後の動向

- 可塑剤および乳化剤としての各種塩化アリルポリマーおよびコポリマーの出現

目次

Product Code: 70999

The Allyl Chloride Market size is estimated at 0.98 million tons in 2025, and is expected to reach 1.15 million tons by 2030, at a CAGR of 3.3% during the forecast period (2025-2030).

Key Highlights

- Due to the COVID-19 outbreak, nationwide lockdowns around the world, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

- Over the medium term, the increasing use of allyl chloride derivatives in several applications will be the primary factor for driving the market demand in the studied period.

- On the flip side, factors such as stringent government regulations and increasing knowledge of Bio-based epichlorohydrin are expected to hinder market growth. The emergence of various allyl chloride polymers and copolymers as plasticizers and emulsifiers is expected to act as an opportunity for the market studied.

- Asia-Pacific region represents the largest market owing to the consumption from countries such as China, South Korea, India, and Japan.

Allyl Chloride Market Trends

Increasing Use of Allyl Chloride in Epichlorohydrin Production

- Allyl chloride is typically produced by reacting propylene with chlorine, while epichlorohydrin is typically manufactured by reacting allyl chloride with hypochlorous acid and a base like sodium hydroxide. However, an increasing amount of epichlorohydrin is now being manufactured by adding hydrochloric acid to glycerin.

- The key demand for allyl chloride comes from epichlorohydrin production. This compound can be obtained either by transforming allyl chloride through the epoxidation process or by reacting allyl chloride with hypochlorous acid.

- Epichlorohydrin finds primary usage in producing epoxy resins, which are widely used in coatings, adhesives, and plastics. It also serves in manufacturing synthetic glycerine, textiles, paper, inks and dyes, solvents, surfactants, and pharmaceuticals.

- Leading epichlorohydrin producers include Olin Corporation, Shandong Haili Chemical, and Vinythai AGC Group. Some companies have initiated production plant projects for epichlorohydrin, aiming to meet the demand in the allyl chloride market.

- In March 2023, Sinopec launched a USD 1.56 billion project at its Northern China refinery, incorporating epichlorohydrin production in the upgrade. This expansion aims to increase production capacity, bolster the Chinese economy through job creation, and advance the chemical sector. The project encompasses several facilities, including a 3000 thousand tonnes per annum catalytic cracker, a 700 thousand tonnes per annum gasoline hydrotreating unit, and a 100 thousand tonnes per annum epichlorohydrin unit.

- While the use of allyl chloride for producing epichlorohydrin has been replaced by glycerin in some cases, certain manufacturers like Olin, Solvay, and INEOS continue using the traditional method, which is expected to shape the market in the years ahead.

- Additionally, the increasing production of epoxy resin is driving the demand for epichlorohydrin and allyl chloride.

- In May 2023, the Dongying Economic and Technological Development Zone of Shandong Province announced its approval of a new project by Dongying Yi Rui Zengnew Material Technology Co. LTD. This project aims to develop electronic-grade epoxy resin and new special resin materials with an annual capacity of 200,000 tons.

- In February 2022, Alko Nobel announced investment plans to expand in-house resin manufacturing as part of its Grow & Deliver strategy. This ongoing scale-up program aims to enhance resilience against supply disruptions and contribute significantly to the company's financial goals and upstream carbon reduction ambitions.

- Therefore, considering these factors, the application of allyl chloride in epichlorohydrin production is expected to dominate the market during the forecast period.

Asia Pacific Region to Dominate the Market

- The Asia-Pacific region witnessed the highest demand for allyl chloride due to rapid expansion and consumption in various industries, including epichlorohydrin (ECH), glycidyl ether, allyl amines, monomers of polyacrylonitrile, various water treatment chemicals, and allyl compounds such as sodium allyl sulfonate. This demand predominantly stems from countries like China, South Korea, Japan, and India.

- China accounts for nearly 60% of Asia's total ECH output and has consistently expanded its epichlorohydrin capacity, representing around half of the global nameplate capacity. For example, in March 2023, Sinopec initiated a USD 1.56 billion upgrade to its Northern China refinery, primarily to enable Epichlorohydrin production. The project includes 12 facilities, featuring a 100,000 tons per annum (TPA) Epichlorohydrin unit.

- Moreover, China stands as the world's largest producer of epoxy resin and is among the top five exporters. Nan Ya Epoxy Resin (Kunshan) Co. Ltd, Sanmu Group, and Kingboard Chemical Holdings Ltd are some of the key manufacturers in China's epoxy resin industry.

- China's pharmaceutical industry ranks among the largest globally, manufacturing generics, therapeutic medicines, active pharmaceutical ingredients, and traditional Chinese medicine. Over 90% of registered drugs in the country are generic. According to the National Bureau of Statistics of China, in 2022, the pharmaceutical industry generated operating revenue exceeding 3.36 trillion yuan (USD 0.459 trillion), showcasing a 0.5% growth from the previous year, with revenue surpassing CNY 3.33 trillion (USD 0.451 trillion) in 2021.

- Under the 'Aatma Nirbhar Bharat' reform, India's Department of Pharmaceuticals is implementing schemes like the Production Linked Incentive (PLI) Scheme for promoting domestic manufacturing of critical APIs and Key Starting Materials (KSMs)/ Drug Intermediates (DIs) and APIs, allocating INR 15,000 crores (USD 1.8 billion) from FY 2020-21 to FY 2028-29. Additionally, the Scheme for the Promotion of Bulk Drug Parks, worth INR 3,000 crores (USD 362.5 million) from FY 2020-21 to FY 2024-25, aims to provide financial assistance for establishing Bulk Drug Parks in three States.

- India plans to establish a fund of nearly INR 1 lakh crore (USD 1.3 billion) to bolster domestic pharmaceutical ingredient manufacturing by 2023. Furthermore, the Government of India intends to set up an electronic platform to regulate online pharmacies under a new policy to curb potential misuse due to easy availability.

- Considering these factors, the region's demand for allyl chloride is expected to rise during the forecast period.

Allyl Chloride Industry Overview

The global allyl chloride industry is fragmented in nature, as no company accounts for a significant market share. Leading companies in this industry are INEOS, Kashima Chemical Co. LTD, Olin Corporation, OSAKA SODA, Solvay, Sumitomo Chemical Co. Ltd, and BefarGroup Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use of Allyl Chloride Derivatives in Several Applications

- 4.2 Restraints

- 4.2.1 Increasing Knowledge of Bio-based Epichlorohydrin

- 4.2.2 Stringent Environmental Regulations

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Allyl Amines

- 5.1.2 Allyl Sulfonates

- 5.1.3 Epichlorohydrin

- 5.1.4 Glycidyl Ether

- 5.1.5 Water Treatment Chemicals

- 5.1.6 Other Applications (Adhesives, Perfumes, Pharmaceuticals)

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AccuStandard

- 6.4.2 Befar Group Co.ltd.

- 6.4.3 Gelest, Inc.

- 6.4.4 INEOS

- 6.4.5 Kashima Chemical Co.,LTD.

- 6.4.6 Olin Corporation

- 6.4.7 OSAKA SODA

- 6.4.8 Solvay

- 6.4.9 Sumitomo Chemical Co., Ltd

- 6.4.10 Thermo Fisher Scientific Inc

- 6.4.11 Vizag Chemical

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emergence of Various Allyl Chloride Polymers and Copolymers as Plasticizers and Emulsifiers