|

市場調査レポート

商品コード

1549850

スペインのデータセンターストレージ:市場シェア分析、産業動向、成長予測(2024年~2029年)Spain Data Center Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スペインのデータセンターストレージ:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

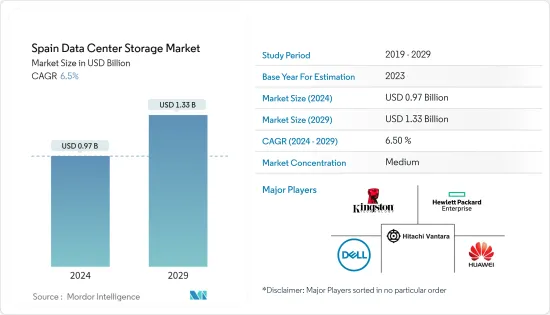

スペインのデータセンターストレージ市場規模は、2024年に9億7,000万米ドルと推定され、2029年には13億3,000万米ドルに達すると予測され、予測期間(2024~2029年)のCAGRは6.5%で成長する見込みです。

中小企業におけるクラウドコンピューティング需要の増加、データセキュリティに関する政府規制、国内企業による投資の拡大などが、同国のデータセンター需要を促進する主要要因となっています。

主要ハイライト

- 建設中のIT負荷容量:スペインのデータセンターラック市場の今後のIT負荷容量は、2029年までに1,400MWに達する見込み。

- 建設中の高床スペース:2029年までにスペインの床面積は600万平方フィートに増加すると予想されます。

- 計画中のラック:同国に設置されるラックの総数は、2029年までに33万個に達する見込みです。2029年までに最大数のラックが設置されるのはマドリードであると考えられます。

- 計画中の海底ケーブル:スペインを結ぶ海底ケーブルシステムは32近くあり、その多くが建設中です。

- データストレージへのニーズの高まりにより、全国的にデータセンターの数が急増しています。スペイン国内のデータセンター需要とその成長にはいくつかの要因が寄与しており、それは同国の進化するIT状況、ビジネス活動、技術的イニシアティブに反映されています。スペインのデータセンター開発を促進する主要要因には、デジタルトランスフォーメーション、クラウドコンピューティングの導入、eコマースとデジタルサービス、再生可能エネルギーと持続可能性、スマートシティとIoTへの取り組みなどがあります。したがって、こうした要因が予測期間中の市場成長を促進するとみられます。

スペインのデータセンターストレージ市場動向

IT・通信セグメントが大きなシェアを占める。

- ビッグデータや人工知能などの技術により、大企業によるクラウド利用が増加していることがスペイン市場の主要促進要因となっています。ITソリューションサービス産業の企業数は、2020年の1万6,648社から2023年には1万8,264社へと大幅に増加しています。

- クラウドベースのサービス導入の増加が、スペインにおける小売・卸売コロケーションサービスの拡大に拍車をかけ、需要増につながっています。このため、データセンターにはより多くのラックが必要となります。

- デジタル化に不可欠なクラウドサービス市場は急成長しています。スペインではデジタル経済の台頭とインターネット利用の増加に伴い、データ保存と処理のニーズが高まっている

- 政府は、中央政府プライベート・クラウド(SARAクラウド)構想の拡大と改善のために、8,400万ユーロ(9,081万米ドル)を割り当てた。クラウドの利用は新たなビジネスモデルの開発を促進し、あらゆる規模や業種の企業がイノベーションを起こし、競合を獲得することを可能にします。

- さらに、データセンター産業は通信部門に大きく依存しています。5Gとブロードバンド産業は、全国で急速にリンクを構築・展開しています。同国は、5Gの採用をさらに推し進めるため、2025年までに43億2,000万ユーロ(45億5,110万米ドル)を拠出する「コネクティビティとデジタルインフラ計画」と「5G技術推進戦略」を策定しました。このような市場の動きにより、今後数年間はデータセンターストレージの需要が高まると予想されます。

ハイブリッドストレージが大きな市場シェアを占める見込み

- オンプレミスとクラウドのストレージソリューションの組み合わせは、データセンターにおけるハイブリッド・ストレージと呼ばれます。このアプローチは、両方の環境の長所を活用し、オンサイトとクラウドにデータを保存・管理する柔軟性を記載しています。

- デジタルトランスフォーメーションは、スペインの企業だけでなく世界中で適用されています。デジタル化に向けた段階的かつ戦略的なアプローチをサポートするため、ハイブリッド・データセンターによって、古いシステムと新しいクラウドベースの技術の統合が促進されています。

- スペイン経済の特定のセクターでは、特定のデータ保存や処理要件が存在する場合があります。ハイブリッド・アーキテクチャの柔軟性により、金融、医療、製造業など特定のセクターの要件別の多様なソリューションが可能になります。

- さらに、インターネット・ユーザーやオンラインショッピングなどの要因も、データや処理設備の増加に寄与すると考えられます。魅力的なお得情報が提供されるオンラインショッピングにユーザーが傾倒するにつれ、デジタル決済サービスやウェブサイトのトラフィックが増加し、データ消費量が増加します。国内のデジタル決済ユーザー数は、2022年の3,235万人から2027年には4,060万人に達すると予測されています。これらすべての要因が消費の大幅な増加に寄与し、同地域のDC冷却インフラ需要を押し上げると考えられます。

- 同市場の主要企業は、市場需要に対応するため、データセンターストレージソリューションの提携と改良に注力しています。2023年6月、Hitachiの著名なインフラストラクチャー、データ管理、デジタルソリューションの子会社であるHitachi Vantaraは、Ciscoとの2つの新しい世界パートナーシップ契約を発表しました。これらの契約により、Hitachi VantaraはCiscoの技術をシームレスにストレージ製品に統合し、Vantaraサービスプロバイダと技術インテグレータ(STI)パートナープログラムに参加することで、データセンターインフラとハイブリッドクラウドマネージドサービスのリーディングプロバイダとしての地位を確立します。

スペインのデータセンターストレージ産業概要

スペインでは今後DC建設プロジェクトが予定されており、スペインのデータセンターストレージ市場の需要は今後数年間で増加するとみられます。スペインのデータセンターストレージ市場は、Dell、Hewlett Packard Enterprise、Huawei Technologies、Hitachi Vantara LLC、Kingston Technology Company Inc.これらの主要企業は市場シェアが高く、地域の顧客基盤の拡大に注力しています。

- 2023年5月、クラウドコンピューティングとハイブリッドマルチクラウドの著名なプロバイダーであるNutanixは、オンプレミス、ホスト型、またはエッジインフラにわたって可視化、モニタリング、または管理のための単一のコンソールを提供するクラウドベースのソリューション、Nutanix Centralの発売を発表しました。Nutanix Centralは、Nutanix Cloud Platformのユニバーサルクラウドオペレーティングモデルを拡大し、サイロ化を解消し、どこにいても一貫してアプリとデータを管理できるようにします。

- 2023年3月、2023年のワールド・モバイル・コングレス・バルセロナで、ファーウェイのA-Aアーキテクチャ別の産業有数のエントリーレベルのプライマリとセカンダリストレージポートフォリオを発表。このポートフォリオソリューションは、中小企業が新しいHuawei OceanStor Dorado 2,000とOceanProtect X3,000を使用してコスト効率の高いデータストレージシステムを構築するのを支援するために開発されました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- クラウドコンピューティング機能の需要の増加が市場成長を促進

- エネルギー効率とコスト効率に優れたデータセンターに対する需要の増加

- 市場抑制要因

- 熟練労働力の確保とセキュリティへの懸念

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- ストレージ技術

- ネットワーク接続ストレージ(NAS)

- ストレージ・エリア・ネットワーク(SAN)

- ダイレクト・アタッチド・ストレージ(DAS)

- その他

- ストレージタイプ

- 従来型ストレージ

- オールフラッシュ・ストレージ

- ハイブリッド・ストレージ

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他

第6章 競合情勢

- 企業プロファイル

- Dell Inc.

- Hewlett Packard Enterprise

- Huawei Technologies Co. Ltd.

- Hitachi Vantara LLC

- Kingston Technology Company Inc.

- Pure Storage Inc.

- Infinidat Ltd.

- Lenovo Group Limited

- Fujitsu Limited

- Oracle Corporation

- KIOXIA Singapore Pte. Ltd.

- Commvault Systems Inc.

- NetApp Inc.

- Nutanix Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The Spain Data Center Storage Market size is estimated at USD 0.97 billion in 2024, and is expected to reach USD 1.33 billion by 2029, growing at a CAGR of 6.5% during the forecast period (2024-2029).

The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country.

Key Highlights

- Under Construction IT Load Capacity: The upcoming IT load capacity of the Spain data center rack market is expected to reach 1400 MW by 2029.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase to 6 million sq. ft by 2029.

- Planned Racks: The country's total number of racks to be installed is expected to reach 330,000 units by 2029. Madrid will likely house the maximum number of racks by 2029.

- Planned Submarine Cables: There are close to 32 submarine cable systems connecting Spain, and many are under construction.

- An increasing need for data storage has resulted in an upsurge in the number of data centers nationwide. Several factors contribute to the demand for data centers and their growth within the spain, which is reflected by the country's evolving IT landscape, business activities, and technological initiatives. Key drivers that propel the development of data centers in the nation include Digital Transformation, Cloud Computing Adoption, E-commerce & Digital Services, Renewable Energy & Sustainability, and Smart Cities & IoT Initiatives. Hence, such factors are expected to drive market growth during the forecast period.

Spain Data Center Storage Market Trends

IT & Telecommunication Segment holds the major share.

- The increasing use of the cloud by large companies, driven by technologies such as big data and artificial intelligence, is the main driver of the Spanish market. The number of companies in the IT solutions and services industry has grown significantly from 16,648 in 2020 to 18,264 in 2023.

- Increased adoption of cloud-based services has fueled the expansion of retail and wholesale colocation services in Spain, leading to increased demand. This will require more racks in the data center.

- The cloud service market, which is indispensable for digitalization, is growing rapidly. With the rise of the digital economy and increased internet usage in Spain, the need for data storage and processing is increasing.

- The government has allocated EUR 84 million (USD 90.81 million )for the expansion and improvement of the Central Government Private Cloud (SARA Cloud) initiative. The use of the cloud facilitates the development of new business models, enabling companies of all sizes and industries to innovate and gain a competitive edge.

- Additionally, the data center industry heavily depends on the telecommunications sector. The 5G and broadband industries are rapidly building and deploying links across the nation. The nation has developed the Plan for Connectivity and Digital Infrastructures and the Strategy to Promote 5G Technology, which would be endowed with EUR 4,320 million (USD 4,551.1 million) through 2025 to push the adoption of 5G further. Such instances in the market are expected to create more demand for data center Storage in the coming years.

Hybrid Storage is Expected to Hold a Significant Market Share

- The combination of on-premises and cloud storage solutions is called hybrid storage in data centers. This approach leverages the strengths of both environments, offering the flexibility to store and manage data on-site and in the cloud.

- Digital transformation is being applied by Spanish businesses and around the world. In support of a phased and strategic approach towards Digitalisation, the integration of old systems with new cloud-based technologies is facilitated by hybrid data centers.

- Specific data storage and processing requirements may exist in certain sectors of the Spanish economy. The flexibility of the hybrid architecture allows for a wide variety of solutions based on specific sector requirements like finance, healthcare, or manufacturing.

- Furthermore, factors such as internet users, online shopping, would contribute to the increasing generation of data and processing facilities. As users grow more inclined to online shopping with attractive deals offered, this would lead to a rise in digital payment services and traffic on websites, thus increasing data consumption. The number of digital payment users in the country is projected to reach 40.6 million by 2027, up from 32.35 million users in 2022. All these factors would contribute to a significant increase in consumption, boosting the demand for DC cooling infrastructre in the region.

- The key players in the market focus on collabrations and improving the data center storage solutions to meet the market demand. In June 2023, Hitachi Vantara, a prominent infrastructure, data management, and digital solutions subsidiary of Hitachi, Ltd., announced its two new global partnership agreements with Cisco. These agreements will enable Hitachi Vantara to seamlessly integrate Cisco technologies into its storage products and position it as a leading provider of data center infrastructure and hybrid cloud-managed services by bringing it into the Vantara Service Provider and Technology Integrator (STI) Partner programs.

Spain Data Center Storage Industry Overview

The upcoming DC construction projects in the country would increase the demand for Spain data center storage Market in the coming years. The Spain Data Center Storage Market is moderately consolidated with some players in the market, including Dell Inc., Hewlett Packard Enterprise, Huawei Technologies Co. Ltd., Hitachi Vantara LLC, and Kingston Technology Company Inc. These major players, with a prominent market share, focus on expanding their regional customer base.

- May 2023: Nutanix, a prominent provider in cloud computing and hybrid multi-clouds, announced the launch of Nutanix Central, a cloud-based solution that provides a single console for visibility, monitoring, or management across on-premises, hosted, or edge infrastructure. This will extend the universal cloud operating model of the Nutanix Cloud Platform to break down silos and simplify consistently managing apps and data anywhere.

- March 2023: At the World Mobile Congress Barcelona in 2023, it released the industry's prominent entry-level primary and secondary storage portfolio based on a Huawei A-A architecture. This portfolio solution is developed to assist SMEs in building cost-effective data storage systems using the new Huawei OceanStor Dorado 2000 and OceanProtect X3000.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand of Clolud Computing Capabilities Drives the Market Growth

- 4.2.2 Increase in the Demand for Energy-Efficient and Cost-Effective Data Centers

- 4.3 Market Restraints

- 4.3.1 Skilled Workforce Availability and Security Concerns

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Storage Technology

- 5.1.1 Network Attached Storage (NAS)

- 5.1.2 Storage Area Network (SAN)

- 5.1.3 Direct Attached Storage (DAS)

- 5.1.4 Other Technologies

- 5.2 Storage Type

- 5.2.1 Traditional Storage

- 5.2.2 All-Flash Storage

- 5.2.3 Hybrid Storage

- 5.3 End-User

- 5.3.1 IT & Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Media & Entertainment

- 5.3.5 Other End-User

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Hewlett Packard Enterprise

- 6.1.3 Huawei Technologies Co. Ltd.

- 6.1.4 Hitachi Vantara LLC

- 6.1.5 Kingston Technology Company Inc.

- 6.1.6 Pure Storage Inc.

- 6.1.7 Infinidat Ltd.

- 6.1.8 Lenovo Group Limited

- 6.1.9 Fujitsu Limited

- 6.1.10 Oracle Corporation

- 6.1.11 KIOXIA Singapore Pte. Ltd.

- 6.1.12 Commvault Systems Inc.

- 6.1.13 NetApp Inc.

- 6.1.14 Nutanix Inc.