|

市場調査レポート

商品コード

1693521

放出制御肥料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Controlled Release Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 放出制御肥料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 298 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

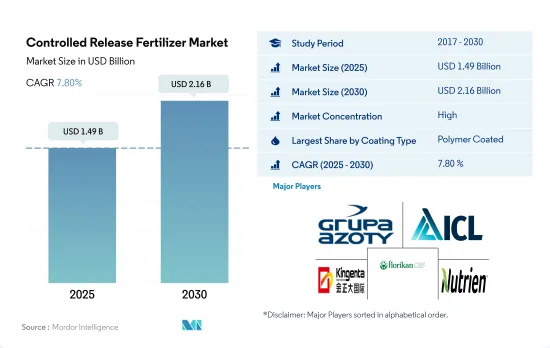

放出制御肥料の市場規模は2025年に14億9,000万米ドルと推定・予測され、2030年には21億6,000万米ドルに達し、予測期間中(2025~2030年)にCAGR 7.80%で成長すると予測されます。

農作業による環境への影響を減らすという農業産業への圧力の高まりと、高い養分効率と正確な施用が市場を牽引します。

- 2022年の特殊肥料市場における放出制御肥料の金額シェアは3.0%でした。環境への影響を最小限に抑えるよう農業セクタへの圧力が高まるなか、コントロール・リリース肥料の市場は成長の態勢を整えています。その高い栄養効率と正確な施用方法によって、2023~2030年のCAGRは7.6%になると予測されています。

- ポリマーコーティング肥料は、過剰な降雨や灌漑によって根域から栄養分が流出するプロセスである栄養分の溶出を抑制する上で重要な役割を果たしています。調査期間中、ポリマーコーティング肥料の市場規模は120.6%急増し、2022年には76.3%の圧倒的な市場シェアを獲得しました。しかし、2020年にはCOVID-19の封鎖に端を発したサプライチェーンの混乱により、世界市場は後退に直面しました。

- ポリマー硫黄コーティング肥料は2022年に18.4%の第2位の市場シェアを占め、CRF市場全体の2億8,160万米ドルに相当します。精密農業や、放出制御肥料を含む特殊肥料の投与といった先進的技術によって生産を強化する取り組みが増加していることが、ポリマー硫黄被覆肥料市場を押し上げると予想されます。ポリマー硫黄被覆肥料市場は、2023~2030年の間にCAGR 7.3%を記録するとみられます。

- 2022年、「その他のCRF」は放出制御肥料市場全体の5.3%を占めました。このセグメントには様々なコーティングが含まれ、2023~2030年にかけて数量ベースで4.3%のCAGRが予測されます。これは、生分解性コーティング肥料への嗜好の高まりと、環境への関心の高まりがその採用を後押ししているためです。

米国が最大の市場シェアを占め、畑作物の栽培面積が多い

- 北米は世界の放出制御肥料市場を独占しています。この地域では米国が放出制御肥料の最大市場で、2022年の市場シェアの69.0%を占めています。

- 欧州は世界の放出制御肥料市場で2番目のシェアを占めています。フランスが22.4%の最大シェアを占め、英国がそれに続きます。

- アジア太平洋は、放出制御肥料の世界第3位の地域市場です。中国はアジア太平洋の放出制御肥料市場を独占しており、2022年の市場シェアの約42.1%を占めています。中国では、ポリマー被覆肥料が放出制御肥料市場で最も高いシェアを記録し、ポリマー硫黄被覆肥料がそれに続いています。ポリマー被覆肥料セグメントは2017年に3,030万米ドルと評価され、2030年末までに9,720万米ドルに達すると予測されています。

- 放出制御型尿素は、世界で最も一般的に使用されているCRFです。窒素損失は稲作農業従事者が直面する主要問題の1つであり、稲の窒素利用効率はしばしば不十分です。これは、揮発、浸出、脱窒による窒素の損失が大きいためです。窒素利用効率を改善する1つの方法は、放出制御型尿素を使用することです。放出制御型尿素は一般に、窒素損失の低減、植物成長の促進、窒素濃度の増加において粒状尿素肥料を上回り、嗜好性を高めています。

- 放出制御肥料の効率向上が、2023~2030年の世界市場を牽引すると予想されます。

世界の放出制御肥料市場動向

増大する食糧需要を満たすための農業への圧力の高まりにより、世界的に畑作物の栽培面積が増加すると予想されます。

- 世界の農業部門は多くの課題に直面しています。国連によると、世界人口は2050年までに90億人を超える可能性があります。この人口増加は、すでに労働力不足と都市化の進展による農地の縮小で生産高が減少している農業に過大な負担をかける可能性があります。国連食糧農業機関によると、2050年までに世界人口の70%が都市に住むようになると予想されています。世界的に耕地が減少しているため、農業従事者は作物の収穫量を増やすために、より多くの肥料を利用する必要があります。

- アジア太平洋は世界最大の農産物生産地です。農業はこの地域の経済にとって不可欠であり、全労働人口の約20%を雇用しています。畑作物の栽培がこの地域を支配しており、地域全体の作物栽培面積の約95%以上を占めています。米、小麦、トウモロコシがこの地域で生産される主要な畑作物で、2022年の総栽培面積の約24.3%を占めます。

- 北米は世界第2位の耕作可能地域です。その農場では、畑作物を中心に多様な作物が栽培されています。特に、トウモロコシ、綿花、米、大豆、小麦は、米国農務省が強調しているように、著名な畑作物です。2022年、米国は北米の作物栽培面積の46.2%を占めました。しかし、同国は2017~2019年にかけて作物栽培面積の大幅な減少を確認したが、これは主にテキサスやヒューストンのような地域で深刻な洪水につながる悪環境条件のためです。

畑作物における窒素、カリウム、リンなどの一次栄養素の世界平均施用量は164.31kg/haです。

- トウモロコシ/メイズ、菜種/カノーラ、綿花、ソルガム、コメ、小麦、大豆は、一次養分の消費量という点で、世界の主要作物の一部です。これらの畑作物の一次養分施用量は、それぞれ230.57 kg/ha、255.75 kg/ha、172.70 kg/ha、158.46 kg/ha、154.49 kg/ha、135.35 kg/ha、120.97 kg/haです。一次養分は、植物の代謝プロセスにおいて重要な役割を果たし、細胞、細胞膜、葉緑素などの組織の形成を助けるため、作物にとって極めて重要です。リンは高品質の作物を育てるために不可欠であり、カリウムは植物の成長と開発に必要な酵素を活性化します。

- 畑作物における窒素、カリウム、リンの世界平均施用量は164.31kg/haです。窒素は、畑作物で最も広く使用されている元肥です。その施用量は224.6 kg/ヘクタールであり、次いでカリ肥料が150.3 kg/ヘクタール、リンは2022年の施用量が117.9 kg/ヘクタールで3番目に多く消費される肥料です。

- 2022年の窒素施用量は菜種が最も多く、347.4kg/ヘクタールでした。同様に、リン施用率はトウモロコシで最も高く156.3 kg/ヘクタール、カリウム施用率はカノーラで最も高く248.6 kg/ヘクタールでした。

- 世界の畑作物の栽培面積は、特に南米とアジア太平洋諸国で増加しています。これらは肥料の成長市場です。特殊肥料はその効率性から、欧州や北米などの先進地域や、栄養不足が蔓延しているその他の中東・アフリカで広く使用されています。これらの要因が、2023~2030年にかけての世界の一次栄養肥料市場を牽引すると予想されます。

放出制御肥料産業概要

放出制御肥料市場はかなり統合されており、上位5社で77.38%を占めています。この市場の主要企業は、Grupa Azoty S.A.(Compo Expert)、ICL Group Ltd、Kingenta Ecological Engineering Group、New Mountain Capital(Florikan)and Nutrien Ltd.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 主要養分

- 畑作物

- 園芸作物

- 主要養分

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- コーティングタイプ

- ポリマーコーティング

- ポリマー・硫黄コーティング

- その他

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

- 地域

- アジア太平洋

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

- 欧州

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他の欧州

- 中東・アフリカ

- ナイジェリア

- サウジアラビア

- 南アフリカ

- トルコ

- その他の中東・アフリカ

- 北米

- カナダ

- メキシコ

- 米国

- その他の北米地域

- 南米

- アルゼンチン

- ブラジル

- その他の南米

- アジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ekompany International BV(DeltaChem)

- Grupa Azoty S.A.(Compo Expert)

- Haifa Group

- ICL Group Ltd

- Kingenta Ecological Engineering Group Co., Ltd.

- Mivena BV

- New Mountain Capital(Florikan)

- Nutrien Ltd.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Controlled Release Fertilizer Market size is estimated at 1.49 billion USD in 2025, and is expected to reach 2.16 billion USD by 2030, growing at a CAGR of 7.80% during the forecast period (2025-2030).

The rising pressure on the agriculture industry to reduce the environmental impact of farming practices and the high nutrient efficiency and precise application will drive the market

- In 2022, control-release fertilizers held a 3.0% value share of the specialty fertilizer market. With mounting pressure on the agriculture sector to minimize environmental impact, the market for control release fertilizers is poised for growth. Their high nutrient efficiency and precise application methods are projected to drive a 7.6% value CAGR from 2023 to 2030.

- Polymer-coated fertilizers play a crucial role in curbing nutrient leaching, a process where excessive rainfall or irrigation washes away nutrients from the root zone. During the study period, the market value of polymer-coated fertilizers surged by 120.6%, capturing a dominant 76.3% market share in 2022. However, the global market faced a setback in 2020 due to supply chain disruptions triggered by the COVID-19 lockdown.

- The polymer-sulfur-coated fertilizers hold the second-largest market share of 18.4% in 2022, worth USD 281.6 million of the overall CRF market. The increasing efforts to enhance production through advanced techniques such as precision farming and dosing of specialty fertilizers, including controlled-release fertilizers, are expected to boost the market for polymers with sulfur-coated fertilizers. The market for polymer-sulfur-coated fertilizers is likely to record a CAGR of 7.3% during 2023-2030.

- In 2022, "other CRFs" constituted 5.3% of the total controlled-release fertilizer market. This segment, encompassing various coatings, is anticipated to witness a 4.3% CAGR in volume from 2023 to 2030. The upswing is attributed to the growing preference for biodegradable coated fertilizers and heightened environmental concerns driving their adoption.

The United States accounted for the largest market share, with field crops accounting for a higher cultivation area

- North America dominates the global controlled-release fertilizer market. In the region, the United States is the largest market for controlled-release fertilizers, accounting for 69.0% of the market share in 2022.

- Europe occupied the second-largest share in the global controlled-release fertilizer market. The controlled-release fertilizer market in Europe is observed to have notably stable growth across all countries in the region, with France occupying the largest share of 22.4%, followed by the United Kingdom for the year 2022.

- The Asia-Pacific is the third-largest regional market for controlled-release fertilizers globally. China dominates the APAC controlled-release fertilizers market, accounting for about 42.1% of the market share in 2022. In China, polymer-coated fertilizers recorded the highest share in the controlled-release fertilizers market, followed by polymer sulfur-coated fertilizers. The polymer-coated fertilizers segment was valued at USD 30.3 million in 2017 and is anticipated to reach USD 97.2 million by the end of 2030.

- Controlled-release urea is the most commonly used form of CRF in the world. Nitrogen loss is one of the main problems faced by rice farmers, and the efficiency of nitrogen utilization in rice is often inadequate. This is due to the large loss of nitrogen due to volatilization, leaching, and denitrification. One way to improve nitrogen efficiency is to use controlled-release urea. Controlled-release urea generally outperforms granular urea fertilizers in reducing nitrogen loss, stimulating plant growth, and increasing nitrogen concentration, thus boosting its preference.

- The increased efficiency of controlled-release fertilizers is anticipated to drive the global market from 2023 to 2030.

Global Controlled Release Fertilizer Market Trends

Rising pressure on the agriculture industry to meet the growing demand for food is expected to increase the area under field crop cultivation globally

- The global agricultural sector is facing many challenges. According to the UN, the world population may exceed 9 billion by 2050. This population growth may overburden the agricultural industry, which is already experiencing an output loss due to a lack of laborers and the shrinkage of agricultural fields caused by rising urbanization. According to the Food and Agriculture Organization, 70% of the global population is expected to live in cities by 2050. Due to the global loss of arable land, farmers now need to utilize more fertilizers to increase crop yields.

- Asia-Pacific is the world's largest producer of agricultural products. Agriculture is critical to the region's economy, as it employs about 20% of the total available workforce. Field crop cultivation dominates the region, accounting for about more than 95% of the total crop area in the region. Rice, wheat, and corn are the major field crops produced in the region, together accounting for about 24.3% of the total crop area in 2022.

- North America ranks as the second-largest arable region globally. Its farms cultivate a diverse range of crops, with a focus on field crops. Notably, corn, cotton, rice, soybean, and wheat are the prominent field crops, as highlighted by the USDA. In 2022, the United States accounted for 46.2% of North America's crop cultivation area. However, the country witnessed a significant drop in crop acreage between 2017 and 2019, primarily due to adverse environmental conditions, leading to severe flooding in regions like Texas and Houston.

The global average application rate of primary nutrients like nitrogen, potassium, and phosphorus in field crops is 164.31 kg/ha

- Corn/maize, rapeseed/canola, cotton, sorghum, rice, wheat, and soybean are some of the major crops worldwide in terms of consumption of primary nutrients. The primary nutrient application rates for these field crops are 230.57 kg/ha, 255.75 kg/ha, 172.70 kg/ha, 158.46 kg/ha, 154.49 kg/ha, 135.35 kg/ha, and 120.97 kg/ha, respectively. Primary nutrient fertilizers are crucial for crops because they play an essential role in plant metabolic processes and assist in forming tissues such as cells, cell membranes, and chlorophyll. Phosphorus is essential for growing high-quality crops, while potassium activates the enzymes needed for plant growth and development.

- The global average application rate of nitrogen, potassium, and phosphorus in field crops is 164.31 kg/ha. Nitrogen is the most widely used primary nutrient fertilizer used in field crops. It accounted for an application rate of 224.6 kg/hectare, followed by potassic fertilizers with 150.3 kg/hectare, and phosphorus as the third-most consumed fertilizer with an application rate of 117.9 kg/hectare in 2022.

- In 2022, the nitrogen application rate was highest in rapeseed, amounting to 347.4 kg/hectare. Similarly, the phosphorus application rate was the highest in corn, at 156.3 kg/hectare, while the potassium application rate was highest in canola, at 248.6 kg/hectare.

- Global field crop cultivation area is increasing, particularly in South American and Asia-Pacific countries. These are the growing markets for fertilizers. Due to their efficiency, specialty fertilizers are widely used in developed regions such as Europe and North America, as well as other regions with widespread nutrient deficiencies. These factors are anticipated to drive the global primary nutrient fertilizers market between 2023 and 2030.

Controlled Release Fertilizer Industry Overview

The Controlled Release Fertilizer Market is fairly consolidated, with the top five companies occupying 77.38%. The major players in this market are Grupa Azoty S.A. (Compo Expert), ICL Group Ltd, Kingenta Ecological Engineering Group Co., Ltd., New Mountain Capital (Florikan) and Nutrien Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 Bangladesh

- 5.3.1.3 China

- 5.3.1.4 India

- 5.3.1.5 Indonesia

- 5.3.1.6 Japan

- 5.3.1.7 Pakistan

- 5.3.1.8 Philippines

- 5.3.1.9 Thailand

- 5.3.1.10 Vietnam

- 5.3.1.11 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Netherlands

- 5.3.2.5 Russia

- 5.3.2.6 Spain

- 5.3.2.7 Ukraine

- 5.3.2.8 United Kingdom

- 5.3.2.9 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Nigeria

- 5.3.3.2 Saudi Arabia

- 5.3.3.3 South Africa

- 5.3.3.4 Turkey

- 5.3.3.5 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ekompany International BV (DeltaChem)

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 ICL Group Ltd

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Mivena BV

- 6.4.7 New Mountain Capital (Florikan)

- 6.4.8 Nutrien Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms