|

市場調査レポート

商品コード

1693527

北米の放出制御肥料:市場シェア分析、産業動向、成長予測(2025年~2030年)North America Controlled Release Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の放出制御肥料:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 157 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

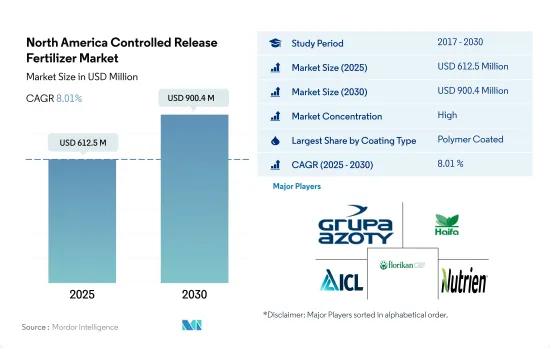

北米の放出制御肥料市場規模は2025年に6億1,250万米ドルと推定され、2030年には9億40万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは8.01%で成長する見込みです。

適切なタイミングで適切な量の栄養素を摂取するための取り組みが、この地域でのCRF採用を増加させています。

- 2017~2022年にかけて、北米の放出制御肥料市場のCAGRは15.0%でした。精密農業は、この地域で広く受け入れられているアプローチであり、作物へのタイムリーで正確な栄養供給を優先しています。その中で放出制御肥料は極めて重要な役割を担っており、作物に最適な栄養分を確実に供給し、精密農業に不可欠なものとなっています。

- 2022年には、畑作物が北米の放出制御肥料市場を独占し、市場シェアの88.4%を占めました。園芸作物は3.7%でした。放出制御型肥料は、穀物、穀類、野菜、果樹園、苗床などの高価値作物で幅広く使用されています。連作作物への特殊化学肥料の導入はまだ普及していないが、穀物価格の高騰、環境問題への関心の高まり、養分施用規制の厳格化などにより、徐々に増加しています。

- 2022年には、米国が放出制御肥料の消費をリードし、69.9%を占めました。この優位性は、同国が養分施用量と肥料汚染防止を規制していることに起因しています。

- 環境保護庁(EPA)と米国農務省(USDA)は、肥料ラボ(TFI)、国際肥料開発センター(IFDC)、自然保護団体(TNC)、全米トウモロコシ生産者協会(NCGA)といった主要利害関係者と協力して、肥料産業の技術的発展を認識しています。彼らの目的は、農業従事者の間で放出制御型肥料に対する認識を高め、国の畑作生産にプラスの波及効果をもたらすことです。

肥料の過剰使用と主要作物による窒素使用の減少に関する環境問題への懸念が、CRF市場を牽引する可能性があります。

- 2022年、米国はCRF市場の69.9%のシェアを記録しました。調査期間中のCAGRは14.0%でした。ポリマーコーティングが首位に立ち、2022年には76.4%のシェアを獲得しました。米国の作付面積の約69%は畑作物で、大麦、トウモロコシ、綿花、オート麦、ピーナッツ、ソルガム、大豆、小麦などが含まれます。これらの作物の窒素要求量が高いことから、窒素効率の高さで知られるポリマーコーティング尿素の採用が増加しており、ポリマーコーティング肥料の市場シェアをさらに押し上げています。

- カナダでは小麦、キャノーラ、トウモロコシなどの畑作物の栽培が急増しています。この動向を支えるため、カナダ政府はファーム・クレジット・カナダ(Farm Credit Canada)のような取り組みを通じて、農業従事者の信用供与の機会を増やし、特に放出制御肥料のような投入資材への融資を促進しています。このような有利な環境は、今後数年間、カナダの放出制御型肥料市場を推進する態勢を整えています。

- 2021年、メキシコ議会は2022年連邦政府予算において、農業農村開発事務局(SADER)に対する27億米ドルの予算を承認しました。この配分の約70%は肥料補助金に充てられました。これはメキシコの放出制御肥料市場の主要な促進要因になると予想されます。

- その他の北米地域では、精密農業の推進と気候変動に対応した取り組みによって、放出制御肥料の採用が急増しています。これらの対策は環境への懸念に対処し、サステイナブル農法を促進するものです。

- この地域全体では、畑作物の生産を促進することが急務であり、政府の強力な取り組みや農業従事者の意識の高まりと相まって、今後数年間の有望な市場展望の舞台となっています。

北米の放出制御肥料市場動向

補助金など政府による財政支援が畑作物の拡大に貢献

- 北米の農場では、畑作物を中心にさまざまな作物が栽培されています。トウモロコシ、綿花、米、大豆、小麦は、この地域で主要な畑作物の一部です。米国、カナダ、メキシコは、この地域の農業生産に大きく貢献しています。2022年、北米では畑作物が栽培全体の約97.6%を占め、穀物と油糧種子が市場を独占しています。

- 国別では米国が市場を独占し、調査期間中の作物栽培面積全体の1億3,570万ヘクタールを占めています。中でも畑作と園芸が面積の大半を占めており、2022年には97.2%と2.8%を占めています。しかし、2018~2019年にかけて、国は作物栽培面積の大幅な落ち込みを確認したが、これは主にテキサスやヒューストンなどの地域で大洪水をもたらした不利な環境条件によるものです。

- 最大の栽培作物はトウモロコシで、その大部分は米国中西部の「コーンベルト」と呼ばれる伝統的地域で栽培されており、インディアナ州西部、イリノイ州、アイオワ州、ミズーリ州、ネブラスカ州東部、カンザス州東部をほぼカバーし、トウモロコシ(メイズ)と大豆が主要作物となっています。また、この地域は米の主要輸出国であり、米の栽培は主に4つの地域に集中しています。従って、この地域の畑作物に対する市場の可能性が高まり、政府の資金援助と保護が強化されることで、この地域の畑作物栽培面積が増加すると予想されます。

一次栄養素の中で、窒素は畑作物により多く施用されます。

- 稲、トウモロコシ/メイズ、小麦、菜種/カノーラなどの畑作物は、この地域で主要な一次養分を消費する作物の一部です。2022年には、約140.85kg/ヘクタールの一次養分がコメで消費され、次いで118.40kg/ヘクタールの一次養分が菜種/カノーラで消費されます。穀物が最も多くの窒素肥料を消費すると予想されます。この地域では集中的に栽培されているため、土壌の養分が枯渇し、生育を補うために多くの肥料が必要となります。

- 主栄養素の中では窒素の施用量が多く、2022年には約74.0%を占め、畑作物では229.8kg/ヘクタールに相当します。しかし、窒素欠乏はこの地域で最も一般的な作物養分の問題のひとつです。そのため、窒素補給のほとんどは土壌施用によって行われています。土壌に施用されると、窒素は植物が吸収しやすいようにミネラル硝酸塩に変換されます。主要な窒素消費作物である菜種は、米国で広く栽培されています。

- 菜種は、潤滑油、油圧作動油、プラスチックなどの工業用途の油の抽出に使用されます。肥料の使用量は土壌の質と降雨の可能性によって決まるが、窒素の必要量は1エーカー当たり100ポンドから150ポンドです。リンとカリウムの施肥率も土壌によって異なります。しかし、AgMRCによると、推奨される割合は0~80ポンド/エーカー、0~140ポンド/エーカーです。

- 一次養分は様々な作物にとって主要な養分源であるため、土壌の枯渇や溶出などにより、その施用量は年々大幅に増加すると予想されます。

北米の放出制御肥料産業概要

北米の放出制御肥料市場はかなり統合されており、上位5社で88.15%を占めています。この市場の主要企業は、Grupa Azoty S.A.(Compo Expert)、Haifa Group、ICL Group Ltd、New Mountain Capital(Florikan)and Nutrien Ltd.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 主要養分

- 畑作物

- 園芸作物

- 主要養分

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- コーティングタイプ

- ポリマーコーティング

- ポリマー・硫黄コーティング

- その他

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

- 生産国

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- AgroLiquid

- Grupa Azoty S.A.(Compo Expert)

- Haifa Group

- ICL Group Ltd

- New Mountain Capital(Florikan)

- Nutrien Ltd.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The North America Controlled Release Fertilizer Market size is estimated at 612.5 million USD in 2025, and is expected to reach 900.4 million USD by 2030, growing at a CAGR of 8.01% during the forecast period (2025-2030).

Initiatives toward achieving right amount of nutrients at the right time will increase the CRFs adoption in the region

- Between 2017 and 2022, the North American controlled-release fertilizers market witnessed a CAGR of 15.0%. Precision farming, a widely embraced approach in the region, prioritizes timely and precise nutrient delivery to crops. Controlled-release fertilizers, in this context, assume a pivotal role, ensuring crops receive optimal nutrient dosages, thus becoming integral to precision farming.

- In 2022, field crops dominated the North American controlled-release fertilizers market, capturing 88.4% of the market share. Horticultural crops accounted for 3.7%. Controlled-release fertilizers found extensive usage in high-value crops like cereals, grains, vegetables, orchards, and nurseries. While specialty chemical adoption in row crops is not yet widespread, it is gradually rising due to surging grain prices, heightened environmental concerns, and stricter nutrient application regulations.

- In 2022, the United States led the consumption of controlled-release fertilizers, accounting for 69.9%. This dominance can be attributed to the nation's regulations governing nutrient application rates and fertilizer pollution control.

- Recognizing the technological strides in the fertilizer industry, the Environmental Protection Agency (EPA) and the US Department of Agriculture (USDA) have collaborated with key stakeholders like The Fertilizer Institute (TFI), the International Fertilizer Development Center (IFDC), The Nature Conservancy (TNC), and the National Corn Growers Association (NCGA). Their collective aim is to raise awareness about controlled-release fertilizers among farmers, with a positive ripple effect anticipated on the country's field crop production.

Environmental concerns about excessive use of fertilizers and reduced nitrogen use by major crops may drive the CRF market

- In 2022, the United States recorded a 69.9% share of the CRF market. The market grew by a CAGR of 14.0% during the study period. Polymer coating emerged as the leader, commanding a 76.4% share in 2022. Around 69% of the US cropland is dedicated to field crops, including barley, corn, cotton, oats, peanuts, sorghum, soybeans, and wheat. Given the high nitrogen requirements of these crops, the adoption of polymer-coated urea, known for its nitrogen efficiency, is on the rise, further bolstering the market share of polymer-coated fertilizers.

- Canada is witnessing a surge in the cultivation of field crops like wheat, canola, and maize. To support this trend, the Canadian government, through initiatives like Farm Credit Canada, is facilitating increased credit accessibility for farmers, specifically for inputs like controlled-release fertilizers. This favorable environment is poised to propel the controlled-release fertilizer market in Canada in the coming years.

- In 2021, the Mexican legislature approved a USD 2.70 billion budget for the Secretariat of Agriculture and Rural Development (SADER) in its 2022 Federal Government Budget. Around 70% of this allocation was earmarked for fertilizer subsidies. This is expected to be a key driver for the controlled-release fertilizer market in Mexico.

- The Rest of North America is witnessing a surge in the adoption of controlled-release fertilizers driven by the push for precision agriculture practices and climate-smart initiatives. These measures address environmental concerns and promote sustainable farming practices.

- Across the region, the imperative to boost field crop production, coupled with robust government initiatives and growing farmer awareness, sets the stage for a promising market outlook in the coming years.

North America Controlled Release Fertilizer Market Trends

The financial support by the government such as subsidies has contributed to the expansion of field crops

- A wide array of crops are grown on North American farms, mainly covering field crops. Corn, Cotton, Rice, Soybean, and Wheat are some of the dominating field crops across the region. The United States, Canada, and Mexico are major contributors to the region's agricultural output. In 2022, field crops covered around 97.6% of the overall cultivation in North America, with cereals and oilseeds dominating the market.

- By country, the United States dominates the market, covering 135.7 million hectares of the overall area under crop cultivation during the study period. Among them, field crops and horticulture are covering the majority of the area and accounted for 97.2% and 2.8% in 2022. However, between 2018-2019, the country witnessed a significant dip in crop acreages which is majorly due to unfavorable environmental conditions resulting in heavy floods in areas like Texas and Houston.

- The largest crop cultivated is corn, the majority of which is grown in a region known as the 'Corn Belt' traditional area in the midwestern United States, roughly covering western Indiana, Illinois, Iowa, Missouri, eastern Nebraska, and eastern Kansas, in which corn (maize) and soybeans are the dominant crops. Also, It is the major rice exporter, and the rice cultivation in the region is mainly concentrated within 4 regions with three in the South and one in California. Therefore, the increased market potential for the region's field crop, coupled with the increased government funding and protection is anticipated to positively drive the area under field crop cultivation in the region.

Among all the primary nutrients, nitrogen is applied in a higher quantity for field crops

- Field crops, such as rice, corn/maize, wheat, and rapeseed/canola, are some of the major primary nutrient-consuming crops in the region. In 2022, about 140.85 kg/hectare of primary nutrients were consumed by rice, followed by 118.40 kg/hectare consumed by rapeseed/canola. Cereals are anticipated to consume the maximum amount of nitrogen fertilizer. As they are grown intensively in the region, they deplete the nutrients in the soil and require more fertilizers to supplement growth.

- Among all the primary nutrients, nitrogen is applied in a higher quantity, accounting for about 74.0% in 2022, equivalent to 229.8 kg/hectare for field crops. Nitrogen deficiency, however, is one of the most prevalent crop nutrient problems in the region. Hence, most of the nitrogen supplement is provided through soil application. When applied to the soil, nitrogen is converted to mineral nitrate for the plants to absorb easily. Rapeseed, the major nitrogen-consuming crop, is widely grown in the United States.

- Rapeseed is used for extracting oil for industrial applications, like lubricants, hydraulic fluids, and plastics. While fertilizer usage is based on soil quality and rainfall potential, its nitrogen requirements range from 100 to 150 lbs/acre. Phosphorus and potassium fertility rates also vary from soil to soil. However, the recommended rates range from 0 to 80 lbs/acre and 0 to 140 lbs/acre, as per the AgMRC.

- Since primary nutrients are the major sources of nutrients for various crops, their application rates are anticipated to grow significantly over the years due to soil depletion, leaching, etc.

North America Controlled Release Fertilizer Industry Overview

The North America Controlled Release Fertilizer Market is fairly consolidated, with the top five companies occupying 88.15%. The major players in this market are Grupa Azoty S.A. (Compo Expert), Haifa Group, ICL Group Ltd, New Mountain Capital (Florikan) and Nutrien Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 AgroLiquid

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 ICL Group Ltd

- 6.4.5 New Mountain Capital (Florikan)

- 6.4.6 Nutrien Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms