|

市場調査レポート

商品コード

1693502

米国の放出制御肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)United States Controlled Release Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の放出制御肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 139 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

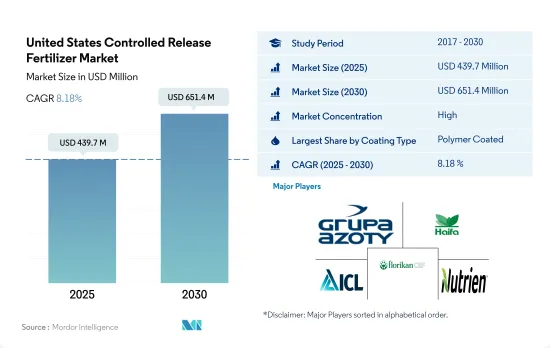

米国の放出制御肥料市場規模は2025年に4億3,970万米ドルと推計され、2030年には6億5,140万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは8.18%で成長すると予測されます。

窒素とリンの溶出を低減するCRFの効率性が市場成長を促進

- 米国の放出制御肥料の市場規模は、2022年に4億2,870万米ドルとなりました。環境への影響を軽減するという農業部門への圧力の高まりと、栄養効率の向上と正確な施用という利点が相まって、市場価値は2023年から2030年にかけて8.0%の堅調なCAGRで推移すると予測されています。

- 放出制御肥料は、緩やかで長時間の養分放出を実現し、作物が成長サイクルを通じて重要な要素を安定的に供給できるようにします。養分の溶出や流出を抑制することで、これらの肥料は畑作農業が環境に与える影響を軽減する上で極めて重要な役割を果たし、特に水質や汚染に対する懸念に対処する上で重要です。

- 圃場試験では、コーティングされた放出制御肥料がコーティングされていない肥料よりも優れていることが示されており、窒素ベースの肥料では69.0%、リン酸ベースの肥料では82.0%も溶出を削減しています。対照的に、コーティングされていない従来の尿素は、揮発によってアンモニア含有量の最大40%を失う可能性があります。複数年にわたる広範な試験により、コーティング尿素はアンモニア損失を最低95.0%削減できることが一貫して実証されています。

- 2022年には、ポリマーコーティングが米国の放出制御肥料市場の76.4%を占め、圧倒的なシェアを占めています。環境とコストへの配慮が、ポリマー・コーティングされた放出制御肥料の需要を牽引しています。ポリマーコーティング分野は、2023年から2030年にかけて7.7%の健全な成長率が見込まれています。

- 米国では、肥料の過剰蓄積に起因する環境への影響を抑制することを目的とした政府規制によって、放出制御肥料の需要が急増しています。

米国の放出制御肥料市場動向

大豆とトウモロコシは米国で栽培されている2大作物です。

- 米国では、人口が2020年の3億3,590万人から2022年には3億3,820万人に増加します。2000年以降、農地の総面積は5,000万エーカー近く減少し、2022年には8億9,340万エーカーに達します。農地が限られているということは、農業投入物を使用して農業生産性を高める必要があることを示しています。作物の生産性を高めるために、長い間肥料が使用されてきました。米国の主要4作物は、トウモロコシ、綿花、大豆、小麦であり、2022年の主要作物作付面積の65.7%以上を占める。

- 大豆とトウモロコシは米国で栽培されている2大作物です。2022年には、大豆の栽培面積が最も多く、米国の耕地面積全体の25.8%を占め、次いでトウモロコシが25.7%、小麦が11.1%です。これらの作物の大部分は、インディアナ西部、イリノイ州、アイオワ州、ミズーリ州、ネブラスカ州東部、カンザス州東部をカバーする「コーンベルト」と呼ばれる地域で栽培されています。トウモロコシと大豆の生産がこの地域を支配しています。米国農務省によれば、米国は米の主要輸出国であり、その栽培の大部分は4つの地域で行われています。

- 農業資材メーカーは、農家の正確な肥料散布を支援する革新的な製品を開発しています。これにより、農家は効率性を高めながら栽培コストを削減することができます。同国の畑作産業は計り知れない市場ポテンシャルを秘めており、政府からの資金援助や支援が増えることで、この分野の作物栽培のプラス成長が期待されます。

窒素欠乏は、米国の作付面積全体で最も広く見られる作物養分の問題のひとつです。

- 米国の畑作物における一次養分(窒素、カリウム、リン)の平均施用量は、2022年には1ヘクタール当たり約166.61kgとなりました。このうち窒素が45.93%を占め、カリウムが28.11%、リンが25.96%と続きます。

- 畑作物の中では菜種/カノーラが突出しており、2022年の平均一次養分施用量はヘクタール当たり284.92kgで、この分野では最高です。一次養分の中では窒素がリードしており、平均施用量は1ヘクタール当たり229.60kgです。この優位性は、窒素が葉緑素とアミノ酸の重要な構成要素であるため、植物の代謝において極めて重要な役割を担っていることに起因しています。

- 米国では、トウモロコシ/メイズが第2位の畑作作物で、菜種/カノーラが僅差で続いています。2022年、農家は平均して1ヘクタール当たり245.40kgの一次養分を施用しました。トウモロコシだけで、国内の畑作物総生産量の約31.44%を占めています。一次養分の施用に関しては、2022年のトウモロコシの窒素要求量は50.06%、リンは23.77%、カリは26.17%でした。

- 一次栄養素は、植物の酵素機能、細胞成長、生化学的プロセスの強化において極めて重要な役割を果たします。これらの栄養素が欠乏すると、植物の健康に大きな影響を与え、成長を阻害し、作物の収量を妨げる可能性があります。生産性を向上させる必要性が高まっていることから、畑作物への一次栄養素の施用は顕著な上昇を示すと予想されます。

米国の放出制御肥料産業の概要

米国の放出制御肥料市場はかなり統合されており、上位5社で89.58%を占めています。この市場の主要企業は以下の通りです。 Grupa Azoty S.A.(Compo Expert), Haifa Group, ICL Group Ltd, New Mountain Capital(Florikan)and Nutrien Ltd.(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 主要養分

- 畑作物

- 園芸作物

- 主要養分

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- コーティングタイプ

- ポリマー・コーティング

- ポリマー・硫黄コーティング

- その他

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- AgroLiquid

- Grupa Azoty S.A.(Compo Expert)

- Haifa Group

- ICL Group Ltd

- New Mountain Capital(Florikan)

- Nutrien Ltd.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The United States Controlled Release Fertilizer Market size is estimated at 439.7 million USD in 2025, and is expected to reach 651.4 million USD by 2030, growing at a CAGR of 8.18% during the forecast period (2025-2030).

The efficiency of CRFs in reducing nitrogen and phosphorus leaching propels market growth

- The market for controlled-release fertilizers in the United States was valued at USD 428.7 million in 2022. With mounting pressure on the agriculture sector to mitigate environmental repercussions, coupled with the benefits of enhanced nutrient efficiency and precise application, the market value is projected to witness a robust CAGR of 8.0% from 2023 to 2030.

- Controlled-release fertilizers offer a gradual and prolonged nutrient release, ensuring crops receive a consistent supply of vital elements throughout their growth cycle. By curbing nutrient leaching and runoff, these fertilizers play a pivotal role in reducing the environmental impact of field crop agriculture, particularly in addressing concerns about water quality and pollution.

- Field trials have shown that coated controlled-release fertilizers outperform their uncoated counterparts, reducing leaching by 69.0% for nitrogen-based fertilizers and 82.0% for phosphate-based ones. In contrast, uncoated conventional urea can lose up to 40% of its ammonia content through volatilization. Extensive testing over multiple years has consistently demonstrated that coated urea can slash ammonia losses by a minimum of 95.0%.

- In 2022, polymer coating dominated the United States controlled-release fertilizer market, accounting for 76.4% of the industry. Environmental and cost considerations are driving the demand for polymer-coated controlled-release fertilizers, thanks to the nation's focus on field crop cultivation. The polymer-coated segment is expected to witness a healthy growth rate of 7.7% from 2023 to 2030.

- The United States is witnessing a surge in demand for controlled-release fertilizers, propelled by government regulations aimed at curbing the environmental impact stemming from excessive fertilizer accumulation.

United States Controlled Release Fertilizer Market Trends

Soybean and corn are the two prominent crops grown in the United States

- In the United States, the population increased from 335.9 million in 2020 to 338.2 million in 2022. From 2000 onwards, the total farmland area decreased by almost 50 million acres, reaching a total of 893.4 million acres in 2022. The limited farmland indicates the need to increase agricultural productivity with the use of agri inputs. Fertilizers have been used for a long time to increase the productivity of crops. The four major crops in the United States are corn, cotton, soybean, and wheat, which account for more than 65.7% of the principal crop acreage in 2022.

- Soybean and corn are the two prominent crops grown in the United States. In 2022, soybean had the highest area under cultivation, accounting for 25.8% of the total arable land in the United States, followed by corn at 25.7% and wheat at 11.1%. The majority of these crops are grown in a region known as the "Corn Belt," which covers Western Indiana, Illinois, Iowa, Missouri, Eastern Nebraska, and Eastern Kansas. The production of corn (maize) and soybeans dominates this area. Additionally, the United States is a major exporter of rice, with most of the cultivation happening in four regions, three of which are in the South and one in California, according to the USDA.

- Manufacturers of farm inputs are developing innovative products to assist farmers with the precise application of fertilizers. This is helping farmers in reducing the cost of cultivation while increasing efficiency. The field crop industry of the country has immense market potential, and with increased government funding and support, it is expected to drive positive growth in crop cultivation in this area.

Nitrogen deficiency is one of the most prevalent crop nutrient problems across cropping areas in the United States

- The average application rate of primary nutrients (nitrogen, potassium, and phosphorus) in field crops in the United States stood at approximately 166.61 kg per hectare in the year 2022. Nitrogen represented 45.93% of this application, followed by potassium at 28.11% and phosphorus at 25.96% in the same year.

- Rapeseed/canola stands out among field crops, with an average primary nutrient application rate of 284.92 kg per hectare, the highest in this sector in 2022. Among the primary nutrients, nitrogen takes the lead, with an average application rate of 229.60 kg per hectare. This dominance can be attributed to nitrogen's pivotal role in plant metabolism, as it is a key component of both chlorophyll and amino acids.

- In the United States, corn/maize stands as the second-largest field crop, with rapeseed/canola following closely behind. On average, farmers applied 245.40 kg of primary nutrients per hectare in 2022. Corn alone contributes to around 31.44% of the nation's total field crop production. When it came to primary nutrient application, corn's nitrogen requirement accounted for 50.06%, phosphorus stood at 23.77%, and potash at 26.17% in 2022.

- Primary nutrients play a pivotal role in enhancing plant enzyme function, cellular growth, and biochemical processes. A deficiency in these nutrients can significantly impact plant health, stifle growth, and hamper crop yields. Given the rising need for increased productivity, the application of primary nutrients in field crops is expected to witness a notable uptick.

United States Controlled Release Fertilizer Industry Overview

The United States Controlled Release Fertilizer Market is fairly consolidated, with the top five companies occupying 89.58%. The major players in this market are Grupa Azoty S.A. (Compo Expert), Haifa Group, ICL Group Ltd, New Mountain Capital (Florikan) and Nutrien Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 AgroLiquid

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 ICL Group Ltd

- 6.4.5 New Mountain Capital (Florikan)

- 6.4.6 Nutrien Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms