中国の放出制御肥料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

China Controlled Release Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 131 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693507

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

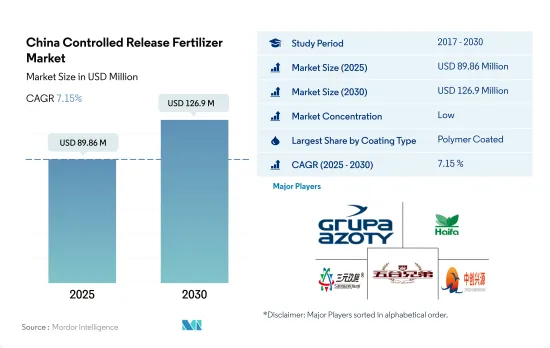

中国の放出制御肥料市場規模は2025年に8,986万米ドルと推定され、2030年には1億2,690万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは7.15%で成長する見込みです。

ポリマー被覆尿素は含有量が高いため、国内で最も採用されているCRFです。

- 2022年には、放出制御肥料(CRF)は中国の特殊肥料市場のわずか0.6%を占めるに過ぎなかりました。しかし、CRFの市場規模は過去一貫して上昇基調を示し、2023~2030年のCAGRは6.9%と堅調に推移すると予測されています。

- CRFの中では、ポリマーコーティング尿素が中国における主要品種として際立っています。これは主に、窒素(N)含有量が高く、被覆が薄く、分解しやすく、放出期間が長いためです。米、トウモロコシ、小麦などの主食作物の基肥として広く使われています。尿素を含むポリマーコーティング肥料は、2022年にCRFセグメントの75.9%という大きなシェアを占めました。注目すべきは、ポリマーコーティングに採用されている具体的な技術はメーカーによって異なり、コーティング材料とプロセスの選択に影響されていることです。

- 硫黄を濃縮したポリマーコーティング肥料は、作物の品質と回復力に好影響を与えるため好まれています。硫黄と窒素の相乗効果により、作物の硝酸レベルが向上し、全体的な品質が向上します。ポリマー硫黄コーティング肥料のサブセットである窒素肥料は、2022年にこのセグメントで59.7%の圧倒的シェアを占めました。

- 化学コーティングの他に、バイオベースのポリウレタン、エポキシ樹脂、ポリオレフィンワックス複合材を含む、バイオベースのコーティングの肥料への動向が高まっています。政府からの需要の高まりに後押しされたこれらのコーティングは、特に「その他」のカテゴリーで際立っています。2022年、「その他」セグメントは中国の放出制御肥料市場の5.4%を占めます。

- このような明確な利点と進化する動向を考慮すると、被覆放出制御肥料の需要は今後数年で大きく成長する見込みです。

中国の放出制御肥料の市場動向

栽培面積の拡大は、食糧需要の増加と主食の自給自足を目指す国の目標に後押しされています。

- 中国の畑作物の栽培面積は、2017年の1億3,050万haから2021年には1億2,780万haに増加し、総栽培面積の71.4%を占めます。畑作物の中ではトウモロコシが34.2%と最大のシェアを占め、次いでコメが23.6%、小麦が18.3%です。耕作面積の増加は、同国における肥料の必要性を高めると予想されます。

- 同国では通常、夏・春(4月~9月)と冬の2つの季節に畑作物を栽培しています。春作には主に、早生トウモロコシ、早生米、早生小麦、綿花が含まれます。冬作物には冬小麦と菜種があります。しかし、米とトウモロコシは中国で栽培されている最も重要な作物であり、中国の穀物生産の3分の1を占めています。世界最大のコメ生産国であり、2022年には3,000万ヘクタールの土地を稲作に利用し、2億1,000万トンの収穫を見込んでいます。中国の主要米生産地域には、黒龍江省、湖南省、江西省、湖北省、江蘇省、四川省、広西チワン族自治区、広東省、クラウド南省が含まれます。2022~23年の中国のトウモロコシ生産量は2億7,720万トンに達すると予想され、豊作により昨年より460万トン増加しました。主要トウモロコシ生産地は東北部の黒龍江省、吉林省、内モンゴル自治区です。

- 国内では春が主要作期だが、6月と7月の高温の影響を若干受けています。例えば、米は中国の数百万人の主食です。高温と降水量の少なさは土壌中のミネラルの損失を増大させ、土壌への肥料の施用量を増やす必要性につながります。このような乾燥した気象条件は、作物の収量を制限することもあります。

世界の農地から排出される亜酸化窒素の約28%は、中国の農地から排出されています。

- 一次栄養素は、植物の酵素活性などの生化学的プロセスを強化し、植物細胞の成長を促進します。一次栄養素の欠乏は、植物の健康、発育、作物生産量に影響を与えます。畑作物における窒素、カリウム、リンを合わせた平均施用量は、2022年には159.9kg/ヘクタールでした。畑作物における一次養分の平均施用量は、窒素65.23%、リン28.07%、カリウム6.68%でした。

- 窒素は植物の代謝に不可欠で、葉緑素やアミノ酸の構成成分であるため、一次養分の中で第1位です。窒素の平均施用量は279.65kg/ヘクタールでした。次いでカリが105.3kg/ヘクタール、リンが94.9kg/ヘクタールであった(2022年)。窒素とリンによる地表水と地下水の汚染は、施肥量に関する農業従事者への不適切なアドバイスの結果と考えられています。世界の農地からの亜酸化窒素排出量の約28%は、中国の農地から排出されています。

- 2022年に平均養分施用率が最も高かった作物は、綿(255.41kg/ヘクタール)、小麦(232.25kg/ヘクタール)、トウモロコシ(198.44kg/ヘクタール)、コメ(157.76kg/ヘクタール)でした。2022年の綿花生産量は640万トンで、中国は世界最大の綿花生産国、消費国、輸入国となっています。世界で消費される綿花の約20%が中国で生産され、その84%が新疆ウイグル自治区で生産されています。

- 人口増加の需要を満たすためには、農作物生産の拡大が不可欠であり、その結果、畑作物への一次栄養素の施用は2023~2030年にかけて増加すると予想されています。

中国の放出制御肥料産業概要

中国の放出制御肥料市場はセグメント化されており、上位5社で19.69%を占めています。この市場の主要企業は、Grupa Azoty S.A.(Compo Expert)、Haifa Group、Hebei Sanyuanjiuqi Fertilizer、Hebei Woze Wufeng Biological Technology、Zhongchuang xingyuan chemical technologyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 主要養分

- 畑作物

- 園芸作物

- 主要養分

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- コーティングタイプ

- ポリマーコーティング

- ポリマー・硫黄コーティング

- その他

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Grupa Azoty S.A.(Compo Expert)

- Haifa Group

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- Hebei Woze Wufeng Biological Technology Co., Ltd

- Zhongchuang xingyuan chemical technology co.ltd

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The China Controlled Release Fertilizer Market size is estimated at 89.86 million USD in 2025, and is expected to reach 126.9 million USD by 2030, growing at a CAGR of 7.15% during the forecast period (2025-2030).

Polymer-coated urea is the most adopted CRF in the country due to its higher content

- In 2022, controlled-release fertilizers (CRFs) represented a mere 0.6% of China's specialty fertilizer market. However, the market value of CRFs exhibited a consistent upward trajectory in the past and is projected to maintain a robust CAGR of 6.9% from 2023 to 2030.

- Among CRFs, polymer-coated urea stands out as the dominant variant in China. This is primarily due to its high nitrogen (N) content, thin coating, easy degradability, and extended release period. It finds extensive use as a basal fertilizer for staple crops like rice, corn, and wheat. Polymer-coated fertilizers, including urea, commanded a significant 75.9% share of the CRF segment in 2022. Notably, the specific technologies employed in polymer coatings vary across manufacturers, influenced by the choice of coating material and process.

- Polymer-sulfur-coated fertilizers, enriched with sulfur, are preferred for their positive impact on crop quality and resilience. The synergistic effect of sulfur and nitrogen enhances crop nitrate levels and overall quality. Nitrogenous fertilizers, a subset of polymer-sulfur-coated fertilizers, held a dominant 59.7% share in this segment in 2022.

- Besides chemical coatings, there is a rising trend of biobased coatings on fertilizers, including biobased polyurethane, epoxy resin, and polyolefin wax composites. These coatings, driven by heightened demand from governments, particularly stand out in the "others" category. In 2022, the "others" segment accounted for 5.4% of China's controlled-release fertilizer market.

- Given these distinct advantages and evolving trends, the demand for coated controlled-release fertilizers is poised for significant growth in the coming years.

China Controlled Release Fertilizer Market Trends

The expansion of the cultivation area is driven by increasing demand for food and the country's goal to achieve self-sufficiency in staple food

- The cultivation area of field crops in China increased from 130.5 million ha in 2017 to 127.8 million ha in 2021, accounting for 71.4% of the total area under cultivation. Among field crops, corn occupied the maximum share of 34.2%, followed by rice and wheat, accounting for 23.6% and 18.3%, respectively. The rising area under cultivation is expected to increase the need for fertilizer usage in the country.

- The country usually grows field crops in two seasons: summer/spring (April-September) and winter. Spring crops mainly include early corn, early rice, early wheat, and cotton. Winter crops include winter wheat and rapeseed. However, rice and corn are the most important crops grown in China, accounting for one-third of the grain production in China. It is the world's largest rice producer and utilized 30 million hectares of land for rice farming in 2022, producing a harvest of 210 million tonnes. The major rice-producing regions in China include Heilongjiang, Hunan, Jiangxi, Hubei, Jiangsu, Sichuan, Guangxi, Guangdong, and Yunnan. Corn production in China for 2022-23 was expected to reach 277.2 million tonnes, which was 4.6 million tonnes higher than last year due to a better harvest. The major corn-growing regions are in the Northeast provinces of Heilongjiang, Jilin, and Inner Mongolia.

- Although spring is the main cropping season in the country, it is slightly affected by high heat in June and July. For instance, rice is the staple food for millions in China. High temperatures and low precipitation increase the loss of minerals in the soil, leading to the need for a higher application of fertilizers to the soil. These dry weather conditions may also limit the yield of the crops.

About 28% of nitrous oxide emissions from cropland in the world are from Chinese agricultural lands

- Primary nutrients enhance biochemical processes such as enzyme activity in plants and promote plant cell growth. Deficiencies in primary nutrients can affect plant health, development, and crop production output. The average application rate of nitrogen, potassium, and phosphorus combined in field crops was 159.9 kg/hectare in 2022. The average primary nutrient application in field crops accounted for 65.23% nitrogen, 28.07% phosphorous, and 6.68% potassium.

- Nitrogen ranks first among primary nutrients, as it is essential for plant metabolism and is a component of chlorophyll and amino acids. Nitrogen had an average application rate of 279.65 kg/hectare. Potash followed with 105.3 kg/hectare and phosphorous with 94.9 kg/hectare in 2022. The contamination of surface and groundwater with nitrogen and phosphorus has been considered a result of inadequate advice given to farmers regarding fertilizer application rates. About 28% of nitrous oxide emissions from cropland in the world are from China's agricultural lands.

- In 2022, crops with the highest average nutrient application rates were cotton (255.41 kg/hectare), wheat (232.25 kg/hectare), corn (198.44 kg/hectare), and rice (157.76 kg/hectare). In 2022, cotton production accounted for 6.4 million metric tons, making China the world's largest producer, consumer, and importer of cotton. Around 20% of the cotton consumed worldwide is produced in China, and 84% of that production comes from Xinjiang.

- To meet the demands of a growing population, boosting crop production is essential; as a result, the application of primary nutrients in field crops is expected to grow between 2023 and 2030.

China Controlled Release Fertilizer Industry Overview

The China Controlled Release Fertilizer Market is fragmented, with the top five companies occupying 19.69%. The major players in this market are Grupa Azoty S.A. (Compo Expert), Haifa Group, Hebei Sanyuanjiuqi Fertilizer Co., Ltd., Hebei Woze Wufeng Biological Technology Co., Ltd and Zhongchuang xingyuan chemical technology co.ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Grupa Azoty S.A. (Compo Expert)

- 6.4.2 Haifa Group

- 6.4.3 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.4 Hebei Woze Wufeng Biological Technology Co., Ltd

- 6.4.5 Zhongchuang xingyuan chemical technology co.ltd

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 131 Pages

- 納期

- 2~3営業日