自動車部品ダイカスト:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Automotive Parts Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687183

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

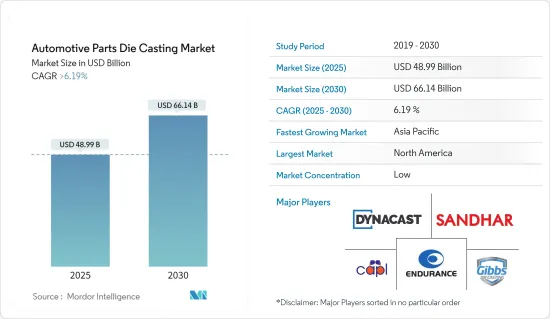

自動車部品ダイカストの市場規模は2025年に489億9,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは6.19%を超え、2030年には661億4,000万米ドルに達すると予測されます。

自動車部品ダイカスト市場は、主に自動車の軽量化への世界のシフトと電気自動車の人気の高まりによって大きな成長を遂げています。自動車の軽量化の動向は、世界の環境規制や持続可能性の目標に合わせて、燃費を改善し、二酸化炭素排出量を削減する必要性から生じています。特に電気自動車には、軽量かつ頑丈な複雑で高精度な部品が必要であり、ダイカストはこうした要求を満たす理想的なプロセスです。

例えば、自動車の排出ガスを削減し、燃費を向上させるためのCAFE基準やEPA政策は、自動車メーカーを軽量非鉄金属の使用による自動車の軽量化に駆り立てています。EPAが2025年までにマイル/ガロン(mpg)基準を54.5mpgに引き上げようとする動きは、ダイカスト業界を支援しています。その結果、軽量化戦略としてダイカスト部品を使用することが市場の主要な促進要因となっています。

さらに、ダイカスト技術の進歩が市場の拡大に大きく寄与しています。機械設計、プロセス制御、金型技術の革新は、ダイカスト作業の効率と品質を向上させる。これらの技術改良は、鋳造部品の精度と強度を向上させ、廃棄物とエネルギー消費を削減し、プロセスをより環境に優しく、費用対効果の高いものにしています。コンピュータ支援エンジニアリング(CAE)やモノのインターネット(IoT)などの自動化とデジタル技術の統合は、ダイカストプロセスを最適化し、リードタイムの短縮と生産性の向上につながります。

さらに、ダイカストの汎用性により、複雑なエンジン部品、トランスミッション・システム、構造要素など、幅広い自動車部品の生産が可能になります。高圧ダイカスト(HPDC)は、高速生産能力と高い寸法精度で複雑な形状を製造する能力を提供し、著名な技術として台頭してきました。さらに、真空ダイカストは、優れた機械的特性と最小限の気孔率で部品を製造する能力により、自動車部品の品質と耐久性をさらに高めることができるため、人気を集めています。

自動車メーカーが厳しい排ガス規制を満たし、EVのバッテリー航続距離を向上させるため、車両の軽量化にますます力を入れるようになるにつれ、革新的なダイカスト・ソリューションの需要が急増すると予想されます。このため、自動車業界の進化する要件に対応するため、新しい合金の開発や鋳造技術の強化など、材料やプロセスのさらなる進歩が見込まれています。

自動車部品ダイカスト市場動向

圧力ダイカストが最大の市場シェアを占める一方、真空ダイカストは高成長が期待される

圧力ダイカストは、生産タイプに基づく最大のカテゴリーです。圧力ダイカストは、効率的で大量生産が可能で、複雑かつ耐久性のある部品を製造できることから、自動車部品ダイカスト市場を独占しています。

加圧ダイカストは、主に、完璧な表面仕上げを持つ大量かつ複雑な部品を製造することに長けているため、自動車部品ダイカスト市場において極めて重要な位置を占めています。さらに、高圧ダイカスト(HPDC)は大型自動車部品の生産にますます使用されるようになっています。

テスラのような大手自動車会社は、自動車のフロントエンドやリアエンドのような重要な部品を単一部品として製造するためにHPDCを活用しています。HPDCのこの応用により、自動車製造工程の効率性と持続可能性が大きく進歩しました。例えば、HPDCは70から100の部品を単一の部品で置き換えることを可能にし、生産の複雑さを劇的に減らし、全体的な効率を向上させる。

圧力ダイカストのシェアが最も大きい一方で、真空ダイカストは、製造された部品の品質と強度を向上させる能力によって、自動車部品ダイカスト市場で最も急成長しているセグメントとして浮上すると予想されます。この成長軌道は、鋳造プロセス中の空気の巻き込みを緩和し、それによって構造的完全性を高めた部品の製造を保証するという、この技術の本質的な優位性に支えられています。

さらに、真空ダイカストは気孔率を大幅に減少させ、より高密度で堅牢な自動車部品を作り出します。この特性は、優れた品質と強度が譲れない重要な自動車部品の製造にますます求められています。さらに、この方法は高品質で耐久性のある部品の製造に長けているため、特に高い信頼性と性能基準を必要とする部品の製造において、進化する自動車製造セクターに不可欠な技術として位置づけられています。

アジア太平洋地域が市場で重要な役割を果たすと予想される

アジア太平洋地域は、インド、中国、日本といった主要国の存在により、市場で支配的な役割を果たすと予想されます。中国はダイカスト部品の主要生産国のひとつであり、アジア太平洋地域のダイカスト市場シェアの60%以上を占めています。

アジア太平洋地域が自動車部品ダイカスト市場をリードしているのは、中国とインドが大きく貢献しているためです。これは、成長する自動車産業、高い自動車生産台数、同地域を拠点とする大手自動車メーカーによるものです。

2022年、アジア太平洋地域では3,500万台以上の自動車が生産され、中国だけで2,700万台の自動車が生産されました。中国に続いて、日本が780万台以上、インドが540万台以上の自動車を生産しました。さらに、2022年の同地域の商用車販売台数は全体で660万台超となり、中国だけで330万台超が販売されました。

さらに、アジア太平洋地域は、自動車産業の成長に好意的な政府の政策によって強化された、定着した製造インフラから強みを得ており、それによって世界の文脈における主導的地位を確固たるものにしています。新しい製造技術や低燃費車への注力といった要因が市場を形成しています。

また、中間層の富裕化が市場成長にプラスの影響を与えています。同地域では、クリーンエネルギー車や環境問題に対する政府の政策を背景に、電気自動車やハイブリッド車のような先進的な自動車技術が市場を牽引しています。急成長と技術進歩によって特徴づけられるアジア太平洋地域のこのような進化する市場環境は、世界の自動車部品ダイカスト業界をさらに牽引すると予想されます。

自動車部品ダイカスト業界の概要

ダイカストの世界市場は断片化されており、新興国市場からも多くの地域中小規模のプレーヤーが参入しています。Nemak、Georg Fischer Automotive、Ryobi Die casting、Rheinmetall AG、Form Technologies Inc.(Dynacast)、Shiloh Industriesといった認知度の高い主要企業が世界市場シェアの16%以上を占めています。これらの主なプレーヤーは、より優れた自動車部品用の生産プロセスと合金を開発するため、研究開発に収益を集中しています。例えば

- は2023年10月、ケンタッキー州ラッセルビルにあるRane Precision Die Casting施設を買収しました。この工場は、自動車やその他の産業向けのアルミ鋳造を専門としています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 高性能車への需要増加が市場を牽引

- 市場抑制要因

- 原材料のサプライチェーン寸断が課題

- 原材料購入に関する初期コストの高さが課題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ

- 圧力ダイカスト

- 真空ダイカスト

- スクイズダイカスト

- セミソリッドダイカスト

- 原材料

- アルミニウム

- 亜鉛

- マグネシウム

- その他の原材料タイプ

- 用途

- ボディアセンブリ

- エンジン部品

- トランスミッション部品

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Castwel Auto Parts Pvt Ltd

- Die-casting Solutions GmbH

- Dynacast International Inc.

- Endurance Group

- Gibbs Die-casting Group

- Kinetic Die-casting Company

- Mino Industry USA Inc.

- Ningbo Parison Die-casting Co. Ltd

- Raltor Metal Technik India Pvt. Ltd

- Rockman Industries Ltd

- Ryobi Die-casting Inc.

- Sandhar Technologies Limited

- Sipra Engineers Pvt. Ltd

- Spark Minda, Ashok Minda Group

- Sunbeam Auto Pvt Ltd

- Texas Die-casting

- Tyche Diecast Private Limited

第7章 市場機会と今後の動向

- 軽量かつ持続可能な素材への志向の高まりが主要動向となります。

目次

The Automotive Parts Die Casting Market size is estimated at USD 48.99 billion in 2025, and is expected to reach USD 66.14 billion by 2030, at a CAGR of greater than 6.19% during the forecast period (2025-2030).

The automotive parts die casting market is experiencing significant growth, primarily driven by the global shift toward lightweight vehicles and the increasing popularity of electric vehicles. This trend toward lighter vehicles arises from the need to improve fuel efficiency and reduce carbon emissions, aligning with global environmental regulations and sustainability goals. Electric vehicles, in particular, require complex, high-precision components that are both lightweight and sturdy, and die casting is an ideal process to meet these demands.

For instance, CAFE standards and EPA policies to reduce automobile emissions and increase fuel efficiency are driving automobile manufacturers to reduce the weight of the automobile by using lightweight, non-ferrous metals. The move by the EPA to raise the miles per gallon (mpg) standards to 54.5 mpg by 2025 has helped the die casting industry, as the only way to get to those mileage standards is by manufacturing lightweight vehicles. Subsequently, using die cast parts as a weight-reduction strategy is a major driver for the market.

Further, advancements in die casting technology are significantly contributing to the expansion of the market. Innovations in machine design, process control, and mold technologies improve the efficiency and quality of die casting operations. These technological improvements increase the precision and strength of the cast parts and reduce waste and energy consumption, making the process more environmentally friendly and cost-effective. Integrating automation and digital technologies, such as computer-aided engineering (CAE) and the Internet of Things (IoT), optimizes the die casting process, leading to reduced lead times and increased productivity.

Moreover, the versatility of die casting allows for the production of a wide range of automotive parts, including intricate engine components, transmission systems, and structural elements. High-pressure die casting (HPDC) has emerged as a prominent technology, offering high-speed production capabilities and the ability to produce complex shapes with high dimensional accuracy. Moreover, vacuum die casting is gaining traction due to its ability to produce parts with superior mechanical properties and minimal porosity, further enhancing the quality and durability of automotive components.

As vehicle manufacturers increasingly focus on reducing vehicle weight to meet stringent emission standards and improve battery range in EVs, the demand for innovative die casting solutions is expected to surge. This is likely to lead to further advancements in materials and processes, such as the development of new alloys and enhanced casting techniques, to meet the evolving requirements of the automotive industry.

Automotive Parts Die Casting Market Trends

Pressure Die Casting Holds the Largest Market Share While Vacuum Die Casting is Expected to Witness a High Growth Rate

Pressure die casting is the largest category based on production type. Pressure die casting dominates the automotive parts die casting market with its efficient, high-volume, intricate, and durable components production.

Pressure die casting has been pivotal in the automotive parts die casting market, primarily due to its proficiency in fabricating high-volume, complex parts with perfect surface finish. Additionally, high-pressure die casting (HPDC) is increasingly used to produce large auto parts.

Major automotive companies like Tesla are utilizing HPDC to manufacture significant components, such as the front and rear ends of vehicles, as single parts. This application of HPDC has led to significant advancements in the efficiency and sustainability of automotive manufacturing processes. For instance, HPDC allows for replacing 70 to 100 parts with a single part, drastically reducing production complexity and improving overall efficiency.

While pressure die casting has the largest share, vacuum die casting is expected to emerge as the fastest-growing segment in the automotive parts die casting market, driven by its ability to enhance the quality and strength of manufactured components. This growth trajectory is underpinned by the technology's intrinsic advantage in mitigating air entrapment during the casting process, thereby ensuring the production of components with enhanced structural integrity.

Further, vacuum die-casting significantly reduces porosity, creating denser and more robust automotive parts. This attribute is increasingly sought in producing critical automotive components, where superior quality and strength are non-negotiable. Moreover, the method's proficiency in manufacturing high-quality, durable parts positions it as an indispensable technology in the evolving automotive manufacturing sector, particularly for components that require higher reliability and performance standards.

The Asia-Pacific Region is Expected to Play Key Role in the Market

The Asia-Pacific region is expected to play a dominant role in the market owing to the presence of key countries like India, China, and Japan. China is one of the major producers of die casting parts, accounting for more than 60% of the regional (Asia-Pacific) die casting market share.

The Asia-Pacific region leads in the automotive parts die casting market because of significant contributions from China and India. This is due to their growing car industry, high vehicle production, and major car manufacturers based there.

In 2022, over 35 million vehicles were produced in Asia-Pacific, with China accounting for 27 million motor vehicles alone. China was followed by Japan and India, which produced over 7.8 million and 5.4 million motor vehicles, respectively. Additionally, the overall commercial vehicle sales in the region in 2022 were registered at over 6.6 million units; over 3.3 million units were sold in China alone.

Moreover, the Asia-Pacific region derives strength from a well-entrenched manufacturing infrastructure, augmented by government policies favorably inclined toward the automotive industry's growth, thereby cementing its leadership position in the global context. Factors such as new manufacturing technologies and a focus on fuel-efficient cars shape the market.

The increasing wealth of the middle class also positively impacts the market growth. The region's push for advanced car technologies like electric and hybrid vehicles, backed by government policies for clean energy vehicles and environmental concerns, drives the market. This evolving market environment in Asia-Pacific, marked by rapid growth and technological advancements, is expected to drive the global automotive parts further die casting industry.

Automotive Parts Die Casting Industry Overview

The global market for die casting is fragmented, with many regional small-medium scale players from developing countries entering the market. Major recognized players, such as Nemak, Georg Fischer Automotive, Ryobi Die casting, Rheinmetall AG, Form Technologies Inc. (Dynacast), and Shiloh Industries, accounted for over 16% of the global market share. These key players have focused their revenues on R&D to develop better production processes and alloys for automotive parts. For instance,

- In October 2023, Kentucky Industrial Holdings Inc. purchased the Rane Precision Die Casting facility in Russellville, Kentucky. The plant specializes in aluminum castings for the automotive and other industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Demand for High-Performance Vehicles Will Drive the Market

- 4.2 Market Restraints

- 4.2.1 Supply Chain Disruption of Raw Materials Could be a Challenge

- 4.2.2 High Initial Cost Related to the Purchase of Raw Materials is a Challenge

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD Billion)

- 5.1 Production Process Type

- 5.1.1 Pressure Die Casting

- 5.1.2 Vacuum Die Casting

- 5.1.3 Squeeze Die Casting

- 5.1.4 Semi-solid Die Casting

- 5.2 Raw Material

- 5.2.1 Aluminum

- 5.2.2 Zinc

- 5.2.3 Magnesium

- 5.2.4 Other Raw Material Types

- 5.3 Application Type

- 5.3.1 Body Assemblies

- 5.3.2 Engine Parts

- 5.3.3 Transmission Parts

- 5.3.4 Other Application Types

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Mexico

- 5.4.4.2 Brazil

- 5.4.4.3 Argentina

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Castwel Auto Parts Pvt Ltd

- 6.2.2 Die-casting Solutions GmbH

- 6.2.3 Dynacast International Inc.

- 6.2.4 Endurance Group

- 6.2.5 Gibbs Die-casting Group

- 6.2.6 Kinetic Die-casting Company

- 6.2.7 Mino Industry USA Inc.

- 6.2.8 Ningbo Parison Die-casting Co. Ltd

- 6.2.9 Raltor Metal Technik India Pvt. Ltd

- 6.2.10 Rockman Industries Ltd

- 6.2.11 Ryobi Die-casting Inc.

- 6.2.12 Sandhar Technologies Limited

- 6.2.13 Sipra Engineers Pvt. Ltd

- 6.2.14 Spark Minda, Ashok Minda Group

- 6.2.15 Sunbeam Auto Pvt Ltd

- 6.2.16 Texas Die-casting

- 6.2.17 Tyche Diecast Private Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Inclination Towards the Use of Lightweight and Sustainable Materials Will be Key Trend

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日