米国のデータセンター向けストレージ:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

United States Data Center Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549841

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

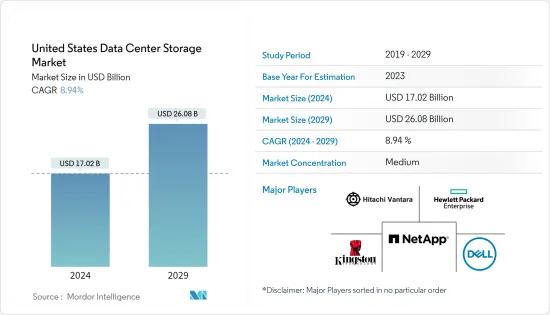

米国のデータセンター向けストレージ市場規模は2024年に170億2,000万米ドルと推定され、2029年には260億8,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは8.94%で成長する見込みです。

中小企業におけるクラウドコンピューティング需要の増加、データセキュリティに関する政府規制、国内企業による投資の拡大などが、同国のデータセンター需要を促進する主な要因となっています。

主なハイライト

- 建設中のIT負荷容量:米国データセンター・ラック市場の今後のIT負荷容量は、2029年までに2万4,000MWに達する見込み。

- 建設中の高床スペース:米国では2029年までに、高床面積の建設が8,000万平方フィートに増加すると予想されます。

- 計画中のラック:2029年までに設置されるラックの総数は403万5,000ユニットに達すると予想されます。バージニア州北部には2029年までに最大数のラックが設置される見込み。

- 計画されている海底ケーブル米国を結ぶ海底ケーブルシステムは90以上あり、その多くが建設中です。2025年に開通が予定されている海底ケーブルのひとつがGold Data-1で、米国のナポリから2,333kmにわたって伸びています。

- データ・ストレージへのニーズの高まりにより、全国的にデータ・センターの数が急増しています。米国内のデータセンター需要とその成長にはいくつかの要因が寄与しており、それは同国の進化するIT状況、ビジネス活動、技術的取り組みに反映されています。米国におけるデータセンターの発展を後押しする主な要因としては、デジタルトランスフォーメーション、クラウドコンピューティングの採用、eコマースとデジタルサービス、再生可能エネルギーと持続可能性、スマートシティとIoT構想などが挙げられます。したがって、このような要因が予測期間中の市場成長を促進すると予想されます。

米国のデータセンター向けストレージ市場動向

IT・通信セグメントが主要シェアを占める

- COVID-19の大流行は、デジタル変革に取り組む競合他社よりもデジタル製品やサービスの提供、デジタルプロセスの利用を開始したため、デジタル変革への早期参入者の経済効果に影響を与えました。

- 米国企業のインフラ担当意思決定者のうち、94%が少なくとも1つのクラウドを導入しており、ハイブリッドまたはマルチクラウドのソリューションがより一般的となっています。米国のインフラ意思決定者の74%近くが、オンプレミスまたはパブリッククラウド環境で、コンテナをPlatform as a Service(PaaS)として採用していると回答しています。クラウドは大幅に増加すると予想されます。

- 米国のクラウドプロバイダーには、AWS、Microsoft、Googleが含まれます。少なくとも1種類のクラウド導入を利用している企業インフラの意思決定者のうち、94%が少なくとも1種類のクラウド導入を利用しており、その大半はハイブリッドクラウドまたはマルチクラウドです。

- 米国では、あらゆるビジネスで費用対効果の高いデータのバックアップ、保管、バックアップの需要が高まっていること、また携帯電話の利用が増加していることから発生するデータを管理する必要性が高まっていることから、クラウド・ストレージの利用が拡大しています。

- 米国ではデジタル経済の台頭とインターネット利用の増加に伴い、データの保存と処理のニーズが高まっています。ハイブリッド・クラウド・サービス・プロバイダーの普及により、コロケーション・サービスの需要が高まり、ラックの利用率が上昇。

- 通信プロバイダーのネットワーク接続を利用するIoTデバイスの数は、膨大な量のデータを生成する可能性が高いです。例えば、米国におけるコネクテッド・コンシューマー・デバイスの出荷台数は、2023年までに8億台以上に達すると予測されています。2025年までに、米国のIoT接続は40億以上に成長すると予測されています。米国では、5Gサービスにより、2029年には月平均モバイルデータ通信速度が534Mbpsに達すると予測されています。このような市場では、データセンターへのニーズが高まり、データセンター向けストレージ・ソリューションの需要が今後数年間で高まると予想されます。

ハイブリッドストレージが大きな市場シェアを占める見込み

- オンプレミスとクラウドのストレージ・ソリューションの組み合わせは、データセンターにおけるハイブリッド・ストレージと呼ばれます。このアプローチは、両方の環境の長所を活用し、オンサイトとクラウドにデータを保存・管理する柔軟性を提供します。

- 米国は技術革新の中心地であり、AI、機械学習、アナリティクスなどの先進技術が広く採用されています。ハイブリッド・ストレージ・インフラは、これらのテクノロジーをスムーズに統合し、サポートするために必要です。

- 競合環境では、適応力と革新力が不可欠です。堅牢でコスト効率に優れ、技術的にも先進的なストレージ・ソリューションを提供することで、ハイブリッド・ストレージ型DC施設は米国の企業の競争力を向上させる。

- さらに、5Gの登場とスマートフォンの普及に伴い、十分な速度利用可能性を確保する必要があります。その結果、国内ではクラウド・コンピューティングの導入、インターネット・ユーザーの増加、光ファイバー技術の採用などが進んでいます。こうした技術のイントロダクションとデータ利用の増加に伴い、国内ではハイブリッド・ストレージ・データセンターの利用が増加しています。

- 2023年には、米国人口の約92%がインターネット・ユーザーとなり、2012年の約75%から増加します。米国は世界最大級のオンライン市場であり、2022年のインターネットユーザー数は約2億9,900万人に上ります。このような市場の改善がデータセンターの成長を促進し、セグメントの成長に寄与しています。

- 同市場の主要企業は、市場の需要に応えるため、データセンター向けストレージ・ソリューションの改善に注力しています。2023年7月、日立製作所の著名なインフラストラクチャー、データ管理、デジタルソリューションの子会社であるHitachi Vantaraは、マイクロソフトとの協業により、Hitachi Unified Compute Platform(UCP)for Azure Stack HCIを発表しました。この合理的で強力なハイブリッドクラウドソリューションは、ビジネスの柔軟性を高め、データセンター、支店、エッジコンピューティングなど、さまざまな環境にわたって強化されたクラウド管理を実現し、企業がデータの保存、管理、使用方法についてより高い可視性と制御性を提供します。

米国のデータセンター向けストレージ業界の概要

米国では今後DC建設プロジェクトが予定されており、米国のデータセンター向けストレージ市場の需要は今後数年間で増加すると予想されます。米国のデータセンター向けストレージ市場は、Dell Inc.、Hewlett Packard Enterprise、NetApp Inc.、Hitachi Vantara LLC、Kingston Technology Company Inc.などの大手企業によって適度に統合されています。これらの主要企業は市場シェアが高く、各地域の顧客基盤の拡大に注力しています。

- 2023年4月ヒューレット・パッカード・エンタープライズ(HPE)は、データサイロの解消、コストと複雑性の軽減、パフォーマンスの向上を目的とした新しいファイル、災害、ブロック、バックアップリカバリデータサービスを発表しました。新しいファイル・ストレージ・データ・サービスは、データ・ワークロードにスケールアウト可能なエンタープライズ向けのパフォーマンスを提供し、拡張されたブロック・サービスはミッションクリティカルなミッドレンジ・ストレージの経済性を実現します。

- 2023年2月クラウドをリードするデータ中心の重要なソフトウェア企業であるネットアップは、低コストなオールフラッシュストレージを実現する大容量フラッシュストレージの新しい製品ラインであるNetApp AFF Cシリーズと、オールフラッシュシステムのAFF Aシリーズの新しいエントリレベルストレージシステムであるNetApp AFF A150のラインアップの拡充を発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- クラウドコンピューティング機能に対する需要の高まりが市場成長を促進

- データセンターにおけるグリーン・プラクティスの採用が市場成長を促進

- 市場抑制要因

- 高い保守・交換コスト

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- ストレージ技術別

- ネットワーク接続ストレージ(NAS)

- ストレージ・エリア・ネットワーク(SAN)

- ダイレクト・アタッチド・ストレージ(DAS)

- その他の技術

- ストレージタイプ別

- 従来型ストレージ

- オールフラッシュ・ストレージ

- ハイブリッド・ストレージ

- エンドユーザー別

- IT・通信

- BFSI

- 政府機関

- メディア・エンターテイメント

- その他のエンドユーザー

第6章 競合情勢

- 企業プロファイル

- Dell Inc.

- Hewlett Packard Enterprise

- NetApp Inc.

- Hitachi Vantara LLC

- Kingston Technology Company Inc.

- Pure Storage Inc.

- Infinidat Ltd

- Lenovo Group Limited

- Fujitsu Limited

- Nutanix Inc.

- KIOXIA Singapore Pte. Ltd

- Commvault Systems Inc.

第7章 投資分析

第8章 市場機会と今後の動向

目次

The United States Data Center Storage Market size is estimated at USD 17.02 billion in 2024, and is expected to reach USD 26.08 billion by 2029, growing at a CAGR of 8.94% during the forecast period (2024-2029).

The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country.

Key Highlights

- Under Construction IT Load Capacity: The upcoming IT load capacity of the US data center rack market is expected to reach 24,000 MW by 2029.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase to 80 million sq. ft by 2029.

- Planned Racks: The country's total number of racks to be installed is expected to reach 4,035,000 units by 2029. Northern Virginia is expected to house the maximum number of racks by 2029.

- Planned Submarine Cables: There are more than 90 submarine cable systems connecting the United States, and many are under construction. One such submarine cable that is estimated to start service in 2025 is Gold Data-1, which stretches over 2,333 km with landing points from Naples, United States.

- An increasing need for data storage has resulted in an upsurge in the number of data centers nationwide. Several factors contribute to the demand for data centers and their growth within the United States, which is reflected by the country's evolving IT landscape, business activities, and technological initiatives. Key drivers that propel the development of data centers in the nation include digital transformation, cloud computing adoption, e-commerce and digital services, renewable energy and sustainability, and smart cities and IoT initiatives. Hence, such factors are expected to drive market growth during the forecast period.

United States Data Center Storage Market Trends

IT and Telecommunication Segment Holds the Major Share

- The COVID-19 pandemic impacted the economic effects of early entrants on digital transformation as they began offering digital products and services and using digital processes more than their competitors engaged in digital transformation.

- Among US corporate infrastructure decision-makers, 94% have at least one cloud deployment, with hybrid or multi-cloud solutions more common. Nearly 74% of US infrastructure decision-makers say their organizations are adopting containers as a platform as a service (PaaS) in on-premises or public cloud environments. Clouds are expected to increase significantly.

- US cloud providers include AWS, Microsoft, and Google. Among enterprise infrastructure decision-makers who use at least one type of cloud deployment, 94% use at least one type of cloud deployment, with the majority being hybrid or multi-cloud.

- In the United States, cloud storage is growing due to the growing demand for cost-effective data backup, storage, and backup in every business and the need to manage the data generated by the increasing use of mobile phones.

- With the rise of the digital economy and increased internet usage in the United States, the need for data storage and processing has increased. The proliferation of hybrid cloud service providers has increased demand for colocation services and increased rack utilization.

- The number of IoT devices utilizing network connections from telecommunication providers is likely to generate huge amounts of data. For instance, connected consumer device unit shipments in the United States were projected to reach more than 800 million units by 2023. By 2025, IoT connections in the United States are projected to grow to more than 4 billion. In the United States, the average monthly mobile data speed is projected to reach 534 Mbps in 2029 through 5G service. Such instances in the market are expected to create more need for data centers, resulting in rising demand for data center storage solutions in the coming years.

Hybrid Storage is Expected to Hold a Significant Market Share

- The combination of on-premises and cloud storage solutions is called hybrid storage in data centers. This approach leverages the strengths of both environments, offering the flexibility to store and manage data on-site and in the cloud.

- The United States is a hub of technological innovation, and there is widespread adoption of advanced technologies, such as AI, machine learning, and analytics. Hybrid storage infrastructure is needed for these technologies to be integrated and supported smoothly.

- The ability to adapt and innovate is vital in a competitive business environment. By providing a robust, cost-efficient, and technically advanced storage solution, hybrid storage-type DC facilities improve the competitiveness of businesses in the United States.

- Furthermore, with the advent of 5G and the increasing use of smartphones, we need to ensure adequate speed availability. As a result, the country has adopted cloud computing, increased the number of Internet users, and adopted fiber optic technology. With the introduction of such technologies and the increase in data usage, the use of hybrid storage data centers is increasing in the country.

- In 2023, around 92% of the US population was an internet user, up from approximately 75% in 2012. The United States is one of the world's largest online markets, with approximately 299 million internet users in the country in 2022. Such market improvements propel data centers' growth and contribute to segmental growth.

- The key players in the market focus on improving the data center storage solutions to meet the market demand. In July 2023, Hitachi Vantara, a prominent infrastructure, data management, and digital solutions subsidiary of Hitachi Ltd, announced its collaboration with Microsoft to launch the Hitachi Unified Compute Platform (UCP) for Azure Stack HCI. The streamlined and powerful hybrid cloud solution increases business flexibility and delivers enhanced cloud management across various environments, including data centers, branch offices, and edge computing, to give businesses greater visibility and control over how their data is stored, managed, and used.

United States Data Center Storage Industry Overview

The upcoming DC construction projects in the country are expected to increase the demand in the US data center storage market in the coming years. The US data center storage market is moderately consolidated with some major players, including Dell Inc., Hewlett Packard Enterprise, NetApp Inc., Hitachi Vantara LLC, and Kingston Technology Company Inc. These major players, with a prominent market share, focus on expanding their regional customer base.

- April 2023: Hewlett Packard Enterprise (HPE) announced new file, disaster, block, and backup recovery data services designed to assist customers in eliminating data silos, reduce cost and complexity, and improve performance. The new file storage data services deliver scale-out, enterprise-intensive performance for data workloads, and the expanded block services provide mission-critical, midrange storage economics.

- February 2023: NetApp, a significant, cloud-led, data-centric software company, announced the expansion of NetApp AFF C-Series, a new product line of capacity flash storage that delivers lower-cost all-flash storage, and NetApp AFF A150, a new entry-level storage system in the AFF A-Series line of all-flash systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Cloud Computing Capabilities Drives Market Growth

- 4.2.2 Adoption of Green Practices in Data Centers Drives Market Growth

- 4.3 Market Restraints

- 4.3.1 High Maintenance and Replacement Cost

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Storage Technology

- 5.1.1 Network Attached Storage (NAS)

- 5.1.2 Storage Area Network (SAN)

- 5.1.3 Direct Attached Storage (DAS)

- 5.1.4 Other Technologies

- 5.2 By Storage Type

- 5.2.1 Traditional Storage

- 5.2.2 All-Flash Storage

- 5.2.3 Hybrid Storage

- 5.3 By End User

- 5.3.1 IT and Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Media and Entertainment

- 5.3.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dell Inc.

- 6.1.2 Hewlett Packard Enterprise

- 6.1.3 NetApp Inc.

- 6.1.4 Hitachi Vantara LLC

- 6.1.5 Kingston Technology Company Inc.

- 6.1.6 Pure Storage Inc.

- 6.1.7 Infinidat Ltd

- 6.1.8 Lenovo Group Limited

- 6.1.9 Fujitsu Limited

- 6.1.10 Nutanix Inc.

- 6.1.11 KIOXIA Singapore Pte. Ltd

- 6.1.12 Commvault Systems Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日