|

市場調査レポート

商品コード

1521445

日本のデータセンター用ストレージ:市場シェア分析、産業動向、成長予測(2024年~2029年)Japan Data Center Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のデータセンター用ストレージ:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

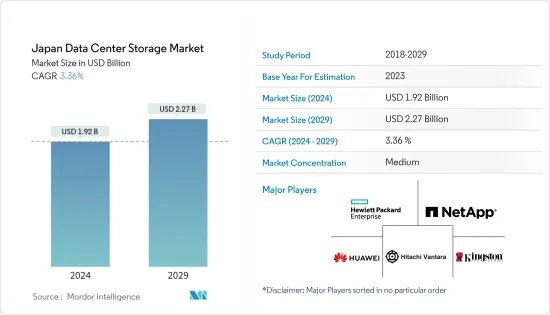

日本のデータセンター用ストレージ市場規模は、2024年に19億2,000万米ドルと推定され、2029年には22億7,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは3.36%で成長すると予測されます。

主なハイライト

- 中小企業におけるクラウドコンピューティング需要の増加、国内データセキュリティに関する政府規制、国内プレイヤーによる投資拡大などが、国内のデータセンター需要を促進する主な要因の1つであり、データセンター用ストレージ機器に対するニーズの高まりにつながっています。

- 建設中のIT負荷容量:日本のデータセンター市場のIT負荷容量は、2029年までに2,000MWに達すると予想されます。

- 建設中の高床スペース:日本の床面積は2029年までに1,000万平方フィートに増加すると予想されます。

- 計画中のラック:国内に設置されるラックの総数は、2029年までに50万ユニットに達すると予想されます。2029年には、東京に最大数のラックが設置されると予想されます。

- 計画中の海底ケーブル:フィリピンを結ぶ海底ケーブルは30近くあり、その多くが建設中です。2023年にサービス開始が予定されている海底ケーブルのひとつは、東南アジア-日本ケーブル2(SJC2)で、日本の千倉から志摩までの10,500キロメートルを陸揚げしています。

日本のデータセンター用ストレージ市場動向

IT・通信分野が市場の大半を占める

- 2020年、日本の子どもたちのインターネット利用状況に関する調査で、高校生が1日にインターネットを利用する時間は平均4時間8分で、前年から31分増加し、インターネットへの依存度が高まっていることが明らかになった。同調査によると、高校生の99.1%がインターネットを利用し、91.9%がスマートフォンからアクセスしています。この動向は、予測期間中に大幅なトラフィック占有に貢献すると予想されます。

- データセンターは国家安全保障、インターネット・インフラ、経済パフォーマンスにおいて重要な役割を担っており、日本ではデータセンター・インフラが急成長しています。この成長は、クラウドサービスへの嗜好の高まりや、拡大するデジタル・ユーザー・ベースによるデータの消費と生成の増加によって、データセンターとストレージ・デバイスの使用量が増加していることが後押ししています。

- 日本は、2028年までにほぼ全世帯を高速光ファイバー網に接続することを目標とする政府政策を実施しており、海底ケーブルとデータセンターの分散化に約500億円を割り当て、セキュリティと経済発展を強化しています。データセンターを通じたITインフラの高度化により、企業はより大容量のデータを管理・処理できるようになり、フラッシュストレージの追加を含むストレージインフラの拡張が必要となった。そのため、既存のデータセンターや新しいデータセンターの建設が推進されます。データセンター数の増加は、ITインフラにおけるストレージ・デバイスの需要に直結しています。

- データセンター・サービスの需要は、アプリケーション・パフォーマンスの向上、ストレージ要件の拡大、アプリケーションの普及とインターネット利用の増加によるモバイル・データ利用の増加といったニーズによってデータセンターのワークロードが増加することによって、さらに促進されます。世界中の企業がクラウドデータストレージにシフトする中、データセンターサービスへの需要は増加傾向にあります。

- 2021年以降、日本の移動体通信事業者が基地局配備と人口カバー率の野心的な目標を掲げて5G展開を加速させていることは、通信分野の優位性の高まりを反映しています。スマートフォンの普及と5Gネットワークの利用拡大はデータトラフィックの急増に寄与し、日本のデータセンターの成長にプラスの影響を与えます。その結果、データストレージとデータセンター用ストレージ機器の需要が増大し、市場全体の価値が高まっています。

ハイブリッド・ストレージが大きなシェアを占める見込み

- 日本政府のデジタル庁は、中央官庁と地方官庁の両方に対してクラウド・サービスの採用を積極的に推進しています。このイニシアチブの一例として、2022年10月に発表された「ガバメント・クラウド」サービスの年度内採用に関する発表があります。このアプローチは、データセンター・ハイブリッド・ストレージと呼ばれる、オンプレミスとクラウドのストレージ・ソリューションを組み合わせたもので、両環境の長所を活かし、データの保存と管理に柔軟性を提供します。

- ハイブリッド・ストレージにおけるオンプレミスとクラウドのストレージ・ソリューションの統合は、企業が特定の法的要件を満たすためにストレージ戦略を調整することをサポートし、データの整合性と法令遵守を保証します。このようなハイブリッドストレージソリューションの採用は、国内におけるデータストレージへのニーズの高まりに貢献しています。

- 経済産業省(METI)は、2017年度からの補助金を通じて、クラウドサービスを含むIT導入促進の一翼を担ってきました。さらに、厚生労働省は2021年に、COVID-19パンデミックの影響を受けた組織に対して「働き方改革推進助成金」を提供し、クラウドサービスやその他のIT機器の契約料や設備費用を負担することで、リモートワークへの移行を支援しました。ビジネスの拡大と進化に伴い、データセンターは様々な業界の接続ニーズを満たすために成長し、柔軟性、拡張性、リモートワークのためにハイブリッドインフラとクラウド機能への依存度が高まっています。データトラフィックの増加は、企業にとってのストレージの重要性を強化し、ハイブリッドストレージ・ソリューションの市場価値を高める要因となっています。

- ハイブリッド・クラウドにおけるデータの可用性とアクセスを確保するため、さまざまなサービス・プロバイダーが先進的なストレージ・ソリューションを導入しています。特に、HPE GreenLakeのような企業は、2022年にプラットフォームのアップグレードや新しいクラウドサービスなど、最適化されたハイブリッドストレージシステムを発表しています。大規模なデータストレージ容量を持つ大企業がこうした製品ポートフォリオを採用し、日本におけるハイブリッドストレージの需要をさらに促進しています。

- 日本のインターネットユーザー数は大幅に増加し、2021年から2022年にかけて84万4,000人(0.7%)増加しました。インターネットトラフィックの急増は、2019年のCOVID-19以前のレベルの1.6倍であり、パンデミックによる家庭でのテレビ会議、遠隔学習、ビデオストリーミングの増加に起因すると考えられます。クラウドストレージや音声会議サービスの人気の高まりにより、リモートワークを採用する企業が増え、ハイブリッドストレージを利用するデータセンターの出現に寄与しています。ハードドライブとSSDの機能を組み合わせたハイブリッドストレージ・ソリューションのイントロダクションは、SSDの高速アクセス機能とハードドライブの大容量ストレージを活用し、頻繁にアクセスされるデータのアクセス速度をキャッシュ利用で最適化するという革新的なアプローチを示しています。

日本のデータセンター用ストレージ産業の概要

日本のデータセンター用ストレージ市場は中程度の断片化を示しており、市場シェアの大半を主要企業が占めています。この市場で注目すべき企業には、Hewlett Packard Enterprise、NetApp Inc.、Huawei Technologies、Hitachi Vantara LLC、Kingston Technology Company Inc.などがあります。これらの企業は、市場シェアを高め、収益性を強化するために、戦略的に協力的な取り組みを行っています。

2023年8月、Kioxia Corporationはエンタープライズおよびデータセンターインフラ向けに設計された新しいPCIe 5.0 SSDを発表し、ストレージソリューションの進歩に貢献しました。

2023年8月、Kioxia Corporationは、データセンタークラスのソリッドステートドライブ(SSD)のラインアップにKIOXIA CD8Pシリーズを追加することを発表しました。KIOXIA CD8Pシリーズは、PCIe 5.0(32GT/s x4)性能を活用できる汎用サーバーおよびクラウド環境に適しています。これらのデータセンター・アプリケーションは、24時間365日稼働のデータセンターにおいて、大規模な仮想化システムに広がる複雑な混合ワークロードを生成することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3カ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ITインフラの拡大による市場成長の拡大

- ハイパースケールデータセンターへの投資増加による市場成長の拡大

- 市場抑制要因

- 初期投資コストの高さが市場成長の妨げに

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- ストレージ技術

- ネットワーク接続ストレージ(NAS)

- ストレージ・エリア・ネットワーク(SAN)

- ダイレクト・アタッチド・ストレージ(DAS)

- その他のテクノロジー

- ストレージタイプ

- 従来型ストレージ

- オールフラッシュ・ストレージ

- ハイブリッド・ストレージ

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他のエンドユーザー

第6章 競合情勢

- 企業プロファイル

- Hewlett Packard Enterprise

- NetApp Inc.

- Huawei Technologies Co. Ltd.

- Hitachi Vantara LLC

- Kingston Technology Company Inc.

- Pure Storage Inc.

- Lenovo Group Limited

- Fujitsu Limited

- Seagate Technology LLC

- Western Digital Corporation

第7章 投資分析

第8章 市場機会と今後の動向

The Japan Data Center Storage Market size is estimated at USD 1.92 billion in 2024, and is expected to reach USD 2.27 billion by 2029, growing at a CAGR of 3.36% during the forecast period (2024-2029).

Key Highlights

- The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country, leading to a growing need for data center storage equipment.

- Under Construction IT Load Capacity: The upcoming IT load capacity of the Japan data center market is expected to reach 2,000 MW by 2029.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase to 10 million sq. ft by 2029.

- Planned Racks: The country's total number of racks to be installed is expected to reach 500K units by 2029. Tokyo is expected to house the maximum number of racks by 2029.

- Planned Submarine Cables: There are close to 30 submarine cable systems connecting the Philippines, and many are under construction. One such submarine cable that is estimated to start service in 2023 is Southeast Asia-Japan Cable 2 (SJC2), which stretches over 10,500 Kilometers with landing points from Chikura, Japan, to Shima, Japan.

Japan Data Center Storage Market Trends

IT & Telecommunication Segment to Hold Major Share in the Market

- In 2020, a survey on internet usage among Japanese children revealed that high school students spent an average of 4 hours and 8 minutes online daily, marking a 31-minute increase from the previous year and underlining the escalating reliance on the internet. The survey found that 99.1% of high schoolers use the internet, with 91.9% accessing it through smartphones. This trend is anticipated to contribute to significant traffic occupancy in the forecast period.

- Data centers play a crucial role in national security, internet infrastructure, and economic performance, and Japan is witnessing rapid growth in its data center infrastructure. This growth is propelled by an increasing preference for cloud services and the rising consumption and generation of data by an expanding digital user base, leading to higher data center and storage device usage.

- Japan has implemented a government policy aiming to connect nearly all households to a high-speed fiber optic network by 2028, with an allocation of approximately JPY 50 billion for subsea cable and data center decentralization to enhance security and economic development. The advancement of IT infrastructure through data centers has enabled businesses to manage and process larger volumes of data, requiring the scaling of storage infrastructure, including the addition of flash storage. It drives to existing data centers or the construction of new ones. The growth in the number of data centers is directly linked to the demand for storage devices in IT infrastructure.

- The demand for data center services is further fueled by increasing data center workloads, driven by the need for improved application performance, expanding storage requirements, and rising mobile data usage due to the proliferation of applications and increased internet usage. As businesses worldwide shift to cloud data storage, the demand for data center services is on the rise.

- The acceleration of the 5G rollout by Japan's mobile operators since 2021, with ambitious targets for base station deployment and population coverage, reflects the growing dominance of the telecommunications sector. The widespread adoption of smartphones and the increasing use of 5G networks contribute to a surge in data traffic, positively impacting the growth of data centers in Japan. This, in turn, augments the demand for data storage and data center storage equipment, thereby increasing the overall market value.

Hybrid Storage Expected To Hold Significant Share

- The Government of Japan's Digital Agency actively promotes the adoption of cloud services for both central and local government offices. An example of this initiative is the announcement made in October 2022, wherein the agencies of the Government of Japan committed to adopting "Government Cloud" services for the fiscal year. This approach combines on-premises and cloud storage solutions, referred to as data center hybrid storage, leveraging the strengths of both environments and offering flexibility in storing and managing data.

- The integration of on-premises and cloud storage solutions in hybrid storage supports enterprises in tailoring their storage strategies to meet specific legal requirements, ensuring data integrity and legal compliance. This adoption of hybrid storage solutions contributes to the increasing need for data storage in the country.

- The Ministry of Economics, Trade, and Industry (METI) has played a role in promoting IT adoption, including cloud services, through subsidies provided since FY2017. Additionally, in 2021, the Ministry of Health, Labour, and Welfare (MHLW) offered a "Workstyle Reform Promotion" subsidy to organizations affected by the COVID-19 pandemic, supporting their transition to remote work by covering contracting fees and equipment costs for cloud services and other IT devices. As businesses expand and evolve, data centers are growing to meet the connectivity needs of various industries, with an increasing reliance on hybrid infrastructure and cloud capabilities for flexibility, scalability, and remote work. The rising data traffic reinforces the importance of storage for businesses, contributing to an increased market value for hybrid storage solutions.

- Various service providers are deploying advanced storage solutions to ensure data availability and access in hybrid clouds. Notably, companies like HPE GreenLake have introduced optimized hybrid storage systems, including platform upgrades and new cloud services in 2022. Large enterprises with substantial data storage capacities are adopting such product portfolios, further driving the demand for hybrid storage in the country.

- The number of internet users in Japan saw a significant increase, rising by 844 thousand (0.7%) between 2021 and 2022. The surge in internet traffic, 1.6 times higher than pre-COVID-19 levels in 2019, can be attributed to the pandemic-driven rise in at-home videoconferencing, distance learning, and video streaming. The growing popularity of cloud storage and audio conferencing services has led more companies to embrace remote work, contributing to the emergence of data centers utilizing hybrid storage. The introduction of hybrid storage solutions, combining the functionality of hard drives and SSDs, demonstrates an innovative approach where cache utilization optimizes access speed for frequently accessed data, capitalizing on the fast access capabilities of SSDs and the greater storage capacity of hard drives.

Japan Data Center Storage Industry Overview

The Japan Data Center Storage market exhibits a moderate level of fragmentation, with a majority of the market share held by key players. Noteworthy companies in this market include Hewlett Packard Enterprise, NetApp Inc., Huawei Technologies Co. Ltd., Hitachi Vantara LLC, and Kingston Technology Company Inc. These entities strategically engage in collaborative initiatives to enhance their market share and bolster profitability.

In August 2023, Kioxia Corporation introduced new PCIe 5.0 SSDs designed for Enterprise and Data Center Infrastructures, contributing to advancements in storage solutions.

In August 2023, Kioxia Corporation announced the addition of the KIOXIA CD8P Series to its lineup of data center-class solid state drives (SSDs). The KIOXIA CD8P Series is well-suited to general purpose server and cloud environments that can take advantage of PCIe 5.0 (32GT/s x4) performance. These data center applications can generate complex mixed workloads spread across large scale virtualized systems in 24x7 operational data centers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of IT Infrastructure to Increase Market Growth

- 4.2.2 Increased Investments in Hyperscale Data Centers To Increase Market Growth

- 4.3 Market Restraints

- 4.3.1 High Initial Investment Cost To Hinder Market Growth

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 Storage Technology

- 5.1.1 Network Attached Storage (NAS)

- 5.1.2 Storage Area Network (SAN)

- 5.1.3 Direct Attached Storage (DAS)

- 5.1.4 Other Technologies

- 5.2 Storage Type

- 5.2.1 Traditional Storage

- 5.2.2 All-Flash Storage

- 5.2.3 Hybrid Storage

- 5.3 End-User

- 5.3.1 IT & Telecommunication

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Media & Entertainment

- 5.3.5 Other End-Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Hewlett Packard Enterprise

- 6.1.2 NetApp Inc.

- 6.1.3 Huawei Technologies Co. Ltd.

- 6.1.4 Hitachi Vantara LLC

- 6.1.5 Kingston Technology Company Inc.

- 6.1.6 Pure Storage Inc.

- 6.1.7 Lenovo Group Limited

- 6.1.8 Fujitsu Limited

- 6.1.9 Seagate Technology LLC

- 6.1.10 Western Digital Corporation