|

市場調査レポート

商品コード

1440408

バーチャルケア:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Virtual Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| バーチャルケア:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

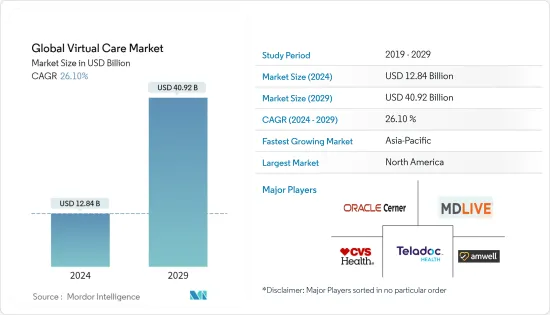

世界のバーチャルケア市場規模は、2024年に128億4,000万米ドルと推定され、2029年までに409億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に26.10%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)のパンデミックはバーチャルケア市場にプラスの影響を与えました。パンデミックにより、あらゆる年齢層の人々の間でバーチャルケア支援の導入が増加しました。当初、バーチャルケアの概念は若者などの特定の年齢層に限定されていました。しかし、新型コロナウイルス感染症(COVID-19)の出現により、年齢に関係なく、すべての患者の間で「バーチャルケア」という用語が非常に目立つようになりました。たとえば、2020年 6月にカナダ医師協会(CMA)が実施した調査によると、COVID-19危機の最中に、カナダ人の47%が電話、電子メール、メッセージ、ビデオなどの「バーチャルケア」を利用しました。 91%が訪問に非常に満足していると回答しました。同情報筋はさらに、パンデミック中にアドバイスを必要とした個人の34%が電話で医師に連絡したと述べた。しかし、直接医師の診察を受けたのはわずか10%、ウォークインクリニックに行ったのは6%、救急外来に行ったのは5%でした。さらに、Canada Health Infowayによると、パンデミックが宣言される前に、カナダのプライマリケア訪問の約4%がリモート(電話、ビデオ、テキスト、またはアプリ)で行われていました。したがって、このような事例は、パンデミック段階で仮想ケアソリューションに対する需要が高まったことを示しています。

さらに、バーチャルケアによって医師と患者の両方に提供される相互利点は、市場の成長を促進する主要な要因の1つです。バーチャルケアにより、患者は自宅から診察を受けることができます。また、医師は物理的な診察を介さずに、より多くの患者にバーチャルで対応できるため、患者と医師の間の溝を埋めることにも役立ちます。さらに、バーチャルケアは交通費や待ち時間がかからないため、物理的な診察よりもはるかに安価です。バーチャルケアの導入の増加により、多くの主要企業や小規模企業がバーチャルケアに関連するサービスを開始するようになっています。たとえば、LifeMDは2021年 11月に仮想ケアプラットフォームを立ち上げ、世界中の患者が手頃な価格で年中無休でヘルスケアを受けられるようにしました。同様に、2022年 4月、成長株式会社ゼネラルアトランティックが主導する3億米ドルのシリーズ D投資により、仮想ケアとデジタル医療のパイオニアであるBiofourmisはユニコーンの地位を獲得しました。 Biofourmisは、この資金調達によりバーチャルケアの提供を拡大する予定です。これには、増加する急性疾患患者に個別化された予測型在宅ケアを提供することと、仮想専門ケアサービスであるBiofourmis Careを複雑な慢性疾患を持つ患者に拡大することが含まれます。同時に、Biofourmisは臨床試験に資金を提供し、高価値の医薬品と連携して有効性を高め、デジタルヘルスおよびバーチャルファーストケアのエコシステムにおける企業との戦略的関係を構築するデジタル医薬品の開発を加速する予定です。このようなイノベーションは、予測期間中に市場を牽引すると予想されます。

したがって、上記の要因により、調査対象市場は分析期間中に大幅な成長を遂げると予想されます。ただし、病院の統合の問題とプライバシーの侵害につながるデータ侵害の可能性により、市場の成長が妨げられる可能性があります。

バーチャルケア市場の動向

在宅ヘルスケア部門は予測期間中に大幅な成長が見込まれる

在宅ヘルスケア部門は、予測期間中に大幅な成長が見込まれると予想されます。COVID-19の出現により、患者は徐々にバーチャルケアの概念を採用しつつあります。この概念は米国などの先進国ではすでに存在していますが、多くの新興諸国ではまだ新しいものです。新型コロナウイルス感染症(COVID-19)の発生により、バーチャルケアは、あらゆる年齢層の間で最も簡単で最も利用されている相談方法の1つとして浮上しました。

病院のベッド不足と診察待ち時間の多さが、物理的ケアからバーチャルケアへの動向の移行に大きく寄与しています。たとえば、英国の国民保健サービスは、2021年 12月に患者用のテクノロジー対応の仮想病棟の確立に関するガイドラインを発表しました。仮想病棟を使用すると、通常は入院する患者が急性期治療、遠隔監視、治療を受けることができます。彼らはケアホームを含む快適な自宅での生活を必要としています。同組織はさらに、テクノロジーによって、適切な情報を適切なタイミングで適切な人が利用できるようにすることで、組織が最前線で働く人々のストレスを軽減し、患者の転帰を向上させるのに役立つ可能性があると述べた。仮想病棟は、自宅で安全かつ適切に治療および監視できるさまざまな病気に適しています。多くのコミュニティでは、呼吸器疾患、心不全、虚弱関連疾患の急性増悪などのさまざまな患者のための仮想病棟を作成しているか、作成に取り組んでいます。さらに、仮想訪問では感染のリスクはありませんが、物理的な訪問ではリスクが比較的高くなります。したがって、このような事例は、在宅ヘルスケアセグメントが予測期間中に大幅な成長を遂げると予想されることを示しています。

予測期間中、北米がバーチャルケア市場を独占すると予想される

バーチャルケアモデルの採用の増加、企業の地理的範囲の拡大、バーチャルヘルスケアのスタートアップ企業の数の急増、主要な小規模企業によるサービス立ち上げの増加などの要因により、北米が市場を独占すると予想されています。この地域では。たとえば、2022年 2月、臨床医はカナダ初の子供向け仮想ケアサービス KixCareを開始しました。したがって、このような開発は、この地域の市場の成長を促進すると予想されます。

さらに、主要なサービスの開始、バーチャルケアに向けた政府の取り組み、米国における市場関係者や製造業者の集中度の高さなども、この国のバーチャルケア市場の成長を促進する要因の一部です。たとえば、2022年 2月に米国保健福祉省(HHS)が発行した報告書によると、HHSは地域医療センターを通じた仮想医療へのアクセスと質を向上させるために約5,500万米ドルを交付しました。この資金は、保健センターが最新のイノベーションと技術を導入して、十分なサービスを受けられていない地域社会のプライマリケア施設を拡張するのに役立ちます。同様に、CVS Healthは2022年 5月に、単一のデジタルプラットフォームからアクセスできる新しい仮想ケアソリューションであるCVS Health Virtual Primary Careを導入しました。より調整された消費者中心のヘルスケア体験を実現するために、このソリューションはCVS Healthのサービス、臨床専門知識、およびデータを統合します。したがって、そのような要因は、予測期間中に米国の市場の成長を推進すると予想されます。したがって、前述の要因により、調査対象市場は北米地域での成長が予想されます。

バーチャルケア業界の概要

バーチャルケア市場は、世界的および地域的に事業を展開する複数の企業が存在するため、本質的に細分化されています。競合情勢には、Teladoc Health, Inc.、American Well Corporation、Unitedヘルスケア Services, Inc.、CVS Health、MDLIVE、Medocity、 Inc.、Amazon.com, Inc.、VirtualHealth、General Electric Company、およびCerner Corporationなど。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- バーチャルケアを採用する患者数の増加とバーチャルケアへの政府の取り組み

- バーチャルケアのメリットと市場関係者による新サービス開始

- 市場抑制要因

- 医師のサポート不足とプライバシーへの懸念による病院統合の問題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(金額別の市場規模)

- 配送方法別

- ビデオ

- オーディオ

- メッセージング

- コンポーネント別

- ソリューション

- サービス

- エンドユーザー別

- 在宅ヘルスケア

- 病院

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Teladoc Health, Inc.

- American Well Corporation

- United HealthCare Services, Inc.

- CVS Health

- MDLIVE

- Medocity, Inc.

- Amazon.com, Inc.

- VirtualHealth

- General Electric Company

- Oracle Corporation(Cerner)

第7章 市場機会と将来の動向

The Global Virtual Care Market size is estimated at USD 12.84 billion in 2024, and is expected to reach USD 40.92 billion by 2029, growing at a CAGR of 26.10% during the forecast period (2024-2029).

The COVID-19 pandemic had a positive impact on the virtual care market. The pandemic has increased the adoption of virtual care assistance among people of all age groups. Initially, the concept of virtual care was restricted to certain age groups, such as youngsters. However, with the advent of COVID-19, the term "virtual care" gained significant prominence among all patients, irrespective of their age. For instance, as per the survey conducted by the Canadian Medical Association (CMA) in June 2020, during the COVID-19 crisis, 47% of Canadians used "virtual care" such as phone calls, emails, messages, or videos during the outbreak. Ninety-one percent indicated they were incredibly satisfied with their visit. The same source further stated that 34% of individuals who required advice during the pandemic contacted their doctor by phone. However, only 10% saw a doctor in person, 6% went to a walk-in clinic, and 5% went to an emergency department. Furthermore, according to Canada Health Infoway, about 4% of primary care visits in Canada were done remotely (by phone, video, text, or app) before the pandemic was declared. Therefore, such instances indicate the demand for virtual care solutions bolstered during the pandemic phase.

Furthermore, the mutual advantages offered by virtual care for both doctors and patients are one of the major factors driving the market's growth. Through virtual care, patients can undergo consultation from home. It also helps to bridge the gap between patient and doctor, as doctors can reach out to more patients virtually rather than through physical consultation. In addition, virtual care is much more inexpensive than physical consultation as no traveling costs or waiting time are involved. The rising adoption of virtual care has encouraged many key and small players to launch services related to virtual care. For instance, in November 2021, LifeMD launched its virtual care platform to enable affordable and accessible healthcare 24/7 to patients globally. Likewise, in April 2022, with a USD 300 million Series D investment led by growth equity company General Atlantic, Biofourmis, a pioneer in virtual care and digital medicine, achieved unicorn status. Biofourmis intends to expand its virtual care offerings with this financing. This involves providing individualized and predictive in-home care to an increasing number of acutely ill patients and expanding Biofourmis Care, its virtual specialist care service, to patients with complicated chronic diseases. Parallelly, Biofourmis intends to fund clinical trials to accelerate the development of digital medicines that collaborate with high-value medications to boost efficacy and build strategic relationships with firms in digital health and virtual-first care ecosystems. Such innovations are anticipated to drive the market over the forecast period.

Therefore, owing to the above-mentioned factors, the studied market is anticipated to witness considerable growth over the analysis period. However, hospital integration issues and the chances of data breaches leading to compromised privacy are likely to impede the market's growth.

Virtual Care Market Trends

Home Healthcare Segment is Expected to Witness Significant Growth Over the Forecast Period

The home healthcare segment is anticipated to witness significant growth over the forecast period. With the advent of COVID-19, patients are gradually adopting the virtual care concept. Although the concept already exists in developed countries such as the United States, it is still new in many developing countries. With the onset of COVID-19, virtual care has emerged as one of the easiest and most utilized modes of consultation among all age groups.

The lack of beds and high consultation waiting time in hospitals have majorly contributed to the shift of the physical to virtual care trend. For instance, the National Health Service in the United Kingdom published a guideline on establishing technology-enabled virtual wards for patients in December 2021. Virtual wards enable patients who would normally be admitted to the hospital to receive the acute care, remote monitoring, and therapy they require in the comfort of their own homes, including care homes. The organization further stated that by making the appropriate information available to the right people at the right time, technology might help organizations lessen the stress on frontline workers and enhance patient outcomes. Virtual wards are appropriate for a variety of illnesses that can be handled and monitored safely and successfully at home. Many communities have created or are working to create virtual wards for a variety of patients, including those with respiratory issues, heart failure, or acute exacerbations of a frailty-related ailment. In addition, there is no risk of getting any infections during virtual visits, while in physical visits, the risk is comparatively high. Therefore, such instances indicate that the home healthcare segment is expected to witness significant growth over the forecast period.

North America is Expected to Dominate the Virtual Care Market Over the Forecast Period

North America is expected to dominate the market owing to factors such as increasing adoption of virtual care models, expanding the geographical reach of the companies, a surge in the number of virtual healthcare start-ups, and growing service launches by key and small players operating in this region. For instance, in February 2022, Clinicians launched the first virtual care service, KixCare, for kids in Canada. Therefore, such developments are anticipated to propel the market's growth in this region.

Moreover, key service launches, government initiatives toward virtual care, and a high concentration of market players or manufacturers' presence in the United States are some of the other factors driving the growth of the virtual care market in the country. For instance, as per the report published by the US Department of Health & Human Services (HHS) in February 2022, HHS awarded around USD 55 million to increase virtual health care access and quality through community health care centers. The funding will help the health centers adopt the latest innovations and technologies to expand facilities for primary care for underserved communities. Likewise, in May 2022, CVS Health introduced CVS Health Virtual Primary Care, a new virtual care solution accessible via a single digital platform. For a more coordinated and consumer-centric health care experience, the solution integrates CVS Health's services, clinical expertise, and data. Hence, such factors are anticipated to propel the market growth in the United States over the forecast period. Therefore, owing to the aforementioned factors, the growth of the studied market is anticipated in the North American region.

Virtual Care Industry Overview

The virtual care market is fragmented in nature due to the presence of several companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international as well as local companies that hold the market shares and are well known, including Teladoc Health, Inc., American Well Corporation, United HealthCare Services, Inc., CVS Health, MDLIVE, Medocity, Inc., Amazon.com, Inc., VirtualHealth, General Electric Company, and Cerner Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Number of Patients Adopting Virtual Care and Government Initiatives Towards Virtual Care Access

- 4.2.2 Advantages Of Virtual Care and New Service Launches by Market Players

- 4.3 Market Restraints

- 4.3.1 Lack of Physician Support and Hospital Integration Issues Due to Privacy Concerns

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers and Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - in USD Million)

- 5.1 By Mode of Delivery

- 5.1.1 Video

- 5.1.2 Audio

- 5.1.3 Messaging

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.2 Services

- 5.3 By End Users

- 5.3.1 Home Healthcare

- 5.3.2 Hospitals

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Teladoc Health, Inc.

- 6.1.2 American Well Corporation

- 6.1.3 United HealthCare Services, Inc.

- 6.1.4 CVS Health

- 6.1.5 MDLIVE

- 6.1.6 Medocity, Inc.

- 6.1.7 Amazon.com, Inc.

- 6.1.8 VirtualHealth

- 6.1.9 General Electric Company

- 6.1.10 Oracle Corporation (Cerner)