|

市場調査レポート

商品コード

1689694

非乳製品アイスクリーム:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Non-dairy Ice Cream - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 非乳製品アイスクリーム:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 224 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

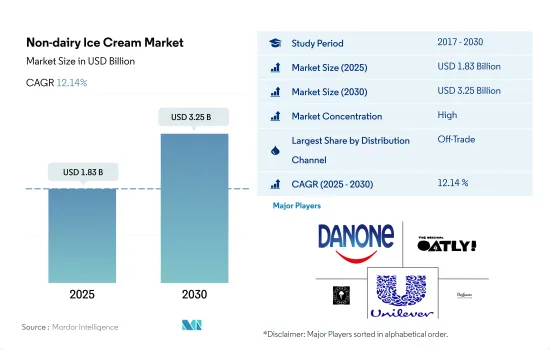

非乳製品アイスクリーム市場規模は2025年に18億3,000万米ドルと推定・予測され、2030年には32億5,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは12.14%で成長すると予測されます。

スーパーマーケットやオンラインショップを通じた大きな売上が、オフチャネルを通じたセグメント売上を押し上げています。

- 2020年には、小売食料品店(オフトレード)を通じてより多くの植物性アイスクリームを購入する消費者の大きな需要があり、15.68%の増加でした。非乳製品アイスクリームは、2020年と比較して2023年には全体として50.51%の成長率を示しました。これは近年の持続的な増加を示しており、店舗のあらゆる部分とオンラインプラットフォーム全体において、ブランドが利用できる素晴らしい機会があることを示しています。

- しかし、この地域にはオンチャネルの市場はあまりなく、未発達の段階にあります。消費者は植物性乳製品を一定量食べており、自宅で食べることを好み、レストランや外食店で食べることはあまりないです。消費者が従来の製品に代わるより良いものを見つけようとする中で、意識的で健康的な生活習慣へと消費者の嗜好が変化し、数多くの産業が影響を受けています。ヴィーガン文化の広がりとソーシャルメディアの影響力が重要な要因です。2021年4月現在、ヴィーガンフレンドリーレストランの割合が最も高いのはインドネシアのウブドで、同市を拠点とする全レストランの約38%がヴィーガン料理を提供しており、次いでスコットランドのエディンバラ(英国)が約33%となっています。

- オンラインチャネルは、オフトレードセグメントで最も急成長する流通チャネルになると予想されます。予測期間中のCAGRは18.25%と予測されています。より多くの食料品をオンラインで購入するようになった買い物客の61.1%にとって、利便性が主要動機となっています。この成長は、スマートフォンユーザーの増加によるもので、2023年には69億2,000万人、すなわち世界人口の86.29%に達すると予想されます。

北米と欧州における非乳製品アイスクリームの消費急増が市場を活性化

- 非乳製品アイスクリーム市場は、2021年と比較して2022年には17.7%の成長率を記録しました。消費者の健康志向とヴィーガンベース製品への嗜好の高まりが、世界の非乳製品アイスクリーム市場を牽引しています。

- 北米が非乳製品アイスクリーム市場を独占しています。2022年、同地域のシェアは55.3%を占め、非乳製品アイスクリームの販売額は2025年に33.5%の成長が見込まれます。植物性アイスクリームの人気が急上昇しているのは、乳製品を使わないデザートに対する消費者の関心が急増していることと、アクセスしやすさ、食感、風味の面でヴィーガンアイスクリームの提供が大幅に改善されていることに起因しています。

- 欧州は、乳製品不使用アイスクリームの販売で2番目に主要な地域です。欧州では、菜食主義者の数が増加しており、人口の半数以上がフレキシタリアンだと考えて肉の消費を減らしたいと考えています。2021年現在、同地域の菜食主義者は260万人で、人口の3.2%を占めています。同年、7,500万人近くの欧州の消費者がヴィーガン食品を購入しました。その結果、欧州における非乳製品アイスクリームの総販売額は、2021年の3億7,810万米ドルから2022年には4億7,902万米ドルに増加しました。

- アイスクリームパーラーの数が世界的に増加するにつれて、非乳製品アイスクリームの需要は予測期間中に伸びると予想されます。Baskin-Robbins、Dairy Queen、Haagen-Dazs、Wall'sは、世界中で営業している主要な非乳製品アイスクリーム販売店です。バスキン・ロビンスは世界最大のヴィーガンアイスクリーム専門店チェーンです。デイリークイーンは米国、カナダ、その他18カ国に6,000店舗以上を展開しています。

世界の非乳製品アイスクリーム市場の動向

健康への影響に対する意識の高まり、乳糖不耐症の増加、植物性食生活の普及、消費者の多忙なライフスタイルが、植物性アイスクリームや非乳製品代替品の需要を牽引しています。

- 菜食主義やベジタリアンのような植物ベースの食事は、世界的に増加傾向にあります。2022年には、回答したドイツの18~64歳の消費者の約3%が菜食主義を実践していました。ブラジル、中国、メキシコ、米国では、回答者の2%から6%が菜食主義者でした。

- 非乳製品アイスクリームは、フレキシタリアン、乳糖不耐症、厳格な菜食主義者の増加により、アメリカや欧州の消費者の間で人気を集めています。2022年、米国の非乳製品アイスクリームセグメントは2021年比で11.98%の成長を示しました。この成長は、肥満の結果に対する意識の高まりが、無脂肪または低脂肪食品への嗜好と消費の増加につながっていることに起因しています。同地域では2020年に11.98%の肥満の増加が観察されました。カナダでは、成人の肥満率は女性より男性の方が高い(それぞれ28.0%対24.7%)。世界的に、消費者の栄養選択に対する意識は高まっています。多忙なライフスタイルのため、消費者の購買決定は製品の栄養価に左右され、これが世界中の植物性アイスクリームの需要を牽引しています。消費者、特に牛乳アレルギーの人々は、植物性乳製品の摂取に熱心です。例えば、牛乳アレルギーは幼児によく見られる食物アレルギーのひとつです。日本の消費者の多くも乳糖不耐症で、牛乳や乳製品を摂取しないです。2022年現在、オーストラリアでは、乳幼児の約50人に1人が牛乳アレルギーの兆候を示しています。こうして、植物由来の乳製品への需要が徐々に高まっていりました。非乳製品アイスクリームの一人当たり消費量は、2023~2024年にかけて世界で13.27%増加しました。

非乳製品アイスクリーム産業概要

非乳製品アイスクリーム市場はかなり統合されており、上位5社で80.10%を占めています。この市場の主要企業は、Danone SA、Oatly Group AB、Oregon Ice Cream Company、Unilever PLC、Van Leeuwen Ice Creamです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原料/商品生産

- 代替乳製品-原料生産

- 規制の枠組み

- オーストラリア

- カナダ

- ドイツ

- メキシコ

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 流通チャネル

- オフ・トレード

- コンビニエンスストア

- オンライン小売

- 専門小売店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オフ・トレード

- 地域

- アジア太平洋

- 流通チャネル別

- オーストラリア

- 欧州

- 流通チャネル別

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- スペイン

- 英国

- その他の欧州

- 中東

- 流通チャネル別

- サウジアラビア

- アラブ首長国連邦

- 北米

- 流通チャネル別

- カナダ

- メキシコ

- 米国

- アジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Danone SA

- Nadamoo

- Oatly Group AB

- Oregon Ice Cream Company

- The Brooklyn Creamery

- Tofutti Brands Inc.

- Unilever PLC

- Van Leeuwen Ice Cream

- WildGood

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 67366

The Non-dairy Ice Cream Market size is estimated at 1.83 billion USD in 2025, and is expected to reach 3.25 billion USD by 2030, growing at a CAGR of 12.14% during the forecast period (2025-2030).

Significant sales through supermarkets and online stores are boosting the segment sales through off-trade channel

- There was a huge demand for consumers to purchase more plant-based ice cream through retail groceries (off-trade) in 2020, with an increase of 15.68%. The non-dairy ice cream showed an overall growth rate of 50.51% in 2023 compared to 2020. This illustrates a sustained increase over recent years and demonstrates the incredible opportunities available for brands in every part of the store and across online platforms.

- However, the region does not have a considerable market for the on-trade channel and is at an underdeveloped stage in the region. Consumers eat plant-based dairy in a definite amount, and they prefer to eat at home and are less likely to eat from a restaurant or foodservice outlet. Numerous industries are being impacted by the shift in consumer preference toward conscious and healthy lifestyle habits as consumers attempt to find better alternatives for conventional products. The spread of vegan culture and the influence of social media are the key factors. Ubud, Indonesia, had the highest percentage of vegan-friendly restaurants as of April 2021, with approximately 38% of all restaurants based in the city offering vegan cuisine, followed by Edinburgh, Scotland (UK), with around 33%.

- The online channel is expected to be the fastest-growing distribution channel in the off-trade segment. It is projected to register a CAGR of 18.25% during the forecast period. Convenience is the primary motivation for 61.1% of shoppers who have transitioned to shopping for more groceries online. This growth is due to the increasing number of smartphone users, which is expected to be 6.92 billion in 2023, i.e., 86.29% of the world's population.

Surging non-dairy ice cream consumption in North America and Europe is fueling the market

- The non-dairy ice cream market experienced a growth rate of 17.7% in 2022 compared to 2021. Consumers' inclination toward health consciousness and increasing preference toward vegan-based products is driving the global non-dairy ice cream market.

- North America dominates the non-dairy ice cream market. In 2022, the region accounted for 55.3% of the share, and the sales value of non-dairy ice cream is anticipated to grow by 33.5% in 2025. The surge in the popularity of plant-based ice cream can be attributed to burgeoning consumer interest in dairy-free desserts and the significant improvement in vegan ice cream offerings in terms of accessibility, texture, and flavor.

- Europe is the second leading region for the sales of non-dairy ice cream. In Europe, the number of vegans is growing, and more than half of the population wants to reduce meat consumption, considering themselves flexitarian. As of 2021, 2.6 million consumers in the region were vegans, representing 3.2% of the population. Nearly 75 million European consumers purchased vegan food in the same year. As a result, the total sales value of non-dairy ice cream in Europe increased from USD 378.1 million in 2021 to USD 479.02 million in 2022.

- As the number of ice cream parlors increases globally, the demand for non-dairy ice cream is anticipated to grow during the forecast period. Baskin-Robbins, Dairy Queen, Haagen-Dazs, and Wall's are some major non-dairy ice cream outlets operating worldwide. Baskin-Robbins is the world's largest chain of vegan ice cream specialty shops. As of 2022, it had more than 7,500 stores located in around 50 countries, while Dairy Queen had more than 6,000 outlets located in the United States, Canada, and 18 other countries.

Global Non-dairy Ice Cream Market Trends

The increasing awareness of health consequences, rise in lactose intolerance, growing adoption of plant-based diets, and busy lifestyles of consumers are driving the demand for plant-based ice cream and non-dairy alternatives

- A plant-based diet, such as veganism and vegetarianism, is becoming a growing trend globally. In 2022, around 3% of responding German consumers between 18 and 64 followed a vegan diet. In Brazil, China, Mexico, and the United States, between 2% and 6% of respondents were vegan.

- Non-dairy ice creams are gaining popularity among American and European consumers because of the rise in the population who are flexitarian, lactose-intolerant, or strict vegan. In 2022, the non-dairy ice cream segment of the United States witnessed a growth of 11.98% compared to 2021. The growth is attributed to the rising awareness about the consequences of obesity, which is leading to an increased preference for and consumption of non-fat or less-fat food products. The region observed growth in its obesity by 11.98% in 2020. In Canada, obesity rates in Canadian adults are higher in men than women (28.0% versus 24.7%, respectively). Globally, consumers are becoming increasingly aware of their nutritional choices. Owing to their busy lifestyles, their purchasing decision is dependent on the nutritional value of the product, which is driving the demand for plant-based ice cream worldwide. Consumers, especially those allergic to milk, are keen to consume plant-based milk products. For example, cow milk allergy is one of the common food allergies in young children. Many Japanese consumers are also lactose-intolerant and do not consume milk or milk products. As of 2022, in Australia, around 1 in 50 babies and young children showed signs of an allergy to cow's milk. Thus, the demand for plant-based dairy products increased gradually. The per capita consumption of non-dairy ice cream grew by 13.27% globally during 2023-2024.

Non-dairy Ice Cream Industry Overview

The Non-dairy Ice Cream Market is fairly consolidated, with the top five companies occupying 80.10%. The major players in this market are Danone SA, Oatly Group AB, Oregon Ice Cream Company, Unilever PLC and Van Leeuwen Ice Cream (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 Canada

- 4.3.3 Germany

- 4.3.4 Mexico

- 4.3.5 United Kingdom

- 4.3.6 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Distribution Channel

- 5.1.1 Off-Trade

- 5.1.1.1 Convenience Stores

- 5.1.1.2 Online Retail

- 5.1.1.3 Specialist Retailers

- 5.1.1.4 Supermarkets and Hypermarkets

- 5.1.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.1.1 Off-Trade

- 5.2 Region

- 5.2.1 Asia-Pacific

- 5.2.1.1 By Distribution Channel

- 5.2.1.2 Australia

- 5.2.2 Europe

- 5.2.2.1 By Distribution Channel

- 5.2.2.2 Belgium

- 5.2.2.3 France

- 5.2.2.4 Germany

- 5.2.2.5 Italy

- 5.2.2.6 Netherlands

- 5.2.2.7 Spain

- 5.2.2.8 United Kingdom

- 5.2.2.9 Rest of Europe

- 5.2.3 Middle East

- 5.2.3.1 By Distribution Channel

- 5.2.3.2 Saudi Arabia

- 5.2.3.3 United Arab Emirates

- 5.2.4 North America

- 5.2.4.1 By Distribution Channel

- 5.2.4.2 Canada

- 5.2.4.3 Mexico

- 5.2.4.4 United States

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Danone SA

- 6.4.2 Nadamoo

- 6.4.3 Oatly Group AB

- 6.4.4 Oregon Ice Cream Company

- 6.4.5 The Brooklyn Creamery

- 6.4.6 Tofutti Brands Inc.

- 6.4.7 Unilever PLC

- 6.4.8 Van Leeuwen Ice Cream

- 6.4.9 WildGood

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms