|

市場調査レポート

商品コード

1431546

オートバイローン:市場シェア分析、産業動向と統計、成長予測(2024~2029年)Motorcycle Loan - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オートバイローン:市場シェア分析、産業動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

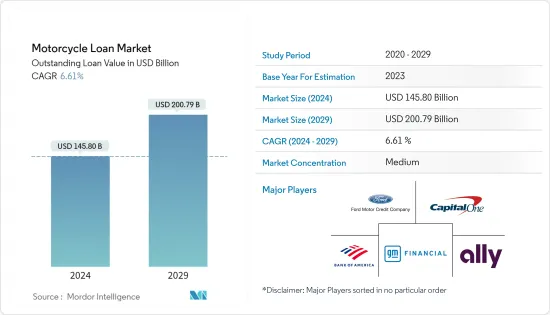

オートバイローン市場規模は、2024年の1,458億米ドルから2029年には2,007億9,000万米ドルに拡大し、予測期間(2024年~2029年)のCAGRは6.61%となる見込みです。

主なハイライト

- 二輪車は世界中の人々の生活において身近で重要な役割を果たしており、その用途は物資輸送などの純粋な実用性から、個人的な楽しみやスポーツまで多岐にわたっています。二輪車は多様な製品ラインナップによってこれらのニーズを満たしています。二輪車ローン市場は、さまざまな管轄地域の金融当局による規制の対象となっています。これらの規制は、消費者を保護し、公正な融資慣行を確保することを目的としています。規制要件には、金利に関するガイドライン、ローン条件の開示、借り手保護措置などが含まれる場合があります。

- オートバイ・ローン市場は、他の多くのセクターと同様、申込みと承認のプロセスを合理化するために、オンラインやデジタル・プラットフォームを採用しています。多くの貸金業者はオンライン・ローン申し込みを提供しており、借り手は自宅に居ながらにして申し込むことができます。デジタル・プラットフォームはまた、貸し手が事前承認の決定を提供し、より迅速なローン処理を提供することを可能にします。

- バイクローンを利用するには、一般的に一定レベルの信用力が必要です。貸し手は、信用履歴、収入の安定性、負債比率、借り手の返済能力などの要素を評価します。貸し手の基準を満たすことで、ローン承認の可能性が高まり、提示される金利に影響することもあります。

- オートバイ・ローンには通常、固定金利が適用され、返済期間は数ヶ月から数年に及ぶ。ローンの条件は、貸し手と借り手の信用度によって異なる場合があります。貸し手によっては、バルーン払いや借入期間の延長など、柔軟な返済オプションを提供している場合もあります。

- COVID-19は世界のサプライチェーンを混乱させ、二輪車の生産と供給力に影響を与えました。製造工場や流通網が一時的な閉鎖や遅延に直面し、新車二輪車の供給が減少しました。このため、オートバイの購入資金を調達しようとする借り手の選択肢が狭まった。

- パンデミックは消費者の行動や嗜好に影響を与えました。公共交通機関への不安や社会的距離の遠ざかりから、一部の個人は移動手段としてオートバイを含む自家用車にシフトしました。このような嗜好の変化は、二輪車の需要が回復するにつれて、二輪車ローン市場に新たな機会を生み出す可能性があります。

オートバイローン市場の動向

二輪車販売の増加が市場を牽引

- 二輪車の販売台数が増加すれば、二輪車の購入を検討する個人も増えます。購入希望者の多くは、二輪車購入に必要な資金を全額準備できないため、二輪車ローンのような資金調達手段を求めるようになります。販売台数が増えれば増えるほど、バイクローンの需要も高まる。

- 二輪車市場における販売台数の増加は、しばしば金融業者間の競争の激化につながります。顧客を惹きつけ、より大きな市場シェアを獲得するために、金融機関はより競争力のあるローン条件を提示することがあります。これには、金利の引き下げ、返済期間の延長、手数料の引き下げなどがあります。

- 競争は、消費者により有利なローンの選択肢や条件を提供することで利益をもたらします。オートバイ・ローンの需要が高まる中、貸金業者はローン申し込みの増加に対応するため、ローン・プロセスを合理化する可能性があります。

インドは二輪車市場最大の収益市場

- 二輪車産業における収益の増加は、多くの場合、二輪車の販売と需要の増加に対応します。二輪車の販売台数が増えれば、二輪車ローンなどの融資オプションのニーズも高まる。購入資金の全額を準備できない消費者は、希望するオートバイを購入するためにローンを利用します。このように、オートバイの販売台数の増加は、オートバイ・ローンの需要の増加につながります。

- アジア太平洋地域は、生産台数、販売台数ともに二輪車の最大市場となっています。中国、インド、インドネシア、ベトナムなどの国々は、人口が多く、都市化が急速に進み、手頃な価格の交通手段に対する需要が高いため、二輪車市場が大きいです。

- 金融機関や貸し手は、二輪車産業の収益と販売実績を注意深く監視しています。オートバイの売上が伸びれば、金融機関はこの市場セグメントに特化したローンの提供を拡大する可能性があります。二輪車購入用に特化したローン商品を開発し、競争力のある金利、柔軟な返済期間、魅力的な融資パッケージを提供することもあります。ローン提供の拡大は、消費者がオートバイの融資を求める際に、より幅広い選択肢を提供します。

オートバイ・ローン業界の概要

オートバイ・ローン市場は競争が激しく、様々な金融業者が顧客の獲得にしのぎを削っています。借り手を引き付けるため、金融機関は競合金利、柔軟な条件、付加価値サービスを提供することがあります。借り手は、複数の金融業者からの提案を比較して、自分のニーズに合った最良のローン条件を見つけることが推奨されます。

オートバイ・ローン市場には、銀行、信用組合、専門金融業者など、さまざまな金融機関が参入しています。銀行はクレジットヒストリーが良好な顧客にローンを提供することが多いが、専門金融機関はクレジットスコアが低い個人や特定のオートバイ関連融資オプションを求める人に対応することがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- オートバイ所有者の増加

- カスタマイズされたローンオプション

- 市場抑制要因

- 市場の飽和と競合

- モビリティ嗜好の変化

- 市場を形成する様々な規制動向に関する洞察

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 市場における技術の影響に関する洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 自動車タイプ別

- 二輪車

- 乗用車

- 商用車

- プロバイダータイプ別

- 銀行

- NBFC(非銀行金融サービス)

- OEM(相手先ブランド製造)

- その他(フィンテック企業)

- 認可額の割合別

- 25%未満

- 25-50%

- 51-75%

- 75%以上

- 支払い期間別

- 3年未満

- 3~5年未満

- 5年以上

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- ベトナム

- オーストリア

- その他アジア太平洋地域

- 中東・アフリカ

- サウジアラビア

- エジプト

- アラブ首長国連邦

- その他中東とアフリカ

- 南米

- アルゼンチン

- コロンビア

- その他南米

- 北米

第6章 競合情勢

- Market Concetration Overview

- 企業プロファイル

- Ally Financial Inc.

- Bank of American Corporation

- GM Financial Inc.

- Capital One Financial Corporation

- Ford Motor Credit Company

- Daimler Financial Services

- Mitsubishi HC Capital UK PLC

- General Motors Financial Company, Inc

- Toyota Financial Services

- JPMorgan Chase & Co.*

第7章 市場機会と今後の動向

第8章 免責事項と出版社について

The Motorcycle Loan Market size in terms of outstanding loan value is expected to grow from USD 145.80 billion in 2024 to USD 200.79 billion by 2029, at a CAGR of 6.61% during the forecast period (2024-2029).

Key Highlights

- Motorcycles play a familiar and vital role in the lives of people around the world, their applications spanning from the pure utility, such as the transportation of goods, to personal enjoyment and sports; motorcycles satisfy these needs with their diverse product line-up. The motorcycle loan market is subject to regulations imposed by financial authorities in different jurisdictions. These regulations aim to protect consumers and ensure fair lending practices. Regulatory requirements may include guidelines on interest rates, disclosure of loan terms, and borrower protection measures.

- The motorcycle loan market, like many other sectors, has embraced online and digital platforms to streamline the application and approval process. Many lenders provide online loan applications, allowing borrowers to apply from the comfort of their homes. Digital platforms also enable lenders to offer pre-approval decisions and provide faster loan processing.

- Obtaining a motorcycle loan generally requires a certain level of creditworthiness. Lenders assess factors such as credit history, income stability, debt-to-income ratio, and the borrower's ability to repay the loan. Meeting the lender's criteria increases the chances of loan approval and may also impact the interest rate offered.

- Motorcycle loans typically come with fixed interest rates and repayment terms that can range from a few months to several years. The terms and conditions of the loans may vary depending on the lender and the borrower's creditworthiness. Some lenders may also offer flexible repayment options, such as balloon payments or extended loan terms.

- The Covid 19 disrupted global supply chains, affecting the production and availability of motorcycles. Manufacturing plants and distribution networks faced temporary closures or delays, leading to a decrease in the supply of new motorcycles. This limited the options available for borrowers looking to finance their motorcycle purchases.

- The pandemic influenced consumer behavior and preferences. With concerns about public transportation and social distancing, some individuals shifted towards personal vehicles, including motorcycles, as a mode of transportation. This shift in preference could potentially create new opportunities in the motorcycle loan market as the demand for motorcycles rebounds.

Motorcycle Loan Market Trends

Increasing Sales of Motorcycles will Drive the Market

- When motorcycle sales increase, more individuals are looking to purchase motorcycles. Many potential buyers may not have the full amount of funds needed to purchase a motorcycle upfront, leading them to seek financing options such as motorcycle loans. The higher the sales volume, the greater the demand for motorcycle loans.

- Increased sales in the motorcycle market often lead to increased competition among lenders. To attract customers and capture a larger market share, lenders may offer more competitive loan terms. This can include lower interest rates, extended repayment periods, or reduced fees.

- The competition benefits consumers by providing them with more favorable loan options and terms. With the rising demand for motorcycle loans, lenders may streamline their loan processes to accommodate the increased volume of loan applications.

India is largest Revenue generating Market in Motorcycle Market

- Higher revenue in the motorcycle industry often corresponds to increased sales and demand for motorcycles. As more motorcycles are sold, the need for financing options, such as motorcycle loans, also rises. Consumers who may not have the full purchase amount available upfront turn to loans to afford their desired motorcycles. Thus, higher motorcycle revenue leads to increased demand for motorcycle loans.

- Asia-Pacific has emerged as the largest market for motorcycles, both in terms of production and sales. Countries like China, India, Indonesia, and Vietnam have significant motorcycle markets due to their large populations, rapid urbanization, and high demand for affordable transportation.

- Financial institutions and lenders closely monitor the revenue and sales performance of the motorcycle industry. As motorcycle revenue grows, lenders may expand their loan offerings to cater specifically to this market segment. They may develop specialized loan products tailored for motorcycle purchases, offering competitive interest rates, flexible repayment terms, and attractive financing packages. The expansion of loan offerings provides consumers with a wider range of options when seeking motorcycle financing.

Motorcycle Loan Industry Overview

The Motorcycle loan market is competitive, with various lenders vying for customers' business. To attract borrowers, lenders may offer competitive interest rates, flexible terms, and value-added services. Borrowers are encouraged to compare offers from multiple lenders to find the best loan terms and conditions for their needs.

Various financial institutions participate in the motorcycle loan market, including banks, credit unions, and specialized lenders. Banks often provide loans to customers with good credit histories, while specialized lenders may cater to individuals with lower credit scores or those seeking specific motorcycle-related financing options.

Following is the list companies that operate in this market: Ally Financial Inc., Bank of American Corporation, GM Financial Inc., Capital One Financial Corporation, Ford Motor Credit Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Motorcycle Ownership

- 4.2.2 Customized Loan Options

- 4.3 Market Restraints

- 4.3.1 Market Saturation and Competition

- 4.3.2 Changing Mobility Preferences

- 4.4 Insights on Various Regulatory Trends Shaping the Market

- 4.5 Industry Attractiveness - Porters' Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Insights on Impact of Technology in the Market

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Vehicle Type

- 5.1.1 Two-Wheeler

- 5.1.2 Passenger Car

- 5.1.3 Commercial Vehicle

- 5.2 By Provider Type

- 5.2.1 Banks

- 5.2.2 NBFCs (Non-Banking Financial Services)

- 5.2.3 OEM (Original Equipment Manufacturer)

- 5.2.4 Other Provider Types (Fintech Companies)

- 5.3 By Percentage of Amount Sanctioned

- 5.3.1 Less than 25%

- 5.3.2 25-50%

- 5.3.3 51-75%

- 5.3.4 More than 75%

- 5.4 By Tenure

- 5.4.1 Less than 3 Years

- 5.4.2 3-5 Years

- 5.4.3 More than 5 Years

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 USA

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 UK

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Vietnam

- 5.5.3.5 Austrilia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle-East and Africa

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 Egypt

- 5.5.4.3 UAE

- 5.5.4.4 Rest of Middle-East and Africa

- 5.5.5 South America

- 5.5.5.1 Argentina

- 5.5.5.2 Colombia

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concetration Overview

- 6.2 Company Profiles

- 6.2.1 Ally Financial Inc.

- 6.2.2 Bank of American Corporation

- 6.2.3 GM Financial Inc.

- 6.2.4 Capital One Financial Corporation

- 6.2.5 Ford Motor Credit Company

- 6.2.6 Daimler Financial Services

- 6.2.7 Mitsubishi HC Capital UK PLC

- 6.2.8 General Motors Financial Company, Inc

- 6.2.9 Toyota Financial Services

- 6.2.10 JPMorgan Chase & Co.*