|

市場調査レポート

商品コード

1683231

インダクタ・コア・ビーズ市場:市場シェア分析、産業動向、成長予測(2025~2030年)Inductors, Cores and Beads - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インダクタ・コア・ビーズ市場:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 121 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

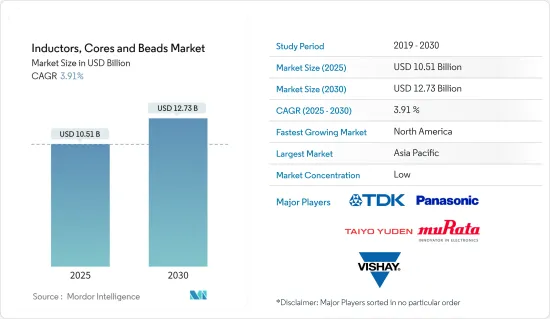

インダクタ・コア・ビーズ市場規模は2025年に105億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.91%で、2030年には127億3,000万米ドルに達すると予測されます。

SMDの新製品開発は、スマートフォン、モジュール、IoT端末向けの小型チップ、車載向けの高信頼性チップを中心に活発化しています。

主要ハイライト

- 電源密度と効率の向上は、インダクタ設計者の大半にとって課題です。ますます厳しくなる用途要件に対応するため、小型で高性能な電源ソリューションが絶えず求められています。

- 世界的には、スマートフォン、タブレット、ポータブルゲーム機、ノートパソコン、セットトップボックスなどの民生用電子機器の需要拡大が、各種インダクタ・コア・ビーズの需要を押し上げる大きな要因となっています。

- また、産業、航空宇宙・防衛、医療セグメントなど、高い信頼性が要求される用途からの需要も増加しています。

インダクタ・コア・ビーズ市場動向

民生用電子機器が大きな市場シェアを占める

- スマートフォンの約15%はセラミックとガラスで作られており、熱管理用の回路基板にインダクタ、ヒューズ、抵抗器などの受動部品のコアが使われています。

- モノのインターネットと5Gネットワークは、デバイスとネットワーク、IoT、自律走行、M2M間の情報通信の全体的な速度と効率を高めると予想されます。

- 民生用電子製品のほとんどは高出力機器であり、その電力は百から数キロワットに及びます。採用される磁気部品の量は、充電パイルの電力に依存します。充電パイルには平均して20個の磁性部品が必要で、その中でもインダクタの使用量が多いです。

- 課題は依然としてチップ面積の大きさです。例えば、Intelは、マルチコアプロセッサの電源管理用DC-DCコンバータで使用されるオンチップインダクタは、利用可能なチップ総面積の約4分の1を占め、コスト高になると述べています。

北米が大きな市場シェアを占める

- 米国では、車載用電子機器でのインダクタの使用が拡大し、スマートグリッド技術の採用が増加しています。さまざまな用途があるため、インダクタは多くの電子システムの主要部品のひとつとなっています。幅広い用途があるため、北米のいくつかの産業でより多くのインダクタが応用されています。

- 米国の公益企業は2016年、発電、送電、配電インフラに約1,440億米ドルを投資しました。IEAによると、米国のスマートグリッドインフラへの投資は2018年に126億米ドルに達しました。

- インダクタ・コア・ビーズの用途は、低消費電力と多機能適応性から、最新のアダプティブLEDヘッドライトに用途が見出されており、これらは従来のハロゲンやHIDヘッドライト、ADAS、自動車点火システムなどに置き換わっています。

- 2018年の米国の自動車生産台数は113億1,000万台、カナダの自動車生産台数は202万台です。

- 米国が2,000億米ドルの中国製品に対する輸入関税を引き上げたことで、電子部品産業はさらに影響を受けました。

インダクタ・コア・ビーズ産業概要

インダクタ・コア・ビーズ市場機会は激しい競合をもたらしました。かなりの数のメーカーが市場シェアの拡大を争っています。同市場は、より高いインダクタンスを達成するために、小型化し、コアの形態を変化させるという形で、技術革新の高まりを確認しています。

- 2019年9月-TDKは、厳しい車載環境に対応するメタルコアパワーインダクタを発表。

- 2019年6月-TDKは、モバイル機器設計に特化した薄膜パワーインダクタを発売し、従来製品より4%高い電流と12%低い抵抗に対応。

- 2019年6月-Kemet Corporationは、ノートブックコンピュータ、タブレット、サーバー、HDTVなど、さまざまな商用と民生用用途で利用されるDC-DCコンバータの最新パワー用途に適したSMDメタル複合材料パワーインダクタの新シリーズを発売しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 市場促進要因と市場抑制要因の導入

- 市場促進要因

- 市場抑制要因

第5章 市場セグメンテーション

- インダクタタイプ別

- パワーインダクタ

- 多層チップインダクタ

- RFインダクタ

- その他インダクタタイプ

- 芯材別

- エアーコア

- フェライトコア

- セラミックコア

- その他のコアタイプ

- チップビーズ別

- 多層ビーズ

- フェライトビーズ

- EMIビーズ

- エンドユーザー産業別

- 自動車

- コンピューティング

- 通信機器

- コンシューマー・エレクトロニクス

- その他

- 地域

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- TDK Corporation

- Vishay International Inc.

- Panasonic Corporation

- Murata Manufacturing Co. Ltd.

- Taiyo Yuden Co. Ltd.

- Kemet Corporation

- AVX Corporation

- Texas Instruments

- TT Electronics Plc

- Hefei MyCoil Technology Co., Ltd.

第7章 投資機会

第8章 市場機会と今後の動向

The Inductors, Cores and Beads Market size is estimated at USD 10.51 billion in 2025, and is expected to reach USD 12.73 billion by 2030, at a CAGR of 3.91% during the forecast period (2025-2030).

New product development of SMDs are gaining momentum, centering on small chips for smartphones, modules, and IoT terminals, and high-reliability chips for automotive application.

Key Highlights

- The increasing power supply density and efficiency is a challenge for most of the inductor designers. There is a continuous need for reduced size and high-performance power solutions to meet increasingly stringent application requirements.

- Globally, the growing demand for consumer electronics, such as smartphones, tablets, portable gaming consoles, laptops, set-top boxes, among others, is the major factor driving the demand for various inductors, core and beads.

- The market is also witnessing a boost in demand from applications, which require high reliability, in the industrial, aerospace and defense, and medical sectors.

Inductors Cores & Beads Market Trends

Consumer Electronic to Witness a Significant Market Share

- Around 15 percent of a smartphone is made from ceramics and glass that is from electronic applications with circuit boards for thermal management employs cores of passive components like inductors, fuses or resistors.

- The Internet of Things and 5G network is expected to boost the overall speed and efficiency of communicating information between devices and networks, IoT, autonomous driving and M2M performances.

- Most of consumer electronic products are high-power devices, and the power ranges from hundred to several kilowatts.The amount of magnetic components employed depends on the power of the charging pile. On an average, 20 magnetic components are required in a charging pile, of which the inductor is used in a larger amount.

- The challenge remains the large chip area utilisation. For instance, Intel stated that the on-chip inductors used in their DC-DC converters for power management in multi-core processors occupy approximately a quarter of the total available chip area, which made them costly.

North America to Hold a Significant Market Share

- The United States witnesses a growing use of inductors in automotive electronics and increasing adoption of smart grid technologies. Due to their various applications, inductors are one of the primary components of many electronic systems. Because of the extensive usage, more inductors are being applied in several industries across North America.

- U.S. utilities invested approximately USD 144 billion in electricity generation, transmission, and distribution infrastructure in 2016. According to IEA, U.S. investments in smart grids infrastructure stood at USD 12.6 billion in 2018.

- The application of inductors, core and beads find their applications in modern adaptive LED headlights because of their low power consumption and multifunctional adaptability, these are replacing conventional halogen and HID headlights, ADAS, automotive ignition systems, among others.

- The Unites States automotive production in 2018 stands at 11.31 billion cars and commercial vehicles and Canada's automotive production at 2.02 miliion cars and commericial vehicles, as per OICA.

- The region expects a gradual ease in China-US trade spats after May of 2019, when the United States raised import tariffs on USD 200 billion of Chinese goods, which further affected the electronic component industry.

Inductors Cores & Beads Industry Overview

The inductor, cores and beadsmarket's opportunities have resulted in intense competition. There are a significant number of manufacturers vying for the increasing market share. The market witnesses increased innovation in the form of reduced size and varying the form of cores to achieve higher inductance.

- September 2019 - TDK introduced metal-core power inductors tomeet the tough conditions forharsh automotive environments, these conductors have a wide operating temperature range from -55 °C up to +155 °C.

- June 2019 -TDK launched a Thin-Film Power Inductor specifically for Mobile Device Design tohandle 4% higher currents and 12% lower resistance than conventional products.

- June 2019 - Kemet Corporation launched new range of SMD metal composite power inductors to suit modern power applications inDC-DC converters that are utilized in a variety of commercial and consumer applications including notebook computers, tablets, servers and HDTVs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Force Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Introduction to Market Drivers and Restraints

- 4.4 Market Drivers

- 4.5 Market Restraints

5 MARKET SEGMENTATION

- 5.1 By Inductor Type

- 5.1.1 Power Inductors

- 5.1.2 MultiLayer Chip Inductors

- 5.1.3 RF Inductors

- 5.1.4 Other Inductor Types

- 5.2 By Core Material

- 5.2.1 Air Core

- 5.2.2 Ferrite Core

- 5.2.3 Ceramic Core

- 5.2.4 Other Core Types

- 5.3 By Chip Beads

- 5.3.1 MultiLayered Beads

- 5.3.2 Ferrite Beads

- 5.3.3 EMI Beads

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Computing

- 5.4.3 Communications

- 5.4.4 Consumer Electronics

- 5.4.5 Other End-User Industries

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia Pacific

- 5.5.4 Latin America

- 5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 TDK Corporation

- 6.1.2 Vishay International Inc.

- 6.1.3 Panasonic Corporation

- 6.1.4 Murata Manufacturing Co. Ltd.

- 6.1.5 Taiyo Yuden Co. Ltd.

- 6.1.6 Kemet Corporation

- 6.1.7 AVX Corporation

- 6.1.8 Texas Instruments

- 6.1.9 TT Electronics Plc

- 6.1.10 Hefei MyCoil Technology Co., Ltd.