|

市場調査レポート

商品コード

1773447

ワインおよびグレープマストの市場機会と成長促進要因、産業動向分析、2025年~2034年予測Wine and Grape Must Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ワインおよびグレープマストの市場機会と成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月23日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

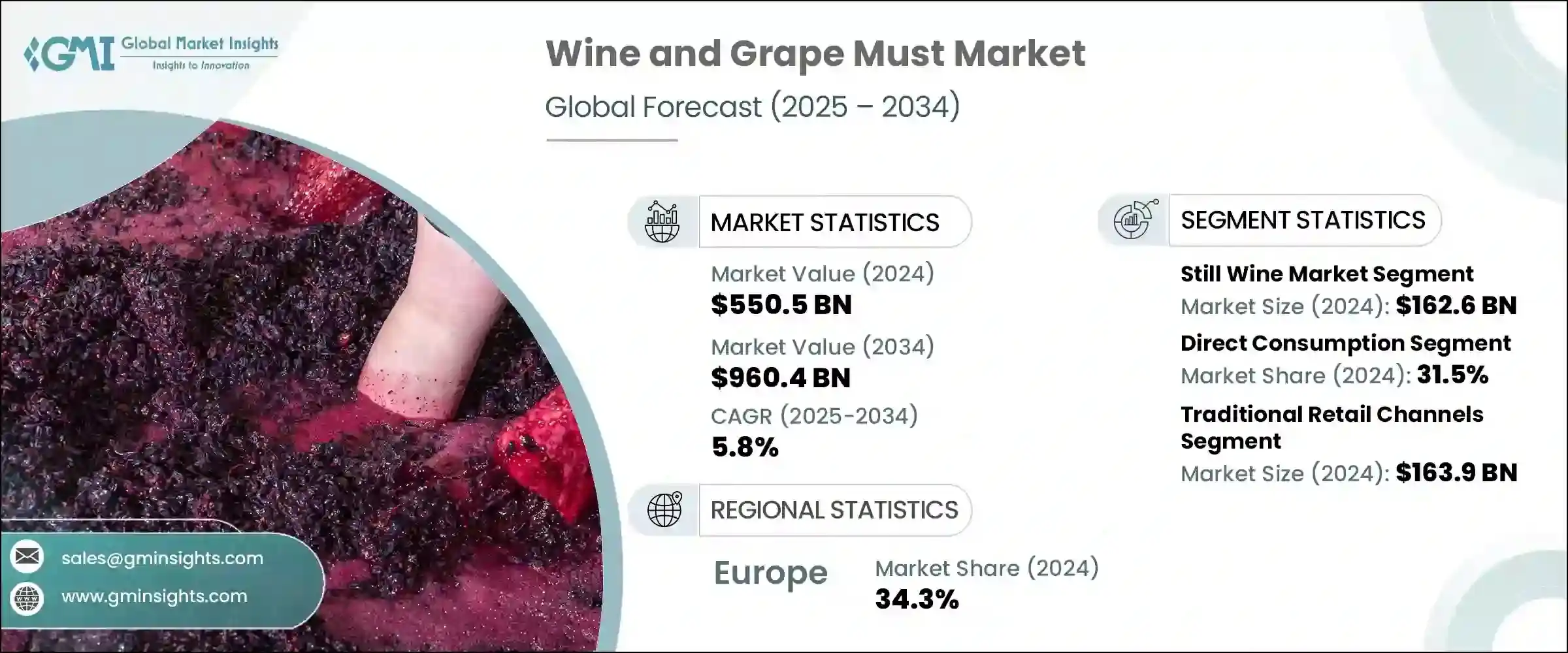

世界のワインおよびグレープマスト市場は、2024年には5,505億米ドルとなり、CAGR 5.8%で成長し、2034年には9,604億米ドルに達すると推定されます。

より多くの消費者がプレミアムで持続可能な方法で生産された飲料に傾倒しているため、高品質で職人的なワインに対する世界の旺盛な需要が引き続き市場拡大を牽引しています。ブドウ栽培技術の進化と気候適応性の向上により、収穫量とブドウの品質が向上し、この分野の安定した成長を支えています。健康志向や環境に配慮したライフスタイルへのシフトが進む中、消費者はオーガニックやバイオダイナミック、地元産のブドウを好む傾向が強まっています。

オンライン小売や消費者直販チャネルの影響力が高まったことで、プレミアムなワインおよびグレープマストがこれまで以上に身近なものとなり、世界市場全体の成長がさらに加速しています。さらに、缶やリサイクル可能なボトルなどの革新的なパッケージ形態は、環境負荷を低減しながら利便性を高め、持続可能性を重視する購買層にアピールしています。本物志向、クリーンラベルの動向、地域の特色は、今や主要なセールスポイントであり、購入者は一口飲むごとに本物の体験を求めるようになっています。このような直接消費の動向は、ブランドとエンドユーザーとのつながりを再構築し、よりパーソナライズされた透明性の高い関わりを提供しています。市場の変革は、あらゆるタッチポイントにおけるプレミアム品質、トレーサビリティ、持続可能性に対する消費者の期待によって主導されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 5,505億米ドル |

| 予測金額 | 9,604億米ドル |

| CAGR | 5.8% |

2024年のスティルワイン部門の売上高は1,626億米ドルで、29.5%のシェアを占める。この分野は、地域の特色があり、オーガニックで持続可能な、魅力的な背景を持つセレクションへの需要が高まるにつれて、成長を続けています。スパークリングワインも、特に開発途上地域で人気が高まっており、贅沢と祝賀の象徴と見なされ、向上心のある消費者の動向と一致しています。酒精強化ワインは、伝統的な品種や、クラフトカクテル文化や高級レストランに関連するハイエンドなオプションへの新たな関心に支えられ、愛好家の間でニッチな人気を維持しています。

直接消費分野は2024年に31.5%のシェアを占め、2034年までのCAGRは5.2%と予測されます。より多くの消費者が、新鮮で自然に生産され、最小限の加工しか施されていないワインやブドウ果汁を好むようになり、この消費形態は牽引力を増しています。ワインおよびグレープマストのユニークな味覚プロファイルと自然な健康増進特性が料理や機能性製品に活用され、より幅広い飲食品用途で需要が急増しています。消費者が食べ物や飲み物の中身をより意識するようになるにつれ、自然発酵やクリーンラベルの商品は、カテゴリーを問わず魅力的になってきています。

欧州ワインおよびグレープマスト2024年の市場シェアは34.3%。この地域は、品質に対する長年の定評と、地理的アイデンティティとオーガニック認証のあるワイン生産へのコミットメントにより、世界的リーダーであり続けています。気候に左右されるブドウ栽培の実践と地域のストーリー性が、欧州ワインの魅力をさらに高めています。北米では、持続可能性と少量生産の革新が重要な原動力となっており、特に健康志向の製品ラインではブドウの需要が伸びています。その他では、東南アジア、南米、中国の市場が急速に拡大しており、古くからの伝統と革新的な技術を組み合わせて、生産と消費の両方を伸ばしています。地域の多様性は、業界の世界的成長の特徴になりつつあります。

世界のワインおよびグレープマスト業界の競合ダイナミクスを形成している主要企業には、トレジャリー・ワイン・エステーツ、ザ・ワイン・グループ、E.&J.ガロ・ワイナリー、コンステレーション・ブランズ、ペルノ・リカールなどがあります。ワインとブドウのセクターでは、持続可能な生産方法、プレミアム製品の開発、消費者との直接的な関係に投資する企業が増えています。原産地、オーガニック認証、自然な製法を重視する目の肥えた消費者に対応するため、トレーサビリティと信憑性が重視されています。ブランドはデジタル・プラットフォームとeコマースを活用してパーソナライズされた体験を創造し、消費者が限定商品にアクセスしやすくしています。新興市場に戦略的に進出することで、企業は新たな顧客層を開拓し、パッケージの継続的な革新は環境目標をサポートします。また、多くのブランドが、地域の伝統やワイン造りの伝統にまつわるストーリーテリングを強化し、消費者とより強い感情的なつながりを築いています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- スティルワイン市場

- 赤ワインセグメント

- プレミアム赤ワイン

- 中級赤ワイン

- バリュー赤ワイン

- 白ワインセグメント

- プレミアム白ワイン

- 中級白ワイン

- バリュー白ワイン

- ロゼワインセグメント

- 赤ワインセグメント

- スパークリングワイン市場

- シャンパンとプレミアムスパークリング

- プロセッコと中級スパークリング

- バリュースパークリングワイン

- 強化ワイン市場

- ポートワインとシェリー酒

- ベルモットと食前酒

- その他の強化ワイン

- グレープマスト市場

- 生鮮グレープマスト

- 濃縮グレープマスト

- 精留濃縮グレープマスト

- オーガニックグレープマスト

- スペシャルティワインと代替ワイン製品

- オーガニックワインとバイオダイナミックワイン

- 低アルコールワインとノンアルコールワイン

- 缶詰および代替包装

- プライベートラベルワイン

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 直接消費

- 店内飲食(レストラン、バー、ホテル)

- 店外消費(小売店、スーパーマーケット)

- 消費者への直接販売

- 食品・飲料業界向けアプリケーション

- 料理用ワインと料理への応用

- 飲料のブレンドとフレーバー

- 食品加工および製造

- 産業用途

- 医薬品および栄養補助食品としての使用

- 化粧品およびパーソナルケア用途

- 化学および工業処理

- ブドウ果汁の特定の用途

- ワイン醸造と発酵

- 食品・菓子類業界

- 健康食品およびサプリメントの製造

- 従来および文化的用途

第7章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 従来の小売チャネル

- スーパーマーケットとハイパーマーケット

- ワイン専門店

- コンビニエンスストア

- デパート

- オンプレミスチャネル

- レストランと高級レストラン

- バーやパブ

- ホテルとホスピタリティ

- ワインバーとテイスティングルーム

- 直接販売チャネル

- ワイナリー直販

- ワインクラブとサブスクリプション

- セラードアセール

- ワイン観光とテイスティング体験

- eコマースとデジタルチャネル

- オンラインワイン小売業者

- マーケットプレースプレイスプラットフォーム

- モバイルアプリケーション

- ソーシャルコマース

- 卸売・流通

- 従来の3層システム

- 専門ワイン販売業者

- インポート/エクスポートチャネル

- ブローカーネットワーク

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- E. &J. Gallo Winery

- Constellation Brands, Inc.

- Treasury Wine Estates

- Pernod Ricard

- The Wine Group

- Castel Group

- Accolade Wines

- Caviro Group

- Freixenet Group

- Changyu Pioneer Wine Company

- Great Wall Wine Company

- Dynasty Fine Wines Group

- Suntory Holdings

- Sapporo Holdings

The Global Wine and Grape Must Market was valued at USD 550.5 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 960.4 billion by 2034. Strong global demand for high-quality and artisanal wine continues to drive market expansion, as more consumers gravitate toward premium, sustainably produced beverages. Evolving viticulture techniques and improved climate adaptability have enhanced both yield and grape quality, supporting consistent growth in this space. Consumers are showing stronger preferences for organic, biodynamic, and locally crafted options, driven by an increasing shift toward health-aware and environmentally responsible lifestyles.

The rising influence of online retail and direct-to-consumer distribution channels has made premium wine and grape must more accessible than ever, further accelerating growth across global markets. In addition, innovative packaging formats such as cans and recyclable bottles are appealing to sustainability-minded buyers, enhancing convenience while reducing environmental impact. Authenticity, clean-label trends, and regional character are now major selling points, as buyers seek genuine experiences with every sip. This direct consumption trend is reshaping how brands connect with end-users, offering a more personalized and transparent engagement. The market's transformation is being led by consumer expectations for premium quality, traceability, and sustainability across all touchpoints.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $550.5 Billion |

| Forecast Value | $960.4 Billion |

| CAGR | 5.8% |

In 2024, the still wine segment generated USD 162.6 billion, claiming a 29.5% share. This segment continues to thrive as demand rises for regionally distinct, organic, and sustainable selections with compelling backstories. Sparkling wine is also gaining popularity, especially in developing regions, where it is seen as a symbol of luxury and celebration, aligning with aspirational consumer trends. Fortified wine remains a niche favorite among enthusiasts, supported by renewed interest in heritage varieties and high-end options connected to craft cocktail culture and fine dining.

The direct consumption segment represented a 31.5% share in 2024 and projected to grow at a CAGR of 5.2% through 2034. This mode of consumption is experiencing increased traction as more consumers favor wines and grape must that are fresh, naturally produced, and minimally processed. There is a notable surge in demand for wine and grape must in broader food and beverage applications, where their unique taste profiles and natural health-enhancing qualities leveraged in culinary and functional products. As consumers become more aware of what goes into their food and drinks, naturally fermented and clean-label offerings are becoming more attractive across categories.

Europe Wine and Grape Must Market held a 34.3% share in 2024. The region remains a global leader due to its long-established reputation for quality and its commitment to producing wines with geographic identity and organic certification. Climate-driven viticultural practices and regional storytelling further enhance the appeal of European wines. In North America, sustainability and small-batch innovation are key drivers, while demand for grapes is growing, especially in wellness-oriented product lines. Elsewhere, markets in Southeast Asia, South America, and China are rapidly expanding, combining age-old traditions with innovative technology to grow both production and consumption. Regional diversity is becoming a hallmark of the industry's global growth.

Key players shaping the competitive dynamics of the Global Wine and Grape Must Industry include Treasury Wine Estates, The Wine Group, E. & J. Gallo Winery, Constellation Brands, Inc., and Pernod Ricard. Companies within the wine and grape sector are increasingly investing in sustainable production practices, premium product development, and direct consumer relationships. Emphasis is placed on traceability and authenticity to cater to a discerning audience that values origin, organic certification, and natural methods. Brands are leveraging digital platforms and e-commerce to create personalized experiences, making it easier for consumers to access exclusive products. Strategic expansion into emerging markets allows companies to tap into new customer bases, while continuous innovation in packaging supports environmental goals. Many are also enhancing storytelling around regional heritage and winemaking traditions to build stronger emotional connections with their audiences.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Still wine market

- 5.2.1 Red wine segment

- 5.2.1.1 Premium red wine

- 5.2.1.2 Mid-range red wine

- 5.2.1.3 Value red wine

- 5.2.2 White wine segment

- 5.2.2.1 Premium white wine

- 5.2.2.2 Mid-range white wine

- 5.2.2.3 Value white wine

- 5.2.3 Rose wine segment

- 5.2.1 Red wine segment

- 5.3 Sparkling wine market

- 5.3.1 Champagne and premium sparkling

- 5.3.2 Prosecco and mid-range sparkling

- 5.3.3 Value sparkling wine

- 5.4 Fortified wine market

- 5.4.1 Port and sherry

- 5.4.2 Vermouth and aperitifs

- 5.4.3 Other fortified wines

- 5.5 Grape must market

- 5.5.1 Fresh grape must

- 5.5.2 Concentrated grape must

- 5.5.3 Rectified concentrated grape must

- 5.5.4 Organic grape must

- 5.6 Specialty and alternative wine products

- 5.6.1 Organic and biodynamic wines

- 5.6.2 Low and No-alcohol wines

- 5.6.3 Canned and alternative packaging

- 5.6.4 Private label wines

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Direct consumption

- 6.2.1 On-premise consumption (restaurants, bars, hotels)

- 6.2.2 Off-premise consumption (retail, supermarkets)

- 6.2.3 Direct-to-consumer sales

- 6.3 Food and beverage industry applications

- 6.3.1 Cooking wine and culinary applications

- 6.3.2 Beverage blending and flavoring

- 6.3.3 Food processing and manufacturing

- 6.4 Industrial applications

- 6.4.1 Pharmaceutical and nutraceutical uses

- 6.4.2 Cosmetic and personal care applications

- 6.4.3 Chemical and industrial processing

- 6.5 Grape must specific applications

- 6.5.1 Winemaking and fermentation

- 6.5.2 Food and confectionery industry

- 6.5.3 Health food and supplement manufacturing

- 6.5.4 Traditional and cultural uses

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Traditional retail channels

- 7.2.1 Supermarkets and hypermarkets

- 7.2.2 Specialty wine stores

- 7.2.3 Convenience stores

- 7.2.4 Department stores

- 7.3 On-premise channels

- 7.3.1 Restaurants and fine dining

- 7.3.2 Bars and pubs

- 7.3.3 Hotels and hospitality

- 7.3.4 Wine bars and tasting rooms

- 7.4 Direct sales channels

- 7.4.1 Winery direct-to-consumer

- 7.4.2 Wine clubs and subscriptions

- 7.4.3 Cellar door sales

- 7.4.4 Wine tourism and tasting experiences

- 7.5 E-commerce and digital channels

- 7.5.1 Online wine retailers

- 7.5.2 Marketplace platforms

- 7.5.3 Mobile applications

- 7.5.4 Social commerce

- 7.6 Wholesale and Distribution

- 7.6.1 Traditional three-tier system

- 7.6.2 Specialized wine distributors

- 7.6.3 Import/Export channels

- 7.6.4 Broker networks

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 E. & J. Gallo Winery

- 9.2 Constellation Brands, Inc.

- 9.3 Treasury Wine Estates

- 9.4 Pernod Ricard

- 9.5 The Wine Group

- 9.6 Castel Group

- 9.7 Accolade Wines

- 9.8 Caviro Group

- 9.9 Freixenet Group

- 9.10 Changyu Pioneer Wine Company

- 9.11 Great Wall Wine Company

- 9.12 Dynasty Fine Wines Group

- 9.13 Suntory Holdings

- 9.14 Sapporo Holdings